Skip to content

Skip to content PREFACE

The report on combating fraud and tax evasion is an instrument of the greatest relevance in the monitoring the policies and actions of the tax and customs administration, within a framework in which Fraud, evasion and tax avoidance behaviors constitute a threat to social justice in our modern societies.

After around two years conditioned by the COVID-19 pandemic, the year 2022 was marked by invasion of Ukraine, giving rise to a complex socio-economic context: growing inflation in fundamental sectors, such as energy or agri-food; accelerated increase in interest rates; difficulties in supply chains and a geopolitical framework of greater uncertainty worldwide.

Whether in the previous context of the Covid-19 pandemic or in this context of inflationary pressure, they deserve Special emphasis is placed on support measures for families and companies implemented through the Authority Tax and Customs (AT) or with the latter’s contribution, both at the fiscal level and at the level of support of another nature.

Seeking to induce voluntary compliance on the part of taxpayers, AT has been dedicating a special focus on supporting taxpayers, issuing alerts to them, as well as introducing a new phase in the inspection procedure: the regularization meeting. In this context, the inspection action prioritizes the fight against highly complex fraud and the informal economy, associated with the identification and detection of fraudulent conduct and abusive tax planning schemes.

The year 2022, in terms of tax inspection, is marked by an increase in the level of regularizations voluntary activities and the growing focus on more complex actions aimed at planning tax (including the promotion of instruments such as the exchange of international information and the derogation banking secrecy).

In terms of combating the informal economy, in 2022, there was a 14.59% growth in the number of invoices with the taxpayer number (NIF), as well as an increase of 15.62% in the total annual value of invoices with NIF communicated to AT, amounting to a total of 71,619,813,640 EUR. That year, The two-dimensional barcode (QR code) is now mandatory on all invoices issued through a certified invoicing program. As a result of this change, there was a significant growth in the communication of invoices by acquirers using code reading QR, through the e-Fatura App, instead of registering on the Finance Portal.

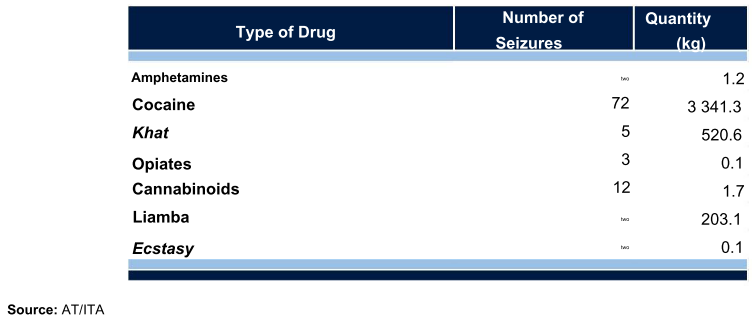

Considering that AT also has an important mission of controlling the external border, not only in the tax aspect, but also in the protection and security of society when importing and export of goods, it is important to highlight that AT carried out, in 2022, the detection and seizure of more than four tons of illicit drugs, in more than 100 seizures.

Finally, I would like to thank the commitment of AT workers and managers, both in the services central offices, whether in regional and local services, as well as other entities that collaborate in the combating fraud and tax and customs evasion. Taxes are one of the pillars of the Social State of Law, ensuring the financing of services provided to society by the State and other entities public and having an important redistributive function at a social level. Therefore, combating fraud and Tax and customs evasion is essential for a more fair, equitable and cohesive society.

Lisbon, June 30, 2023

The Secretary of State for Fiscal Affairs,

Nuno Santos Felix

INTRODUCTION

AT is a direct administration service of the State, endowed with administrative autonomy, and its purpose is to mission is the administration of taxes, customs duties and other duties assigned to it, as well as exercising control over the external border of the European Union and the customs territory nationally, for tax, economic and societal protection purposes, in accordance with defined policies by the Government and European Union Law.

To this end, AT has a set of attributions (Decree Law no. 118/2011, of December 15) among which stand out:

- Ensure the settlement and collection of taxes and other taxes or revenues of the State that it is up to administration;

- Inform taxpayers and economic operators about their respective tax obligations and customs and support them in voluntary compliance with them;

- Promote the correct application of legislation and administrative decisions and propose measures of a normative, technical and organizational nature that proves to be appropriate;

- Carry out and promote technical and scientific research in the tax and customs field, taking into account with a view to improving legal and administrative measures and permanent qualification human resources;

- Carry out tax and customs inspection actions, preventing, investigating and combating tax and customs fraud and evasion and illicit trafficking;

- Collaborate with the competent authorities in defining and implementing security policies preventing and combating money laundering and terrorist financing;

- Carry out tax and customs justice actions, ensuring the representation of the Treasury

- Ensure technical negotiation and execute international agreements and conventions on matters Public with judicial bodies; tax and customs, cooperate with European and international organizations and other tax and customs administrations;

- Ensure the licensing of foreign trade of products typified in special legislation and manage restrictive regimes for the respective foreign trade.

Pursuant to the provisions of article 64-B of the LGT, it is up to the Government to present to the Assembly of Republic, by the end of June each year, a detailed report on the evolution of combat fraud and tax evasion in all areas of taxation, explaining the results achieved, namely regarding the value of additional settlements carried out, as well as the value of collections recovered in the various taxes.

This document highlights the contributions of AT to the preparation of the aforementioned report, describing the activity carried out by AT in combating tax and customs fraud and evasion during the year 2022.

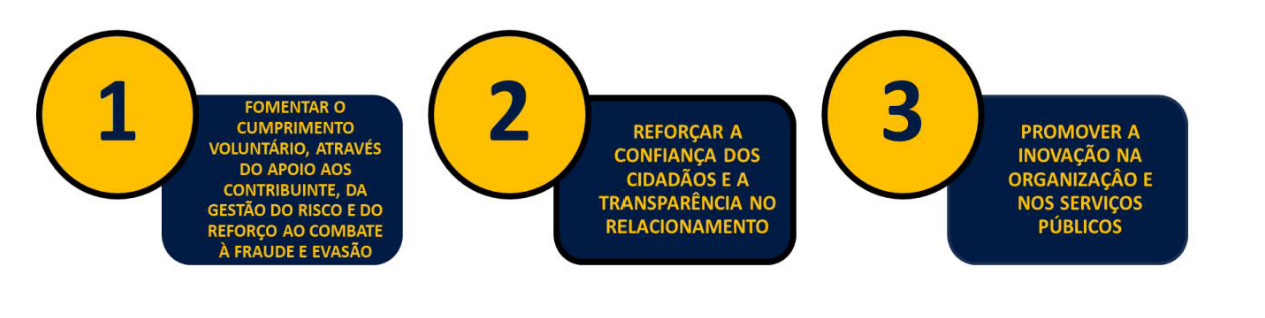

2.1. Strategic objectives

During 2022, AT continued to develop its activity taking into account the strategy defined in the 2020-2022 Strategic Plan, which is outlined with the Plan’s Major Options defined by the XXII Constitutional Government for the period 2020-2023 at the level of fiscal policy, which fits, in turn, into the global strategy of economic and social development and consolidation of public accounts.

Figure 1: AT strategic objectives

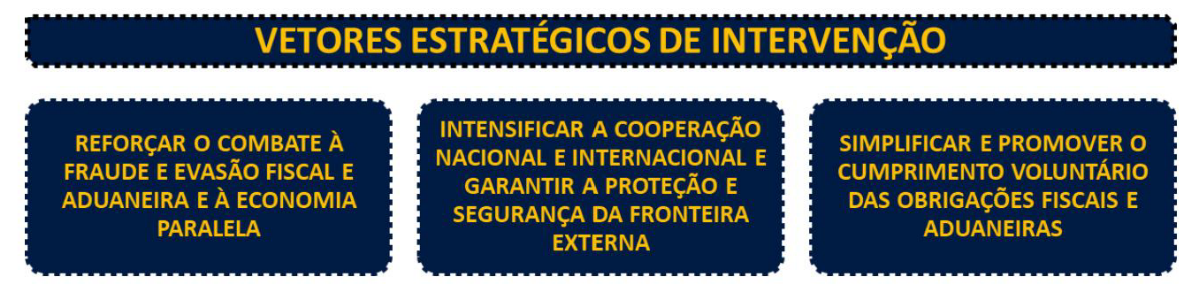

During the year 2022, taking into account the Addendum made following the pandemic COVID-19, for 2021-2022 to the Strategic Plan to Combat Tax and Customs Fraud and Evasion (PECFEFA) 2018-2020, AT continued with the operationalization cycle of the measures provided for in PECFEFA, maintaining the same orientation in carrying out its activity.

This Addendum, oriented according to the three strategic vectors of priority intervention that are below identify, was based on a set of measures in five distinct areas:

- Legislative;

- Criminal;

- Operational;

- Institutional relationships with other national and international public entities; It is

- The relationship with the taxpayer..

Figure 2: PECFEFA strategic vectors

2.2. Challenges of the Post-Pandemic period

After around two years conditioned by the COVID-19 pandemic, with significant effects on economies worldwide, the year 2022 began with the expectation of recovery and resumption of pre-pandemic indicators. However, in February 2022, war once again became a reality in Europe, giving rise to an impactful macroeconomic scenario: inflation in fundamental sectors, such as energy and agri-food, accelerated increase in interest rates by central banks, difficulties in supply chains and raw material production and increased uncertainty geopolitics. These factors contributed to the extension of the economic slowdown scenario global, thus creating new challenges and very significant limitations to the performance of not only the sector business, as well as families. AT, as well as tax administrations across the world in general, continued to play in this context, a very important role in supporting citizens, through their participation in implementation of measures to support the economy, but also in simplifying compliance with declarative and payment obligations.

In this context, in 2022, AT continued to invest in different communication channels, seeking to provide a quality service to taxpayers, in order to support and simplify the compliance with its tax obligations. AT reinforced its presence on social media, having increased its number of followers on the multiple digital platforms where it is present.

The end of restrictions imposed by the COVID-19 pandemic contributed to a considerable increase number of services (with and without appointment) compared to the previous year, as well as the service capacity, prioritizing service by appointment, so that a better support service can be provided to the taxpayer.

2.3. The Compliance Model

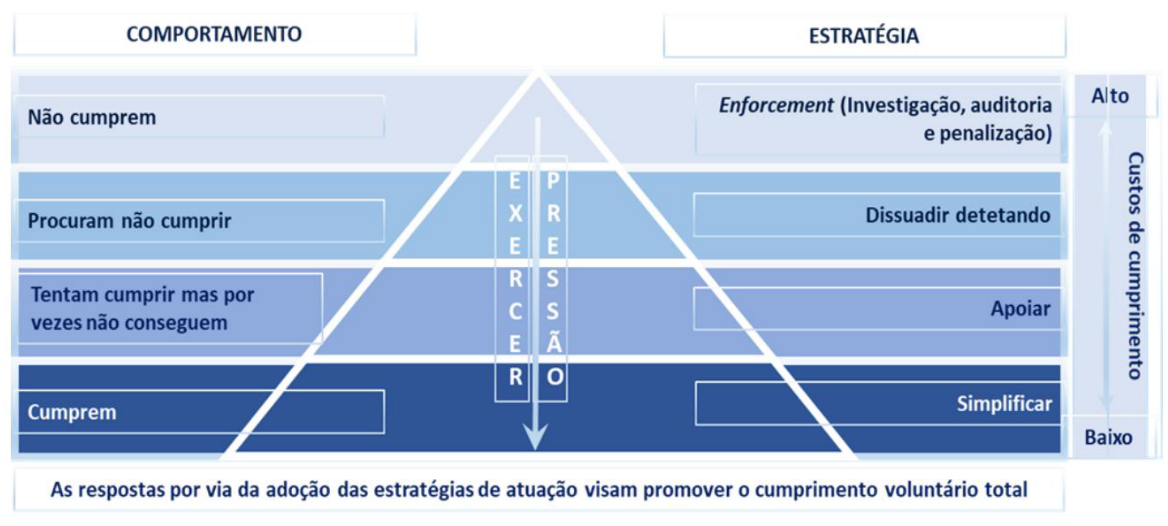

The methodology used by AT is based on the study and understanding of taxpayer behavior, what motivates citizens to comply, or not, with their tax obligations. This model allows taking into account the level of compliance with tax regulations, seeking in a structured way to understand AT adapt its responses and interventions, with the aim of influencing the behavior of taxpayers in a positive way.

The approach recommended at OECD level has as its starting point the recognition that most taxpayers seek to fulfill their tax obligations correctly and on time.

However, there are a smaller number of taxpayers who want to comply, but are not always able to. There is an even smaller number who deliberately do not want to fulfill their obligations. Thus, the taxpayer behavior is, to a large extent, influenced by a series of factors, including by AT’s own actions.

In this sense, AT seeks to adapt its response to the various categories of behavior of voluntary, without prejudice to reserving the use of its powers in inspection and criminal investigation taxpayers and seeks to influence this behavior, encouraging and assisting compliance whenever necessary.

Figure 3 – Fulfillment Model Pyramid

Source: Spectrum of taxpayer attitudes to compliance in MANAGING AND IMPROVING TAX COMPLIANCE SEPT 2004 – OECD FTA Compliance Sub-group

This pyramid expresses the assumptions of the compliance model, namely the stratification of taxpayers’ attitudes and the corresponding strategy to adopt, in order to mitigate this attitude in relation to the desired behavior, and the response must be graduated and depending on the disposition of the taxpayer whether or not to comply with their obligations.

