Skip to content

Skip to content What is a PFIC?

PFICs is a really complex area of international tax law. Special care is needed. For those who are new to this topic? Please scroll down to read my article below.

If however, you are a more sophisticated investor, we discuss PFICs in the context of

1. Australia funds –

– https://htj.tax/2021/07/us-taxation-of-australian-superannuation-funds/

2. UK or United Kingdom or Great Britain or England based funds –

– https://htj.tax/2017/06/do-i-have-to-annually-report-pfics-held/

3. Angel investor or fund manager or international investor using a foreign company holding company structure

– https://htj.tax/2021/07/us-investors-in-foreign-companies-that-turn-into-pfics/

– https://htj.tax/2021/08/qef-election-for-pfics-election-to-extend-the-time-for-payment-of-tax-on-undistributed-earnings-of-a-qualified-electing-fund-temporary/

– https://htj.tax/2014/02/avoiding-sting-of-pfic-classification/

4. Into Bitcoin on foreign exchanges? Crypto trader or crypto investor –

– https://htj.tax/2021/10/tax-efficient-trading-structures-for-us-exposed-crypto-traders/

– https://htj.tax/2021/07/us-investors-in-foreign-companies-that-turn-into-pfics/

5. We can help you mitigate or at least minimize their impact –

– https://htj.tax/2014/02/avoiding-sting-of-pfic-classification/

– https://htj.tax/2021/10/tax-efficient-trading-structures-for-us-exposed-crypto-traders/

– https://htj.tax/2021/08/qef-election-for-pfics-election-to-extend-the-time-for-payment-of-tax-on-undistributed-earnings-of-a-qualified-electing-fund-temporary/

We are the PFIC experts. Email us on help@htj.tax today

While many portions of the U.S. tax code possess confusing and sometimes harsh rulings, the tax regime for Passive Foreign Investment Companies (PFIC) is almost unmatched in its complexity and almost draconian features. Countless times, our international clients have come to us to prepare what they thought would be straightforward tax returns- only to later learn that the small investment they had made in a non-US mutual fund was now subjecting them to all the concomitant filing requirements and tax obligations. While it is beyond the scope of this article to cover all the numerous details related to PFIC reporting requirements, my hope is to provide guidance and insight into the world of PFICs.

History

The PFIC tax regime was created via the Tax Reform Act of 1986 with the intent to level the playing field for US based investment funds (ie mutual funds). Prior to the legislation of 1986, U.S.-based mutual funds were forced to pass-through all investment income earned by the fund to its investors (resulting in taxable income). In contrast, foreign mutual funds were able to shelter the aforementioned taxable income as long as it was not distributed to its U.S. investors. After the passage of the Tax Reform Act of 1986, the main advantage of foreign mutual funds was effectively nullified by a tax regime that made the practice of delaying the distribution of income prohibitively expensive for most investors. To employ this punitive regime, the IRS requires shareholders of PFICs to effectively report undistributed earnings via choosing to be taxed through one of three possible methods- Section 1291 fund, Qualified Election Fund, and Mark to Market election.

Basics

Defined in the Internal Revenue Code (section 1297), a Passive Foreign Investment Company is any foreign corporation that has either:

1. 75% or more of its gross income classified as passive income (i.e. interest, dividends, capital gains, etc…),

or

2. 50% or more of its assets are held for the production of passive income.

While there are a few exceptions to above rules, most foreign mutual funds, pension funds, and money market accounts would be good examples of PFICs. Furthermore, many foreign REITS also get trapped in the PFIC web. Finally, a foreign holding company that possesses passive investments (like rental real estate or government bonds) would be subject to PFIC regulations if the company was set up as a corporation.

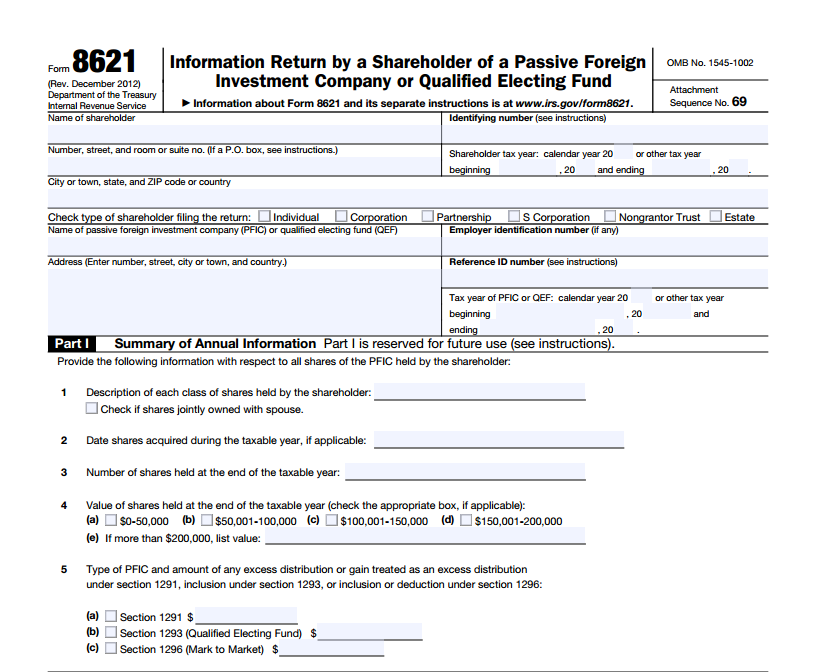

PFIC related information is reported on Form 8621 .

