Skip to content

Skip to content Income tax return in France

Obligation to declare worldwide incomes Income tax in France is determined on a calendar year basis. Thus, you must report income received between January 1 and December 31. The tax return must be filed at the end of May/June of the year following the receipt of your income. You must report all of your worldwide income. Double taxation of income will be avoided thanks to foreign tax credits and the tax treaty signed between France and the United States. Income from the United States that is taxable in the United States is taken into account for the calculation of the French tax.

CSG and CRDS

The Contribution Sociale Généralisée (CSG) and the Contribution pour le Remboursement de la Dette Sociale (CRDS) are two taxes levied on income in France. These taxes are intended to finance the Social Security system and repay the social debt.

These two taxes, whose overall rate is 17.2%, are mainly based on income from assets (financial income, rental income, etc.) taxable in France.

In 2019, the United States and the French Republic memorialized an understanding through diplomatic communications. This understanding stated that the French Contribution Sociale Generalisee (CSG) and Contribution au Remboursement de la Dette Sociale (CRDS) taxes are not social taxes covered by the Agreement on Social Security between the two countries.

Accordingly, the IRS will not challenge foreign tax credits for CSG and CRDS payments on the basis that the Agreement on Social Security applies to these taxes. The IRS’s change in policy means individual taxpayers who paid or accrued these taxes, but did not claim them, can file amended returns to claim a foreign tax credit.

Moving to France from the USA : you must declare the bank accounts held outside France

As a resident of France, you are required to declare any bank accounts you hold abroad (i.e., outside of France), under penalty of a fine. In France, the General Tax Code indicates that “accounts of any kind” must be declared. This encompasses several types of accounts: current accounts, savings accounts, digital asset accounts, securities accounts, term accounts, and retirement accounts, all of which must be declared.

Life insurance owned abroad

Life insurance is a financial investment for savings purposes taken out with the aim of transferring it to a beneficiary, linked to an event related to the insured. For instance, in the event of the insured’s death, the capital and interests will be transmitted to the chosen beneficiary(ies). However, if the insured is not deceased, he/she remains the sole beneficiary and has the right to freely dispose of the capital and the interests linked to the contract.

As a French tax resident, you are required to declare the life insurance policies held abroad.

Moving to France from the USA : Trust return in France

Although trusts do not exist in French law, you must report those you own abroad, if they have a connection with France. In such cases, you are required to file a declaration within one month of its creation, modification or termination . You must also declare the market value of the trust as of January 1 before June 15 of the tax year.

Is the French Special Tax Regime Retroactive?

In the context of the French tax system, the general principle is that tax laws are applied prospectively, meaning they come into effect for the tax year following their enactment. Retroactive application of tax laws is generally discouraged, as it may create uncertainty and disrupt taxpayers’ financial planning.

However, there may be exceptional circumstances where certain tax measures can have retroactive effects. These situations are typically limited to specific cases and usually arise in response to extraordinary events or to address unintended loopholes or ambiguities in the tax code.

Retroactive tax provisions are generally accompanied by specific guidelines or transitional provisions to ensure fairness and clarity for taxpayers. It’s important to consult the relevant tax laws, regulations, and official guidance provided by the French tax authorities or seek advice from a tax professional to determine the specific rules and provisions applicable to your situation.

Let’s talk About American\UK Citizen in France with a UK Structure

The French tax authorities employ four tests outlined in the Code Général des Impôts, and if any one of them is met, you will be regarded as a tax resident of France:

Test 1: If your main residence or home is in France The criterion most heavily relied upon by French authorities is whether your main home or ‘foyer’ is situated in France. This refers to the residence where your closest family members (spouse/cohabiting partner and dependent children, but excluding parents) habitually reside. If you are single and without children, it pertains to the place where most of your personal life is centered. It is not mandatory to spend the majority of your time in France for your ‘foyer’ to be located there.

Test 2: Your lieu séjour principal Translated simply as your principal place of abode, this test is typically satisfied by individuals who spend more than 183 days in France within a calendar year. However, it may also apply if you spend more days there than in any other country. This test is increasingly being employed by authorities due to the emergence of ‘tax nomads’ who cannot demonstrate tax residency elsewhere.

Test 3: Having your principal activity take place in France This third test is quite straightforward. If your primary occupation is in France (whether paid or unpaid), or if your primary income is derived from there, for example.