The majority of taxpayers fall into the lower sections of the pyramid, namely they comply; or try to comply, but sometimes fail, sharing a common denominator – they are willing to comply. A progressively smaller number of taxpayers fall into both upper sections where taxpayers’ behavior is characterized by being less compliant, demanding stronger positions from AT. In this way, the function of AT involves pressuring and discouraging, in order to encourage taxpayers to adopt the behavior correct, voluntarily fulfilling their obligations.

As in previous years, and as is already repeated practice, in 2022 AT sought simplify and support citizens who wish to voluntarily comply with their obligations taxes, however, without ever neglecting its more robust and sanctioning action on defaulting taxpayers, making all necessary efforts to detect possible situations of tax and customs fraud and evasion, and to discourage the practice of these types of acts, acting in a consistent manner on the offenders, through legal means, and aiming to recover the losses generated.

Operationally, it continued to prioritize communication with taxpayers/economic operators, using new information and communication technologies as a means of provision of information, ensuring that taxpayers understand their rights and responsibilities, providing them with accurate and timely information, clarifying the law or expressing their opinion regarding it, through the provision and updating of information on the Finance Portal, YouTube, Twitter, Facebook, Instagram, information leaflets, tax calendar, FAQ (Frequently Asked Questions), administrative guidelines, information binding documents, as well as a vast digital collection of models and forms, respective data and corresponding filling instructions.

Still within this scope, AT has:

- A face-to-face service by appointment (APM);

- A telephone call center (CAT); It is

- e-Counter service on the Finance Portal, through which it can provide taxpayers with faster clarification of their doubts.

As part of inducing voluntary compliance, AT persisted in implementing alerts, as well as in the automatic issuance of divergences identified from regular crossings, based on information contained in the databases held by AT, thus enhancing the voluntary regularization of detected inconsistencies and the perception of the risk of the topics addressed.

Notices continued to be sent to taxpayers informing them of the proximity of deadlines for complying with your tax and customs obligations.

Non-compliance risk management should include a broader set of interventions to correct the identified risks, and the use of inspection should only be for the most serious situations. financial, economic and fiscal complexity, in which the materiality of the values involved justifies the investment of time and resources, as is the case with tax and customs fraud and evasion. In 2022, the inspection action continued to be directed towards combating high-level fraud. complexity and the informal economy, with the identification and detection of conduct fraud, and the identification of abusive tax planning schemes.

2.4. The Economy and digital transformation in the fight against fraud

The rapid development of the digital economy has introduced a new paradigm in the economic process and commercial, which is characterized by the intangible nature and the dematerialization of new business models, as well as the way these businesses are carried out in this new digital era.

Quickly, new concepts such as “cryptoassets”, “mining”, “blockchains” became part of the everyday life and brought with them new challenges, not only at a fiscal level, but also legislatively, financial and criminal, which traditional control mechanisms are unable to respond to, due to their high degree of complexity and lack of legal predictability.

The dematerialization associated with the use of these new systems and technologies makes identification difficult, location and control of the tax fact, posing a challenge for tax authorities. A articulation and cooperation between the various entities is crucial to ensure that the digital economy is taxed in a fair and equitable manner, allowing the continued development of the digital market and companies that operate in it.

In this context, the BEPS project (Base Erosion and Profit Shifting) and the development of effective and efficient international information exchange mechanisms, which allow AFs to exchange essential information about transactions, income and subjects, allowing AFs to AF require compliance with tax obligations.

The international community, in particular the European Union, the G20, the Organization for Cooperation and Economic Development (OECD) and the United Nations, have made an effort not only to debate these issues, but also to try to legislate on these matters, examples of which are theAdministrative Cooperation Directives (DAC) 7 and 8, OECD Crypto-Asset Reporting Framework1 (CARF), Operators with respect to Sellers in the Sharing and Gig Economy.

MiCA (European Regulation for the Cryptoasset Market) and Model Rules for Reporting by Platform Despite the use of digitalization and new forms of digital economy can be used to hide capital arising from the practice of illicit activities, digitalization can be viewed in a positive way, and all its power to support compliance must be observed and enhanced voluntary on the part of citizens. For example, pre completing tax returns, communications through the VAT Information Exchange System (VIES) system, increase transparency between the subjects of the legal-tax relationship, allow the reallocation of human resources to operations of high financial complexity, as well as easier and faster identification of situations of fraud and tax evasion.

To this end, it is essential to develop, in the long term, a data management strategy, in which it is other stakeholders and with the taxpayers themselves. A descriptive, predictive and prescriptive analysis of the analyzed data was carried out, in conjunction with the increasingly, digital transformation and the digital economy will influence and determine not only the way and the way in which economic transactions are carried out, as well as the way in which income and profits are generated and obtained. The AT must be aware of this fact, and for this purpose it must monitor the evolution of the various sectors that make up the market and the digital economy, invest in training of its human resources and continue to develop the process of autonomy and dematerialization of its services..

2.5. Human resources and training

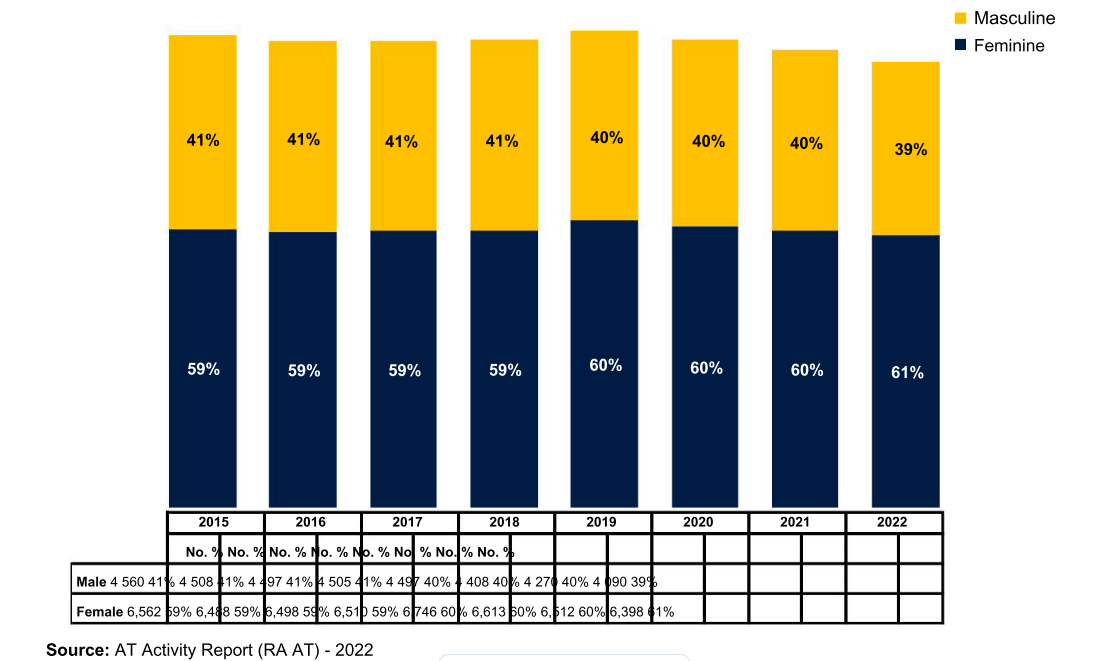

Throughout 2022, there was a reduction in the number of AT human resources by 294 people, rejuvenating them and providing them with different qualifications and new skills, having in 2022 been going from 10,782 to 10,488. There is a need to reinforce its staff, tests for access to the special tax and customs inspection and audit career were carried out, as well as of IT specialists.

1 Available at: https://www.oecd.org/tax/exchange-of-tax-information/crypto-asset-reporting-framework-and-amendments-tothecommon-reporting-standard.htm

Graph 1: Number of AT workers on December 31st of each year by sex

Regarding human resources management, the COVID-19 pandemic essentially marked the first four months of 2022, both in terms of resources directly affected by the disease and in terms of level of maintenance of changes introduced in the organization of work, whether in terms of guarantee of conditions to continue working remotely, whether in terms of implementation of health safety measures for facilities and workers.

Although in the second half of 2022 the impact of the COVID-19 pandemic was much greater reduced, the use of the teleworking model was maintained simultaneously with the work model in person.

At no time did AT’s activity cease to be ensured, highlighting its activities in the area of customs control and maintenance of face-to-face activity to support taxpayers in local services of finance.

TRAINING

As the training of AT workers constitutes one of the most important instruments for permanent updating of knowledge and reinforcement of skills, during 2022 AT invested in training, with 417 training actions, in which 25,210 trainees participated, corresponding in total to a training volume of 113,513 hours.

The number of workers who attended at least one training session was 8,511, which corresponded to a training level of 81%.

Contributed to the results of the training indicators, in a greater percentage, were the actions developed in the subareas:

- Tax Management – Income;

- Customs Management – Regulation;

- Tax and Customs Justice – Other Justice themes;

- Tax and Customs Inspection – Tax;

- Collection – Registration of taxpayers;

- Other transversal courses.

Given the direct and very specific impact on the qualification of technicians in anti-tax fraud units and customs (DSIFAE, DSAFA and the IT Center), the main beneficiaries of the training promoted in the areas of combating cybercrime and fraud, collaboration was maintained with the CEPOL (European Union Agency for Law Enforcement Training). In 2022, 180 participated AT workers in several webinars made available by CEPOL that focus on the topic “Fraud”2 .

2 CEPOL webinars that AT participated in: Tobacco fraud – illegal manufacturing of cigarettes; Counterfeiting and pharmaceutical products I and II; Cyber Telecom fraud; Document fraud investigation: Spanish helpdesk; Combating illegal production of cigarettes in the EU: Missing trader intra community fraud; Investment fraud.

2.6. Relevant results in 2022

2.6.1. Tributary and customs authority

2.6.2. General Finance Inspection

Among the most relevant results of the 2 audits carried out by the IGF in the field of combating tax fraud and evasion, in 2022, the following stand out:

a) In the Audit of the tax incentive system in research and business development (SIFIDE), the main conclusions were as follows:

ÿ Fiscal expenditure with SIFIDE registered a significant increase between 2017 and 2020 (from 137.2 million euros – M€ – to 396.4 M€), estimating a high impact of this expenditure during the legal deduction period, given the tax credit balance carried forward in 2020 (€448.6 M);

ÿ Situations of undue tax credit worth €3.2 million were identified, which were communicated to AT;

ÿ The result and impact indicators used in the audit, for the period 2018/2020, indicate for the effectiveness of the incentive on company results and job creation, but it is not yet there was consolidated data on projects during this period and the degree of implementation of the project was reduced. investment by companies dedicated to R&D;

ÿ Expenditure on R&D in the indirect aspect had a significant increase from 2017 to 2020: in the number of applications with contributions to funds (from 56 to 1,067), in the amount of expenses for contributions (from 11 M€ to 406 M€) and in the representation of the amount invested in Funds Risk Capital in total extramural financing, from 16% to 87%, having identified several critical aspects in the functioning of this aspect of the incentive;

ÿ Control of the conditions for granting/using the benefit was not adequately exercised, as the National Innovation Agency, SA (ANI) only carried out the qualitative validation of expenses, while AT considered that the validation of the respective value must be carried out by ANI, limiting As a rule, the values deducted are controlled in relation to those approved by ANI and the values to be reported to following exercises;

ÿ The control carried out by ANI presented the following shortcomings: lack of a risk analysis; lack of procedures to control the execution of R&D projects; no carrying out technological audits since 2015; outdated approval manual applications; absence of manual on recognizing suitability to practice activities of R&D; insufficient justification for the eligibility of expenses and incorrect calculation of operating expenses.

In view of these conclusions, which, in summary, highlight insufficiencies in ANI’s internal control and in the tax control developed by AT, as well as in the coordination between AT and ANI in controlling the benefit, recommendations were made to those entities in the sense of:

ÿ Implement a risk analysis strategy and develop execution control methodologies of R&D projects and carry out technological audits;

ÿ Address insufficiencies regarding the approval of applications, the recognition of suitability for the practice of R&D activities, justification of the eligibility of expenses and credit calculation Supervisor;

ÿ Ensure the rapid processing of company information, to allow the impact to be assessed of this tax incentive on the respective results, especially regarding the intervention of investment, also promoting a strategy aimed at controlling these;

ÿ Implement the SIFIDE current account and benefit control methodologies, as well as carry out inspection actions to regularize situations of undue tax credit identified in the audit;

ÿ Develop coordination between ANI and AT, in the control and inspection procedures of the compliance with the conditions for granting/using the benefit.