Taxation Methods

Section 1291 Fund

The Section 1291 Fund election (Excess Distribution) is the default taxation regime unless the taxpayer chooses either of the two alternatives. Under the Sect 1291 regime, all “excess distributions” for prior years will be taxed at the highest marginal rate for each particular year an excess occurred and will incur underpayment interest expenses on those unpaid taxes. In contrast, the current year “excess distributions” are added to the “Other income” line of one’s personal tax return. For the purposes of this election an “excess distributions” are either:1. The part of the distribution received from a section 1291 fund in the current tax year that isgreater than 125% of the average distributions received in respect to such stock by the shareholder during the 3 preceding tax years (or, if shorter, the portion of the shareholder’s holding period before the current tax year; or2. Any capital gains that result from the sale of PFIC sharesTo add to the complexity- excess distributions that are taken (in either of the two aforementioned forms) must be allocated ratably over every year since the most recent excess distribution was taken (if any). Furthermore, all dividends are still required to be reported on Schedule B of the income tax return but any capital gains or losses do not get reported on Schedule D.

To provide an illustration:1 share of XYZ Inc. (a foreign mutual fund) that was purchased for $100,000 on January 1, 2008. It distributed $8,000 of dividends on July 4 of each year. On December 31, 2010, the share was sold for $400,000. Since the dividends for each year never exceeded the prior year’s amount, there are no excess distributions relating to the dividends. However, since the sale resulted in a capital gain of 300,000, the gain is an excess distribution and will be allocated ratably of each day the share was held. In particular, the excess distributions would result in $100,000 being allocated to 2008 and 2009 and taxed at the highest marginal tax rate (35% in 2008 and 2009). Also, interest would be charged to both years for the amount owed as of the due date for the particular tax year’s tax return- i.e. interest would accrue from April 15, 2009 for the 2008 excess distribution tax). Finally, the allocation of excess distribution for 2010 would be added to ordinary income line of the income tax return (line 21 for those filing Form 1040). Assuming the taxpayer was in the 33% income tax bracket for 2010, the additional tax caused by the PFIC regime would exceed $120,000. Please note that the transaction will not be recorded on the taxpayer’s Schedule D and that the dividends, though not taxed as part of the excess distribution regime, would still need to be reported on the taxpayer’s schedule B as non-qualified dividends.

To have perspective on the degree of additional taxation that can occur with the Excess Distribution method- if the $300,000 gain listed in the aforementioned scenario would have come from the sale of a non-PFIC, the tax would have been $45,000 (almost a third of the total PFIC tax liability). As you can clearly see- the IRS wants to discourage investing in foreign mutual funds.

QEF Election (Qualifying Electing Fund)

A second, simpler option for shareholders of PFICs is the QEF election. A first glance, it would appear to be a much better option for most investors since effectively results in the PFIC being treated like a US based mutual fund- the ordinary and capital gains income of the PFIC separately flow through to the shareholder according to percentage of ownership. For example, a taxpayer with a 1% stake in a PFIC that earns $100,000 in ordinary income and another $50,000 in capital gains income will report $1,000 as “other income” on the tax return while $500 will be reported on Schedule D.However, there is one huge obstacle to making this election- most PFICs are unable to be classified as a QEF since the IRS demands that a QEF comply with IRS reporting requirements (a large request for a non-US based company). Consequently, the QEF election is not frequently available.

Mark-to-Market Election

The third option available to PFIC shareholders is to make a mark-to-market election. This method allows the shareholder to report the annual gain in market value (i.e. unrealized gain) of the PFIC shares as ordinary income on the “other income” line of their tax returns. Unrealized losses are only reportable to the extent that gains have been previously reported. The adjusted basis for PFIC stock must include the gains and losses previously reported as ordinary income. Upon the sale of the PFIC shares, all gains are reported as ordinary income whereas losses are reported on Schedule D.To choose this method, the PFIC generally must be traded on a major international stock exchange and can only apply to the current and future tax years.

Also, this election is independent of prior PFIC elections (i.e. QEF or Sect 1291 election). for example: If stock X was purchased in 2007 for $100, has a FMV on 12/31/11 of $120, and no PFIC forms were filed until 2011 (when Sect 1296- Mark-to-market- election was made), no PFIC filings would be needed for the prior years as long distributions were less than 125% and no capital gains occurred. For the current year, 8621 would be filed using Mark to market and the ordinary income would be $20. see Section 1.1296-1 3 b.iii

Every effort has been taken to provide the most accurate and honest analysis of the tax information provided in this blog. Please use your discretion before making any decisions based on the information provided. This blog is not intended to be a substitute for seeking professional tax advice based on your individual needs.

Elections to Purge IRC Section 1291 Taint

Before the 1992 Treasury Department regulations, Boris Bittker and Lawrence Lokken concluded that the multitude of disadvantages associated with the IRC section 1291 interest-on-tax-deferral regime “suggest that the rules are designed to force the QEF election to be made wherever feasible” (Fundamentals of International Taxation, Warren, Gorham & Lamont, 1991). If a shareholder makes a QEF election in the first year of PFIC ownership, there is no section 1291 (interest-on-tax-deferral regime, discussed below) taint associated with the stock; however, a taxpayer or preparer may not be aware of the investment’s PFIC status when the stock is acquired, for the reasons mentioned previously. A QEF election after the first year of ownership protects the election and subsequent years from the section 1291 interest-on-tax deferral regime.

But what about the 1291 taint that attached to the pre-QEF election years? Requests for retroactive QEF elections are possible; however, the IRS is reluctant to grant retroactive relief except in special circumstances, such as those in which the shareholder satisfies the provisions of Treasury Regulations section 1.1295-3. Fortunately, IRC section 1291(d)(2) works in tandem with a QEF election to cleanse the 1291 taint associated with pre-election taxable years. It provides two elections by which the shareholder of a section 1291 fund can purge the PFIC stock of its section 1291 taint. The tax cost to cleanse section 1291 taint is taxation in the year of election.

Deemed-sale election (IRC section 1291(d)(2)(A))

Once a shareholder elects the QEF regime and can establish the fair market value of the fund stock on the first day of the taxable year of the QEF election, the shareholder can elect to recognize the inchoate gain in the stock as if he had sold it at its fair market value on the first day of the QEF election year. This election permits a shareholder of a 1291 fund to convert the investment into a QEF. The tax price of the conversion is current recognition of gain. The election is particularly beneficial when little appreciation exists with respect to the PFIC stock.

