Skip to content

Skip to content

The Charitable Remainder Trust (CRT) and Crypto

Ok. Let’s get the obvious part out of the way. I’m not trying to sell you anything. The CRT option has become an attractive option for my crypto clients so I felt compelled to write my own commentary on it. Most of the content available online are from those trying to sell the solution so the content tends to be, naturally, one sided.

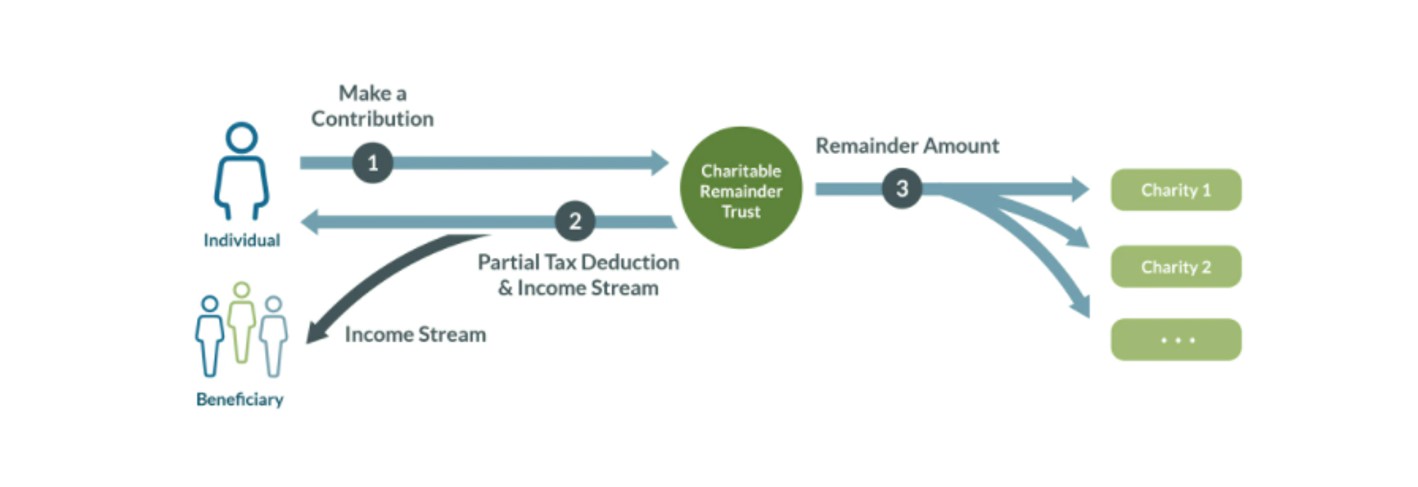

A charitable remainder trust (CRT) is an irrevocable trust (meaning that once you transfer over your crypto assets, it is gone completely) that generates a potential income stream for you, as the donor to the CRT, or other beneficiaries, with the remainder of the donated assets going to your designated charity or charities upon your demise.

The CRT is not designed primarily as a tax planning tool but as charitable giving strategy. This charitable giving strategy generates income and can enable you to pursue your philanthropic goals while also helping provide for living expenses. Charitable trusts can offer flexibility and some control over your intended charitable beneficiaries as well as lifetime income, thereby helping with retirement, estate planning and tax management.

In IRS Notice 2014-21, the IRS took the position that cryptocurrency is property and should be taxed as such. This position has not changed. Accordingly, a taxable event has occurred whenever one disposes of cryptocurrency, whether for a good, service, another coin, or fiat currency (e.g., U.S. dollar). That is, the taxpayer disposing of cryptocurrency will generally have either a capital gain or loss on the transaction.

Much like other types of property, capital gains and losses apply to cryptocurrency; however, the biggest benefit to the tax treatment of cryptocurrency is that the wash-sale rules arguably do not apply. While the IRS has not officially taken a position on this treatment, many commentators have interpreted the IRS’ silence as such. As a result, they effectively allow a taxpayer to harvest losses and eliminate a portion of the taxpayer’s gains.