Proposals were also made to the Government, aimed at obviating or mitigating some critical aspects of the scheme, such as the exclusion of the eligibility of several expenses and the reduction of the period of investment of funds, among others. The proposals presented to the Government were considered in the within the scope of a proposed law, which has since been approved by the Assembly of the Republic.

b) In the Performance Audit – Reverse Charge Regime for VAT due on imports, the main

conclusions were as follows:

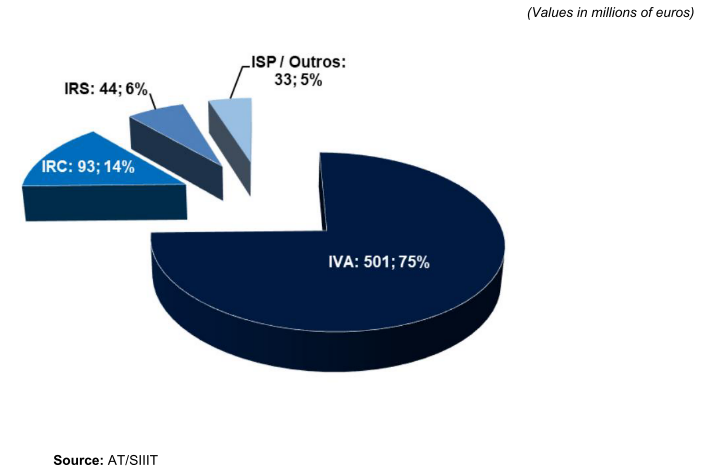

ÿ Control of the regularity of values between the amounts settled by the customs and those declared in the VAT periodic declarations (DP), having been identified, in the year 2019, 1139 taxpayers with discrepancies worth more than 1,000 euros, totaling €69.5 million potentially missing tax;

ÿ AT has not adequately controlled the obligation to submit the declaration of replacement by changes to the taxable value of VAT in the import customs declaration. At 18 taxpayers with regularizations exceeding 50,000 euros, 10 (55.6%) did not present the respective replacement VAT DP;

ÿ The computer system still did not allow the resolution of identified divergences and was in course on adapting the Divergence System for access by customs;

In view of these conclusions, which, in summary, highlight several shortcomings in AT’s performance in control of the scope of the Reverse Charge Regime for VAT due on imports, recommendations to that entity in the sense of:

ÿ Adopt a strategy to control the regularity of VAT amounts due on imports and declared by taxpayers in the periodic declaration, ensuring the completion of adaptations the system of divergences related to import VAT;

ÿ Promote the analysis and regularization of missing tax situations within the scope of divergences identified for the year 2019;

ÿ Promote the effective entry into production of customs systems (e.g. Customs Settlement) with a view to increasing the quality and integrity of the information recorded in the interface of VAT settlements payable in DP.

However, the aforementioned divergence detection procedure was implemented by AT, being applied in the analysis of tax periods corresponding to the year 2018 and following, having a high rate of voluntary regularizations was recorded.

3. ADDENDUM 2021-2022 TO THE STRATEGIC PLAN FIGHTING FRAUD AND TAX AND CUSTOMS EVASION 2018-2020 The 2021 2022

The 2021–2022 Addendum to PECFEFA 2018-2020 was marked by the COVID-19 pandemic, a which led to adjustments to the activity carried out by AT, namely, among other activities, respond to support needs for public support measures aimed at families and companies, in order to mitigate the economic and social impact inflicted by the pandemic.

A set of measures not yet implemented are carried over to PECFEFA 2023-2026, given its relevance and evolution of the socioeconomic and legal situation. PECFEFA 2023-2026 pays special attention to strengthening the fight against both the parallel economy and tax avoidance, as well as promoting citizenship and tax literacy and deepening the relationship between AT and citizens.

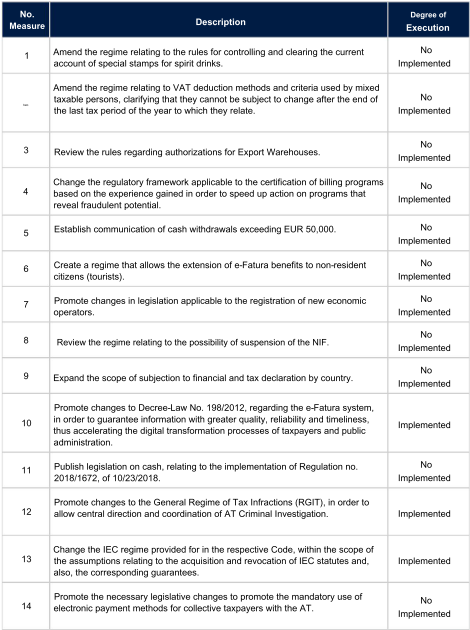

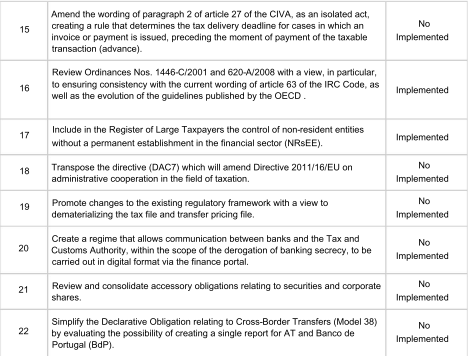

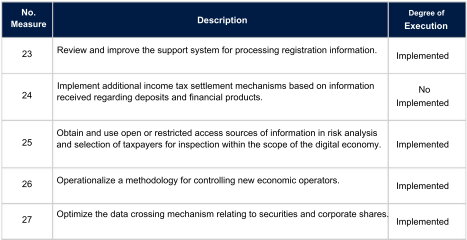

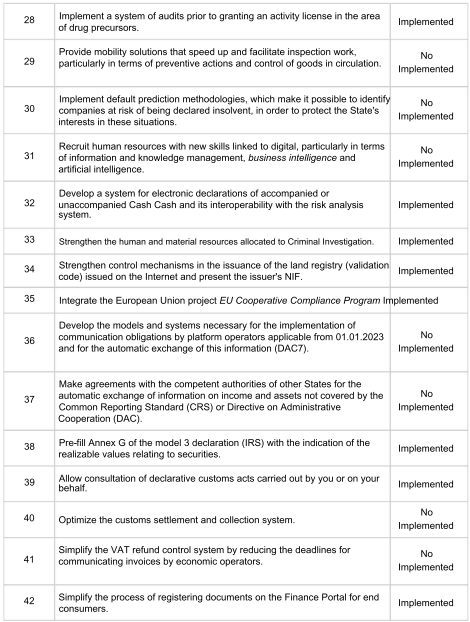

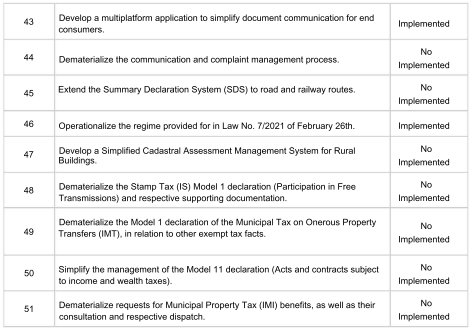

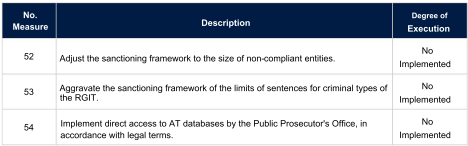

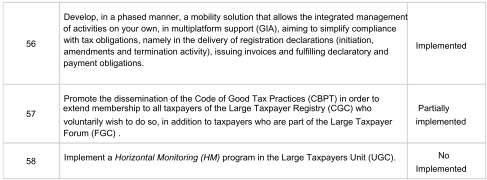

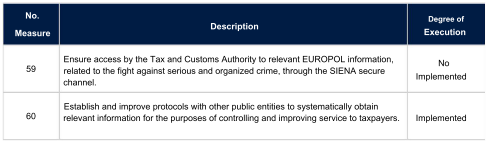

The following table presents the measures recommended in the 2021–2022 Addendum, duly tax evasion, as well as its degree of execution.

Table 1 – Legislative measures

Table 2 – Operational scope measures

Table 3 – Criminal measures

Table 4 – Measures within the scope of the relationship with the taxpayer

Table 5 – Measures within the scope of institutional relationships with other national and international public entities

4. ACTIVITIES TO COMBAT FRAUD AND TAX EVASION AND CUSTOMS IN THE INTERVENTION AREAS STRATEGIC IN 2022

4.1. Performance in the Scope of the Relationship with the Taxpayer

4.1.1. Taxpayer interaction and support

INFORMATION AND TAXPAYER SUPPORT MEASURES ADOPTED IN 2022

Compliance measures are based on two fundamental factors:

- The anticipation of initiative action by the tax administration, for moments that tend to contemporaneous with the practice of tax facts;

- The provision of information and knowledge necessary to carry out your treatment, so that action is a factor of understanding and added value for the promotion of voluntary compliance.

These measures always imply a strong commitment to assistance and support close to taxpayers, through either the telephone service channel or digital service – e-counter and assistant virtual – in fulfilling your tax obligations.

SUPPORT FOR VOLUNTARY COMPLIANCE

In 2022, AT intensified the dissemination of tax and customs information on social media, namely through:

- the YouTube channel (68 publications), where the focus was on promoting services, throughvideos and tutorials, with a strong compliance support component.

- Twitter (495 publications) where news and highlights from the customs area predominate and tax, with links to the Finance Portal. In 2022, more than 153 thousand were registered visits to the AT profile and 1628 new followers.

- the Facebook page (443 publications), where an average of 400 thousand was reached per month users and the number of followers exceeded 63 thousand. Of the published content, the focus is once again given to information supporting compliance, security alerts, news on seizures and actions to combat fraud and tax evasion.

- on Instagram (467 contents), where we gained 16,719 followers and reached more than 83 thousand accounts. In this social network we intend to reach a segment of the population that is in nding SMS (more than 525 thousand)

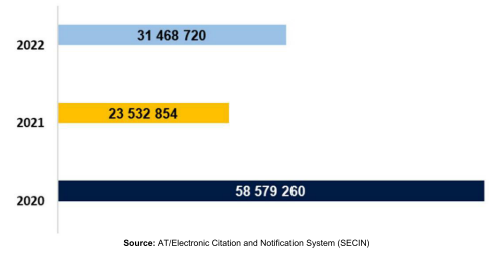

- alerts on taxpayers’ personal pages (more than 11 million), a huge increase principle of active age, with the publication of topics related to the activity being crucial professional, compliance support, as well as tax citizenship; 3; significant compared to the previous year4

- sending around 31 million electronic messages to taxpayers, an increase of around 33.72% compared to the previous year5, as per the following graph:

Graph 2 – Annual evolution of informative emails sent to taxpayers

In 2022, around 184 thousand emails were sent to self-employed workers who registered the start of activity throughout the year and approximately 162 thousand alerts on personal pages. This one procedure aims to support these taxpayers, indicating where to consult information relating to the compliance with declaratory obligations, consultation of tax status, among other situations available on the AT Portal.

3 The decrease in SMS compared to the previous year was due to the sending of SMS related to the IVAucher program in October and November.

4 The observed increase (from 473 thousand to 11 million) was related to the campaign for the new ATGo APP, validation of pending invoices for information, advantages in making contacts reliable and receiving emails and SMS from the Tax Authority and Customs.

5 In 2022, the increase in the sending of compliance emails was due to the fact that AT changed the frequency of its newsletters, going from quarterly (Newsletter) to monthly (Newsletter); as well as the information campaign on Adherence to Electronic Notifications and Citations on the Finance Portal (NCEPF).

AT NEWSLETTER

In terms of support and communication, in 2022 the Newsletter was reformulated quarterly digital “AT em Contacto”. To be closer to the taxpayer, it now has a frequency monthly and to be sent as a PDF attachment, allowing it to be viewed directly in the email.

With its first issue published in August, the now called “Newsletter” maintained The target audience is the broad segment of all individual taxpayers. In 2022 they were published the first five issues that are available on the Finance Portal, on the Support page Contributor, in Useful Information. The Newsletter aims to be another communication tool for AT, which responds to the need for individual taxpayers to obtain relevant information that helps them voluntarily comply with the tax and customs obligations, as well as exercising their rights and guarantees.

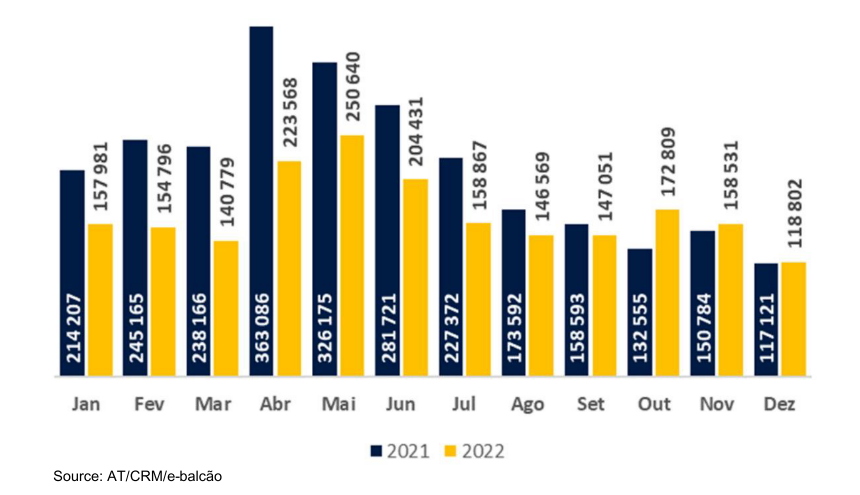

E-COUNTER | AT’S ELECTRONIC CUSTOMER SERVICE

The e-balcão is a customer service open every day, 24 hours a day, operating according to a logic nationwide electronic one-stop shop.

The system allows the reduction of the number of questions asked by taxpayers through the various channels, as the integration of channels through CRM (Customer Relationship Management) allows visualization by the attendant of the various interactions with the taxpayer, avoiding multiple responses to the same issue, as well as allowing the reduction of human resources allocated to face-to-face service and the relocation of these workers to tasks with greater added value.