Treasury Regulations section 1.1291-10(d) describes the deemed-sale election process. The electing shareholder makes the election by filing Form 8621 with the return of the taxable year, reporting the recognized gain as an excess distribution pursuant to IRC section 1291(a), and paying the tax and interest due on the excess distribution.

Treasury Regulations section 1.1291-10(f) provides that an electing shareholder who owns stock directly increases the adjusted basis of the PFIC stock by the amount of gain recognized on the deemed sale, and section 1.1291-10(g) provides a fresh-start holding period for the PFIC stock, beginning on the date of the deemed sale. An indirect shareholder who makes the deemed-sale election increases the basis of the property owned directly by the shareholder through which ownership of the PFIC is attributed. This is further evidence that knowledge of indirect PFIC ownership is essential to mitigate the impact of any PFIC tax consequences.

Deemed-dividend election (IRC section 1291(d)(2)(B))

If a QEF is also a controlled foreign corporation (CFC) as defined in IRC section 957(a), a shareholder can purge the fund’s section 1291 taint by electing to include in gross income her proportionate share of the post-1986 PFIC earnings as of the first day that the QEF election is effective. This election is particularly beneficial when the shareholder’s proportionate share of post-1986 PFIC earnings is small.

When the interest on deferral regime is in effect, a shareholder who receives an excess distribution or disposes of PFIC stock at a gain is subject to tax on the deferral and an interest charge.

The election process and the consequences of the deemed-dividend election are similar to those of the deemed-sale election, and they are described in Treasury Regulations section 1.1291-9. For example, the deemed dividend is treated as an excess distribution on the day of the deemed dividend, the adjusted basis of the fund stock is increased by the amount of the dividend, and the shareholder’s holding period in the stock is treated as beginning on the day of the deemed dividend.

Interest on Tax Deferral Regime

The interest on tax deferral regime allows a U.S. person to defer taxation on PFIC income until the U.S. person receives an excess distribution from the PFIC or disposes of PFIC stock at a gain. When the interest on deferral regime is in effect, a shareholder who receives an excess distribution or disposes of PFIC stock at a gain is subject to tax on the deferral and an interest charge. The income from an excess distribution and the gain from a disposition of PFIC stock are ordinary income, in accordance with IRC sections 1291(a)(1)(B) and 1291(a)(2), respectively.

Excess distribution

IRC section 1291(b)(2)(A) defines an excess distribution as the excess (if any) of—

- the amount of the distribution received by the taxpayer during the taxable year, less

- 125% of the average amount received by the taxpayer during the three preceding taxable years (or, if shorter, the part of the taxpayer’s holding period before the taxable year).

Allocation of excess distributions

The amount of the excess distribution (or gain) is ratably allocated to each day that the shareholder held the stock [IRC sections 1291(a)(1)(A) and (a)(2)]. Amounts allocated to the current year (i.e., the taxable year of the excess distribution or disposition) are subject to regular U.S. taxation. The tax on amounts allocated to PFIC years exclusive of the current year is computed at the highest rate of tax that is applicable to the shareholder for the applicable tax years [IRC section 1291(c)(2)]. Furthermore, IRC section 1291(c)(3) imposes an interest charge on the tax, computed using the rates and method applicable under IRC section 6621 for underpayment of tax.

Adjustments

Implementation of the deferral method also requires taking into account certain adjustments described in IRC section 1291(b)(3). For example:

- Computations are on a share-by-share basis, except that shares with the same holding period can be aggregated.

- Stock splits and stock dividends must be taken into account.

- If the shareholder’s holding period includes periods during which stock was held by another shareholder, distributions to the other shareholder must be treated as if they were received by the subject shareholder.

- If distributions are received in a foreign currency, computations are made in that currency, and the amount of any excess distribution is translated into dollars.

Coordination with mark-to-market regime

Treasury Regulations section 1.1291-1(c)(3) provides that if PFIC stock is marked to market under IRC section 1296 (discussed below) for any taxable year, then IRC section 1291 and the Treasury Regulations thereunder are not applicable to any distribution with respect to section 1296 stock or any disposition of such stock for that taxable year.

Election of Mark to Market for Marketable Stock

IRC section 1296 permits a U.S. shareholder of a PFIC to mark to market the PFIC stock if it is “marketable stock,” as defined by Treasury Regulations section 1.1296-2. The stock must be regularly traded on a qualified exchange or other market, defined by Treasury Regulations section 1.1296-2(c) as—

- a national securities exchange that is registered with the SEC;

- the national market system established under section 11A of the Securities Exchange Act of 1934; or

- a foreign securities exchange that is regulated or supervised by a governmental authority of the country in which the market is located and has the characteristics described in Treasury Regulations section 1.1296-2(c)(1)(2), such as trading volume and disclosure requirements.

In accordance with IRC section 1296(a), the PFIC shareholder tax consequences of the mark-to-market election are either—

- gain recognized to the extent that the fair market value of the stock as of the close of the taxable year exceeds its adjusted basis; or

- loss recognized to the extent that the adjusted basis of the stock exceeds the fair market value of the stock as of the close of the taxable year.

IRC section 1296(c)(1) further provides that the gain included in gross income is ordinary income and the loss, which is also ordinary, is deductible in computing adjusted gross income. The six examples in Treasury Regulations section 1.1296-1(c)(7) illustrate the recognition of gain or loss associated with the mark-to-market election.

In addition, a PFIC shareholder’s stock basis is adjusted to reflect recognized gain or loss. Treasury Regulations section 1.1296-1(d)(1) provides that if the shareholder holds the stock directly, stock basis is increased by the amount included in gross income or decreased by the amount allowed as a deduction. If the stock is held through a foreign entity, held through a regulated investment company, or acquired from a decedent, the basis adjustment is described in Treasury Regulations sections 1.1296-1(d)(2), (d)(3), or (d)(4), respectively.

