Skip to content

Skip to content

We have significant experience assisting our clients with complicated, international tax issues.

The following list represents some of the areas in which we have provided both planning and compliance services for our clients:

- US shareholders of foreign corporations

- US partners in foreign partnerships

- US grantors and beneficiaries of foreign trusts

- US shareholders of Passive Foreign Investment Companies (PFICS)

- Reporting for Foreign Bank and Financial Accounts (FBARs)

- Blocked income reporting for deferral of tax in currency restriction situations

- Donations to foreign charities by US private foundations via expenditure responsibility grants

- Income tax treaty analysis for various issues including determination of residency, re-sourcing of income to avoid double taxation, reduction or exemption of tax

- Determination of residency for income tax purposes for foreign nationals including optimization of elections for first and last year of residency

- Social Security tax implications to compensation of foreign nationals and US expatriates including application and analysis of Totalization agreements

- Foreign tax credit optimization including analysis of paid versus accrued methods and maximizing foreign source income

- Optimization for US expatriates including analysis of foreign tax credit versus foreign earned income exclusions

- Reporting of foreign rental properties including proper depreciation methods and treatment of rental of a principal residence

- Reporting and planning for US real property interests by nonresidents including applications for reduction/exemption from withholding on sale proceeds

- Reporting and planning for nonresidents with US investments or US effectively-connected income

- State residency and domicile issues for foreign nationals and US expatriates

- Reporting gifts and inheritances from nonresidents

- Consulting to employers of international assignees relating to tax equalization policy development and application, tax planning for international assignments including coordination with tax advisors in local jurisdictions, compensation structuring, payroll reporting and employee education and tax return preparation

- Determination of residency for US citizens in US possessions

- Given the uniqueness of the U.S. Tax Code, we are perfectly positioned to assist American Citizens, American Permanent Residents (Green Card holders) and American companies who want to expand to Asia with:

- Incorporation and corporate structuring

- Annual returns for both Asia and the United States

- Work passes across the region

- Corporate secretarial and full accounting services

US Tax Portugal for US Expats and Those Exposed to US Taxation

For American Citizens, American Permanent Residents (Green Card holders) and American companies already in Asia and Europe, we can assist with U.S. tax issues including -

- US Tax Amnesty – both Offshore Voluntary Disclosure (OVDP) and US Streamlined Tax Amnesty

- FATCA compliance including Form 8966, W-8 Ben-E and entity analysis

- Reporting of foreign companies, partnerships and foreign trusts

- Passive Foreign Investment Companies (PFICs)

- Foreign Bank Account Reporting (FBARs)

- Pre-immigration Tax Planning

- Cross border tax planning

- Expat Salary negotiation

- Corporate structuring

- ITINs (U.S. Tax IDs)

- Ordinary 1040s

US Tax Returns Portugal Questions

Do You Have to Pay Expat Taxes in Portugal?

As a U.S. Citizen or green card holder you are legally required to file a U.S. tax return each year regardless of whether you already pay taxes in your residence country.

All US citizens and green card holders who earn more than $12,550 (in 2021, or just $400 of self-employment income or just $5 if you’re married to a foreigner) anywhere in the world are required to file a US federal tax return and pay taxes to the IRS, regardless of where in the world they live or where their income originates.

Residency for Portugal Income Tax

You are officially a resident if you spend 183 days or more in Portugal over a 12-month period, or maintain an abode. An abode can be described as one’s home, habitation, residence, domicile, or place of dwelling. It does not mean your principal place of business. “Abode” has a domestic rather than a vocational meaning and does not mean the same as “tax home,” when it comes to Portugal income tax.