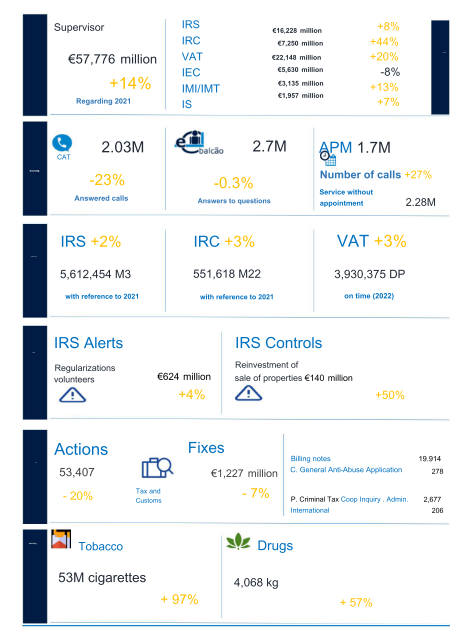

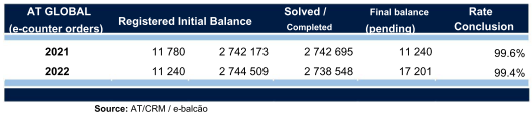

The e-balcão substantially eliminates the contextual costs that taxpayers bear in their interaction with AT. In 2021, 11,247 requests were transferred. In the year 2022, 2,744,509 new requests for information, of which 2,738,548 were responded to, corresponding to a national achievement rate of 99.40%.

Graph 3 – Number of information requests via e-balcon

IN-PERSON SERVICE BY APPOINTMENT | APM

With a view to improving the quality of services provided, AT implemented the “In-person Service by Appointment” (APM) which constitutes another channel that facilitates response made available to the taxpayer, through the following means:

- Finance Portal, electronically (Internet);

- Telephone booking, via the Telephone Service Center (CAT);

- In person, at local services (SF) and Customs.

APM operates on a platform, initially created only for CAT and SF and, since December 2016, extended directly to taxpayers through the Finance Portal where they can choose, within the availability, theme, location and opening hours.

The APM allows you to regulate service and communication with the AT, in a way that is convenient for the taxpayer, and AT also derives benefits from this type of service due to its predictability, anticipation and prior knowledge of the issue. It also allows the taxpayer to avoid having to go to work if you are contacted in advance by phone.

From a multichannel service perspective, the creation of an APP that allows users to taxpayer schedule a face-to-face appointment, contact the CAT or ask a question on e counter.

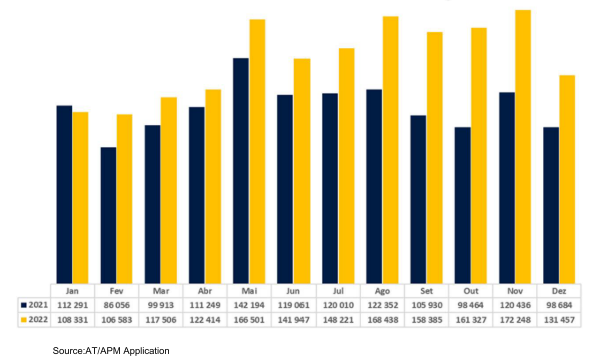

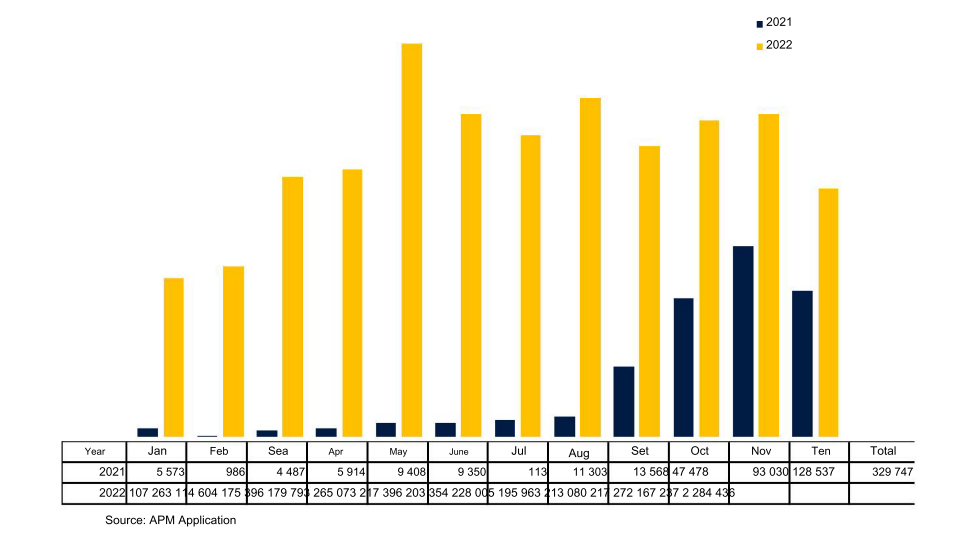

With the gradual return to normality after the pandemic, and regardless of the channels of alternative services that AT provides, there was a significant increase in demand for face-to-face service, which combines APM with spontaneous service.

Graph 2 – In-person service by appointment (evolution in the number of services)

From year to year, in-person service with prior appointment has increased, and in 2022 1,703,358 face-to-face services were provided, an increase of 366,718 services, approximately 27%, compared to 2021. However, taxpayer demand is below supply capacity, in hours, that AT makes available, so it is important to maintain the purpose of promoting this functionality, betting in providing a quality service.

Graph 3 – APM available and appointments

Source: APM Application

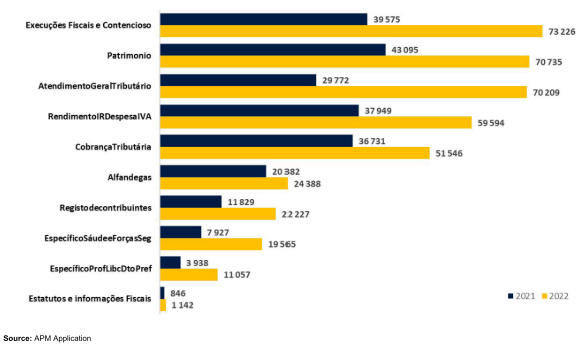

In the following graph, we can see the number of positions available to taxpayers, for aggregate subjects, in the years 2021 and 2022.

Graph 4 – APM – number of positions available by subject (aggregated)

Note: Given the change in the coding of options made in 2022, it is not possible to make exact comparisons with the document from the previous year.

As can be seen, the areas of Tax Executions and Litigation and Heritage are the ones that more positions are offered due to demand, followed by the opening of undifferentiated positions, noting if a deficit in relation to demand in the opening of taxpayer registration posts, usually very required for the attribution of NIF to citizens from third countries.

With the easing of COVID-19 measures, AT services also increased their capacity serve taxpayers, who go to the finance services spontaneously and without appointment, the increase in services compared to 2021 is visible in the following graph.

Graph 5 – Spontaneous Services

TELEPHONE CALL CENTER (CAT)

CAT remains a highly sought after service channel, not only because it avoids travel services, but also because it provides an immediate response to citizens, companies and economic operators.

To meet the demand of citizens, it was necessary to allocate to the CAT, in addition to the employees of the area of Communication, Promotion and Compliance Support Services, service workers deconcentrated areas of AT, namely with the collaboration and involvement of the Directorates and Services of Finance in the country, which allocated the necessary human resources depending on the alert levels expected, in order to respond to requests, while guaranteeing the quality of the taxpayer service.

We can see, in the next graph, that demand through this service channel decreased by 2021 to 2022, justified in part by the greater availability of face-to-face assistance in Services of Finance resulting from the easing of restrictions imposed by the COVID-19 pandemic:

Graph 6 – Telephone calls6

ONLINE HELP – VIRTUAL ASSISTANT

The Virtual Assistant (AV) – Catia – is AT’s electronic service channel available on the Portal das Finance, through online help and the “contacts” option, and allows taxpayers to receive assistance carried out in two ways: the first, available 24/7, results from the taxpayer’s interaction with the AV, with responses being fully automated using artificial intelligence; the second way service only occurs when there is no answer to the question posed by the taxpayer, or when this is not completely clarified, moving on to personalized service, carried out in real time by an AT professional, who answers questions asked via chat. O Electronic support via chat is available every working day, between 9:00 am and 19:00 hours.

The AV continues to have as its main objective to provide simple and concrete IRS answers to individual taxpayers without organized accounting. However, the content made available by AV were extended to other tax areas, namely Single Circulation Tax (IUC), obtaining the NIF, property taxes, access passwords to the Finance Portal, being

6 It should be noted that in the quantities presented in this graph, the calls “served” include calls answered by agents and those that are answered through the IVR (automations).

Also worth highlighting is the Fiscal Agenda. This is a project under “construction”, but whose focus is as a channel to support voluntary compliance is considered strategic in AT, from the perspective of integrated service across all channels.

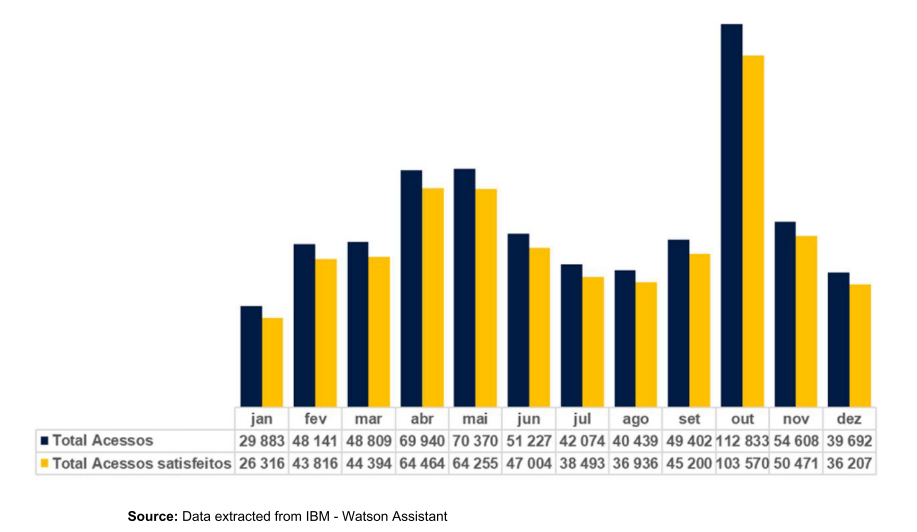

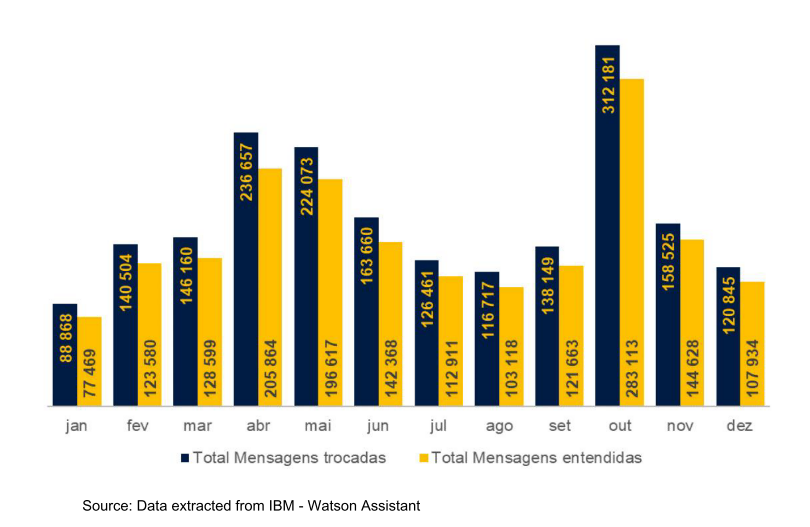

Some figures relating to AT’s AV, with reference to the year 2022:

Access to the Virtual Assistant

Graph 7 – Number of accesses vs. Number of satisfied accesses (monthly values – Year 2022)

Number of automatic messages exchanged with the Virtual Assistant

- In 2022, 1,972,800 messages were exchanged with the Virtual Assistant, of which 1,747,864 (88.60%) were understood. The average number of messages exchanged in each access it was three.

Graph 8 – Number of messages exchanged vs. Number of messages understood (monthly values in 2022)

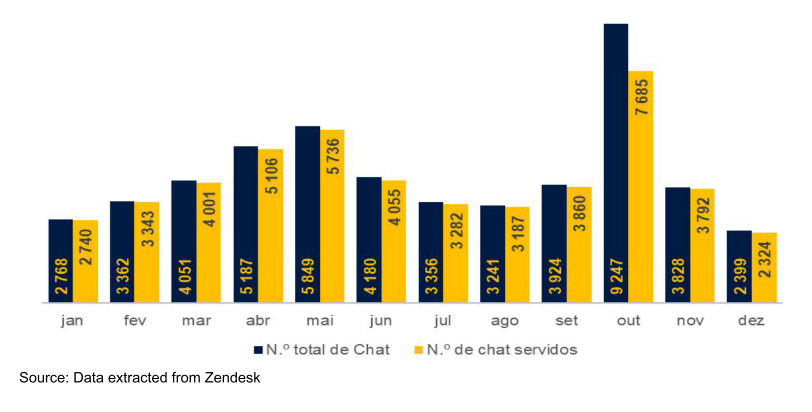

Services provided by AT professionals via CHAT

- In 2022, assistance from AT professionals, via chat, was requested by 51,392 taxpayers, of which 49,111 (95.56%) were assisted.