It has become increasingly possible for U.S. persons to unwittingly become shareholders of PFICs, the results of which are unexpected federal income taxation and an annual requirement to file Form 8621.

PFIC Shareholder Filing Responsibilities

The IRS Instructions for Form 8621 succinctly summarize the filing responsibilities of PFIC shareholders and provide extensive practical guidance about the QEF and the mark-to-market elections. They state that a U.S. person who is a direct or indirect shareholder of a PFIC must file Form 8621 for each taxable year if that person—

- receives certain direct or indirect distributions from a PFIC;

- recognizes gain on a direct or indirect disposition of PFIC stock;

- is reporting information with regard to a QEF or MTM election;

- is making a QEF election; or

- is required to file an annual report pursuant to IRC section 1298(f). Treasury Regulations section 1.1298-1 identifies the IRC section 1298(f) annual reporting requirements for U.S. persons who are shareholders of a passive foreign investment company.

It is significant to note that these criteria are applicable to both direct and indirect shareholders. This once again demonstrates the importance of identifying U.S. persons who are classified by the statute and regulations as indirect PFIC shareholders.

Avoid Being Caught Unawares

It has become increasingly possible for U.S. persons to unwittingly become shareholders of PFICs, the results of which are unexpected federal income taxation and an annual requirement to file Form 8621. Without guidance from their tax advisors, those U.S. persons may not be aware of elections that mitigate the unexpected federal income tax consequences of PFIC ownership. Knowing the ins and outs of what qualifies as a PFIC is crucial for helping taxpayers recognize when an investment has the potential to be classified as a PFIC, understand what the federal income tax consequences of that investment are, and make timely elections to mitigate the negative tax effects of PFIC ownership.

Stealth Exit Tax — PFICs

Then there is the passive foreign investment companies exit tax, which some have called the “stealth exit tax.” Under proposed regulations, this tax applies to anyone (including those who are US persons only by the substantial presence test), regardless of wealth, who changes status from US person to nonresident. I would argue that the PFIC exit tax does not apply because the regulations have remained in proposed form since 1992 and the expatriation rules of section 877 have been thoroughly revised several times since then. Nevertheless, proposed PFIC exit tax rules are out there and may cause sleepless nights to some covered expatriates.

If “disposition”, then tax

The problem comes from the PFIC law. If you have a “disposition” of PFIC stock, you have to pay a lot of tax as you may have an “excess distribution” from a “Section 1291 fund”. – Title 26, Section 1291(a)(2):

If the taxpayer disposes of stock in a passive foreign investment company, then the rules of paragraph (1) shall apply to any gain recognized on such disposition in the same manner as if such gain were an excess distribution.

Resident to nonresident = disposition

You, our L-1 or H-1B friend, owned foreign mutual funds (PFIC shares) before you came to the USA to live. You kept the mutual funds the whole time you were living in the United States. You still owned those same mutual fund shares when you left the United States and returned to your home country. The IRS says you dispose of your PFIC shares when you leave the United States and change from a resident taxpayer in the United States to a nonresident taxpayer of the United States. Just by leaving the United States, you have a tax to pay. Sounds like an exit tax, right? The rule comes from Proposed Regulations published in 1992:

If a shareholder of a section 1291 fund becomes a nonresident alien for U.S. tax purposes, the shareholder will be treated as having disposed of the shareholder’s stock in the section 1291 fund for purposes of section 1291 on the last day that the shareholder is a U.S. person. Termination of an election under section 6013(g) is treated as a change of residence (within the meaning of this paragraph (b)(2)) of the spouse who was a resident solely by reason of the section 6013(g) election.

See Prop. Regs. §1.1291-3(b)(2). Important: this rule (“you are treated as having a disposition of a PFIC when you change from resident to nonresident”) is from Proposed Regulations. It is not in the Internal Revenue Code.

The power (?) of Proposed Regulations

The big question is obvious. These are Proposed Regulations. They are not in effect yet. And they have been proposed — but not finalized — for 23 years. So you, a normal person going from nonresident of the United States to resident and back again. Do you take these Proposed Regulations seriously? Or not?

Judges say . . .

Courts generally say that Proposed Regulations are no better than an argument in a legal brief:

- “[P]roposed regulations are entitled to no deference until final.” In re AppleTree Markets, Inc., 19 F.3d 969, 973 (5th Cir. 1994).

- “Proposed Regulations are suggestions made for comment; they modify nothing.” LeCroy Research Sys. Corp. v. Commissioner, 751 F.2d 123, 127 (2d Cir. 1984).

- “Indeed, whatever may be said about “temporary” regulations that have not gained permanent status after 13 years (see n. 9), any notion of ascribing weight to anything that has remained in the “Proposed Regulation” limbo for a like period is totally unpersuasive.” Tedori v. United States, 211 F.3d 488, 492, n. 13 (9th. Cir. 2000). Emphasis added.

IRS says . . . taxpayers need not follow Proposed Regulations

The Internal Revenue Manual admits that taxpayers do not need to follow the rules laid out in Proposed Regulations.

Proposed Regulations provide guidance concerning Treasury’s interpretation of a Code section. * * * Taxpayers may rely on a Proposed Regulation, although they are not required to do so. Examiners, however, should follow Proposed Regulations, unless the Proposed Regulation is in conflict with an existing final or temporary regulation.

See I.R.M. 4.10.7.2.3.3 (01-01-06). Emphasis added.

IRS says . . . examiners should use Proposed Regulations

But what is that alarming sentence from the Internal Revenue Manual? Just after the IRS says that taxpayers need not follow Proposed Regulations, the Internal Revenue Manual says:

Examiners, however, should follow Proposed Regulations, unless the Proposed Regulation is in conflict with an existing final or temporary regulation.

