Skip to content

Skip to content (a) Purpose and scope. This section provides rules for making the annual election under section 1294. Under that section, a U.S. person that is a shareholder in a qualified electing fund (QEF) may elect to extend the time for payment of its tax liability which is attributable to its share of the undistributed earnings of the QEF. In general, a QEF is a passive foreign investment company (PFIC), as defined in section 1296, that makes the election under section 1295. Under section 1293, a U.S. person that owns, or is treated as owning, stock of a QEF at any time during the taxable year of the QEF shall include in gross income, as ordinary income, its pro rata share of the ordinary earnings of the QEF for the taxable year and, as long-term capital gain, its pro rata share of the net capital gain of the QEF for the taxable year. The shareholder’s share of the earnings shall be included in the shareholder’s taxable year in which or with which the taxable year of the QEF ends.

(b) Election to extend time for payment –

(1) In general. A U.S. person that is a shareholder of a QEF on the last day of the QEF’s taxable year may elect under section 1294 to extend the time for payment of that portion of its tax liability which is attributable to the inclusion in income pursuant to section 1293 of the shareholder’s share of the QEF’s undistributed earnings. The election under section 1294 may be made only with respect to undistributed earnings, and interest is imposed under section 6601 on the amount of the tax liability which is subject to the extension. This interest must be paid on the termination of the election.

(2) Exception. An election under this § 1.1294-1T cannot be made for a taxable year of the shareholder if any portion of the QEF’s earning is includible in the gross income of the shareholder for such year under either section 551 (relating to foreign personal holding companies) or section 951 (relating to controlled foreign corporations).

(3) Undistributed earnings –

(i) In general. For purposes of this § 1.1294-1T the term undistributed earnings means the excess, if any, of the amount includible in gross income by reason of section 1293(a) for the shareholder’s taxable year (the includible amount) over the sum of (A) the amount of any distribution to the shareholder during the QEF’s taxable year and (B) the portion of the includible amount that is attributable to stock in the QEF that the shareholder transferred or otherwise disposed of before the end of the QEF’s year. For purposes of this paragraph, a distribution will be treated as made from the most recently accumulated earnings and profits.

(ii) Effect of a loan, pledge or guarantee. A loan, pledge, or guarantee described in § 1.1294-1T(e) (2) or (4) will be treated as a distribution of earnings for purposes of paragraph (b)(3)(i)(A). If earnings are treated as distributed in a taxable year by reason of a loan, pledge or guarantee described in § 1.1294-1T(e) (2) or (4), but the amount of the deemed distribution resulting therefrom was less than the amount of the actual loan by the QEF (or the amount of the loan secured by the pledge or guarantee), earnings derived by the QEF in a subsequent taxable year will be treated as distributed in such subsequent year to the shareholder for purposes of paragraph (b)(3)(i)(A) by virtue of such loan, but only to the extent of the difference between the outstanding principal balance on the loan in such subsequent year and the prior years’ deemed distributions resulting from the loan. For this purpose, the outstanding principal balance on a loan in a taxable year shall be treated as equal to the greatest amount of the outstanding balance at any time during such year.

(ii) Deemed distribution. In 1988, FC has ordinary earnings of $100,000x but no net capital gain. S‘s pro rata share of FC‘s 1988 ordinary earnings was $50,000x. S‘s loan remained outstanding throughout 1988; the highest loan balance during 1988 was $74,000x. Of S‘s share of the ordinary earnings of FC of $50,000x, $24,000x is deemed distributed to S. This is the amount by which the highest loan balance for the year ($74,000x) exceeds the portion of the undistributed earnings of FC deemed distributed to S in 1987 by reason of the pledge ($50,000x). S may make the election under section 1294 to extend the time for payment of its tax liability on $26,000x, which is the amount by which S‘s includible amount for 1988 exceeds the amount deemed distributed to S during 1988.

(c) Time for making the election –

(1) In general. An election under this § 1.1294-1T may be made for any taxable year in which a shareholder reports income pursuant to section 1293. Except as provided in paragraph (c)(2), the election shall be made by the due date, as extended, of the tax return for the shareholder’s taxable year for which the election is made.

