Skip to content

Skip to content Local tax information summary for Singapore

Local tax information for US Tax Singapore

Local information | Details |

Tax authority | Inland Revenue Authority of Singapore (IRAS) |

Website | |

Tax year | 1 January to 31 December |

Tax return due date | 15 April |

Is joint filing possible | No |

Are tax return extensions possible | No |

Who is liable?

A person is subject to tax on employment income for services performed in Singapore, regardless of whether the remuneration is paid in or outside Singapore. Resident individuals who derive income from sources outside Singapore are not subject to tax on such income. This exemption does not apply if the foreign-source income is received through a partnership in Singapore. Foreign-source dividend income, foreign branch profits and foreign-source service income received by any individual resident in Singapore through partnerships may be exempted from Singapore tax if certain prescribed conditions are met.

Individuals who carry on a trade, business, profession or vocation in Singapore are taxed on their profits. Whether an individual is carrying on a trade is determined based on the circumstances of each case. Foreign-source income received in Singapore by a non-resident is specifically exempt from tax.

For more help with US tax returns Singapore don’t hesitate to contact our experts.

How is a US Exposed Person in Singapore taxed?

The IRS taxes US citizens on their worldwide income unless and until they relinquish their citizenship. U.S. lawful permanent residents (“green card holders”) who live outside the U.S. continue to be subject to U.S. tax on their worldwide income until the green card has been revoked or has been administratively or judicially determined to have been abandoned. Code §7701(b)(6).

For a personal and reliable advice about USA taxation Singapore, please don’t hesitate to contact our US taxation Singapore experts.

Residence status for tax purposes in Singapore

Individuals are resident for tax purposes if, in the year preceding the assessment year, they reside in Singapore except for such temporary absences from Singapore as may be reasonable and not inconsistent with a claim by such persons to be resident in Singapore. This also includes those who are physically present or who exercise employment other than as a director of a company in Singapore for at least 183 days during the year preceding the assessment year.

A concession is available for foreign employees whose employment period straddles two calendar years. Under this concession, which is commonly known as the “two-year administrative concession”, the individual is considered resident for both years if they stay or work in Singapore for a continuous period of at least 183 days straddling the two years, even if fewer than 183 days were spent in Singapore in each year.

Non-resident individuals employed for not more than 60 days in a calendar year in Singapore are exempt from tax on their employment income derived from Singapore. This exemption does not apply to a director of a company, a public entertainer or a professional in Singapore.

Under the Not Ordinarily Resident (NOR) scheme, a qualifying individual may enjoy tax concessions for five consecutive assessment years, including time apportionment of Singapore employment income, if certain conditions are satisfied.

Got questions about American tax Singapore? Please don’t hesitate to contact us for guidance.

US expat in Singapore income tax filing

US expats living in Singapore may have to file an income tax form every year. If this is the case, there are three forms to choose from:

- Employed Singapore residents should file their taxes using Form B1

- Self-employed Singapore residents should file their taxes using Form B

- Non-residents should file their taxes using Form M

For more information on USA tax Singapore filing you may consider checking this file from the Inland Revenue Authority of Singapore.

Income subject to tax in Singapore

Employment income

Taxable employment income includes cash remuneration, wages, salary, leave pay, directors’ fees, commissions, bonuses, gratuities, perquisites, gains received from employee share plans and allowances received as compensation for services. Benefits-in-kind derived from employment, including home-leave passage, employer-provided housing, employer-provided automobiles and children’s school fees, are also taxable. Certain types of these benefits receive special tax treatment. Effective from the 2020 assessment year, the prescribed formula to calculate the taxable car benefit in Singapore has been revised to better reflect the actual benefits enjoyed by the employees and to simplify tax compliance.

Under the Not Ordinarily Resident (NOR) scheme, a resident employee whose resident status is not accorded under the two-year or three-year administrative concessions may benefit from certain concessions for five consecutive assessment years provided certain conditions are met. Under a 2019 budget proposal, the last such NOR status will be from the 2020 assessment year to the 2024 assessment year. Individuals who have been accorded the NOR status will continue to enjoy NOR tax concessions until their NOR status expires if they continue to meet the conditions of the concessions.

Self-employment and business income

Self-employment income subject to tax is based on financial accounts prepared under generally accepted accounting principles. Adjustments are made to the profits or losses according to tax law. Business income is aggregated with other types of income to determine taxable income.

Income from a trade, business, profession or vocation paid to a non-resident is taxed at 22%.

Income from professional services paid to a non-resident is taxed at 15%. This is a final withholding tax on the gross amount, unless the non-resident professional elects to be assessed at a rate of 22% on net income.

