Skip to content

Skip to content Here’s how we can help you

- Option 1 – For $1000, we can review your last 5 years of tax returns to ensure that there are no outstanding issues that would jeopardise your expatriation

- Option 2 – For $3000, we can create a mathematical model to help you calculate your present exit tax exposure and make recommendations on how to reduce it

- Option 3 – For $500, we offer a 1 hour Zoom call to answer questions you may have on any of the tax aspects of renouncing your US citizenship or surrendering your Lawful Permanent Residence status (Green Card Status)

Contact us at help@htj.tax

Insights on Pre-Expatriation Tax Planning

Every year, more and more US citizens renounce their citizenship, and green card holders give up their visa status. These actions could well trigger a tax problem: the US Expatriation Tax Regimes. The Expatriation Tax Regimes has two significant underlying components; the “Exit Tax” (IRC s.877a) and the “Inheritance Tax” (IRC s. 2801).

Most have heard of the Exit Tax. Few have heard that the Heart Act added a new federal transfer tax, which imposes an “Inheritance Tax” on certain gifts or bequests (testamentary dispositions) made by a “covered expatriate” to U.S. recipients. The Inheritance Tax is payable by the recipient of the gift or bequest, not the expatriate. There is no expiration of the potential applicability of §2801. Thus, a gift or bequest made by a covered expatriate several years (or longer) after expatriation could trigger the tax.

The Inheritance Tax is imposed in addition to the mark-to-market tax paid by the covered expatriate upon exit. Currently, the tax rate imposed by §2801 is 40% of the value of the gift or bequest.

Now let’s return to the Exit Tax. The US Expatriation Tax Regime Exit Tax rules impose an income tax on certain people called “Covered Expatriates” who have made their exit from the US tax system. The defining feature of the Exit Tax is that all worldwide appreciated assets are treated “as if” they are sold on the day before citizenship or resident status is terminated. If applicable, net capital gain (after an exclusion amount of roughly $821,000 in 2023) from the deemed sale is taxed when the expatriate’s final US tax return for the year of expatriation is filed.

There are other rules that accelerate income for a person leaving the United States. These other rules apply to items such as IRAs, pensions, deferred compensation plans, and beneficial interests in trusts.

———————————————————–

Not yet convinced we can help you? Here’s more.

Are you a covered expat?

Long-Term Permanent Resident (Green-Card Holder) — An expatriated green-card holder is subject to §877A as a covered expatriate only if a long-term permanent resident prior to expatriation. A long-term lawful permanent resident is a person who has been a green-card holder during eight of the previous 15 years prior to expatriation. If a green-card holder expatriates before this eight-of-15-year test is met, §877A does not apply. A U.S. resident alien (under the U.S. substantial presence income tax test)[9] is not subject to the §§877 or 877A tax if the resident has no green card.

Statutory Tests — Section 877A applies to only covered expatriates who meet any one of the three tests, set out in §877(a)(2)(A)-(C).

1) The Net Worth Test: Having a net worth of $2 million or more on the date of expatriation. The $2 million threshold considers all assets worldwide. The expat is considered to own any interest in property that would be taxable as a gift under Ch. 12 of the code (i.e., the gift tax provisions) if the individual was a citizen who transferred that interest immediately prior to expatriation.

2) The Average Annual Income Tax Liability Test: Earning an average annual net income tax for the five years ending before the date of expatriation of more than a specified amount, adjusted for inflation ($171,000 for 2020).[12] An individual who files a joint tax return must take into account the net income tax reflected on the joint return.

3) Failure to Certify Tax Compliance: Failure to certify satisfaction of federal tax compliance to the Secretary of Treasury for the five preceding taxable years or failure to submit such evidence of compliance as “may be required.” Individuals without considerable assets or income may nonetheless become covered expatriates by failing to certify tax compliance.

Special Deferral Rules of §877A(b) — The exit tax deemed sale or distribution may leave insufficient liquidity to cover the tax, as no actual sales proceeds are available. Under certain circumstances, payment of the tax may be deferred until an actual sale of the property (or death). Section 877A(b) provides detailed rules permitting a covered expatriate to defer payment of the mark-to-market tax (on a property-by-property basis). Payment is tolled until the property is actually sold or exchanged, death, or the security required to make the deferral election fails to meet statutory requirements (whichever is earlier). To make the deferral election, the covered expatriate must provide “adequate security” and agree to pay statutory interest on the deferred tax. If the covered expatriate elects deferral, gains deferred are based on the value of property as of the taxing date (i.e., as of the day prior to expatriation).