(2) Exception. An election under this section may be made within 60 days of receipt of notification from the QEF of the shareholder’s pro rata share of the ordinary earnings and net capital gain if notification is received after the time for filing the election provided in paragraph (c)(1) (and requires the filing of an amended return to report income pursuant to section 1293). If the notification reports an increase in the shareholder’s pro rata share of the earnings previously reported to the shareholder by the QEF, the shareholder may make the election under this paragraph (c)(2) only with respect to the amount of such increase.

(d) Manner of making the election –

(1) In general. A shareholder shall make the election by (i) attaching to its return for the year of the election Form 8621 or a statement containing the information and representations required by this section and (ii) filing a copy of Form 8621 or the statement with the Internal Revenue Service Center, P.O. Box 21086, Philadelphia, Pennsylvania 19114.

(2) Information to be included in the election statement. If a statement is used in lieu of Form 8621, the statement should be identified, in a heading, as an election under section 1294 of the Code. The statement must include the following information and representations:

(i) The name, address, and taxpayer identification number of the electing shareholder and the taxable year of the shareholder for which the election is being made;

(ii) The name, address and taxpayer identification number of the QEF if provided to the shareholder;

(iii) A statement that the shareholder is making the election under section 1294 of the Code;

(iv) A schedule containing the following information:

(A) The ordinary earnings and net capital gain for the current year included in the shareholder’s income under section 1293;

(B) The amount of cash and other property distributed by the QEF during its taxable year with respect to stock held directly or indirectly by the shareholder during that year, identifying the amount of such distributions that is paid out of current earnings and profits and the amount paid out of each prior year‘s earnings and profits; and

(C) The undistributed PFIC earnings tax liability (as defined in paragraph (f) of this section) for the taxable year, payment of which is being deferred by reason of the election under section 1294;

(v) The number of shares of stock held in the QEF during the QEF’s taxable year which gave rise to the section 1293 inclusion and the number of such shares transferred, deemed transferred or otherwise disposed of by the electing shareholder before the end of the QEF’s taxable year, and the data of transfer; and

(vi) The representations of the electing shareholder that –

(A) No part of the QEF’s earnings for the taxable year is includible in the electing shareholder’s gross income under either section 551 or 951 of the Code;

(B) The election is made only with respect to the shareholder’s pro rata share of the undistributed earnings of the QEF; and

(C) The electing shareholder, upon termination of the election to extend the date for payment, shall pay the undistributed PFIC earnings tax liability attributable to those earnings to which the termination applies as well as interest on such tax liability pursuant to section 6601. Payment of this tax and interest must be made by the due date (determined without extensions) of the tax return for the taxable year in which the termination occurs.

(e) Termination of the extension. The election to extend the date for payment of tax will be terminated in whole or in part upon the occurrence of any of the following events:

(1) The QEF’s distribution of earnings to which the section 1294 extension to pay tax is attributable; the extension will terminate only with respect to the tax attributable to the earnings that were distributed.

(2) The electing shareholder’s transfer of stock in the QEF (or use thereof as security for a loan) with respect to which an election under this § 1.1294-1T was made. The election will be terminated with respect to the undistributed earnings attributable to the shares of the stock transferred. In the case of a pledge of the stock, the election will be terminated with respect to undistributed earnings equal to the amount of the loan for which the stock is pledged.

(3) Revocation of the QEF’s election as a QEF or cessation of the QEF’s status as a PFIC. A revocation of the QEF election or cessation of PFIC status will result in the complete termination of the extension.

(4) A loan of property by the QEF directly or indirectly to the electing shareholder or related person, or a pledge or guarantee by the QEF with respect to a loan made by another party to the electing shareholder or related person. The election will be terminated with respect to undistributed earnings in an amount equal to the amount of the loan, pledge, or guarantee.

(5) A determination by the District Director pursuant to section 1294(c)(3) that collection of the tax is in jeopardy. The amount of undistributed earnings with respect to which the extension is terminated under this paragraph (d)(5) will be left to the discretion of the District Director.

(f) Undistributed PFIC earnings tax liability. The electing shareholder’s tax liability attributable to the ordinary earnings and net capital gain included in gross income under section 1293 shall be the excess of the tax imposed under chapter 1 of the Code for the taxable year over the tax that would be imposed for the taxable year without regard to the inclusion in income under section 1293 of the undistributed earnings as defined in paragraph (b)(3) of this section.