Tax Rates When Living Abroad in Portugal

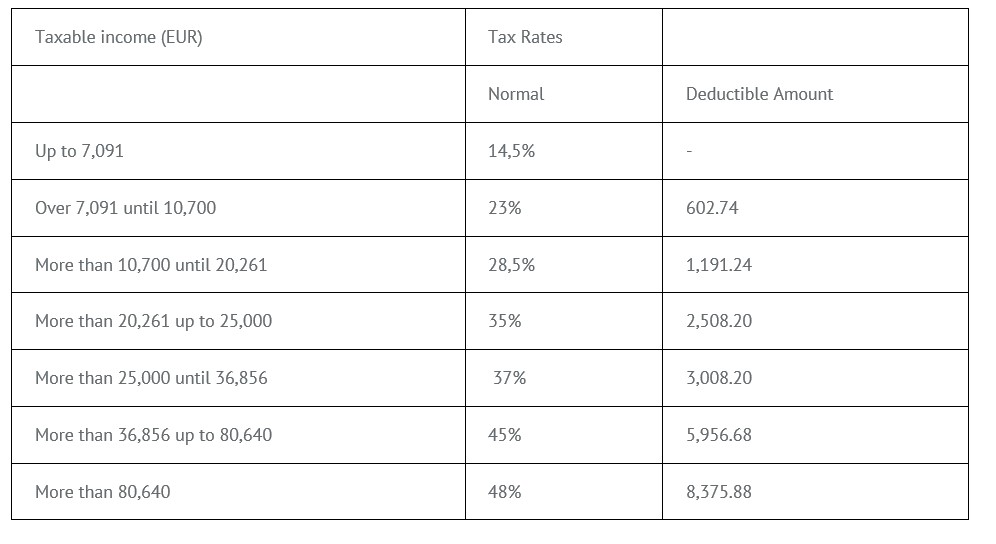

Portugal individual income tax rates are progressive up to 48%.

Income tax is payable by individuals on income obtained from employment, a business activity or independent profession, investment income, immovable property, capital gains, pensions and betting or gambling profits. Resident individuals are subject to income tax on their worldwide income while nonresidents are liable to income tax only on income sourced in Portugal. Residence is determined by physical presence in Portugal for 183 days or more in any tax year. An individual who, at the end of a tax year, owns a dwelling in Portugal that might reasonably be assumed to be the individual's usual residence, is also generally considered resident in that tax year.

When determining the taxable income, certain tax credits are allowed in addition to some specific deductions concerning each category of income. These include a percentage of expenses incurred on health and education.

Husbands and wives living together, and their dependent children, are taxed on their joint income and are jointly liable for the tax of the family unit. Normally, the tax year coincides with the calendar year but may be split in the year of marriage, divorce, separation or death.

Special rules apply for the calculation of gains on immovable property, shares or other corporate rights, securities and patents.

Exempt income includes various employment allowances (up to certain limits); a portion of pension income; capital gains from the sale of the principal private residence, when the proceeds are reinvested in another private residence; and gains on sales of qualifying shares.

Tax returns submitted in paper form are due between 1 February and 15 March of the subsequent tax year for taxpayers with income derived solely from employment or pensions or between 16 March and 30 April for taxpayers who receive any income other than from employment or pensions.

Tax returns submitted via the internet are due between 10 March and 15 April of the subsequent tax year for taxpayers with income which derives solely from employment or pension or between 16 April and 25 May for taxpayers who receive any income other than from employment or pensions.

Domestic income may attract withholding income tax. Tax withheld from residents represents a payment on account of the recipient's ultimate tax liability. However, an individual may treat tax withheld from interest on bank deposits or bonds and dividends as final tax.

Basis – Resident individuals are taxed on their worldwide income; nonresidents are taxed only on their Portuguese-source income.

Residence – An individual is resident if he/she is present in Portugal for 183 days or more in a calendar year or if, on 31 December of a given calendar year, he/she has a residential accommodation that is a permanent residence.

Filing status – Married individuals must file a joint tax return unless 1 spouse is nonresident, in which case the resident spouse files a separate tax return.

Taxable income – Income is taxed at progressive rates. There are 6 categories of income that are subject to personal income tax: wages, business and professional income, investment income, real estate income, increased asset value and pensions.

Capital gains – Capital gains arising from the sale of an individual's main residence are exempt if the proceeds are used to purchase another permanent residence in the Portuguese territory. Only 50% of gains from the disposal of immovable property are subject to tax. Capital gains on the sale of immovable assets are taxable at a rate of 10%. Capital gains on shares are excluded from taxation if they are held for more than 12 months (the exclusion does not apply if more than 50% of the company's assets are in the form of real estate in Portugal).

Tax Deductions and tax allowances – Deductions (up to specified amounts) are available, including health and education expenses, health and life insurance premiums and pension plan contributions. There are also personal tax credits that depend on marital status, the number of children and income.

There are 6 categories of income that are taxable:

1. Income

2. Business and professional income

3. Investment income

4. Real estate income

5. Increases in net worth

6. Pensions.

Other Expat Taxes Portugal

There are a few additional expat taxes Portugal enforces:

• Stamp tax of .8% on the transfer of property

• For Portuguese residents, capital gains tax is assessed on only half the value of the property and the applicable tax rate is based on your individual income. For non-residents, capital gains tax is 25%.

• Gifts and inheritances tax of 10% (plus an additional .8% if the gift is real estate)

• There is also a solidarity rate which varies between 2.5% and 5%, this applies to taxable income above EUR 80,000.

• Self-employment income is subject to a contribution tax rate of 21.4% and should be reported quarterly in April, July, October, and January.

However, there is no wealth tax.