See I.R.M. 4.10.7.2.3.3 (01-01-06). Emphasis added. In the next section of the Internal Revenue Manual, the position is softened a bit:

When no temporary or final regulations have been issued, examiners may use a Proposed Regulation to support a position. Indicate that the Proposed Regulation is the best interpretation of the Code section available.

I.R.M. 4.10.7.2.3.4 (01-01-2006). Emphasis added. Examiners “should” follow Proposed Regulations. Examiners “may” use a Proposed Regulation to support a position. Let me translate this into English. Here is what the IRS just told you:

“Proposed Regulations have no legal power. We know that. You, taxpayer, don’t have to follow them. But we will enforce them if we feel like it.”

AICPA comment from 1992

It is a known problem. When the Proposed Regulations were published in 1992, the AICPA chimed in with comments and suggestions. Here is what they said about the problem discussed in this week’s Friday Edition:

CHANGE OF U.S. RESIDENCE OR CITIZENSHIP. Under the Proposed Regulations, if a shareholder of section 1291 fund becomes a nonresident alien, that shareholder is treated as having disposed of its stock in such a section 1291 fund on the last day the shareholder is a U.S. person. Further, where a nonresident alien individual and that individual’s spouse have made an election under section 6013(g) to treat the nonresident alien as a resident of the U.S., termination of that election is treated as a change of residence of the electing spouse who was resident solely by reason of the election. We believe this rule is too broad in that it operates to impose tax on the full appreciation of shares in a section 1291 fund, much of which may have occurred prior to commencement of a resident alien taxpayer’s U.S. residency. The Proposed Regulation also causes taxable income when there has not yet been a realization event with respect to the shares. This result is beyond the intended scope of the PFIC rules and beyond the specific regulatory authority of section 1291(f) and section 1297(b)(5). We believe U.S. tax should not be imposed on unrealized appreciation that occurred prior to U.S. residency. The Proposed Regulations should be amended to exclude gain attributable to pre-residency appreciation from the excess distribution regime. Additionally, the shareholder’s holding period for purposes of section 1291 should begin on the day the U.S. person first became a U.S. citizen or resident, to prevent an interest charge being imposed on years during which the shareholder was not a U.S. citizen or resident. Alternatively, the regulations, when finalized, should clearly provide Prop. Reg. section 1.1291-3(b)(2) does not apply to section 1291 fund stock acquired during a pre-residency period prior to the effective date of the final regulations.

Return by a Shareholder Making Certain Late Elections To End Treatment as a Passive Foreign Investment Company

Purpose of Form

A U.S. person that is a direct or indirect shareholder of a former Passive Foreign Investment Company (PFIC) or a Section 1297(e) PFIC is treated for tax purposes as holding stock in a PFIC and therefore continues to be subject to taxation under section 1291 unless the shareholder makes a purging election under section 1298(b)(1).

A purging election under section 1298(b) (1) is:

• A deemed dividend election or a deemed sale election made with respect to a former PFIC under the rules of Regulations sections 1.1298-3(b) or 1.1298-3(c),

or

• A deemed dividend election or a deemed sale election made with respect to a Section 1297(e) PFIC under the rules of Regulations sections 1.1297-3(b) or 1.1297-3(c).

A timely filed purging election is made on Form 8621. Form 8621-A is used only to make a late purging election under section 1298(b)(1). A late purging election is a purging election under section 1298(b)(1) that is made:

• In the case of a shareholder of a former PFIC, after 3 years from the due date, as extended, of the tax return for the tax year that includes the termination date,

or

• In the case of a shareholder of a section 1297(e) PFIC, after 3 years from the due date, as extended, of the tax return for the tax year that includes the CFC qualification date. See Regulations sections 1.1298-3(e) or 1.1297-3(e) for more details. Generally, the amount due with respect to a late purging election is computed in the same manner as if the purging election had been timely filed. However, the taxpayer must also pay interest on the amount due determined for the period beginning on the due date (without extensions) for the taxpayer’s income tax return for the election year and ending on the date the late purging.

Election Year

• In the case of a former PFIC, the election year is the tax year of the electing shareholder that includes the termination date.

• In the case of a Section 1297(e) PFIC, the election year is the tax year of the electing shareholder that includes the CFC qualification date.

Former PFIC

A foreign corporation is a former PFIC with respect to the shareholder if the corporation satisfies neither the income test nor the asset test (described under the definition of PFIC below), but whose stock, held by that shareholder, is treated as stock of a PFIC, under section 1297(b)(1), because at any time during the shareholder’s holding period of the stock the corporation was a PFIC (under the income or asset test of section 1297(a) described below) that wasn’t a QEF, and the shareholder hasn’t made a mark-to-market election with respect to the PFIC.

Indirect Shareholder

Generally, a U.S. person is an indirect shareholder of a Section 1297(e) PFIC or a former PFIC if it is:

1. A direct or indirect owner of a pass-through entity that is a direct or indirect shareholder of a Section 1297(e) PFIC or a former PFIC,

2. A shareholder of a PFIC that is a shareholder of a Section 1297(e) PFIC, or a former PFIC,

3. A 50%-or-more shareholder of a foreign corporation that isn’t a PFIC and that directly or indirectly owns stock of a Section 1297(e) PFIC or a former PFIC, or

4. A 50%-or-more shareholder of a domestic corporation that owns a section 1291 fund.

Passive Foreign Investment Company (PFIC)

A foreign corporation is a PFIC if it meets either the income or asset test described below.

1. Income test. 75% or more of the corporation’s gross income for its tax year is passive income (as defined in section 1297(b)).

2. Asset test. At least 50% of the average percentage of assets (determined under section 1297(e)) held by the foreign corporation during the tax year are assets that produce passive income or that are held for the production of passive income.

Basis for measuring assets.

When determining PFIC status using the asset test, a foreign corporation can use adjusted basis if:

1. The corporation isn’t publicly traded for the tax year and

2. The corporation (a) is a CFC or (b) makes an election to use adjusted basis.

Publicly traded corporations must use fair market value when determining PFIC status using the asset test.