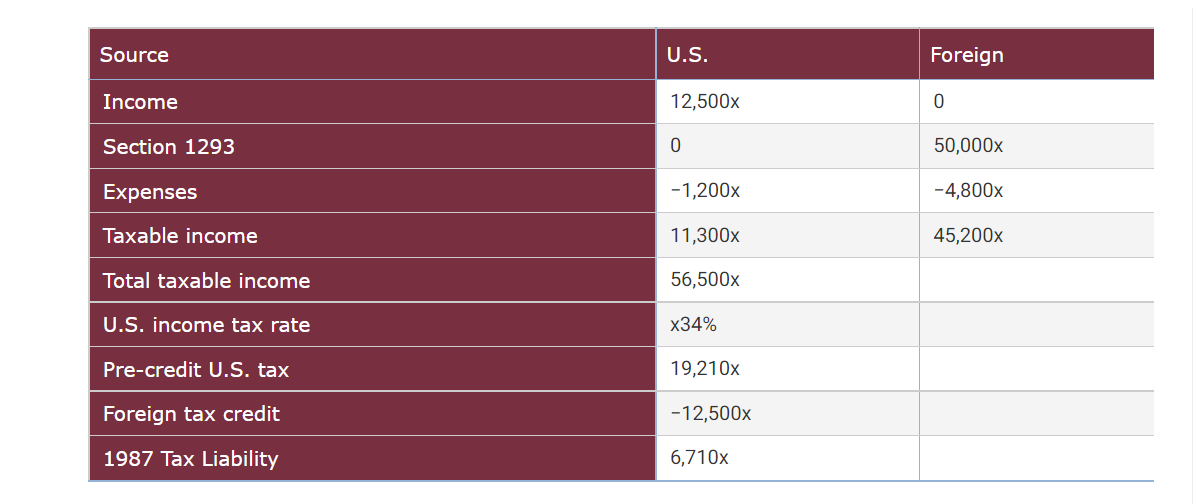

1987 Tax Liability (With Section 1293 Inclusion)

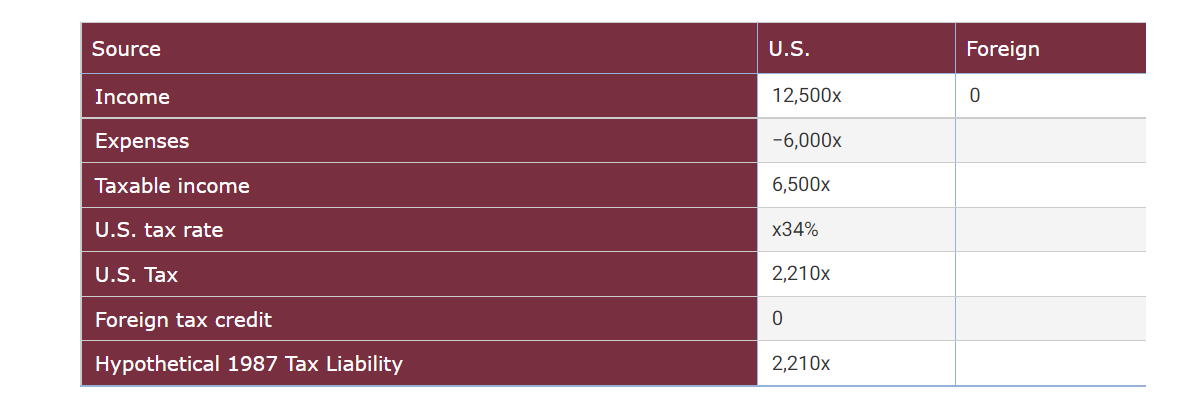

1987 Tax Liability (Without Section 1293 Inclusion)

(g) Authority to require a bond. Pursuant to the authority granted in section 6165 and in the manner provided therein, and subject to notification, the District Director may require the electing shareholder to furnish a bond to secure payment of the tax, the time for payment of which is extended under this section. If the electing shareholder does not furnish the bond within 60 days after receiving a request from the District Director, the election will be revoked.

(h) Annual reporting requirement. The electing shareholder must attach Form 8621 or a statement to its income tax return for each year during which an election under this section is outstanding. The statement must contain the following information:

(1) The total amount of undistributed earnings as of the end of the taxable year to which the outstanding elections apply;

(2) The total amount of the undistributed PFIC earnings tax liability and accrued interest charge as of the end of the year;

(3) The total amount of distributions received during the taxable year; and

(4) A description of the occurrence of any other termination event described in paragraph (e) of this section that occurred during the taxable year.