Cryptocurrency is a highly volatile asset. Charitable remainder trusts, such as a charitable remainder unitrust (CRUT), may be used by taxpayers holding highly appreciated cryptocurrency to address cryptocurrency volatility, spread the income tax hit from the sale of cryptocurrency over a number of years, and possibly receive a charitable income tax deduction. A CRUT is a trust designed to pay the grantor a payment based on a fixed percentage of the trust value yearly for a term of years or the lifetime of the CRUT beneficiary. CRUTs allow a taxpayer to receive an immediate charitable deduction upon their transfer of cryptocurrency into the CRUT. The CRUT can then sell the cryptocurrency and reinvest in a more stable asset, such as stocks, bonds, mutual funds, etc. A CRUT does not pay income tax, but the beneficiary will only on the distributed income. Upon termination of the CRUT, the balance of the CRUT assets are paid out to charity. In effect, a CRUT allows a taxpayer to stretch out a capital gain tax hit over several years.

The United States government has recently taken a strong interest in tax compliance as it relates to cryptocurrency. In fact, the infrastructure bill recently passed in the Senate contemplates financing a large portion of the bill’s cost with increased compliance on crypto tax issues.

Cryptocurrency is significantly underreported to the IRS. The laws are new, and many who operate in this space do not realize that the transactions are taxable. Even if every individual who had a taxable cryptocurrency transaction wanted to report such transaction, the reporting documents issued by the popular cryptocurrency exchanges are not user-friendly. To increase compliance with proper reporting of cryptocurrency, a higher audit rate will likely follow.

How a charitable remainder trust works

A charitable remainder trust is a “split interest” giving vehicle that allows you to make contributions to the trust and be eligible for a partial tax deduction, based on the CRT’s assets that will pass to charitable beneficiaries. You can name yourself or someone else to receive a potential income stream for a term of years, no more than 20, or for the life of one or more non-charitable beneficiaries, and then name one or more charities to receive the remainder of the donated assets.

There are two main types of charitable remainder trusts:

• Charitable remainder annuity trusts (CRATs) distribute a fixed annuity amount each year, and additional contributions are not allowed.

• Charitable remainder unitrusts (CRUTs) distribute a fixed percentage based on the balance of the trust assets (revalued annually), and additional contributions can be made.

Contributions to CRATs and CRUTs are an irrevocable transfer of cash or property and both are required to distribute a portion of income or principal, to either the donor or another beneficiary. At the end of the specified lifetime or term for the income interest, the remaining trust assets are distributed to one or more charitable remainder beneficiaries.

1. Make a partially tax-deductible donation

Donate cash, stocks or non-publicly traded assets such as real estate, private business interests and private company stock and become eligible to take a partial tax deduction. The partial income tax deduction is based on the type of trust, the term of the trust, the projected income payments, and IRS interest rates that assume a certain rate of growth of trust assets.

2. You or your chosen beneficiaries receive an income stream

Based on how you set up the trust, you or your stated beneficiaries can receive income annually, semi-annually, quarterly or monthly. Per the IRS, the annual annuity must be at least 5% but no more than 50% of the trust’s assets.

3. After the specified timespan or the death of the last income beneficiary, the remaining CRT assets are distributed to the designated charitable beneficiaries.

When the CRT terminates, the remaining CRT assets are distributed to the charitable beneficiary, which can be public charities or private foundations. Depending on how the CRT is established, the trustee may have the power to change the CRT’s charitable beneficiary during the lifetime of the trust.

What assets may be donated to a CRT?

Let’s also remember that any low-cost basis stock can take advantage of charitable remainder trust, so if you’ve owned a technology company for a decade and don’t know how to exit the position without paying an exorbitant amount in taxes, this might be the solution.

It’s worth noting that this strategy is generally accompanied with the purchase of life insurance to replace the gift in the event that the donor dies prematurely. The income from the charitable remainder trust would be available to pay the insurance premiums, with minimal impact to the donor’s cash-flow.

These are complicated strategies, and the trust can vary in the frequency of future donations as well as the ability to defer payments from the trust that allows the principal to grow. In the latter instance, the remaining amount left to the charity increases, as would the immediate tax deduction.

Investors considering this course of action would be advised to speak with a qualified estate-planning attorney and a qualified tax advisor to help them navigate the laborious details and IRS requirements. In the end, it may be an excellent opportunity for the early adopters of crypto currencies to keep more of their profits and determine how their social capital is spent.

You can use the following types of assets to fund a charitable remainder trust.