Test 4: Your center of economic interests This criterion is fulfilled if a majority of your significant assets (such as major investments) are located in France if your assets are managed in France, or if your business affairs are conducted there. Additionally, if you primarily earn your income in France, it will also establish it as your center of economic interest. It is important to note that the French tax authorities consider it is your responsibility to inform them and declare all of your income and assets.

Taxation for Retired American Expats Living in France with Investment Income

France and the United States have entered into a tax treaty to prevent situations of double taxation. According to this agreement, retirement pensions and similar payments are only subject to taxation in the country where they are received. Therefore, pensions originating from the United States are only taxable in the United States.

Regarding the application of Article 18 of the Tax Convention, France acknowledges the following:

1. Qualified plans under Section 401(a) of the Internal Revenue Code.

2. Individual retirement plans, including those that are part of a simplified employee retirement plan meeting the conditions of section 408(k), individual retirement accounts (IRAs), individual retirement annuities, and accounts covered by section 408(p).

3. Qualified plans referred to in section 403(a) and those referred to in section 403(b), are generally recognized as equivalent to a pension scheme established and recognized for tax purposes in France.

Tax Considerations of Freelancing in France while Working with US Clients

Many new entrepreneurs and freelancers opt for the micro-entrepreneur status (also known as auto-entrepreneur status) when starting their ventures in France. The social charges are to be paid to URSSAF, the French social contribution collector. They are calculated as a percentage based on your turnover and contribute towards predetermined funds such as maternity, healthcare, retirement, and training. In France, it is mandatory for self-employed individuals to contribute to healthcare.

The level of social contributions depends on your activity and ranges from 12.8% for purchase and resale to 22% for other activities. The two main taxes for micro-entrepreneurs are income tax and business property tax.

Income tax: Once you have an income, you must declare it. Various criteria are considered, including family size, family situation, income level, and type of income.

CFE (Contribution Foncière des Entreprises): This is the business property tax that all entrepreneurs, not just micro-entrepreneurs, must pay annually in December starting from the second calendar year of their activity. This requirement applies even to those who work from home or do not have a dedicated office, such as individuals working at client locations, and so on.

Investing in ETFs as a US Expat Living in Europe

The answer is – it depends. First, let’s consider why French residents are not supposed to purchase US ETFs. The reason is that in France, regulatory authorities are vigilant against unscrupulous individuals and require all funds sold to European residents to provide a simple document called a Kiid. This document outlines the risks and returns of the proposed investment in a few pages.

This approach makes much more sense than the American way, where investors receive a prospectus filled with complex legal language that nobody reads anyway. US ETF providers have been unwilling to furnish such a document to European investors. One reason is that the US regulator, the SEC, prohibits the presentation of “forward” returns. Therefore, if an ETF provides information to one regulator, it would violate the rules of the other.

The question then becomes whether there is a workaround to this issue, and it turns out that there is. It’s important to remember that European regulators are primarily concerned with safeguarding less experienced investors. Hence, if an individual is considered a “professional investor,” they can choose to opt out of the regulation and purchase US ETFs without the required disclosures. The term “professional investor” might sound intimidating, but the regulations define this classification as follows:

“A retail client who possesses a portfolio valued at least €500,000 (£439,000, $529,000) in liquid assets, engages in transactions with a value of more than €600 per transaction on financial instruments, and conducts a minimum of 10 such transactions per quarter on average over the past four quarters.”

Additionally, the brokerage firm must conduct an adequate assessment of the client’s competence, experience, and knowledge to ensure that the client can make investment decisions and comprehend the associated risks.

What about Transferring US Investment Accounts to Europe as an American?

Transferring a portfolio from a US platform to a European custody may be possible, but the specific process and requirements may vary depending on the platforms and custodians involved.

Are US pensions and social security taxable in France?

Individuals domiciled in France for tax purposes are required to annually report their French and worldwide income, subject to the application of international tax treaty provisions. Concerning retirement income, Article 18 of the tax treaty between France and the United States states the following:

“Amounts paid under the social security or similar laws of one Contracting State to a resident of the other Contracting State or to a U.S. citizen, as well as amounts paid under a pension plan and other similar remuneration arising from previous employment in one of the Contracting States to a resident of the other Contracting State, whether received periodically or as a lump sum, shall only be subject to taxation in the State from which they originate. For the purposes of this paragraph, pension, and other similar remuneration shall be considered to arise in a Contracting State only if paid out from a pension or retirement plan established in that State.”