Under the §877A mark-to-market regime, a covered expatriate with an interest in a nongrantor trust (or certain deferred compensation assets) must annually file Form 8854. Form 8854 reflects distributions from the trust. The filing requirement appears to have no time limit under IRS Notice 2009-85. The notice also affirms that a covered expatriate must file a Form 1040-NR in the event he or she earned taxable income and U.S. income taxes are not fully withheld at the source. As foreign institutions or persons will likely not withhold at the source (under §1441), this requirement usually creates a mandatory filing obligation for covered expatriates. Lastly, Notice 2009-85 affirms that a covered expatriate with a beneficial interest in a nongrantor trust (or deferred compensation asset) must file Form W-8CE (which identifies the payor). This filing is required on the earlier of the date of the first distribution from the trust (subsequent to expatriation) or 30 days after the date of expatriation.

Potential Planning Strategies

• Outright Gifts to Spouse and Others — The proposed expatriate may gift assets sufficient to reduce his or her net worth below the $2 million net worth test (for characterization as a covered expatriate). For example, before expatriation, an expatriate may use the §2503(b) annual exclusion (currently $15,000 per donee) to make non-taxable gifts or, alternatively, make larger gifts by utilizing his or her unified estate and gift tax credit.

Gifts should be made at least three years prior to expatriation to avoid §2035, which adds the value of gifts made within three years of a decedent’s death (or deemed expatriation death) to the deceased’s taxable estate. Unless an exception applies,all gifts made during the three years prior to expatriation are not only included as assets subject to deemed sale, but are likely included in calculating the inheritance tax. A potential expatriate may also make unlimited tax-free gifts to a U.S. citizen spouse (prior to expatriation). Interspousal gifts are generally not subject to the three-year “clawback” rule of §2035. If, however, the recipient spouse is also expatriating, the marital gifting strategy will function only if the recipient spouse avoids covered-expatriate status. Otherwise, the proposed transfers will subject the spouse to §877A.

For potential non-citizen covered expats (long-term green-card holders), another possible strategy (to avoid U.S. transfer taxes on foreign assets) is to make transfers after permanently departing the U.S. (but before actually expatriating). Although the green-card holder would remain a U.S. resident for U.S. income tax purposes, domicile (for estate and gift tax purposes) may be moved outside the U.S. Transfers made while a non-resident, non-citizen for estate and gift tax purposes are not subject to U.S. transfer taxes, unless the property gifted is tangible and located in the U.S.[ Under such circumstances, the mark-to-market tax regime may arguably be avoided on assets gifted (three years before expatriation) and completely avoided if the gifts sufficiently reduce new worth.

• Gifts to Trusts/General Transfer Tax Strategies — As a permanent legal resident (green-card holder), the future covered expatriate (domiciled in the U.S.) may take advantage of a full unified estate and gift tax credit by implementing general U.S. transfer tax avoidance strategies before expatriation (three years before expatriation). These include utilizing valuation discounts for potential transfers, gifts to domestic irrevocable trusts, grantor retained annuity trusts, qualified personal residence trusts, intentionally defective grantor trusts (with the toggle-off switch), charitable lead trusts, charitable remainder trusts, etc.

• Use of an Expatriation Trust — As an alternative to outright gifts or other general estate tax-saving vehicles, a potential expatriate may fund an irrevocable (self-settled) trust for himself, his spouse, and descendants. Gifts to a properly structured “expatriation trust” may likely be used to lower net worth (to avoid the $2 million net worth threshold).

One strategy is to establish an expatriation trust, to reduce the potential expatriate’s net worth below the $2 million net worth test. The expatriation trust should be formed as an irrevocable nongrantor discretionary U.S. domestic trust in a state permitting self-settled discretionary trusts. The expatriation trust should be drafted to complete the transfer for U.S. transfer tax purposes (harvesting the settlor’s unified credit). The trust must also qualify as nongrantor for U.S. income tax purposes (with trust income taxed to the trust). To avoid potential inclusion under §877A, the potential expatriate should also release any powers over trust assets (i.e., powers of appointment). As this vehicle remains a domestic trust under §7701, §684 (deemed mark-to-market sale) would not apply to the transfer of assets into the trust. The potential expatriate may retain the ability to remove and replace independent trustees. Following the passage of three years from funding, §877A would not apply to the assets held in trust. Moreover, future distributions from the expatriation trust to U.S. beneficiaries (or the expatriate) would also avoid the §2801 inheritance tax .