Look-thru rule.

When determining if a foreign corporation that owns at least 25% (by value) of another corporation is a PFIC, the foreign corporation is treated as if it held a proportionate share of the assets and received directly its proportionate share of the income of the 25%-or-more owned corporation.

Qualified Electing Fund (QEF)

A PFIC is a QEF if the U.S. person who is a direct or indirect shareholder of the PFIC elects (under section 1295) to treat the PFIC as a QEF. See the instructions for Form 8621 for more information.

Shareholder

A shareholder is a U.S. person that is a direct or indirect shareholder of the foreign corporation. See Indirect shareholder, earlier, for definition.

Termination Date

The termination date is the last day of the last tax year of the foreign corporation during which it qualified as a PFIC under section 1297(a).

§ 1.1298-3 Deemed sale or deemed dividend election by a U.S. person that is a shareholder of a former PFIC.

(a) In general. A shareholder (as defined in § 1.1291-9(j)(3)) of a foreign corporation that is a former PFIC, (as defined in § 1.1291-9(j)(2)(iv)) with respect to such shareholder, shall be treated for tax purposes as holding stock in a PFIC and therefore continues to be subject to taxation under section 1291 unless the shareholder makes a purging election under section 1298(b)(1). A purging election under section 1298(b)(1) is made under rules similar to the rules of section 1291(d)(2). Section 1291(d)(2) allows a shareholder to purge the continuing PFIC taint by making either a deemed sale election or a deemed dividend election.

(b) Application of deemed sale election rules –

(1) Eligibility to make the deemed sale election. A shareholder of a foreign corporation that is a former PFIC with respect to such shareholder may make a deemed sale election under section 1298(b)(1) by applying the rules of this paragraph (b).

(2) Effect of deemed sale election. A shareholder making the deemed sale election with respect to a former PFIC shall be treated as having sold all its stock in the former PFIC for its fair market value on the termination date, as defined in paragraph (d) of this section. A deemed sale is treated as a disposition subject to taxation under section 1291. Thus, gain from the deemed sale is taxed under section 1291 as an excess distribution received on the termination date. In the case of an election made by an indirect shareholder, the amount of gain to be recognized and taxed as an excess distribution is the amount of gain that the direct owner of the stock of the PFIC would have realized on an actual sale or disposition of the stock of the PFIC indirectly owned by the shareholder. Any loss realized on the deemed sale is not recognized. After the deemed sale election, the shareholder’s stock with respect to which the election was made under this paragraph (b) shall not be treated as stock in a PFIC and the shareholder shall not be subject to taxation under section 1291 with respect to such stock unless the foreign corporation thereafter qualifies as a PFIC under section 1297(a).

(3) Time for making the deemed sale election. Except as provided in paragraph (e) of this section, the shareholder shall make the deemed sale election under this paragraph (b) and section 1298(b)(1) in the shareholder’s original or amended return for the taxable year that includes the termination date (election year). If the deemed sale election is made in an amended return, the return must be filed by a date that is within three years of the due date, as extended under section 6081, of the original return for the election year.

(4) Manner of making the deemed sale election. A shareholder makes the deemed sale election under this paragraph (b) by filing Form 8621 (“Return by a Shareholder of a Passive Foreign Investment Company or Qualified Electing Fund”) with the return of the shareholder for the election year, reporting the gain as an excess distribution pursuant to section 1291(a) as if such deemed sale occurred under section 1291(d)(2), and paying the tax and interest due on the excess distribution. A shareholder that makes the deemed sale election after the due date of the return (determined without regard to extensions) for the election year must pay additional interest, pursuant to section 6601, on the amount of underpayment of tax for that year. An electing shareholder that realizes a loss shall report the loss on Form 8621, but shall not recognize the loss.

(5) Adjustments to basis. A shareholder that makes the deemed sale election increases its adjusted basis of the PFIC stock owned directly by the amount of gain recognized on the deemed sale. If the shareholder makes the deemed sale election with respect to a PFIC of which it is an indirect shareholder, the shareholder’s adjusted basis of the stock or other property owned directly by the shareholder, through which ownership of the PFIC is attributed to the shareholder, is increased by the amount of gain recognized by the shareholder. In addition, solely for purposes of determining the subsequent treatment under the Code and regulations of a shareholder of the stock of the PFIC, the adjusted basis of the direct owner of the stock of the PFIC is increased by the amount of gain recognized on the deemed sale. A shareholder shall not adjust the basis of any stock with respect to which the shareholder realized a loss on the deemed sale, but which loss is not recognized under paragraph (b)(2) of this section.

(6) Treatment of holding period. If a shareholder of a foreign corporation has made a deemed sale election, then, for purposes of applying sections 1291 through 1298 to such shareholder after the deemed sale, the shareholder’s holding period in the stock of the foreign corporation begins on the day following the termination, without regard to whether the shareholder recognized gain on the deemed sale. For other purposes of the Code and regulations, this holding period rule does not apply.

(c) Application of deemed dividend election rules –

(1) Eligibility to make the deemed dividend election. A shareholder of a foreign corporation that is a former PFIC with respect to such shareholder may make the deemed dividend election under the rules of this paragraph (c) provided the foreign corporation was a controlled foreign corporation (as defined in section 957(a) (CFC)) during its last taxable year as a PFIC. A shareholder may make the deemed dividend election without regard to whether the shareholder is a United States shareholder within the meaning of section 951(b). A deemed dividend election may be made by a shareholder whose pro rata share of the post-1986 earnings and profits of the PFIC attributable to the PFIC stock held on the termination date is zero.

