Skip to content

Skip to content Most states in the United States define “residency” based on a person’s “domicile.” Domicile, in general, is the place which an individual intends to be his or her permanent home and to which such individual intends to return whenever absent.

Here’s something we wrote on domicile previously, but in the context of pre-immigration tax planning and at the Federal level – https://www.htj.tax/us-pre-immigration-planning/

An individual can only have one domicile at a time. Once a person acquires a domicile, he/she retains that domicile until another is acquired.

A change of domicile requires:

1) abandonment of a prior domicile,

2) physically moving to and residing in the new locality, and

3) intent to remain in the new locality permanently or indefinitely.

If a person moves to a new location but intends to stay there only a limited time (no matter how long), their domicile does not change.

Domicile is not dependent on citizenship. However, 1. a United States citizen shall not ordinarily be deemed to have changed domicile by going to a foreign country unless it is clearly shown that such individual intends to remain there permanently. 2. Special rules apply to United States permanent residents especially when working abroad.

Unlike moving from state to state within the US, tougher rules apply for someone moving from a US State to a foreign country and simply changing residence is not always sufficient to break State domicile. We often encounter situations where US citizens move to a foreign country on a work visa. Many US States will argue that as a visa is conditional (for example on employment), that the individual does not have the right to permanently remain in the foreign country and as such cannot have established a new domicile whilst their immigration status is conditional.

How to Choose a Domicile State

For full-time travelers, the difference between residency and domicile matters a lot. Residency is legally defined as “your place of abode.” It’s where you live right now. Your domicile is your legal, permanent residence; it’s the place where you intend to return after your absence. Your domicile is what ties you to a specific state. You can have many residences but only one domicile.

Another way to look at the difference between residency and domicile is through a profession. For example, a professional in Louisiana might travel to Missouri to work for six or nine months, or even longer. They might be considered “residents” of Missouri because of their length of stay. But they keep their old address, old driver’s license, and vehicle tags in Louisiana. Louisiana is where their home is, and more importantly, where they intend to return when their work is finished. In other words, Louisiana is their domicile.

Every U.S. citizen has to have a domicile to pay taxes, vote, open a bank account, and handle all the other logistical details that come with being a legal citizen. Even when you don’t have a “home” in the traditional sense of the word, you still have to choose and set up a domicile.

Factors to Determine Intent

As indicated above, the location of a person’s domicile is dependent on a person’s intentions. Intent is a state of mind. A state of mind is difficult to prove. As a result, taxing authorities (and courts) look to a person’s actions to determine their intent. Some of the factors that courts and taxing authorities look to include:

- Amount of time you spend in one location versus another

- Location of your spouse and children;

- Location of your principal residence;

- Where your driver’s license was issued;

- Where you maintain your professional licenses;

- Where you are registered to vote;

- Location of the banks where you maintain accounts;

- Location of your doctors, dentists, accountants, and

attorneys; - Location of the church, temple or mosque, professional

associations, or social and country clubs of which you are a member; - Location of your real property and investments;

- Permanence of your work assignments in a location; and

- Location of your social ties.

Overseas Assignments

A classic situation where an individual has moved outside of the US, but has not changed their domicile. Even if the move is for an extended period of time, there has been no change in domicile unless the individual intends to remain in the new locality permanently or indefinitely.

How the States Catch You

States do not typically track in detail the activities of each taxpayer. If a taxpayer leaves a state, has no further income sourced in that state, and ceases to file tax returns in that state, then the tax authorities of that state do not typically inquire where the taxpayer moved to or whether they changed their domicile. The domicile/residency issue usually arises in two different circumstances. In the first circumstance, the taxpayer continues to have income sourced from that state, but the taxpayer begins filing as a nonresident.

The second circumstance is when a person, who has been filing as a resident of the state, ceases all filings in that state, and then at some point in the future again files as a resident of the state. This second circumstance often applies to individuals that move overseas for a period of time and then return to the same state. When the state tax authorities receive a tax return, they check to see if that individual filed a tax return in prior years. If prior year resident tax returns have been filed, but there is a gap in filings (of perhaps several years), the state tax authorities begin to wonder why no tax returns were filed during the intervening years.