Graph 9 – Number of services requested from AT professionals via chat and % of services provided (monthly values in 2022)

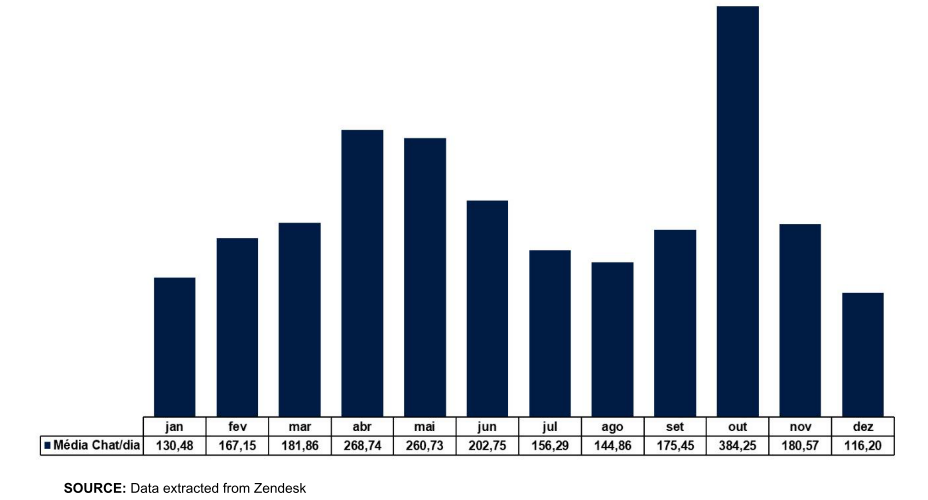

Average number of services provided by AT professionals through CHAT

- In 2022, the average number of chats handled by AT professionals was 195.66/day.

Graph 10 – Average number of daily calls made by AT professionals via chat (monthly values in 2022)

ACTIVITY AT THE TAXPAYER’S SCOPE

AT has been developing a set of strategies focused on promoting compliance voluntary, creating for this purpose the necessary conditions so that taxpayers and operators economic interests in general, can comply with their tax and customs obligations in a more simple, thus reducing the context costs associated with fulfilling these obligations.

These strategies have been oriented towards greater simplicity and transparency in the relationship with taxpayers and economic agents in general and have resulted in an increase widespread levels of voluntary compliance.

Examples of these strategies are:

- pre-completion of declarative obligations such as Automatic IRS or Automatic VAT,

- the availability of an increasing number of online services on the Finance Portal,

- the availability of APPs,

- issuing alerts and divergences,

- the availability and updating of information on the Finance Portal (information leaflets, tax calendar, FAQ’s, administrative guidelines, binding information, as well as a vast digital collection of models and forms, their respective data structures and corresponding filling instructions),

- the various publications on AT’s social networks (Youtube, Twitter, Facebook and Instagram),

- the provision of a set of contact channels such as e-Balcão, the Customer Service Center

Telephone service or the possibility of in-person scheduling by appointment, which were enhanced with new features:

o APM – the possibility of scheduling on the Finance Portal and creating of new themes

o E counter – the implementation of the service in the customs area

o CAT – the implementation of teleworking and the involvement of a greater number of workers made available by the different AT Finance Departments, as well as the reformulation of the CAT in the customs area, involving not only central services, but also also national customs and customs posts

- AV (Catia) – available on the Finance Portal 24 hours a day, 7 hours a week;

- Updated preparation of the fiscal calendar on the Finance Portal.

“LUCK INVOICE” DRAW

AT maintains as an incentive to promote voluntary compliance with tax obligations, the Draw “Lucky Invoice”. The draw began in April 2014, and in 2022 the prizes were made by Treasury Certificates (current issuance), issued by the Treasury and Bank Management Agency Public Debt – IGCP, EPE, with a value of 35,000 EUR in regular draws, and 50,000 EUR in extraordinary draws.

The objective of this initiative is to promote the tax citizenship of taxpayers in the fight against the economy informal, in preventing tax evasion and avoiding distortion of competition, in order to continue a more equitable tax system.

The participation of consumers, who when requesting invoices with NIF are automatically enabled to participate in the “Lucky Invoice” Draw, constitutes a fundamental element and works as a factor of regulation of national economic activity.

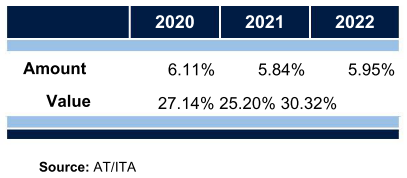

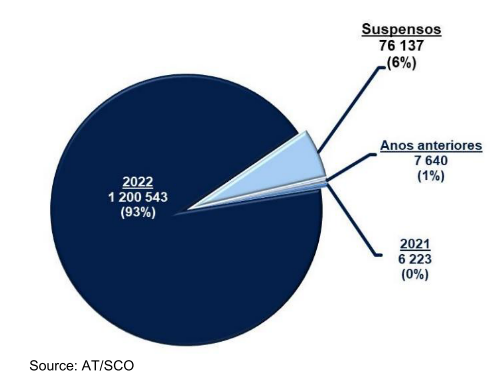

Due to structural contingencies, during 2022, the Fatura da Sorte draw was suspended in the end of February. It was resumed at the end of April, with all suspended draws having been recovered. O number of consumers eligible for the draws registered an average of 10,134,124 contributors, a variation of around 2.84% when compared to the same period in 2021 (9,854,713 taxpayers), as can be seen in the following graph:

Graph 11 – Evolution of the number of taxpayers eligible for the “Lucky Invoice” draws

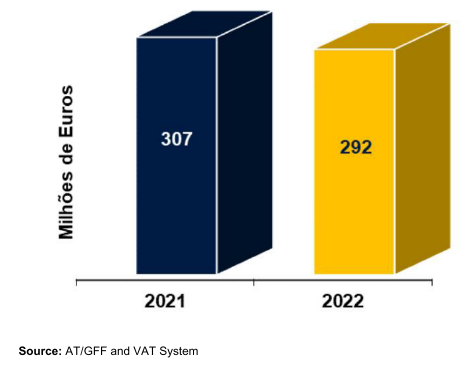

This trend is reflected in the 14.59% growth in the number of invoices with the taxpayer number (NIF), in 2022 compared to the same period in 2021, as well as the increase of 15.62% in the total value annual invoices (71,619,813,640 EUR) in 2022 compared to 2021 (61,943,178,941 EUR), according to the following tables.

Graph 12 – Evolution of the number of invoices eligible for the “Lucky Invoice” draws

Graph 13 – Evolution of the total value of invoices for the “Lucky Invoice” draws

Of the 58 “Treasury Certificates” awards awarded in 2022, 55% of the winners were of the same kind male (32), and 45% are female (26). The winners are distributed across seven tracks ages (ÿ30 years; 31-40; 41-50; 51-60; 61-70; 71-80; >80), it was found that the 51-60 age group (17 winners) represents 29% of the total number of winners, followed by the age group ÿ 30 years (13 winners) with 22%.

4.1.2. Declarative compliance

4.1.2.1. IRS

IRS MODEL 3 DECLARATIONS

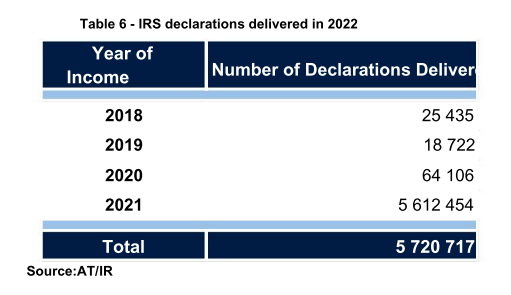

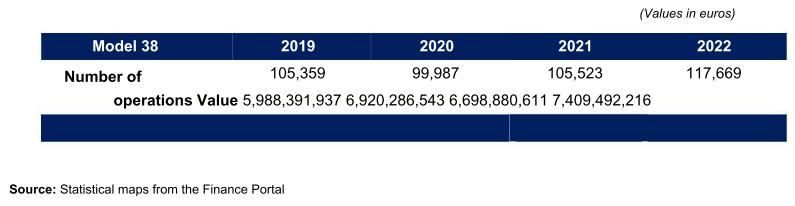

IRS Model 3 declarations received by 2022-12-31 and which are in force amount to 5,720,717, distributed as follows:

Table 6 – IRS declarations delivered in 2022

PRE-COMPLETION OF IRS MODEL 3 DECLARATIONS

In 2022, the project of partial pre-filling of Model 3 declarations of IRS, with more declarations being partially pre-filled – 6,137,163, compared to the year 2021 – 6,038,512.

This year, pre-filling of Annex G began for taxpayers who have received category G income, namely, capital gains arising from the sale of shares and of other securities. Thus, the declaration presents the following pre-filled data:

- Income from dependent employment (category A), property (category F) and pensions (category H) paid or made available to the respective holders;

- Withholdings at source made on income in categories A, B (incomeprofessional and business), F, G (asset increases) and H;

- Mandatory Social Security deductions for income in categories A and H;

- Union dues made in categories A and H;

- Payments on account under category B;

- Tenants’ NIF (attachment F);

- Individual retirement savings plans (PPR);

- Individual contributions to pension funds, mutual associations and others complementary social security schemes;

- Insurance premiums or contributions paid to mutual associations that cover exclusively health risks;

- Interest on debts related to the acquisition, construction, improvement of properties and contract installments concluded with housing cooperatives or in the group purchasing regime, with properties for own and permanent housing or rental for permanent housing of the tenant;

- IBAN;

- Donations;

- NIF of dependents, civil godchildren and dependents in joint custody, as well as the fields relating to Alternate Residence, % of Expense Sharing and Parental Responsibility, for dependents in joint custody;

- Income from dependent work obtained and respective withholdings supported, in the scope of the tax regime applicable to former residents, in accordance with article 12-A of the IRS Code;

- Income from independent work (category B), for taxpayers registered exclusively in the activities provided for in the table of article 151 of the CIRS, with the exception of code 1519.

- Income from capital gains (category G), for taxpayers who carry out the sale shares and other securities.

This year, a total of 1,944,362 automatic IRS declarations were settled, of which 1,806,331 declarations were confirmed by taxpayers, with the remaining 138,031 were settled at the end of the legal delivery period, in accordance with paragraph b) of paragraph 4 of article 58.º-A of the IRS Code.

OFFICIAL IRS SETTLEMENTS

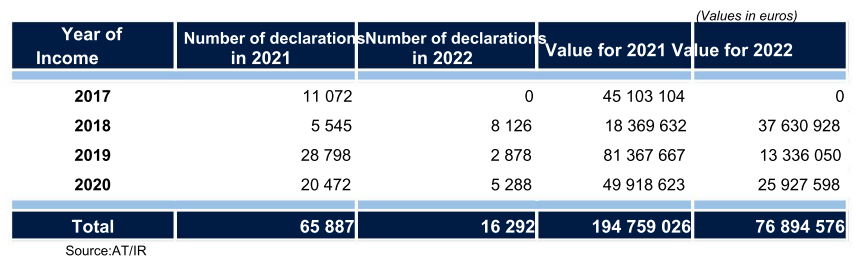

Regarding the number of IRS Model 3 declarations detected missing, during the year 2022, it is noted compared to the previous year, they decreased significantly, both in quantity and value, having 16,292 settlements were made (65,887 in 2021), which translated into an amount of 76,894,576 EUR (194,759,026 EUR, in 2021). This decrease in 2022 was due to the fact that the first 01-12. On that date, 22,573 settlements were generated centrally, resulting in a value of generation of unofficial declarations of Model 3 defaulters from the year 2019 only occurred in 2021- 52,210,861 EUR.

Table 7 – IRS settlements for defaulting taxpayers (2021/2022)

IRC

IRC MODEL DECLARATIONS 22

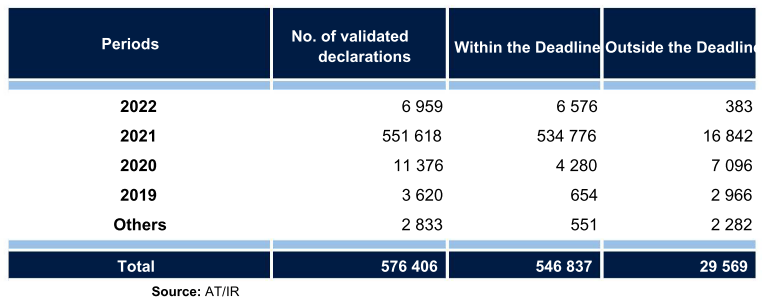

During 2022, 576,406 declarations relating to several tax periods, as can be seen in the following table:

Table 8 – IRC Model 22 declarations received during 2022

Of these declarations, 546,837 were delivered within the legal deadline and 29,569 after the deadline, the latter corresponding to 5.13% of the total validated declarations. The latter include declarations submitted voluntarily following inspection actions. Compared to the In 2021, a further 15,808 declarations were received in 2022, which corresponds to an increase of 2.82%. During 2022, a further 11,044 declarations were also received within the deadline legal, which corresponds approximately to an increase of 2.06% compared to the previous year.