(2) Effect of the deemed dividend election. A shareholder making the deemed dividend election with respect to a former PFIC shall include in income as a dividend its pro rata share of the post-1986 earnings and profits of the PFIC attributable to all of the stock it held, directly or indirectly on the termination date, as defined in paragraph (d) of this section. The deemed dividend is taxed under section 1291 as an excess distribution received on the termination date. The excess distribution determined under this paragraph (c) is allocated under section 1291(a)(1)(A) only to each day of the shareholder’s holding period of the stock during which the foreign corporation qualified as a PFIC. For purposes of the preceding sentence, the shareholder’s holding period of the PFIC stock ends on the termination date. After the deemed dividend election, the shareholder’s stock with respect to which the election was made under this paragraph (c) shall not be treated as stock in a PFIC and the shareholder shall not be subject to taxation under section 1291 with respect to such stock unless the foreign corporation thereafter qualifies as a PFIC under section 1297(a).

(3) Post-1986 earnings and profits defined –

(i) In general. For purposes of this section, the term post-1986 earnings and profits means the post-1986 undistributed earnings, within the meaning of section 902(c)(1) (determined without regard to section 902(c)(3)), as of the close of the taxable year that includes the termination date. For purposes of this computation, only earnings and profits accumulated in taxable years during which the foreign corporation was a PFIC shall be taken into account, without regard to whether the earnings relate to a period during which the PFIC was a CFC.

(ii) Pro rata share of post-1986 earnings and profits attributable to shareholder’s stock: (A) In general. A shareholder’s pro rata share of the post-1986 earnings and profits of the PFIC attributable to the stock held by the shareholder on the termination date is the amount of post-1986 earnings and profits of the PFIC accumulated during any portion of the shareholder’s holding period ending at the close of the termination date and attributable, under the principles of section 1248 and the regulations under that section, to the PFIC stock held on the termination date.

(B) Reduction for previously taxed amounts. A shareholder’s pro rata share of the post-1986 earnings and profits of the PFIC does not include any amount that the shareholder demonstrates to the satisfaction of the Commissioner (in the manner provided in paragraph (c)(5)(ii) of this section) was, pursuant to another provision of the law, previously included in the income of the shareholder, or of another U.S. person if the shareholder’s holding period of the PFIC stock includes the period during which the stock was held by that other U.S. person.

(4) Time for making the deemed dividend election. Except as provided in paragraph (e) of this section, the shareholder shall make the deemed dividend election under this paragraph (c) and section 1298(b)(1) in the shareholder’s original or amended return for the taxable year that includes the termination date (election year). If the deemed dividend election is made in an amended return, the return must be filed by a date that is within three years of the due date, as extended under section 6081, of the original return for the election year.

(5) Manner of making the deemed dividend election: (i) In general. A shareholder makes the deemed dividend election by filing Form 8621 and the attachment to Form 8621 described in paragraph (c)(5)(ii) of this section with the return of the shareholder for the election year, reporting the deemed dividend as an excess distribution pursuant to section 1291(a)(1), and paying the tax and interest due on the excess distribution. A shareholder that makes the deemed dividend election after the due date of the return (determined without regard to extensions) for the election year must pay additional interest, pursuant to section 6601, on the amount of underpayment of tax for that year.

(ii) Attachment to Form 8621. The shareholder must attach a schedule to Form 8621 that demonstrates the calculation of the shareholder’s pro rata share of the post-1986 earnings and profits of the PFIC that is treated as distributed to the shareholder on the termination date pursuant to this paragraph (c). If the shareholder is claiming an exclusion from its pro rata share of the post-1986 earnings and profits for an amount previously included in its income or the income of another U.S. person, the shareholder must include the following information:

(A) The name, address, and taxpayer identification number of each U.S. person that previously included an amount in income, the amount previously included in income by each such U.S. person, the provision of law pursuant to which the amount was previously included in income, and the taxable year or years of inclusion of each amount.

(B) A description of the transaction pursuant to which the shareholder acquired, directly or indirectly, the stock of the PFIC from another U.S. person, and the provision of law pursuant to which the shareholder’s holding period includes the period the other U.S. person held the CFC stock.

(6) Adjustments to basis. A shareholder that makes the deemed dividend election increases its adjusted basis of the stock of the PFIC owned directly by the shareholder by the amount of the deemed dividend. If the shareholder makes the deemed dividend election with respect to a PFIC of which it is an indirect shareholder, the shareholder’s adjusted basis of the stock or other property owned directly by the shareholder, through which ownership of the PFIC is attributed to the shareholder, is increased by the amount of the deemed dividend. In addition, solely for purposes of determining the subsequent treatment under the Code and regulations of a shareholder of the stock of the PFIC, the adjusted basis of the direct owner of the stock of the PFIC is increased by the amount of the deemed dividend.

(7) Treatment of holding period. If the shareholder of a foreign corporation has made a deemed dividend election, then, for purposes of applying sections 1291 through 1298 to such shareholder after the deemed dividend, the shareholder’s holding period of the stock of the foreign corporation begins on the day following the termination date. For other purposes of the Code and regulations, this holding period rule does not apply.

(8) Coordination with section 959(e). For purposes of section 959(e), the entire deemed dividend is treated as having been included in gross income under section 1248(a).

(d) Termination date. For purposes of this section, the termination date is the last day of the last taxable year of the foreign corporation during which it qualified as a PFIC under section 1297(a).

(e) Late purging elections requiring special consent –

(1) In general. This section prescribes the exclusive rules under which a shareholder of a former PFIC may make a section 1298(b)(1) election after the time prescribed in paragraph (b)(3) or (c)(4) of this section for making a deemed sale or a deemed dividend election has elapsed (late purging election). Therefore, a shareholder may not seek such relief under any other provisions of the law, including § 301.9100-3 of this chapter. A shareholder may request the consent of the Commissioner to make a late purging election for the taxable year of the shareholder that includes the termination date provided the shareholder satisfies the requirements set forth in this paragraph (e). The Commissioner may, in his discretion, grant relief under this paragraph (e) only if –

(i) In a case where the shareholder is requesting consent under this paragraph (e) after December 31, 2005, the shareholder requests such consent before a representative of the Internal Revenue Service raises upon audit the PFIC status of the foreign corporation for any taxable year of the shareholder;

(ii) The shareholder has agreed in a closing agreement with the Commissioner, described in paragraph (e)(3) of this section, to eliminate any prejudice to the interests of the U.S. government, as determined under paragraph (e)(2) of this section, as a consequence of the shareholder’s inability to file amended returns for its taxable year in which the termination date falls or an earlier closed taxable year in which the shareholder has taken a position that is inconsistent with the treatment of the foreign corporation as a PFIC; and

(iii) The shareholder satisfies the procedural requirements set forth in paragraph (e)(3) of this section.