In essence, the treaty establishes that pensions are taxable only in the country where they originate. Therefore, U.S.-source retirement benefits received by individuals domiciled in France for tax purposes remain taxable in the United States.

However, the Department’s response concludes with an interesting point: it reminds us that although U.S. source retirement benefits may not be subject to taxation in France, they must still be reported on the French tax return for calculating the effective tax rate. It is important to correctly declare retirement pensions in France, as double taxation on this income will be avoided through a tax credit equal to the French tax amount.

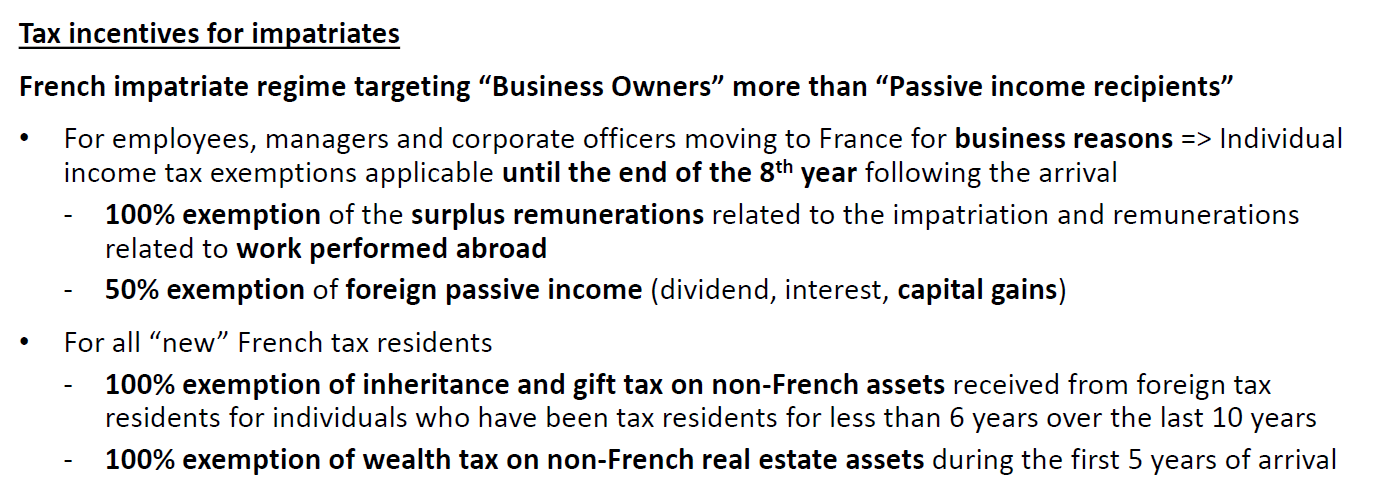

Expat Tax Regime for Americans Moving to France

Designed to attract foreign executives, the expatriate tax regime applies to employees and managers who were not residents of France for tax purposes during the five calendar years prior to taking up their duties in a French-based company. Recruitment can occur through intra-group transfers or direct hiring from abroad for a position in a French company. To qualify, the employee must have their household or primary residence in France and engage in a primary occupation there.

The special expatriate tax regime grants income tax exemptions for eight years on expatriate bonuses and the portion of compensation related to foreign activity conducted in the employer’s interest. In cases where the contract does not specify the bonus amount, a 30% flat rate of total remuneration may be assessed.

However, these tax benefits are subject to the taxpayer’s discretion and can be capped. The overall cap restricts the two elements mentioned above from exceeding 50% of the total remuneration, while another cap limits the exemption for the assignment carried out abroad to a maximum of 20% of the taxable remuneration net of the expatriate bonus.