Losses and excess capital allowances from the carrying on of a trade, business, profession or vocation may be offset against all other chargeable income of the same year. Any unused trade losses and capital allowances can be carried forward indefinitely for offset against future income from all sources, subject to certain conditions.

Relief is also available for the carry back of current year unused capital allowances and trade losses, subject to the satisfaction of certain conditions.

Investment income

Under the one-tier system, dividends paid by Singapore tax-resident companies are exempt from income tax in the hands of shareholders, regardless of whether the dividends are paid out of taxed income or tax-free gains.

Dividends, other than tax-exempt and one-tier dividends, are taxed at the applicable income tax rates.

Singapore-source investment income (that is, income that is not considered to be gains or profits from a trade, business or profession) derived directly by individuals from specified financial instruments, including standard savings, current and fixed deposits, is exempt from tax. Examples of such income include interest from debt securities, annuities and distributions from unit trusts.

Interest (excluding tax-exempt interest from approved banks, finance companies, qualifying debt securities and qualified project debt securities) paid to non-residents is taxed at 15%.

Royalties for the use of, or right to use, movable property and scientific, technical, industrial or commercial knowledge or information paid to non-residents are taxed at 10%.

Net rental income is aggregated with other types of income and taxed at the applicable rates.

Rent or other payments for the use of movable property paid to non-residents is taxable at 15%.

Taxation of employer-provided stock options and share ownership plans – Employer-provided stock options are taxed at the time of exercise, not at the time of grant. Share awards are taxable at the time of award or at the time of vesting, if a vesting period is imposed. The taxable amount is the open market value of the shares at the time of exercise, award or vesting, less the amount paid by the employee, if any.

Stock options and share awards granted during overseas employment are not subject to tax even if the gains derived are remitted into Singapore while the employee is a tax resident, because all foreign-source income received in Singapore (other than through partnerships) by resident individuals is exempt from tax. Stock options and share awards granted on or after 1 January 2003 while the employee is engaged in employment in Singapore are subject to tax, regardless of where the options are exercised or shares are vested. These options and awards are deemed exercised or vested at the time of cessation of employment (including being seconded outside Singapore for an assignment or leaving Singapore for a period more than three months) for a foreign national employee, and tax is due immediately on the deemed gains.

Capital Gains

Singapore does not impose tax on capital gains. However, in certain circumstances, the tax authorities consider transactions involving the acquisition and disposal of real estate, stocks or shares to be the carrying on of a trade. As a result, gains arising from such transactions are taxable. The determination of whether such gains are taxable is based on a consideration of the facts and circumstances of each case.

The buyer of property must pay stamp duty on the value of the property purchased. Certain buyers of residential properties (including residential land) must pay additional buyer’s stamp duty, in addition to the usual stamp duty. Sellers of residential and industrial properties may be liable for seller’s stamp duty depending on when the property was purchased and the holding period. Specified sellers of industrial properties may be liable for stamp duty.

Social Security Impact on Your US Expat Taxes

The Singapore equivalent of Social Security is called the Central Provident Fund (CPF).

The Central Provident Fund (CPF) is a statutory savings scheme to provide for employees’ old-age retirement in Singapore. Only Singapore citizens and permanent residents working in Singapore are required to contribute to the CPF. All foreigners (including Malaysians) are exempt from CPF contributions. Foreigners may not make voluntary contributions to the CPF.

As an expatriate, you are not required to make payments into the Singapore CPF. You will be once you have been approved for permanent residency status by the Immigration and Checkpoint Authority of Singapore. If you decide to become a permanent resident of Singapore, you and your employer will both make contributions into the CPF. The total contribution on your behalf into CPF will total 30% of your annual salary, with 10% coming from your employer and the remainder coming from you.

Both employees and employers must contribute to the fund. For individuals up to 55 years of age, the statutory rate of the employee’s contribution is 20%, and the rate of the employer’s contribution is 17%. Lower contribution rates apply to individuals over 55 years of age. Special transitional contribution rates apply to foreigners who become Singapore permanent residents.

Self-employed individuals who carry on a trade, business, profession or vocation may also participate in the CPF scheme.

A Supplementary Retirement Scheme (SRS) allows Singapore citizens and permanent residents to elect to contribute to private funds in addition to their CPF contributions. Foreigners working in Singapore may also participate in the scheme. Contributions are deductible but are subject to a cap.

If you are a US citizen and self-employed in a foreign country, you are still required to pay US Social Security and Medicare taxes on your earnings. You will pay both the employee and employer portion via Schedule SE on your US Expat Taxes. However, if you are an employee of a foreign employer and required to pay taxes into the foreign country’s social security equivalent, you are not required to pay US Social Security tax.