Taxable profit up to EUR 12,500.00 is taxed at a reduced rate of 12.5% and the excess is taxed at 25% in Portugal. A municipal surtax is levied on taxable profits at rates up to 1.5% (depending on the municipality), resulting in a maximum possible aggregate tax rate of 26.5%.

There are anti-avoidance measures to prevent businesses being split up artificially between different companies to take advantage of the 12.5% rate.

General Regime: Resident corporations are subject to Portuguese corporate income tax (IRC) on their worldwide income. Resident companies are those which have their head office, or place of effective management, in Portugal.

Non-resident companies with a permanent establishment in Portugal are liable for IRC on the income attributable to that permanent establishment. A non-resident company with no permanent establishment in Portugal is taxed on the following types of income sourced in Portugal: real estate, capital gains, dividends, services, interest and royalties.

Portugal tax year usually coincides with the calendar year (1 January to 31 December). However, in some cases such as branches of non-resident companies, different tax years may be adopted.

Permanent establishments of non-resident companies are taxed at the rates applicable to resident companies (i.e. 25%), plus a 1.5% municipal surcharge (effective rate of 26.5%). When there is no permanent establishment, tax is levied at rates varying between 15% and 25% according to the source of income.

CAPITAL GAINS TAX

Worldwide capital gains obtained by resident companies are included in taxable income and taxed at the standard flat rate of 26.5%. The gain (or loss) is calculated by the difference between the sales proceeds and the acquisition cost which may be updated using official inflation coefficients. If the proceeds of the sales are reinvested in other fixed assets, 50% of the gain obtained (net of the related losses) will be excluded from taxation. For this purpose, reinvestments made in the preceding year, the year of sale and the two subsequent years will be taken into account.

When only part of the consideration is reinvested, only the corresponding part of the gain qualifies for the relief.

Gains derived from the disposal of shares by qualifying holding companies (SGPS) are not subject to taxation. However, capital losses arising on the sale of shares, as well as interest incurred on loans used to purchase shares, are not deductible for IRC purposes at the SGPS level.

BRANCH PROFITS TAX

All income attributable to the Portuguese branch (permanent establishment) is subject to corporation tax. No tax is imposed on the eventual remittances of profits to the head office.

FRINGE BENEFITS TAX (FBT)

In general, benefits provided to employees are added to their remuneration and taxed accordingly. There are, however, some exceptions such as lunch allowances, travel allowances and the use of a car (provided such use is not formally agreed in the employment contract).

MUNICIPAL TAX ON REAL ESTATE

Owners of real estate properties are subject to tax at 0.8% for rural properties and between 0.4% and 0.7% for urban properties on the notional net income derived from property. A 1% rate applies when the real estate property is owned by a resident of an offshore jurisdiction (as defined in a 'black list' published by the Finance Ministry). This tax is deductible against rental income.

REAL ESTATE TRANSFER TAX

Stamp duty is levied on many types of transactions. Real Estate Transfer Tax applies to transfer of real estate property and is normally payable by the purchaser. The rate for urban properties is 6.5% and 5% for land for agriculture. Real Estate for habitation is subject to rates varying from 0% to 6%. An 8% rate applies when the purchaser of the property is a resident of a black-listed offshore jurisdiction. Transfers of ownership, which are subject to this tax, are exempt from VAT.

DETERMINATION OF TAXABLE INCOME (IRC)

General regime: Net income, or taxable income, is arrived at by adjusting the accounting profits for non-taxed income and non-deductible expenses. As a general principle, costs are only deductible when necessarily incurred for the purpose of producing income.

Simplified scheme: Companies that a) during the previous year had a total turnover under EUR 149,639.37; and b) have not elected to be assessed under the general regime referred to above, are subject to the simplified taxation scheme. Under this scheme, taxable income is computed as follows:

- 20% of the turnover from sales of goods; plus

- 70% of the gross income from other sources

The simplified scheme was abolished from 1 January 2009, although companies granted this regime before that date may be able to use it until the expiration of the period for which the regime was granted.

DEPRECIATION

Fixed assets can be depreciated for tax purposes. The depreciation rates are set by specific legislation and include 2% for office buildings and 5% for industrial buildings. No depreciation is allowed on land. The normal method of calculation is the straightline basis but declining-balance method may be used except for items such as buildings, cars and office furniture.

CAPITAL GAINS AND LOSSES

Gains obtained by non-resident entities from the disposal of shares are exempt from tax. However, some anti-avoidance provisions apply in order to prevent abuse of this concession.

DIVIDENDS

There is a full participation exemption for payment of dividends between Portuguese resident companies when the recipient of the dividends is a company that has held a participation of not less than 10% of the share capital of the distributing company for a minimum period of one year. If such conditions are not met, 50% of the dividend amount is excluded from taxation (i.e. only 50% of the dividend amount will be subject to tax).