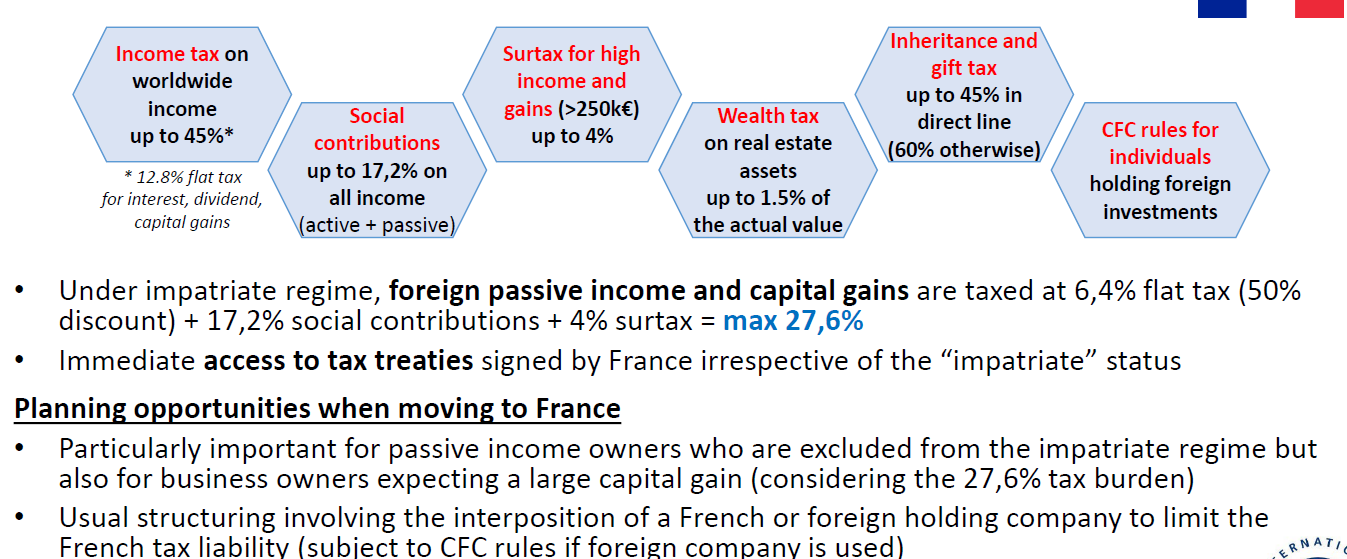

In addition to the exemption for active income, the expatriate tax regime provides a 50% tax exemption for passive income from foreign sources, such as investment income, intellectual property rights, or capital gains on securities. This exemption applies to taxpayers within the personal and temporal scope of the special expatriate tax regime.

Recently, the French Administrative Supreme Court reaffirmed these conditions (Conseil d’État, 21-10-2020, n°442799). The French Tax Authorities had imposed an additional condition, requiring the actual receipt of activity income for the benefit of the tax exemption on passive income. However, this condition was deemed invalid by the French Administrative Supreme Court.

Apart from the favorable income tax regime, new French tax residents also benefit from a favorable wealth tax regime. Article 964 of the French Tax Code (FTC) states that for a period of five years, these residents are liable for property wealth tax (Impôt sur la Fortune Immobilière) only on property and property rights located in France, thus avoiding global territorial scope for this taxation.

Why Americans Struggle to Find a Brokerage Firm or Bank in France or the US?

The issue of tax compliance and reporting obligations is a significant challenge that Americans face when finding a brokerage firm or bank in France or the US. Americans living abroad, including those in France, are still subject to U.S. tax laws and must report their worldwide income to the IRS. The complexity of tax reporting requirements for Americans abroad makes it difficult for brokerage firms or banks to provide services to them.

Financial institutions are required to comply with the Foreign Account Tax Compliance Act (FATCA), which mandates reporting information about their U.S. account holders to the IRS. The additional reporting burden and potential legal risks associated with non-compliance make some institutions hesitant to accept American clients, particularly those living abroad.

Similarly, French citizens in the US may encounter challenges in finding a brokerage firm or bank due to tax implications associated with maintaining accounts and investments in their home country while residing abroad. Navigating dual taxation and reporting obligations between the US and France adds complexity for these individuals.

These tax-related considerations contribute to the complexity of brokerage firms and banks when serving American clients in France or French clients in the US. As a result, there may be a limited number of institutions willing to offer services to individuals with cross-border financial interests.

Fixing a Dual Status Return Mistake for Americans Living in France?

You are a dual-status alien when you have been both a U.S. resident alien and a nonresident alien in the same tax year. Dual status does not refer to your citizenship, only to your residency status in the United States for tax purposes. When determining your U.S. income tax liability for a dual-status tax year, different rules apply for the part of the year you are a resident of the United States and the part of the year you are a nonresident. The most common dual-status tax years are the years of arrival and departure.

https://www.youtube.com/watch?v=tCT2wp8–9Q

Dealing with a frozen US brokerage account or account closure notice

There are several reasons for these restrictions on U.S. expat brokerage accounts, and no single factor is solely to blame. The primary rationale is likely a combination of increased U.S. regulation of financial institutions and perceived compliance risk that U.S. banks have regarding operating in certain foreign countries. This is particularly true for larger financial institutions that offer commercial and investment banking services. They do not wish to subject these core banking functions to undue regulatory oversight by serving U.S. expat retail clients.