• Use of Domicile Planning — Alternatively, as discussed above, the non-citizen settlor may utilize foreign domicile transfer tax planning before expatriating. While maintaining U.S. income tax residency, the proposed expatriate establishes domicile outside the United States. Transfers of non-U.S.-situs assets are then not subject to U.S. transfer tax. Moreover, the transfer of certain U.S.-situs intangible assets avoids U.S. gift tax (including gifts to U.S. donees). For a resident alien with substantial non-U.S. assets and U.S.-situs intangibles, U.S. transfer tax may be avoided. Following the passage of three years from such transfers, §877A does not apply the deemed sale rule to the assets transferred. This strategy may also permit the potential expatriate to completely avoid the exit tax (if transfer brings his or her net worth below $2 million).

• Sale of Personal Residence — The sale of the expatriate’s personal home (prior to expatriation for cash), removes the value of the home from the $2 million net worth test. The actual sale prior to expatriation reduces net worth and avoids taxable gain. Note that, in the event of a deemed sale of the homestead upon expatriation, the popular §121 income tax exclusion (excluding gain from the sale of a personal residence) is likely not available to a covered expatriate.

Conclusion

U.S. citizens and long-term residents must carefully plan for any proposed expatriation from the U.S. abandonment of U.S. citizenship or long-term residency triggers both the exit tax and the inheritance tax. The current form of exit tax deems sold all assets held worldwide by the expatriate. Tax may be potentially avoided by limiting income and net worth (through gifts, transfer tax avoidance strategies, and sale of the principal residence).

Deciding on expatriation Should you surrender your US passport or green card?

A. THE IMMIGRATION & NATIONALITY ACT

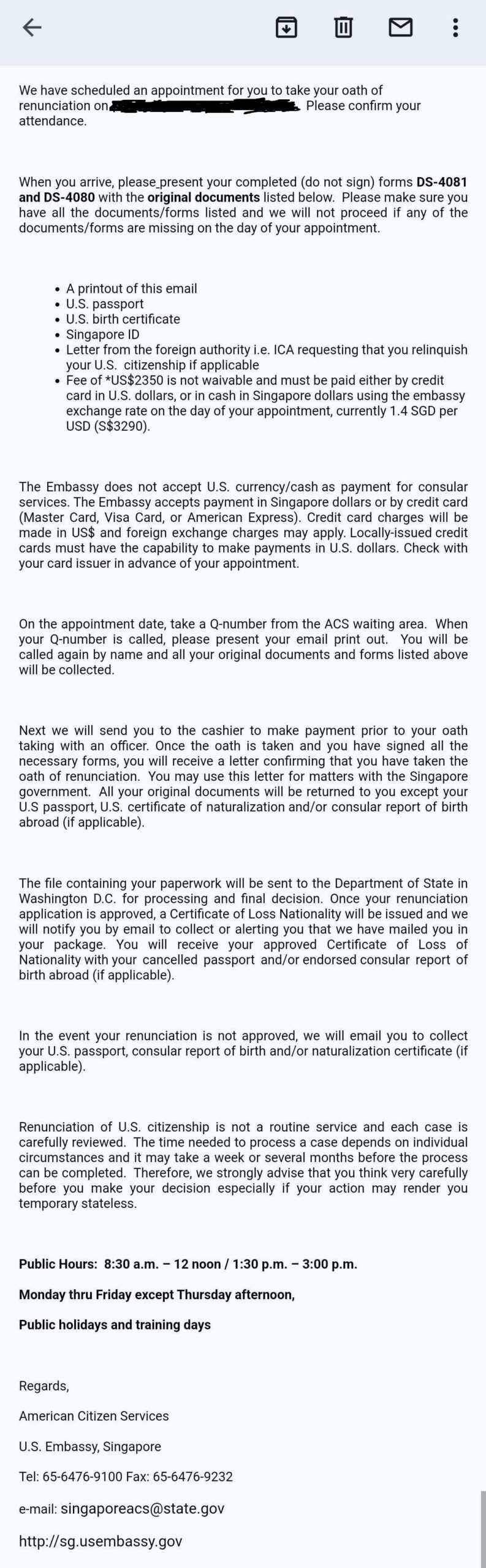

Section 349(a)(5) explains how a United States citizen can give up their U.S. citizenship while living abroad. This section states that a person can lose their nationality by choosing to give it up in a formal way before a diplomatic or consular officer of the United States in a foreign state, in such form as prescribed by the Secretary of State.