Is there a US tax treaty in Singapore?

There has yet to be a treaty established between the United States and Singapore. Despite the lack of treaty, each country offers a tax credit designed to eliminate dual taxation. In the US, this is called the foreign tax credit. In Singapore, this is called the unilateral tax credit, which services the same purpose. Both will give credit for taxes paid to a foreign country.

US Expat Taxes for Employees in Singapore

If you are an employee of a Singapore-based company, your income will be subject to Singapore income tax. Unfortunately, as a US citizen, the income earned in Singapore will also be subject to US expat taxes. The good news is that the US provides a series of exclusions and credits (mentioned above) for income earned and taxes paid in foreign countries. The ultimate goal is optimizing your worldwide tax liability.

US Expat Taxes for the Self-Employed in Singapore

Similar to US requirements, self-employed individuals operating their business in Singapore must pay taxes on their net profits to Singapore. Foreign individuals planning to start a business in Singapore must obtain an EntrePass prior to beginning business. More information on the EntrePass can be obtained from the Singapore Government website. As a US Citizen, the IRS requires that you continue to report and pay tax on your self-employment earnings on your US expat taxes. It does not matter where the income is earned, but you will still qualify to receive the exclusions and credits mentioned above.

How Will the US Government Tax an Annuity from Singapore Given to a US Citizen?

You are required to report the receipt of foreign gifts or bequests only if the applicable threshold is exceeded. For purposes of determining the reporting thresholds, you must aggregate gifts received from related parties. For gifts or bequests from a nonresident alien or foreign estate, you are required to report the receipt of such gifts or bequests only if the aggregate amount received from that nonresident alien or foreign estate exceeds $100,000 during the taxable year. If the gifts or bequests exceed $100,000, you must separately identify each gift in excess of $5,000.

For purported gifts from foreign corporations or foreign partnerships, you are required to report the receipt of such purported gifts only if the aggregate amount received from all entities exceeds $17,339 for 2022 and $18,567 for 2023 (adjusted annually for inflation). You must separately identify each gift and the identity of the donor. Note that the IRS may recharacterize purported gifts from foreign corporations or foreign partnerships.

If you fail to timely file Part IV of Form 3520, or the information you provide on the form is incomplete or incorrect, the IRS may determine the income tax consequences of the receipt of the foreign gift or bequest. In addition, you may be subject to a penalty equal to five percent of the value of the gift or bequest for each month in which the gift or bequest is not reported, not to exceed 25 percent of the gift, unless you have reasonable cause for the failure to timely or accurately file.

Are Insurance Payouts in Singapore Taxable to US Expats?

Most earned and passive investment income is taxable in the US, however, there are types of receipts that are excluded from taxable income. Examples are life insurance proceeds received by the qualified beneficiary, tax-exempt interest, property acquired by bequest, devise, or inheritance.

If any contract which is a life insurance contract under the applicable law does not meet the definition of life insurance contract under section 7702, the excess of the amount paid by the reason of the death of the insured over the net surrender value of the contract shall be deemed to be paid under a life insurance contract for purposes of section 101.7 (In other words, the normal rules for life insurance proceeds will apply).

On the other hand, if the policy is not a life insurance policy under applicable law, or if the entity issuing the policy is otherwise treated as a “passive foreign investment company” (PFIC) under U.S. tax law, the proceeds on death may be taxed as if it were a PFIC.

The ownership of a PFIC by a U.S. individual may result in adverse current annual U.S. income tax consequences, as well as adverse U.S. income tax consequences on the death of the owner. For example, any actual or deemed disposition of a PFIC during a lifetime, possibly including relinquishing U.S. citizenship or U.S. residency, gifting the policy, or even pledging the policy for a loan, may result in adverse U.S. income taxation under the excess distribution regime. Further, the death of the policy owner may also trigger a deemed disposition and result in adverse U.S. income taxation under the excess distribution regime.

The owner’s interest in the foreign insurance company will not be treated as a PFIC if the entity is: A “qualifying insurance corporation”, and It derives its income from the active conduct of an insurance business.

Are foreign dividends taxed in Singapore?

Foreign income remittances in the form of dividends, branch profits, and services income derived by resident companies are usually exempt from tax. Provided that the income is received from a foreign jurisdiction with a certain minimum headline tax rate in the year the income is received or deemed received and the income has been subject to tax in the foreign jurisdiction.

Does Singapore really have a territorial tax system?