If the state tax authorities identify a person with a gap in tax filings, and they believe that that person retained their domicile in that state, then they will require the filing of state income tax returns for the intervening years. Statutes of limitations for tax returns generally begin to run on the date a tax return is filed. If no tax returns have been filed for the intervening years, then the statute of limitations for those years remains open indefinitely.

Substantial Taxes May be Due

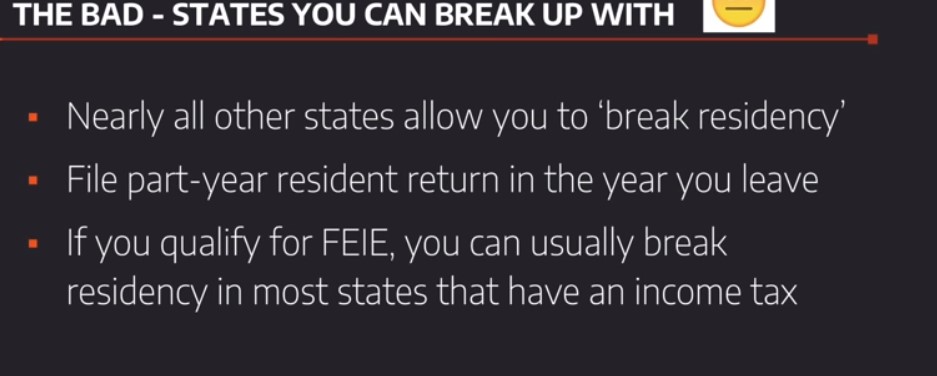

States do not typically allow foreign taxes paid as credits against state income taxes. Further, states may or may not conform to the federal rules which allow certain foreign earned income to be excluded from taxable income. As a result, persons temporarily residing overseas will often owe significant state income taxes, even though they may not be present in the state at all during the year.

Residency Exceptions

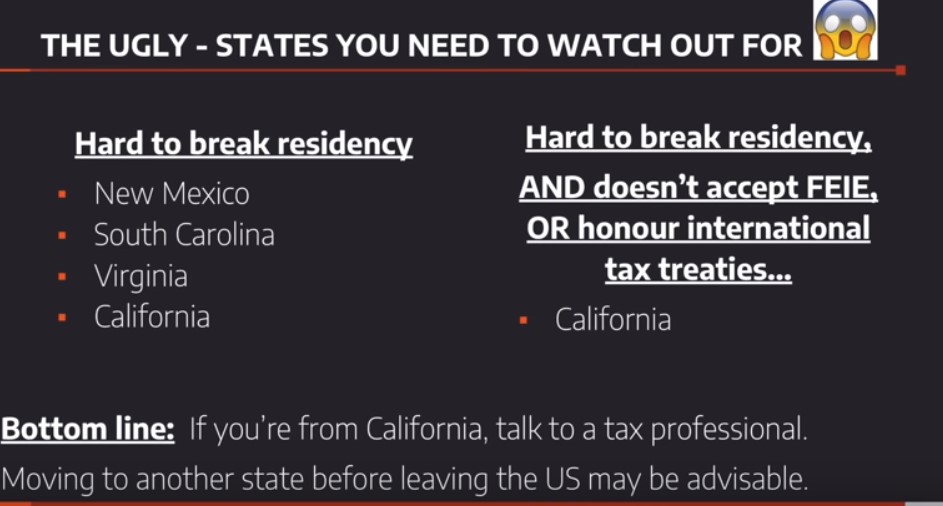

Some states provide exceptions to individuals being treated as residents, even if the individuals retain their domicile in that state. For instance, California allows (with certain exceptions) individuals that are domiciled in California to be treated as nonresidents of California if they are located outside California under an employment-related contract that lasts for at least 546 days. Connecticut, on the other hand, has two alternative tests that allow Connecticut domiciled individuals to be treated as non-residents.

To meet the requirements of the first test, an individual must:

- not maintain a permanent place of abode in Connecticut for the entire year,

- maintain a permanent place of abode outside of Connecticut for the entire year, and

- not spend more than 30 days in Connecticut during the year.

To meet the requirements of the second test, an individual must:

- be in a foreign country for at least 450 days during any period of 548 consecutive days, and

- during this period, not spend more than 90 days in Connecticut (or have a spouse or minor children that spend more than 90 days in Connecticut).

As can be seen from the California and Connecticut rules, the state exceptions to residency for domiciled individuals are not consistent. Thus, it is important to review the rules for the state in which the person is domiciled.