There is no U.S. law that mandates the freezing or closure of American expat brokerage accounts when moving abroad. The decision to freeze an account is an internal policy of the financial institution. Instead of complying with these new international regulations, many U.S.-based brokers (such as UBS, Wells Fargo, Merrill Lynch, and Morgan Stanley) have chosen to close or freeze American expat brokerage accounts.

Do You Need to Pay VAT When Invoicing Clients Outside France?

If a business sells goods to a taxable person who is registered for VAT in another EU Member State and the sale involves the transportation of those goods from France (either by the supplier or the customer) to the EU Member State of the customer, the business does not need to charge VAT and may treat the transaction as a zero-rated intra-Community supply. The supplier must indicate the customer’s VAT identification number on the invoice and should retain evidence of the goods’ transportation outside of France.

If a business sells goods to a customer who is not registered for VAT in another EU Member State and the sale involves the transportation of those goods by the supplier from France to another EU Member State, the supplier will have to charge French VAT. However, under the so-called “Distance Selling Scheme,” if the supplier’s sales exceed a certain threshold applicable in the concerned EU Member State, or if the supplier waives the application of the threshold, they have to register in the EU Member State and charge the local VAT of the EU Member State of arrival.

If a business exports goods to a customer (business or private) outside of the EU and the supplier arranges the transportation of the goods, the supplier does not need to charge VAT.

The rules applicable to determining the place of supply for services have changed considerably with the implementation of the VAT Package since 1 January 2010. As a general rule, supplies of services provided by a taxable person to another taxable person for business purposes (referred to as B2B services) are deemed to be located at the place of business of the recipient or at the place of the fixed establishment for which the services are rendered.

Furthermore, the place of supply for services provided to recipients who are non-taxable persons or do not receive such services for their business (referred to as B2C services) is considered to be the place of establishment of the business providing the services. If a fixed establishment of the supplier provides the services, the place of the fixed establishment is considered the place of supply.

Can I open an IRA or Roth IRA while living in France?

Yes, a U.S. citizen living abroad can have both a traditional and/or Roth IRA. The restrictions only apply to making contributions. So, if you had an existing IRA before you moved abroad, you don’t have to get rid of it or transfer assets, but you may not be able to add to it while you’re overseas.

Tax Considerations for American Investing in PEAs and PERs in France

The PEA (Plan d’Epargne en Actions) and PER (Plan d’Epargne Retraite) are both investment vehicles in France, but they have different purposes and tax advantages.

PEA (Plan d’Epargne en Actions): The PEA is a tax-advantaged investment account designed to encourage long-term investments in French and European stocks.

Here are some key features of the PEA: It is available to French tax residents only. Investments in eligible stocks and equity-based financial instruments can benefit from tax advantages. After a holding period of five years, capital gains and dividends generated within the PEA are tax-free. However, if you withdraw funds from the PEA before the five-year holding period, there may be tax consequences.

PER (Plan d’Epargne Retraite): The PER is a retirement savings plan that allows individuals to build up savings for their retirement. Here are some key features of the PER: It is available to both employees and self-employed individuals in France. Contributions to the PER are tax-deductible, which means they reduce taxable income. The funds invested in the PER are not taxed until they are withdrawn during retirement.

Tax Implications for US Expat’s Gift to French Girlfriend

Like with any of the U.S. transfer taxes, it is important to ascertain the taxpayer’s tax domicile. Whether a person is a U.S. resident or not for U.S. transfer tax purposes will hinge on a facts and circumstances test.

The key to U.S. transfer tax residency is the concept of “domicile” and whether one is considered to be domiciled in the U.S. due to an intent to remain indefinitely in the U.S. The test is subjective, and the case law has provided some surprising results. Some of the factors courts have considered include the possession of a green card or the type of visa an individual holds, the location of the principal residence and family members, the location of the business, declarations of residency in documents such as voter’s registration, driver’s license, wills, or deeds, the location of a person’s financial accounts, and the center of their social life.