• Cash

• Publicly traded securities

• Some types of closely held stock (Note that CRTs cannot hold S-Corp stock)

• Real estate

• Certain other complex assets

• Rental property

• Raw land

• Cryptocurrency

• Stock

• Small Business

• Venture Capital Business Interest

• Precious Metals

• Artwork or any collectible

• Oil, Gas, Mineral or Water interest

• The list goes on and on…

What are the main benefits of a Charitable Remainder Trust?

A number of advantages may flow from a well-drafted CRT. This is clearly a tool that must be designed by a qualified attorney. There is almost an infinite number of variations depending on the type of asset, the gain, the age of the taxpayer, whether they are married or single, their typical tax bracket, and how much of a tax deduction on cash flow they want at the end of the process.

There are (6) six major benefits with the CRT as follows:

1. Pay no tax whatsoever on the sale / transfer of the asset. Thereby creating a larger ‘pool’ of money the trustee can invest within the CRT. A donor will usually create a CRT and designate themselves as an income beneficiary. However, the donor can name other non-spouse non-charitable beneficiaries to receive the income from the CRT. If they do, there is a taxable gift to the non-spouse beneficiary when the CRT is funded. The value of the gift to the non-spouse beneficiary is reduced to the present value of the future income payments. Gifting cryptocurrency is not free from risk. Anytime you gift a highly volatile asset, like cryptocurrency, there is a chance that the asset may decline in value. This would result in a waste of gift tax exemption used for the gift. While gifting cryptocurrency may be a viable option, practical issues arise. Many trustees are unwilling to serve as fiduciaries of trusts holding cryptocurrency due to volatility and custody concerns for gifts in trust. Finding the right trustee could take time. Likewise, charitable organizations may be reluctant to hold cryptocurrency for similar reasons. A qualified appraisal is generally required when gifting cryptocurrency to charity. Given the standard to be a “qualified appraiser” and the short time cryptocurrency has been in existence (Bitcoin, the oldest cryptocurrency, was established in 2009), it may be difficult to find a “qualified appraiser.”

2. Receive a current income tax deduction for the charitable contribution of the value of the asset to the trust. The deduction is permitted when the trust is created even though the charity has yet to sell the asset donated to the CRT. The donor takes a tax deduction over the next five years. The deduction will be based on the property value, typically determined by the sale to the third party or an appraisal. If the CRT is funded with cash, the donor can use a charitable deduction of up to 60% of Adjusted Gross Income (AGI); if appreciated assets are used to fund the trust, up to 30% of their AGI may be deducted in the current tax year. In addition, if the donor cannot use the whole deduction in the year of the gift, he/she can carry over the deduction for up to five additional years. Charitable remainder trusts are particularly suited for appreciated property because any capital gains tax will be deferred until the time that it is distributed out to the income beneficiary. Therefore, a donor can contribute highly appreciated concentrated positions to the CRT and diversify his/her position in a tax-effective manner as the tax burden will be spread out over time.

3. The CRT creates an asset-protected plan for the proceeds from the sale that are generally untouchable by creditors of the donor (assuming the CRT is entered into before any ’cause of action’ or judgments and avoiding a fraudulent transfer claim).

4. The trustee of the CRT will pay out a stream of income to the donor/taxpayer for life, based on the value of the CRT. This annuity or percentage will vary dramatically based on the age of the taxpayer, the value of the CRT, and the amount of the tax deduction. The charity gets the remaining money in the trust in 20 years or upon the donor’s death, whichever is longer. This is typically the incentive for the charity to pay for preparing and implementing the entire charitable trust strategy. Although the beneficiary can’t borrow against the value of his CRUT, since part of that value belongs to his chosen charity, he can open a line of credit using the future income from his CRUT as collateral. What this means in practice is that he can access as much as the full value of his expected payouts from the trust at a reasonable interest rate, should he need more than the liquidity he would normally be able to take out of his trust.

5. The trust will be eligible for the estate tax charitable deduction if it passes to one or more qualified charities at your death, or even excluded from the value of your estate entirely.

6. Finally, through the leveraging effect of life insurance, it is possible to pass on assets of greater value to your family ‘tax-free’, rather than those contributed to the CRT. This is accomplished by purchasing life insurance with some of the cash flow from the CRT for a period of time (typically accomplished through a separate Irrevocable Life Insurance Trust). In this way, your heirs are not deprived of property they had expected to inherit.