Skip to content

Skip to content Accounting Outsourcing

It’s often difficult and expensive to find experienced personnel who can handle complicated institutional reporting functions. We pride ourselves on offering these types of sophisticated accounting services to clients on an outsourced basis. Our team has many years of experience and offers the focus and attention that in-house teams with competing priorities often cannot. Our strength lies in the presence of our regional support facilitating our clients’ growing business. We focused on enduring business value and with the depth of regional support; we have the experience coordinating with other regional offices to tailor services focusing on the international dimension.

Why Us

Most international accounting firms are networks of independent member firms. That includes the “Big 4” accounting firms of PWC, Deloitte, E&Y and KPMG. Moores Rowland in the Asia Pacific or MRAP is no different. Through our office in Singapore, HTJ.Tax is a member of MRAP – https://mooresrowland-asiapac.com/

Established in 1866 in England, the Moores Rowland brand is a well-known one in the Accounting world. Moores Rowland in the Asia Pacific has around 2000 professional staff in over 30 offices in 15 countries primarily in Asia, but through HTJ.Tax we have a presence in Europe and the Middle East as well. This is an important point as it indicates that unlike other US practices, we are not America centric. We think globally. Our team is multicultural, multilingual, accustomed to operating in different time zones (including US time zones) and accustomed to the cultural differences required to serve international clients.

Individual clients come to us with complex, multi-jurisdiction tax issues related to cross-border employment and investment opportunities. Similar to an interpreter or guide who helps travelers understand the language and customs of a particular country, we explain tax and accounting concepts and laws that are foreign to our clients.

More specifically, we prepare U.S. federal and state income tax returns for individuals and corporate entities. Our international tax consulting expertise includes analysis of tax treaties, sourcing of income, and reporting of foreign bank accounts, as well as foreign corporations, partnerships and trusts. As consultants, we help individual clients develop cost-effective strategies, propose solutions, and prepare individual tax projections. We also work closely with our clients’ attorneys and other advisors to provide comprehensive advice.

Lastly, we have significant experience assisting our clients with complicated, international tax issues.

US GAAP is rules based while IFRS is standards based so the theoretical framework and principles of IFRS leave more room for interpretation and sometimes require lengthy disclosures on financial statements. Fortunately, as an international accounting team we are conversant in both standards.

- Cash Flow statement. US GAAP and IFRS differ particularly in how they classify interest and dividends. With US GAAP, interest paid and received, and received dividends are listed under the operating section, while dividends paid are listed in the financing section. With IFRS, all interest and dividends can be listed under the operating or financing section.

- Balance Sheet. US GAAP requires assets in order of liquidity, with the most liquid assets listed first. IFRS suggests putting assets in the opposite order of liquidity, with the least liquid assets listed first—that is, non-current assets, current assets, owners’ equity, non-current liabilities, and current liabilities.

- Asset Revaluation. US GAAP only allows the revaluation of fair market value for marketable securities (i.e., investments and stocks). IFRS allows for the revaluation of more assets, including plant, property, and equipment (PPE), inventories, intangible assets, and investments in marketable securities.

- Inventory write down reversals. A company’s inventory may lose value over time. An asset may, for example, lose value because of market or technological factors, which classifies it as a “loss on impairment.” Both US GAAP and IFRS require that businesses write down their inventory as soon as its cost exceeds its net realizable value (i.e., how much the inventory is expected to generate when sold). While a loss is often permanent, the value of an asset may increase again if the impairing factor is no longer present. US GAAP doesn’t allow companies to re-evaluate the asset to its original price in these cases. In contrast, IFRS allows some assets to be evaluated up to their original price and adjusted for depreciation.

We have significant experience assisting our clients with complicated, international tax issues. The following list represents some of the areas in which we have provided both planning and compliance services for our clients:

- US shareholders of foreign corporations

- US partners in foreign partnerships

- US grantors and beneficiaries of foreign trusts

- US shareholders of Passive Foreign Investment Companies (PFICS)

- Reporting for Foreign Bank and Financial Accounts (FBARs)

- Blocked income reporting for deferral of tax in currency restriction situations

- Donations to foreign charities by US private foundations via expenditure responsibility grants

- Income tax treaty analysis for various issues including determination of residency, re-sourcing of income to avoid double taxation, reduction or exemption of tax

- Determination of residency for income tax purposes for foreign nationals including optimization of elections for first and last year of residency