Regarding declarations submitted after the legal deadline, from 2021 to 2022, a increase of approximately 19.21%, corresponding to 4,764 more declarations.

Regarding the type of declarations delivered, 556,154 correspond to first declarations and 20,252 to replacement declarations, 3.51% of the total validated declarations, as possible check the following table.

Table 9 – First declarations and replacement declarations

PRE-COMPLETION OF IRC MODEL 22 DECLARATIONS

The automatic pre-filling of the Model 22 income statement has not changed during the year 2022, compared to that implemented in previous periods.

The existing automatic pre-filling of the following fields of the Model declaration was maintained 22 of the IRC, through cross-referencing with registration and financial information, which correspond to the which had already been made available in previous periods:

- in table 02 of the cover, the field “Finance Service” and the “Code”;

- in table 03-1 of the cover, the “Designation” field;

- in table 03-3 of the cover, the field “Type of taxable person”;

- in table 10, field 359 “Withholding taxes”, field 360 “Payments on account” and the field 374 “Additional payment on account;

- in table 12 “Withholding taxes”, in field 1 the “Tax identification number” and in field 2 the value of “Withholding taxes”.

FAILURE TO SUBMIT CIT MODEL 22 DECLARATIONS

During 2022, around 33,319 warning letters were issued to defaulting taxpayers. IRC Model 22 income declaration, for the period 2021, for regularization purposes voluntary declaration obligation and payment of self-assessed tax.

OFFICIAL IRC SETTLEMENTS

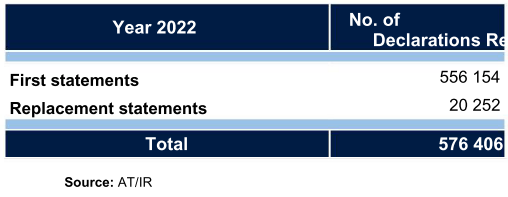

As a form of reaction to declaratory non-compliance, article 90 of the Tax Code on Income of Collective Persons (CIRC) provides for the issuance of unofficial settlements when the taxpayer does not submit the income declaration or self-assess the tax due.

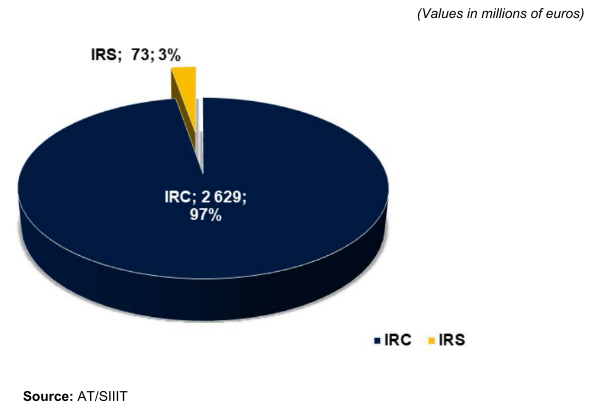

In the year 2022, 22,125 unofficial settlements relating to for the period 2021, corresponding to a global tax base of 961,255,799 EUR and a collection of IRC totaling 200,650,521 EUR.

Throughout 2022, an additional 794 unofficial settlements were generated relating to periods prior to 2021, corresponding to a global tax base of 55,064,578 EUR and a collection of IRC totaling 11,501,669 EUR.

Table 10 – Official IRC settlements

4.1.2.2. VAT

PERIODIC VAT DECLARATIONS

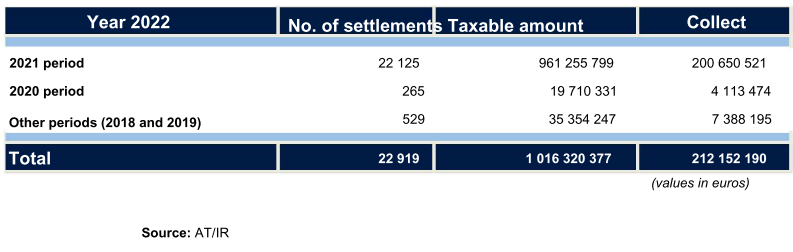

The level of voluntary compliance with the submission of the periodic VAT declaration (DP), for the periods on a monthly basis. VAT for the year 2022 was on average 93.9% on a quarterly basis and 97.3% on a quarterly basis.

Table 11 – Level of voluntary compliance with the submission of the VAT periodic declaration (DP)

The degree of voluntary compliance with the obligation to submit the periodic VAT return results from the ratio between the total number of periodic declarations submitted by taxpayers, within the deadline legal date of delivery and registered as the first declaration and the total number of declarations in force.

AUTOMATIC VAT

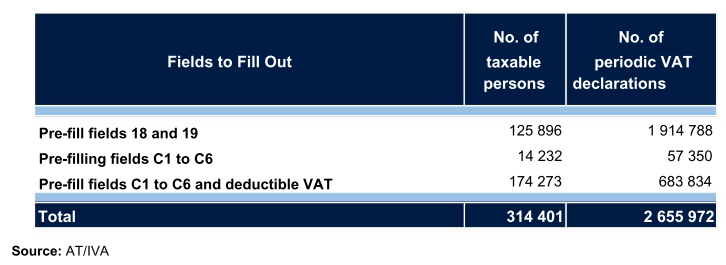

Within the scope of automatic VAT, with reference to the 2022 VAT periods, they were partially prepaid more than 2.6 million declarations were completed, relating to around 314 thousand taxpayers.

Table 12 – Automatic VAT – VAT Periods 2022

PRE-COMPLETION OF VAT DECLARATIONS

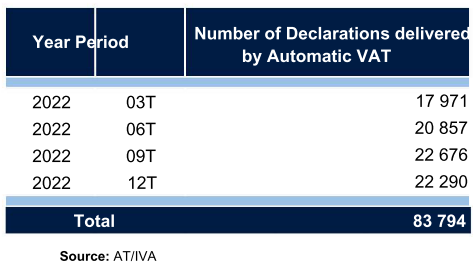

For the quarterly periods, VAT returns for the year 2022 were pre-filled, within the scope of the Automatic VAT, more than 83 thousand VAT declarations.

Table 13 – Pre-filling of quarterly declarations 2021

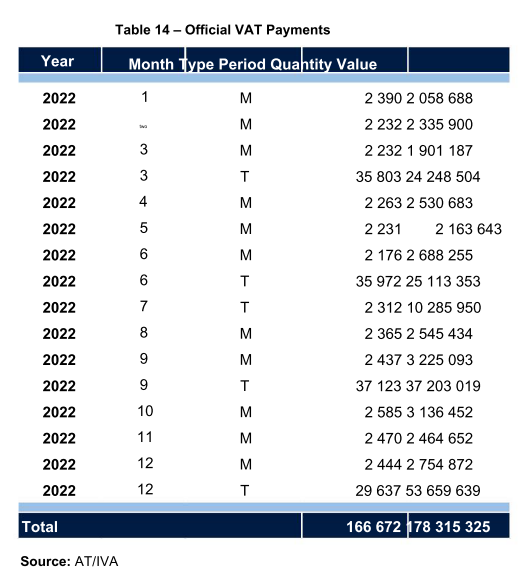

OFFICIAL SETTLEMENTS IN NUMBER AND VALUE ISSUED REGARDING VAT

Furthermore, with reference to the 2022 VAT periods, more than 166,000 assessments were issued VAT unofficials, which correspond to around 178 million EUR of tax paid.

E-TAX FREE

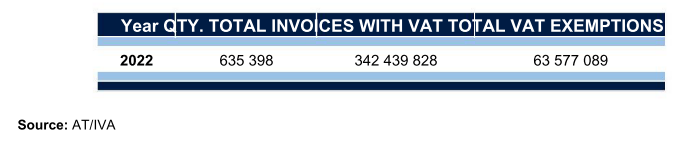

In 2022, more than 635 thousand invoices were certified, corresponding to a total recognized value of VAT exemptions of around EUR 63 million.

Table 15 – e-TaxFree – Global Certified Invoices

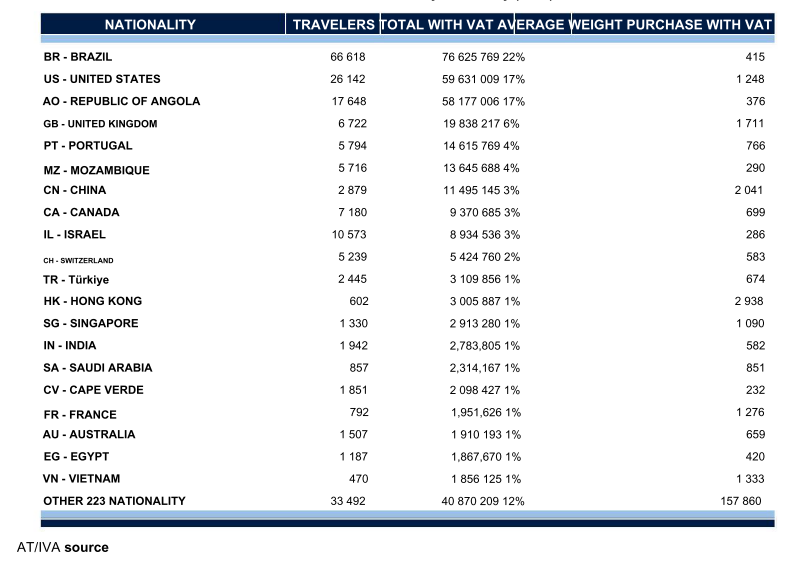

The nationals of Brazil, the United States and Angola, in a total of 243 nationalities, explain this order, more than half of invoices certified on e-taxfree.

Table 16 – e-TaxFree – Invoices certified by nationality (2022)

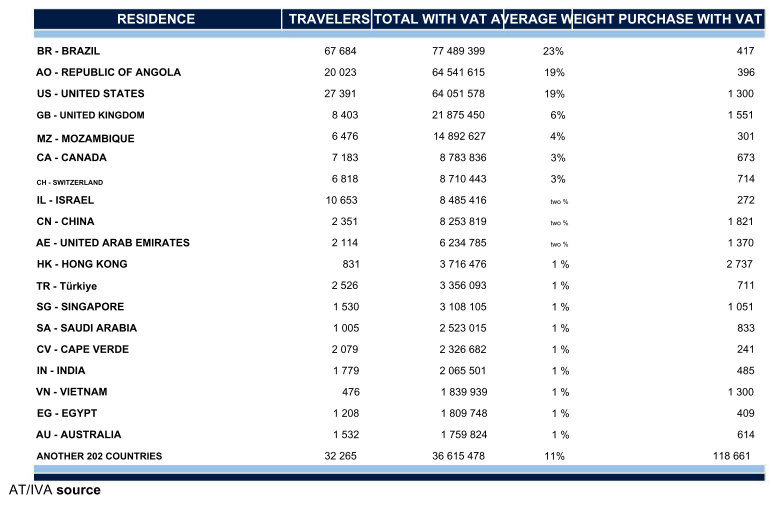

Residents in Brazil, Angola, United States, United Kingdom and Mozambique explain, in this order, more than 71% of the value of purchases with VAT that were subject to e-taxfree certification by country of residence.

Table 17 – e-TaxFree – Invoices certified by country of residence (2022)

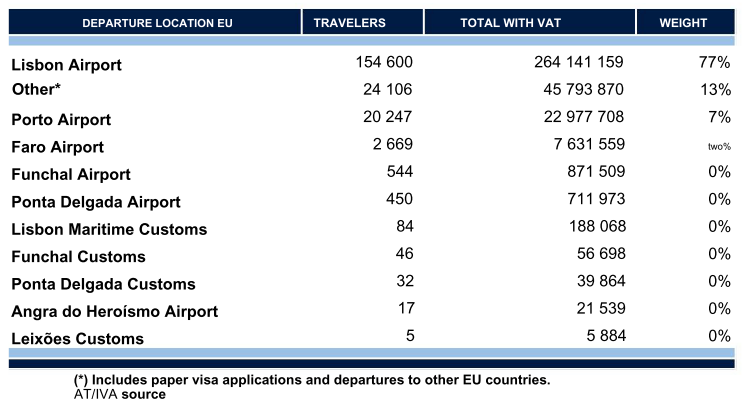

Lisbon airport is by far the main departure point for certified invoices, with a weight of almost three quarters of the total certified invoices.

Table 18 – e-TaxFree – Invoices certified by EU exit location (2022)

4.1.2.3. IMT/IMI/IUC and Stamp Tax

With the publication of Law No. 12/2022, of June 27, which approved the State Budget for the year 2022, changes were introduced to the IMT Code, with the objective incidence being extended.

- Onerous transfer of the right to sharecropping;

- Entry of partners with real estate to make additional payments;

- Adjudication of real estate to partners and investment fund participants closed real estate under private subscription;

- Entry of partners with real estate to pay up the capital of the remaining companiescivilians.

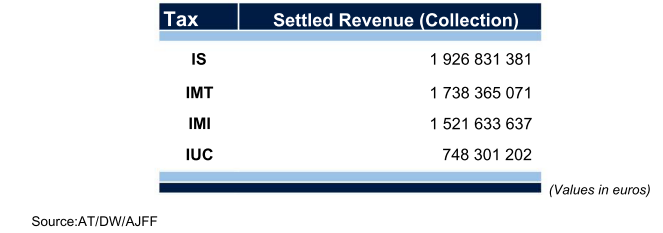

The following table presents the liquidated revenue associated with the various taxes in the area of heritage

Table 19 – Revenue paid by tax in 2022

It should be noted that the IMI is settled annually based on the taxable asset values as of 31 December of the year to which the tax relates. The amount settled, in 2022, refers to 2021 and years previous ones, with 8,172,307 EUR referring to rustic buildings, and 1,513,461,329 EUR referring to urban areas, totaling 1,521,633,636 EUR.