B. ELEMENTS OF RENUNCIATION:

To give up U.S. citizenship, a person must choose/want to do so, go in person to see a U.S. consular or diplomatic officer in a foreign country at a U.S. Embassy or Consulate, and sign an oath saying they want to give up their citizenship. A person cannot give up their citizenship in another way, such as by mail, on the Internet, or through someone else. In fact, U.S. courts have said that some attempts to give up U.S. citizenship do not count for various reasons.

C. REQUIREMENT: RENOUNCE ALL RIGHTS AND PRIVILEGES:

A person who wants to give up their U.S. citizenship must also give up all the rights and privileges that come with being a U.S. citizen.

D. DUAL NATIONALITY / STATELESSNESS:

People who want to give up their U.S. citizenship should know that unless they already have citizenship from another country, they might not have any citizenship at all. This means they will not have the protection of any government and might have trouble traveling because they will not have a passport from any country. Not having any citizenship can cause many problems, such as having difficulty owning or renting a place to live, getting a job, getting married, getting medical help or other benefits, or going to school. Those who renounced their citizenship will need a visa to travel to the United States or show that they can enter the country without a visa under the Visa Waiver Program. If they cannot get a visa, they might never be able to go back to the United States again.

E. TAX & MILITARY OBLIGATIONS / NO ESCAPE FROM PROSECUTION:

People who want to give up their U.S. citizenship should know that it does not change their liabilities on taxes or military service (they can ask the Internal Revenue Service or U.S. Selective Service for more information).

Also, giving up U.S. citizenship does not mean someone cannot be punished for breaking United States law or that they do not have to pay back the money they owe, including child support payments.

F. Can a Non Resident Alien (NRA) Eliminate the US Taxes withheld upon withdrawing money from an IRA or 401(k)

It is common for individuals to have pension accounts arising from a temporary work assignment and they are concerned with the U.S. withholding tax of 30%. They are also concerned about the 10% early withdrawal penalty.

Taxation of Distributions from IRAs and 401(k) Plans Under U.S. Federal Tax Law

Under the Internal Revenue, any distribution from a qualified plan such as an IRA or 401(k) plan that does not qualify as an eligible rollover-distribution is generally subject to mandatory income tax withholding. Although IRA and 401(k) plan distributions are subject to a 20% withholding tax, depending on the participant’s marginal tax bracket, the U.S. income tax assessed on the withdrawal could be significantly higher. In addition, Internal Revenue Code Section 72(t) imposes a 10% additional income tax on some distributions to individuals that have not reached the age of 59 ½.

The Effect of Income Tax Treaties

Tax treaties may provide an additional legal forum for the taxation of distributions from qualified plans. In certain cases, non-resident participants of qualified plans can reduce or even eliminate U.S. tax associated with a distribution from an IRA or 401(k) plan.

In order for a non-resident to utilize a tax treaty to reduce or eliminate the U.S. tax consequences associated with an IRA or 401(k) plan distribution, the non-resident must reside in one of 58 countries that have an income tax treaty with the United States.

What is the process of cashing out a 401(k)?

First tell the custodian that you want to withdraw your 401(K) and to provide you all necessary paperwork. Then make sure you fill out correctly and provide a U.S. form W-8BEN to the withholding agent in order to benefit from a lower tax treaty rate if one exists. The tax treaty article number and the withholding rate must be included to claim the treaty benefit upfront. The withholding agent is required to report the payment and the tax withheld, if any, on the IRS Form 1042-S. The withholding agent has until March 15 (or the next business day if the 15th falls on Saturday, Sunday or a federal holiday) to provide you and the internal revenue service a copy of the Form 1042-S. Be sure to ask if form 1042-S or Form 1099-R will be issued to you.

Will a 10% early withdrawal penalty apply to nonresidents who are under 59 and 1/2?

If you take an early distribution before you turn 59 ½, you generally are subject to an early withdrawal penalty of 10%, unless an exception applies. However, if you separate from service after reaching Age 55, payments received from the Plan are generally not subject to the Early Withdrawal penalty.

If there isn’t an income tax treaty, you may still fill out the W-8Ben to indicate your tax status as a foreign national. Therefore, without a treaty providing a lower tax rate, the withholding agent may withhold and remit 30% of income tax from the 401(k) lump-sum withdrawal. However, because your contributions were from U.S. source income, they are effectively connected income. The growth portion is FDAP income and it is subject to 30% tax rate. In this case, you may request partial tax refund

If you are not a U.S. citizen with a U.S. IRA or 401(k) and expect to depart the United States or have already departed the United States, contact us to discuss your options.