- Social Security tax implications to compensation of foreign nationals and US expatriates including application and analysis of Totalization agreements

- Foreign tax credit optimization including analysis of paid versus accrued methods and maximizing foreign source income

- Optimization for US expatriates including analysis of foreign tax credit versus foreign earned income exclusions

- Reporting of foreign rental properties including proper depreciation methods and treatment of rental of principal residence

- Reporting and planning for nonresidents with US investments or US effectively-connected income

- State residency and domicile issues for foreign nationals and US expatriates

- Reporting gifts and inheritances from nonresidents

- Consulting to employers of international assignees relating to tax equalization policy development and application, tax planning for international assignments including coordination with tax advisors in local jurisdictions, compensation structuring, payroll reporting and employee education and tax return preparation

- Determination of residency for US citizens in US possessions

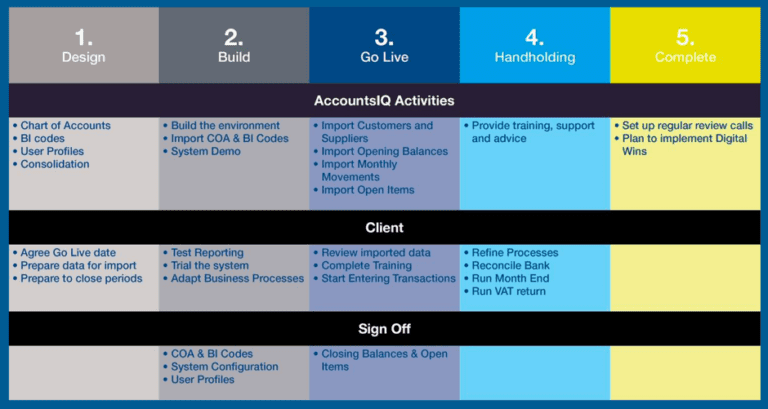

The Three Phases in the Outsourcing of your Accounting Function

Phase 1 – Documenting your existing process

Under this phase we get access to your existing bookkeeping system and your existing staff. We create what is essentially an accounting manual which explains who does what, when and how. This includes screen shots from your existing system to show step by step how they gather data from source documents and eventually produce periodic financial reports for both internal and external consumption.

To do this, we need full and unfettered access to your existing accounting system. We also interview staff and secure job descriptions from the Human Resources department. This process should take a month but could be done sooner for simpler companies. It could take longer for more complex business models

Phase 2 – Creating a Shadow Accounting Department and SLA

Once we understand your system inside out, we then create a shadow accounting department where we have members of our team mirror your existing team. Despite us having a complete shadow accounting department, you as a client would always have a single point of contact.

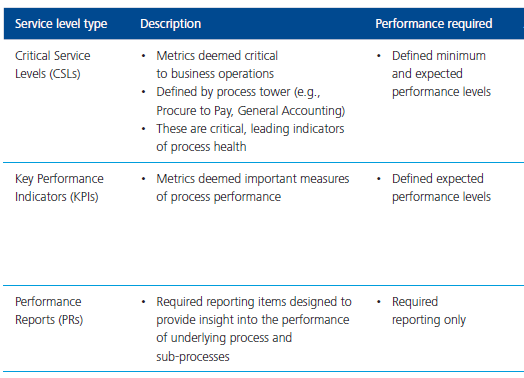

A well-written service level agreement (SLA) stands as a critical component of the relationship between a client and us as the BPO (Business Process Outsourcing) provider. At its simplest level, it ensures everyone is on the same page – protecting the client and provider with mutually agreed-upon terms, guidelines, and metrics that enable everyone to meet expectations and work productively.

But confusion often swirls over the difference between contractual SLA metrics and the broader canvas of key performance indicators (KPIs) that BPO providers can also use to monitor operations – and why it’s important to have both. SLAs in the BPO industry are ultimately determined by the unique needs of an organization and the metrics that matter most to its success.

This phase can take about a week for simple organizations but several months for more complex ones.

Here is what you would find in our standard SLAs

Phase 3 – Parallel Implementation then Cutover

This phase we essentially create a new accounting manual which shows how we will operate the function to ensure that we hit the SLAs agreed in phase 2. This is also the phase where we implement the new process. First in parallel to ensure that the new system is accurate and timely. For finance, there is no need to say that the numbers need to be accurate, and we only know this once we both stress test and accuracy test the new system against the old system. Once we are all confident, then we do a complete cutover to the new system.