OFFICIAL SETTLEMENTS

In relation to the year 2022, 6,084 unofficial settlements were carried out in IMT and 644,560 in terms of IUC, which resulted in the amount of 1,655,683 EUR and 53,079,065 EUR of tax in missing, respectively. With regard to IS, the amount paid ex officio was 667,977 EUR.

4.1.2.4. Customs declarations / Special Consumption Taxes

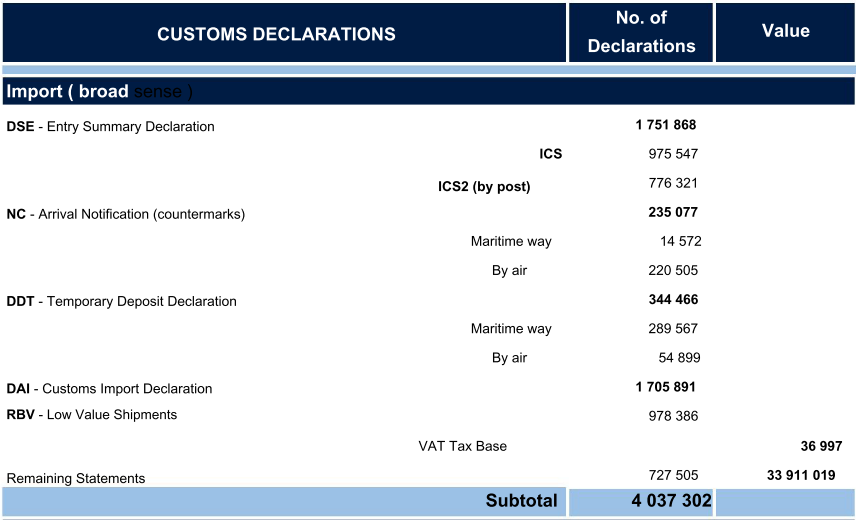

CUSTOMS IMPORT AND EXPORT DECLARATIONS

Table 20 – Customs Declarations

(amounts in thousands of euros)

Source: AT/Gestão Aduaneira

GLOBAL MAP OF NET CUSTOMS COLLECTION

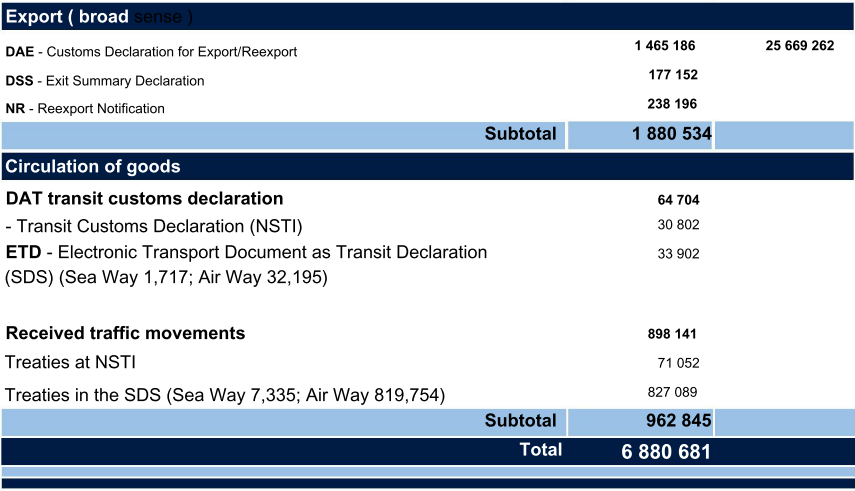

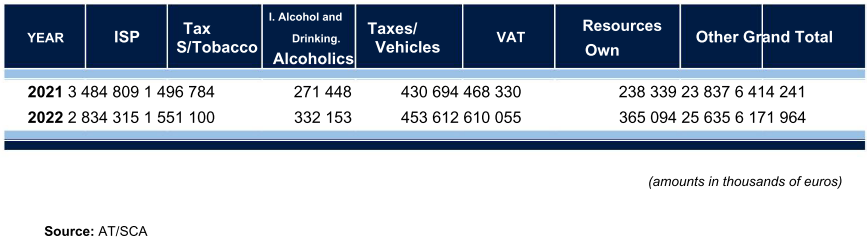

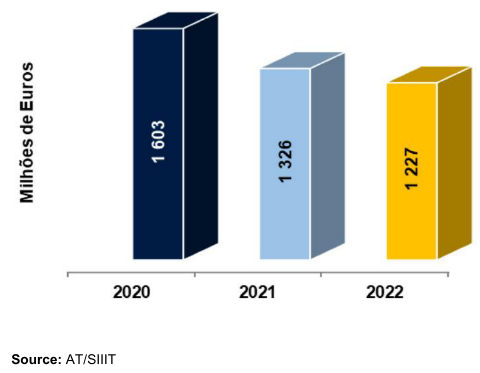

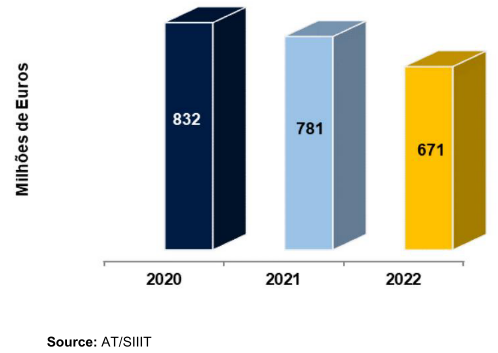

In global terms, net collections related to IEC and Vehicle Tax (ISV) calculated by Customs in 2022, amounted to 5,171.18 million EUR, showing a decrease of 9% (less 512.555 million EUR) compared to 2021, mainly justified by the drop on the ISP, as it develops further.

Table 21 – Net Customs collection

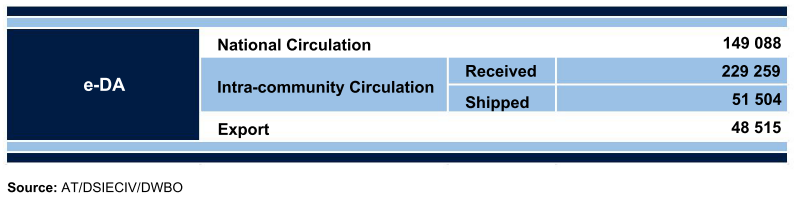

In 2022, in national territory, the following were registered by customs services:

- 353,112 Vehicle Customs Declarations (DAV) referring to imported vehicles and/oradmitted who obtained national registration, and

- 256,965 Electronic release for consumption declarations (e-DIC) referring to products subject toto excise taxes (IEC).

Table 22 – Statistics of electronic accompanying documents (e-DA) issued and received, for the year 2022

TAX ON PETROLEUM AND ENERGY PRODUCTS (ISP)

In 2022, ISP charges determined by Customs totaled 2,834.315 million EUR, amount that reflects a decrease of 18.66% (less EUR 650.494 million) in relation to the period same year last year (EUR 3,484.809 million).

This behavior is justified, in particular, by the Government’s measures (with emphasis on the reduction in ISP rates, which aim to mitigate the effect on the market of price changes for fuels).

TOBACCO TAX (IT)

In 2022, IT charges assessed by Customs totaled EUR 1,551.1 million, amount that reflects an increase of 3.63% (more EUR 54.316 million) in relation to the period same year last year (1,496.784 million EUR). The behavior evidenced by revenue reflects the evolution of economic activity and private consumption, with effects on the introduction of tobaccos.

TAX ON ALCOHOL, ALCOHOLIC DRINKS AND DRINKS WITH ADDITIONAL SUGAR OR OTHER SWEETENERS (IABA)

In 2022, IABA charges cleared by Customs totaled EUR 332.153 million, amount that reflects an increase of 22.36% (more EUR 60.705 million) in relation to the period same year last year (271.448 million EUR). The behavior evidenced by revenue reflects a recovery in economic activity and private consumption, with positive effects on the evolution of introductions into the consumption of products subject to IABA.

VEHICLE TAX (ISV)

In 2022, ISV collection by Customs totaled 453.612 million EUR, representing a variation of 5.3% (22.918 million euros more compared to 2021). This one behavior was due to the increase in vehicle sales in all categories, in particular, new and used passenger vehicles.

4.1.2.5. e-Invoice System

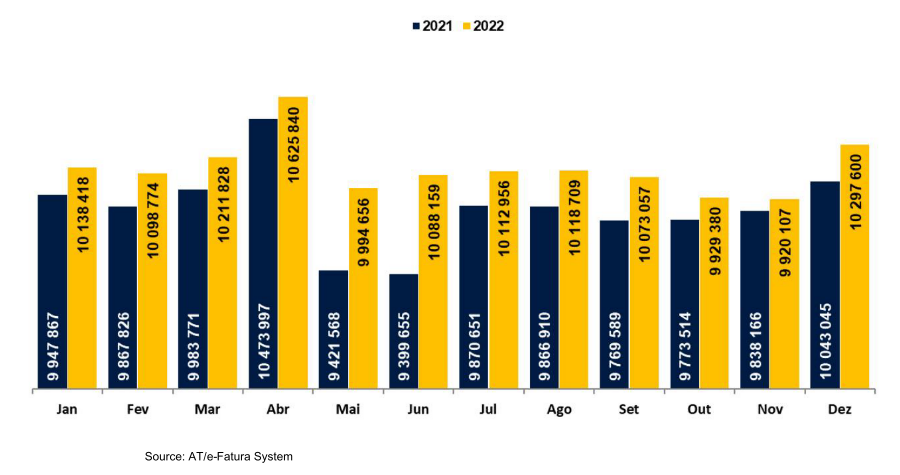

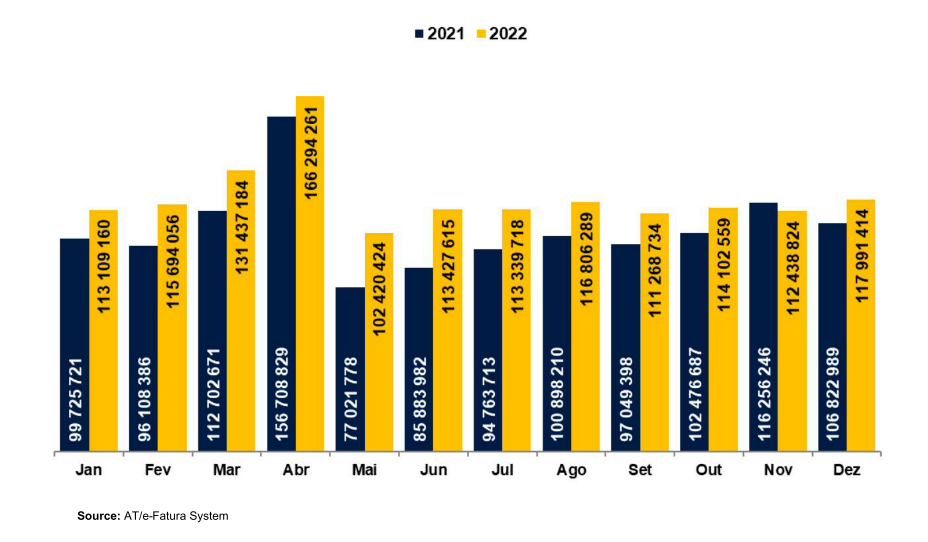

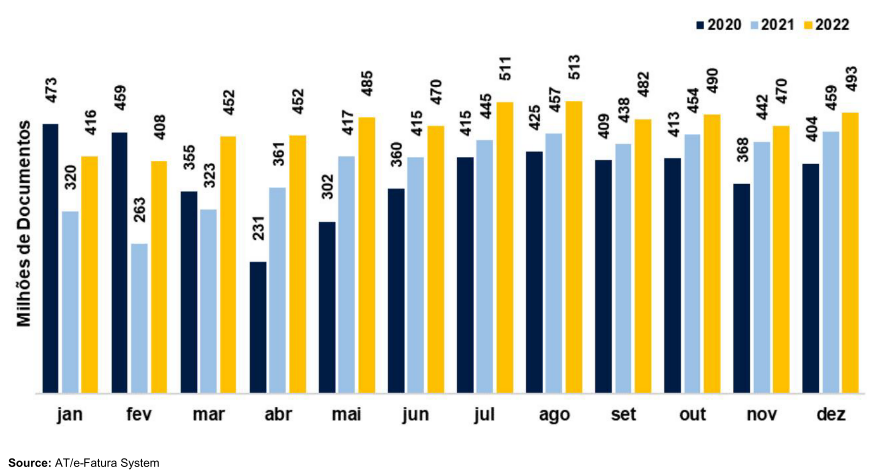

In 2022 there was a 17.7% increase in the number of documents communicated to the system and Invoice compared to the year 2021, with a total of 5,640 million documents having been communicated, which are approaches the number of documents communicated in 2019, which was 5.882 million.