Important Considerations

Choosing your domicile state is one of the most important decisions as a digital nomad. The state you choose will affect how much (if any) income tax you pay. It will affect how your will is processed if you pass away, how much your spouse is entitled to if you get divorced, and even how easy it is to get health insurance.

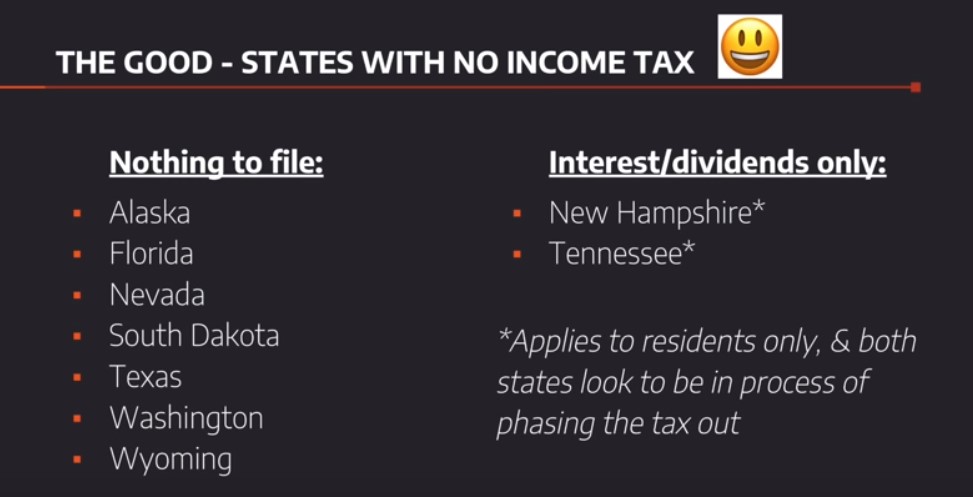

You can choose any state to be your domicile state, but there are three states that are “domicile friendly,” making them popular choices for location independent workers: Texas, Florida, and South Dakota. These states make it easy to establish and maintain domicile. There are many mail-forwarding services set up in these states to process and forward your mail. They also have no state income tax.

Other states are more complicated. Many states require you to spend at least 183 days within the state in fixed quarters, such as a house or apartment, to qualify for domicile. When you transition to your domicile state, it’s important that you do your best to cut all ties with the state you currently live in. When states try to claim you as a resident (for tax and census purposes), they look for property to establish domicile. If that’s nonexistent, they look for other “contacts,” like a driver’s license, vehicle registration, voter registration, or employment records.

If you establish domicile in one state but still have “contacts” in another state, you might find yourself caught between two states that both want you to pay income taxes or other fees. Choose one state, and cut ties with the other completely if you can.

What do you need to consider when choosing your domicile state? Let’s take a closer look at some of the big issues.

Voting

Most states allow you to register to vote when you go in for your driver’s license. But how easy is it to vote absentee in your domicile state of choice? Absentee ballots can always be used in national elections; however, every state is different when it comes to voting absentee for state and local elections. This is an important consideration when you start looking at the benefits and drawbacks of domicile for each state.

Banking

Banking can be challenging as a full-time traveler. Thanks to the Patriot Act, financial institutions are required to have a residential address on file for every consumer. Additionally, the law specifically excludes mail-forwarding addresses. Even if you have existing accounts at your bank, you can still get in trouble if you don’t change your address, and even temporarily lose access to your accounts if you get caught banking under an old address.

The Patriot Act does allow you to use the residential address of a family or friend, and most banks will not ask for proof that you actually live there. However, some will; if your bank does require proof of residency, you’ll have to provide a utility bill or other document showing you pay bills there. If you’re considering going on the road full-time, find out what each of your financial institutions requires in terms of proof of residency and, equally important, how they reinforce this requirement.

You also need to look at how easy it will be to use your current financial institutions on the road. Do they have an easy to use online banking system? If it’s going to be a hassle to access your money easily on the road, you might need to find a new bank.

sources –

https://www.htj.tax/us-pre-immigration-planning

https://intltax.typepad.com/intltax_blog/2008/06/us-state-tax-residency-domicile.html

https://www.moneycrashers.com/rv-living-choose-domicile-state-get-mail/