(2) Prejudice to the interests of the U.S. government. The interests of the U.S. government are prejudiced if granting relief would result in the shareholder having a lower tax liability (other than by a de minimis amount), taking into account applicable interest charges, for the taxable year that includes the termination date (or a prior taxable year in which the taxpayer took a position on a return that was inconsistent with the treatment of the foreign corporation as a PFIC) than the shareholder would have had if the shareholder had properly made the section 1298(b)(1) election in the time prescribed in paragraph (b)(2) or (c)(3) of this section (or had not taken a position in a return for an earlier year that was inconsistent with the status of the foreign corporation as a PFIC). The time value of money is taken into account for purposes of this computation.

(3) Procedural requirements –

(i) In general. The amount due with respect to a late purging election is determined in the same manner as if the purging election had been timely filed. However, the shareholder is also liable for interest on the amount due, pursuant to section 6601, determined for the period beginning on the due date (without extensions) for the taxpayer’s income tax return for the year in which the termination date falls and ending on the date the late purging election is filed with the IRS.

(ii) Filing instructions. A late purging election is made by filing a completed Form 8621-A, “Return by a Shareholder Making Certain Late Elections to End Treatment as a Passive Foreign Investment Company.”

(4) Time and manner of making late election –

(i) Time for making a late purging election. A shareholder may make a late purging election in the manner provided in paragraph (e)(4)(ii) of this section at any time. The date the election is filed with the IRS will determine the amount of interest due under paragraph (e)(3) of this section.

(ii) Manner of making a late purging election. A shareholder makes a late purging election by completing Form 8621-A in the manner required by that form and this section and filing that form with the Internal Revenue Service, DP 8621-A, Ogden, UT 84201.

(5) Multiple late elections. For rules regarding the circumstances under which a shareholder of a foreign corporation may make multiple late purging elections under this paragraph (e) or § 1.1297-3(e), see § 1.1297-3(e)(5).

(f) Effective/applicability date. The rules of this section are applicable as of December 8, 2005.

[T.D. 9231, 70 FR 72915, Dec. 8, 2005, as amended by T.D. 9360, 72 FR 54824, Sept. 27, 2007]

Avoiding the sting of PFIC classification

For most, a PFIC is not necessarily a good thing.

PFICs are subject to complicated and strict tax guidelines by the Internal Revenue Service (IRS), which covers treatment of these investments in Sections 1291 through 1297 of the income tax code. Both the PFIC and the shareholder must keep accurate records of all transactions, including share basis, dividends and any undistributed income earned by the company. The strict guidelines are set up to discourage ownership of PFICs by U.S. investors.

For some US persons with passive overseas investments, there are other structures to consider. One option is establishing a controlled foreign corporation (CFC), using form 5471 as usual and treating earnings as subpart F income. Now by treating CFC’s earnings as subpart F, they may not be subject to the PFIC regime pursuant to the overlap rule.

For more details, have a look at the private letter ruling (PLR) which I quote from below – Index Number: 1297.00-00, 957.00-00

http://www.irs.gov/pub/irs-wd/0943004.pdf

Code section 1297(d)(1) provides that a corporation shall not be treated with respect to a shareholder as a PFIC during the qualified portion of such shareholder’s holding period with respect to the stock in such corporation. (“Overlap Rule”).

The legislative history to Code section 1297(d) provides that the Overlap Rule was enacted because of a concern about the unnecessary complexity caused by the application of the subpart F and PFIC regimes to the same shareholders. To address this concern, the legislative history to Code section 1297(d) states that “a shareholder that is subject to current inclusion under the subpart F rules with respect to stock of a PFIC that is also a CFC generally is not subject also to the PFIC provisions with respect to the same stock.”

US Investors in Foreign Companies That Turn Into PFICs

Many of our clients are sophisticated investors and are familiar with the concept of a PFIC. A PFIC occurs where US exposed investors in overseas entities / assets incur unfavorable tax and reporting treatment on their US returns. I explain this in more detail here – https://htj.tax/?s=pfic

Recently we have had clients who invested in foreign entities which were not initially PFICs but as the working capital of the company (such as cash) grew, it became a PFIC. What happens then?

Notice 88-22, which for many years contained the only guidance on the application of the Income Test and the Asset Test, provides that cash and other current assets readily convertible into cash, including assets that may be characterized as the working capital of an active business, are treated as passive assets for purposes of the Passive Asset Test. Obviously this is nonsense and we (tax professionals) were expecting that recent proposed regs would have addressed this oversight. Unfortunately the response published earlier in 2021 was as follows –

“The Treasury Department and the IRS continue to study the appropriate treatment of working capital.”

Some professionals stand by the view that if the cash is held in a non-interest bearing account then it won’t qualify as a passive asset for the purposes of the passive asset test.

So this may be (depending on the fact pattern) a work around to avoid PFIC classification.

Obviously this is bad for the company (to forgo earning interest because of PFIC concerns). In certain cases we may recommend that the US exposed investor consider alternative holding / investment structures.

Another option to consider is this. The pfic rules (section 1297(e)) sometimes request a valuation be done and this is where IP (or other intangibles) may be formally valued which may help companies with the passive asset test.

Got questions? Get advice from a US qualified professional