Investments US Expats Need to Avoid When Living in France

The PFIC tax regime was created via the Tax Reform Act of 1986 with the intent to level the playing field for US-based investment funds (i.e., mutual funds).

Prior to the legislation of 1986, U.S.-based mutual funds were forced to pass through all investment income earned by the fund to its investors (resulting in taxable income). In contrast, foreign mutual funds were able to shelter the aforementioned taxable income as long as it was not distributed to its U.S. investors.

After the passage of the Tax Reform Act of 1986, the main advantage of foreign mutual funds was effectively nullified by a tax regime that made the practice of delaying the distribution of income prohibitively expensive for most investors.

To employ this punitive regime, the IRS requires shareholders of PFICs to effectively report undistributed earnings by choosing to be taxed through one of three possible methods: Section 1291 fund, Qualified Election Fund, and Mark to Market election.

Navigating Forced Heirship: 3 Effective Strategies

France has a system of forced heirship whereby a deceased’s children are entitled to a minimum share of the estate. This minimum share is generally between half and three quarters of the estate, depending on the number of children who survive their parent.

The entitlement of a surviving spouse can be complicated, especially where the deceased has children from a previous marriage. These children might not be pleased that their stepparent can claim a lifetime interest over the property. It is usual for a surviving spouse either to inherit a minority interest in French property owned by their deceased spouse or a life interest. However, it is possible to vary the usual rules by holding French property en tontine, which is broadly similar to an English joint tenancy arrangement.

France also applies a matrimonial property regime. This regime governs how property is held between spouses and can have implications on tax and estate planning as well as on divorce.

What are the Main Types of Companies in France?

The form of a company also impacts the tax and social security systems of the income derived from the activity.

SARL: Commonly used for business creation in France, SARL offers a simple structure with partners’ liability limited to their contributions. No minimum capital is legally required.

EURL: A special category of SARL with only one shareholder. Its profits are taxed on income tax in the shareholder’s name, with an option for corporation tax.

SELARL: Adapted for liberal professions, SELARL’s rules are similar to SARL but consider the ethics of the professions for which they were created.

SA: Composed of at least two shareholders (seven if listed on the stock exchange), SA requires a minimum share capital of 37,000 €. It’s headed by a President, CEO, and a Board of Directors. Shareholders’ liability is limited to their contributions.

SAS: A new form of company, SAS has no minimum capital requirement. It can be constituted with only one partner. The law allows shareholders to freely organize their operations in the articles of association.

SASU: A special category of SAS with only one partner. Few operating rules differ from SAS.

SNC: Rarely used as it doesn’t protect shareholders’ assets. Constituted without minimum capital, by at least two partners. The SNC’s results are taxed at the level of its shareholders for income tax unless the company opts for corporation tax.

SCP: Allows several individuals practicing the same liberal profession to exercise it collectively.

They are indefinitely liable for the company’s debts. No minimum capital is required. The SCP’s profits are taxed on income tax at the level of each partner. The associative form for developing a company should be used with caution. In most cases, it’s not the most suitable structure and can pose certain risks. It’s important to thoroughly evaluate the specific needs and objectives of the company before deciding on its legal structure. Consulting with a legal or business professional can provide valuable guidance in this process.

Understanding the MTG Tax: France’s Tax on Gratuitous Transfers.

France imposes a tax on gratuitous transfers, known as the MTG tax, which applies to gifts or inheritances. The recipient is generally responsible for paying this tax and filing a return. The tax rates are determined based on the relationship between the transferor and the transferee.

Transfers to direct descendants, spouses, and domestic partners are taxed at lower rates, with graduated rates ranging from 5 percent to 45 percent, depending on the net taxable value. In contrast, transfers to brothers and sisters are taxed at 35 percent or 45 percent, to other family members up to the fourth degree of relationship at 55 percent, and to more remote family members and non-relatives at 60 percent.

All worldwide assets are generally fully subject to the French MTG tax if either the donor or decedent has his fiscal domicile in France, or the inheritor, donee, or legatee has his fiscal domicile in France and has had his fiscal domicile in France for at least six of the 10 years preceding the year of the transfer. However, under Article 8 of the U.S.-France Succession and Gift Tax Treaty, if the donor, deceased, or settlor is a resident of the United States, the French donee, heir, or trust beneficiary isn’t taxed except on French situs real estate, tangibles, and business property.