The full participation exemption is also available for dividends derived from other EU resident companies, provided the participation exceeds 10% of the share capital of the subsidiary and the related shares have been held for a period of one year.

Dividends paid to non-resident shareholders are normally subject to withholding tax at 20% (or at the treaty rate if applicable). When the parent company is resident of an EU Member State and has held a participation of at least 10% in the share capital of the Portuguese subsidiary, no withholding tax shall apply provided the company paying the dividend obtains a tax certificate proving that the conditions of the directive have been met.

INTEREST DEDUCTIONS

Interest is deductible on an accruals basis. The Fiscal Administration is entitled, under certain circumstances, to disallow interest payments to related parties in excess of arm's length arrangements.

In the case of loans granted by non-EU companies, interest expenses are subject to thin capitalisation restrictions.

The thin capitalisation ratio is 2:1. No relief is granted on the interest due to non-EU resident shareholders on the part of a loan that exceeds twice the participation in the equity.

LOSSES

Operating losses incurred by resident companies, or by a branch of a non-resident company, may be carried forward to set off against taxable profits for six years. No deduction is allowed in the following two situations:

(a) where the nature of the activity has changed substantially compared to when the losses were incurred

(b) the ownership of 50% or more of the share capital has changed, compared to the year in which the losses were incurred.

FOREIGN SOURCED INCOME

Taxation of resident companies takes into account their worldwide income.

TAX INCENTIVES

Incentives under Portuguese tax legislation include financial derivatives; the freetrade zones of Azores and Madeira; investment tax credits; incentives for small companies; tax credits for research and development investments; and creation of jobs for persons under 30 years of age.

RELATED PARTY TRANSACTIONS

Transfer pricing legislation enables the tax authorities to make corrections to taxable income when the conditions (and prices) agreed between related parties are different from those that would have been agreed and accepted by independent entities. Taxpayers must keep the necessary documentation to support the transfer pricing policy within the group.

WITHHOLDING TAX

Payments between resident companies are generally subject to withholding tax. The rates vary between 15% and 25%.Where payments are made by residents to non-residents, the tax rate may be reduced if there is a double tax treaty.

PORTUGAL VAT (Value Added Tax)

The standard rate of VAT in Portugal is 23%. The intermediate VAT rate is now 13%, and the reduced rate is 6%.

In the Azores, the applicable rates are 18%, 9% and 4%.

In the Madeira, the applicable rates are 22%, 12% and 5%.

Taxable transactions – VAT is levied on the supply of goods and services.

VAT Registration – A reverse-charge mechanism applies for local supplies made by nonresident entities.

Filing and payment – Monthly returns are filed when annual turnover exceeds EUR 650,000 (otherwise, quarterly returns are required). Payment is required at the time of filing. Monthly VAT returns are filed up to day 10 of the second month following the relevant month of operations. Quarterly returns are filed up to day 15 of the second month following the relevant month of operations.

US TAX FILING REQUIREMENTS

If you are a US citizen, you will still be required to file a US tax return each year. Fortunately, the US has put several deductions and exclusions in place to offset your US tax liability.

If you earned more than US$12,550 (in 2021, or $400 of self-employment income etc), you are required to file Form 1040. While taxes are still due by April 15, expats get an automatic filing extension until June 15, which can be extended further online until October 15. The expatriate Foreign Earned Income Exclusion can only be claimed if you file your tax return on a timely basis. It is not automatic if you fail to file and can even be lost.

If you had a total of at least US$10,000 in one or more foreign bank and/or investment accounts at any time during the tax year, you also have to file FinCEN form 114, otherwise known as a Foreign Bank Account Report or FBAR.

If you have overseas assets worth over US$200,000 per person, excluding your home if it is owned in your own name, you may also have to file form 8938 to declare them.

There is a US-Portugal Tax Treaty, however it doesn’t prevent expats from having to file US taxes. Some expats may be able to claim a provision in it though on specific types of income, such as dividends and royalties. If also contains a clause allowing the US and Portuguese governments to share taxpayer information, and Portuguese banks pass on US account holders’ account info to the IRS too, so it’s not worth not filing or omitting anything on your return or FBAR. The penalties for incorrect or incomplete filing for expats are steep, to say the least.

If you’re a US citizen, green card holder, or US/Portuguese dual citizen, and you have been living in Portugal but you didn’t know you had to file a US tax return, don’t worry: there’s a program called the IRS Streamlined Procedure that allows you to catch up on your filing without paying any penalties. Don’t delay though, as the program is only available before the IRS contacts you