Generally, gains are taxable when employees exercise the share options. This is the case even if the employee has ended his employment with the employer or if the employee has been posted overseas and is no longer employed in Singapore. For an employee who is not a Singaporean Citizen, a “deemed exercise” rule is applied when the employee is no longer employed in Singapore so that tax is payable at that time.

Which Singapore Banks allowed Brokerage accounts for US Expats?

Selecting brokers for international trading is not easy. Many look for platforms that cover international exchange-traded funds (ETFs) and American depositary receipts (ADRs) universes and direct access to global markets assets.

Crypto withdrawal taxation in Singapore

Businesses that buy and sell virtual currencies in the ordinary course of their business will be taxed on the profit derived from trading with virtual currencies. Profits derived by businesses that mine and trade virtual currencies in exchange for money are also subject to tax. Businesses that buy virtual currencies for long-term investment purposes may enjoy a capital gain from the disposal of these virtual currencies. However, as there are no capital gains taxes in Singapore, such gains are not subject to tax.

Whether gains from the disposal of virtual currencies are trading or capital gains depends on the facts and circumstances of each case. Reference is made to the “Badges of Trade” in deciding. Here factors such as purpose, frequency of transactions, and holding periods are considered when determining if such gains are taxable.

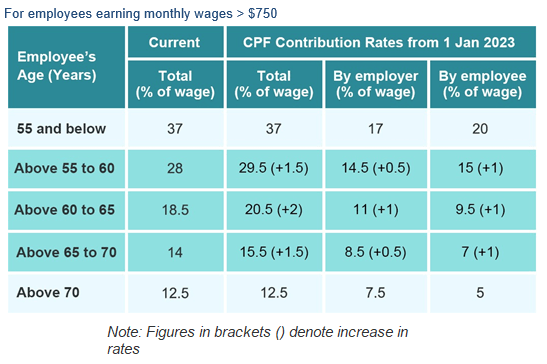

What is CPF in Singapore?

The CPF is a mandatory social security savings scheme funded by contributions from employers and employees.

The CPF is a key pillar of Singapore’s social security system, and serves to meet retirement, housing and healthcare needs.

The CPF contribution rates for employees aged above 55 to 70 will be increased to strengthen their retirement adequacy. The changes will apply to wages earned from 1 January 2023:

How is Singapore’s CPF taxed after death?

All savings in the deceased person’s CPF accounts will be distributed.

Retirement Account (RA) savings that were used for buying an annuity from an approved insurer, or deposited with a participating bank, will likewise be distributed.

Foreign Earned Income Exclusion for US Expats in Singapore

If you meet certain requirements, you may qualify for the foreign earned income exclusion, the foreign housing exclusion, and/or the foreign housing deduction. To claim these benefits, you must have foreign earned income, your tax home must be in a foreign country, and you must be one of the following:

- A U.S. citizen who is a bona fide resident of a foreign country or countries for an uninterrupted period that includes an entire tax year,

- A U.S. resident alien who is a citizen or national of a country with which the United States has an income tax treaty in effect and who is a bona fide resident of a foreign country or countries for an uninterrupted period that includes an entire tax year, or

- A U.S. citizen or a U.S. resident alien who is physically present in a foreign country or countries for at least 330 full days during any period of 12 consecutive months.

How about living in Singapore and owning a property in the US?

When a nonresident individual owns rental real estate in the U.S., there are two alternatives for reporting and paying U.S. income taxes.

The individual may choose not to file an income tax return in the U.S. to report the rental income. In this case, 30% of the gross rental income must be remitted to the Internal Revenue Service. If the rental is handled by a rental agent, the agent must withhold and remit the 30% as rent is collected. If no rental agent is involved, then the nonresident owner is obligated to pay the 30% to the Internal Revenue Service.

Most nonresidents do not choose the first option. Instead, they report the rental income on a U.S. income tax return, Form 1040NR. They must report the rental income received, but, unlike the first option, all expenses associated with the property are deductible against the rental income. These expenses include property taxes, mortgage interest, repairs, etc. In addition, a calculated amount for depreciation is also deducted. Majority of owners do not have any taxable income left after taking into account all of the deductions that are available. If there is no taxable income, there is no tax to pay. In addition, any excess expenses accumulate and carry forward indefinitely and are available to offset profit on sale.

How long does the probate process take in Singapore?

When a loved one passes away, they leave behind their estate. This includes their money and property (such as cash, real estate, financial securities, possessions, and other assets), as well as their liabilities (such as debts). Estates must be administered and distributed in accordance with the law. Probate and administration is the legal process of appointing someone to manage the deceased’s estate. The Family Courts and the Family Division of the High Court hear probate and administration applications.