The MTG tax applies in the normal way if the transfer from the trust is considered to be a transfer by gift or succession under French law. Assets of a trust are subject to the MTG tax, without regard to whether a gift has technically been completed under the laws of a common law jurisdiction. This applies in two scenarios:

On transmission or at the death of the settlor or deemed settlor-beneficiary.

If the beneficiary of a trust, as defined in the Code général des impôts (CGI), has his fiscal domicile in France (except as provided otherwise by a tax treaty).

COMMENTS ON THE BLACK LIST A FRENCH PERSPECTIVE

The French government maintains its own blacklist of tax havens. From a French perspective, transactions with non-cooperative states and territories are heavily taxed or treated differently. As of May 2023, there are 14 countries on this list, and at least two more will be added in 2024. Some countries may also be removed from the list.

Starting from 1 May 2023, the French list has included 14 jurisdictions: American Samoa, Anguilla, the Bahamas, the British Virgin Islands, Fiji, Guam, Palaos, Panama, Samoa, Seychelles, Trinidad and Tobago, the Turks and Caicos Islands, the US Virgin Islands, and Vanuatu.

The French tax haven list is updated at least once a year by means of a decree, which is generally published during the first quarter of the year. When updating its blacklist, France takes into account the countries added by the European Council to the EU blacklist, as stipulated in Article 238-0 A of the French Tax Code.

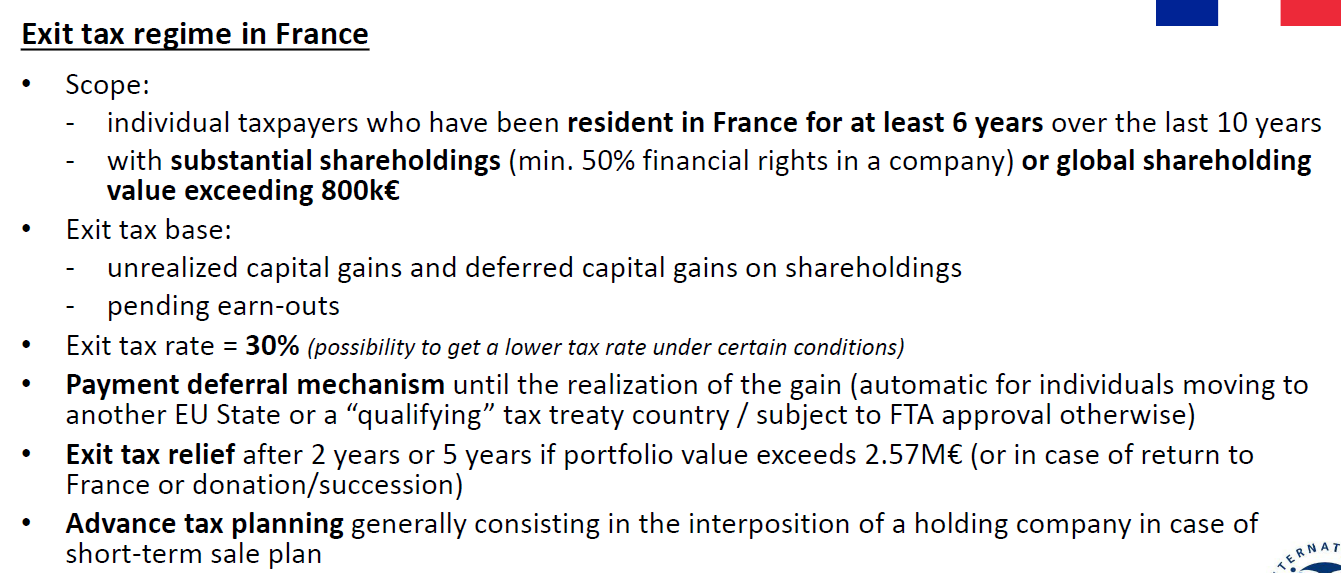

The French Exit Tax: What You Need to Know

After spending 6 years or more in France, investors could be subject to exit taxation if they transfer their residence outside of France. In such cases, they would be taxed on unrealized capital gains if they hold more than 50% in a company or if the total value of their stock exceeds €800,000.

The payment of the tax, which is 30%, may be deferred depending on the state to which the residence is transferred.

Relief from exit taxation may be available to taxpayers if they retain their stocks or shares for 5 years following the transfer of residence, or if they move back to France. The holding period is even reduced to 2 years if the shares subject to exit tax are valued at less than €2.57 million