Graph 14 – Evolution of the number of documents communicated to AT – 2020-2022 – per month

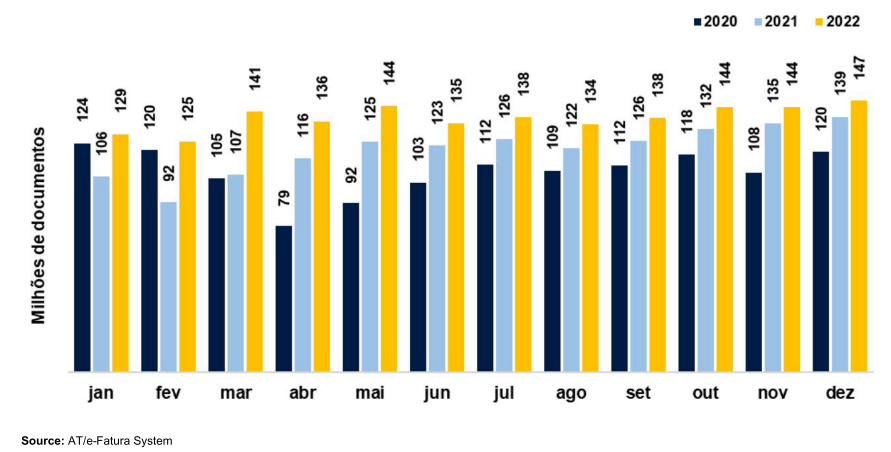

In 2022, 1,656,050,661 documents with NIF from a single acquirer were communicated, verifying an increase of 14.26% compared to the previous year.

Graph 15 – Evolution of the number of documents with individual acquirer NIF from 2020-2022 – per month

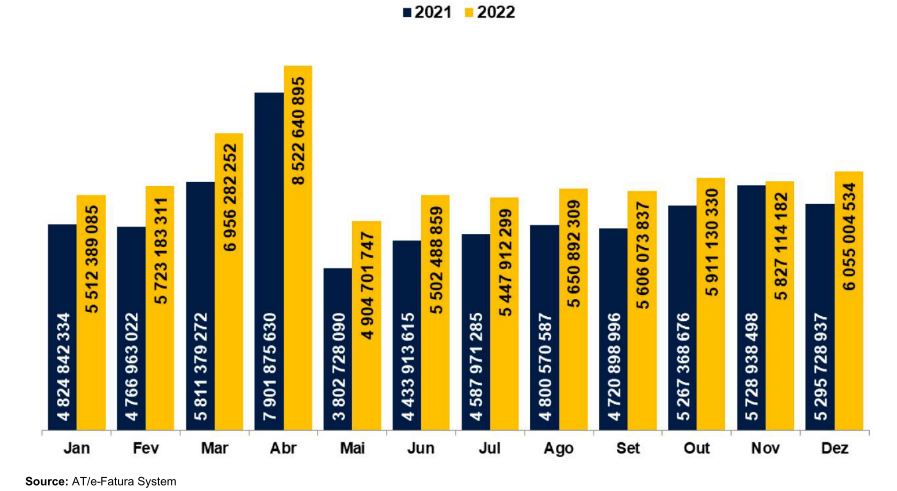

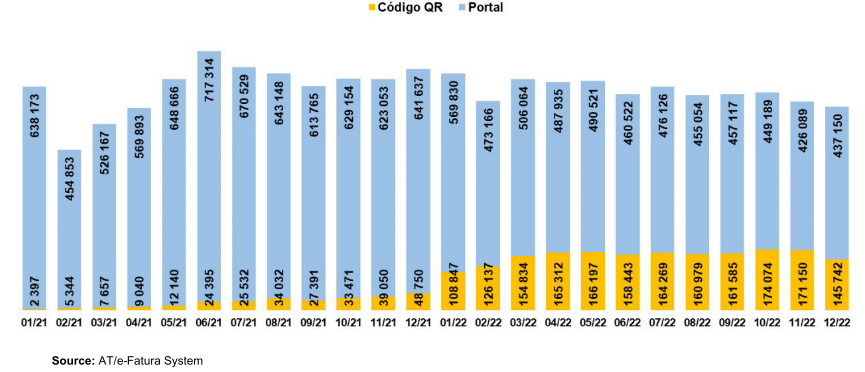

In 2022, the two-dimensional barcode (QR code) became mandatory on all invoices significant growth in the communication of invoices by acquirers using code reading issued through a certified invoicing program. As a result of this change, there was a QR, through the e

Fatura App, instead of registering on the Finance Portal. Of the 7,546,332 documents communicated by acquirers to AT during 2022, 5,688,763 were registered on the Finance Portal and 1,857,569 by reading the QR code using the App e-Invoice.

Graph 16 – Evolution of the number of documents communicated by acquirers from 2021-2022 – per month

TAX PAID, TAX DEDUCTED AND TAX RETURNED TO THE STATE – SECTORS WITH BENEFIT

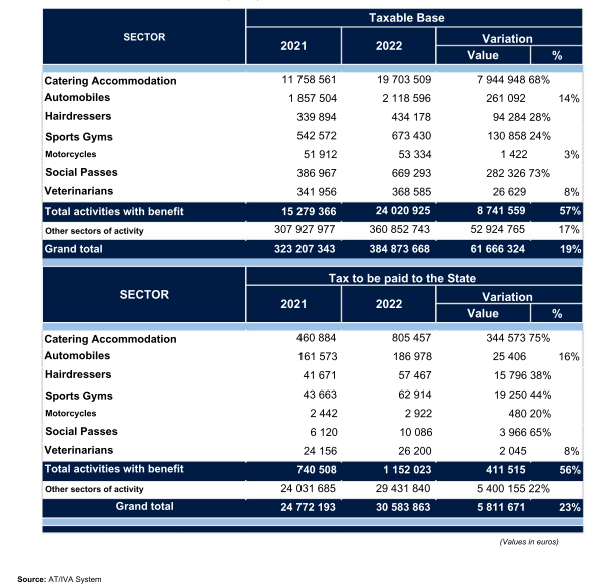

Issuing an invoice in specific sectors of activity gives the right to a tax benefit, provided that it is requested, at the time of acquisition of the good or service, the insertion of the NIF in the invoice, corresponding to the deduction of a percentage of the VAT incurred: 15% on car repair expenses and motorcycles, accommodation and catering, hairdressers and beauty institutes, veterinary activities, centers sports and gyms and 100% on monthly public transport passes.

In this sense, it is important to analyze the behavior of the sectors of activity that provide access to such benefit, given the overall performance of all sectors of activity, as well as evaluating its evolution by comparison between periods and the same period.

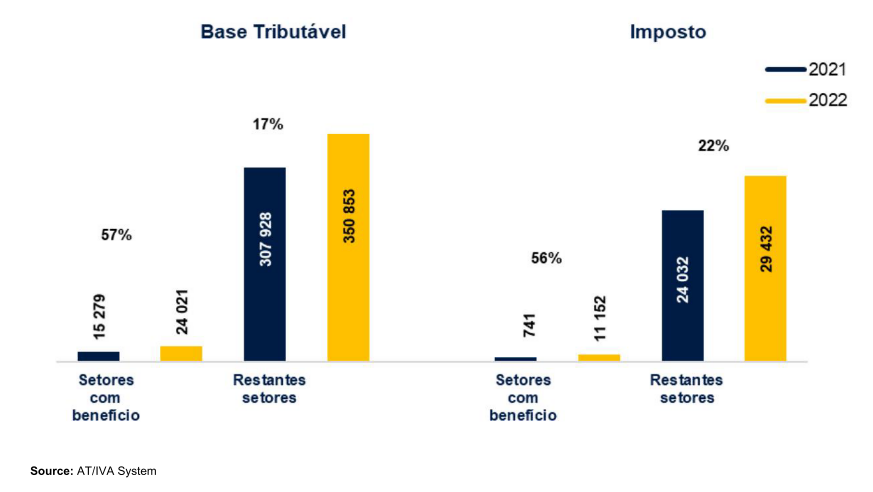

Table 23 – Annual VAT values by activity sectors – Variation 2021-2022

The variation in the level of activity calculated depending on the values of the VAT tax base, constant of the DP delivered with reference to the years 2021 and 2022, it was 19% (plus EUR 61 billion). The sectors of activity associated with the tax benefit that showed a slower evolution Significant were those relating to motorcycles and veterinarians (3% and 8%, respectively).

7 The values for 2021 differ from the corresponding RCFEFA 2021 table, due to changes in VAT DPs

This scenario was influenced by the end of restrictions on the normal exercise of activity, which still influenced the first half of 2021, providing a strong economic recovery, and the increase in the inflation rate8 that occurred during 2022

Graph 17 – Comparative analysis of the tax base / VAT tax between sectors with benefits and other sectors of activity – annual evolution 2020/2021

4.1.2.6. Transport document management system

The system for electronic communication of goods transport documents to AT came into force on the day 2013-07-01, for companies with a turnover equal to or greater than 100,000 EUR in the previous year. With this dematerialization process, it is no longer mandatory to track goods carried over from discriminatory paper documents. Since the communication of each transport must be carried out before its start, the system operates in real time with the activity of companies, reflecting, at all times, the ongoing operations of transport of goods.

8 In 2022 the inflation rate recorded an average annual variation of 7.8%. Consult: https://www.ine.pt/xportal/ xmain?xpid=INE&xpgid=ine_destaques&DESTAQUESdest_boui=577455859&DESTAQUESmodo=2

9 The values for 2021 differ from the corresponding RCFEFA 2021 graph, due to changes in VAT DPs.

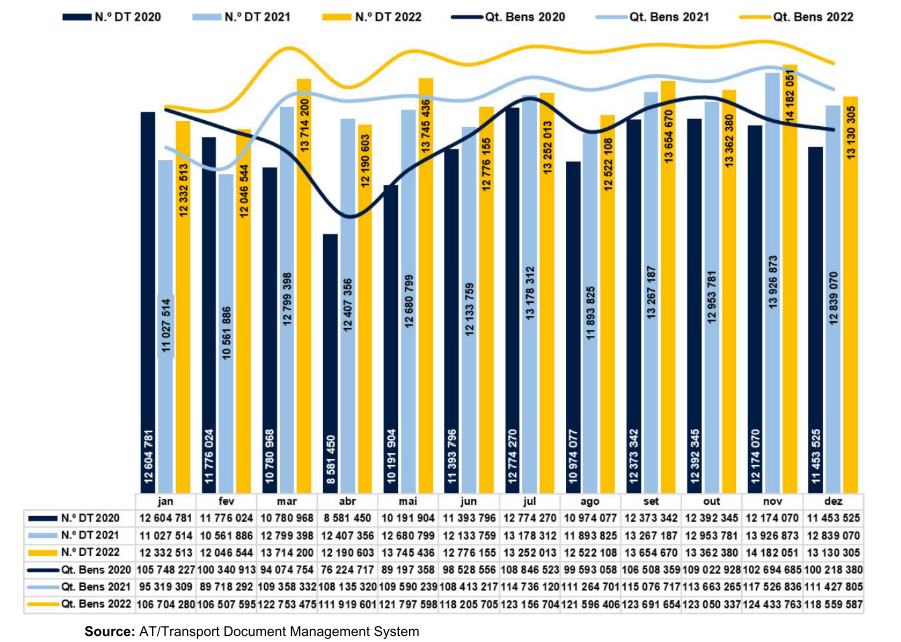

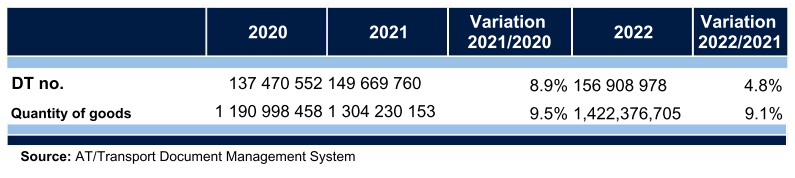

The number of transport documents (DT), as well as the total number of goods transported, relative to the year 2022, the evolution was reflected in the following graph:

Graph 18 – Monthly evolution of electronic transport documents and communicated goods

Table 24 – Annual evolution of the number of DTs and quantity of goods – Variation 2020-2022

In 2022, the growth trend in the number of transport documents and the quantity of goods communicated by more than 71,000 different economic agents, continuing the Webservice being the preferred channel for issuers, with around 88% of documents communicated this way. Because this communication is completely automatic and dematerialized, without the need for any additional human intervention, this option increases the efficiency of the companies’ operation, allowing to reduce the costs associated with fulfilling this obligation.

4.1.3. Taxpayer support alerts

4.1.3.1. Alerts to support voluntary compliance

The evolution of tax systems has led to increasing importance being given to promoting voluntary compliance. In this sense, AT has been giving greater importance to actions that support and help voluntary compliance, aimed at segments of taxpayers who, although they reveal some signs of tax non-compliance, they also appear to have an appetite for comply, if instructed to do so. In fact, among the taxpayers who do not comply, some will do so due to ignorance of the situation, or because, despite being aware that they are not complying, they do so because they feel divergences can play a relevant role due to the interaction it allows with the taxpayer, whether that their conduct is not serious or that it is not fully controlled by AT. In this case, the system of across:

- Alerts to support voluntary compliance with standardized responses pre-configured by the AT, selectable by the taxpayer that allows the detected non-compliance to be justified or assumed it in its different aspects, presenting instructions on how to remedy it;

- Discrepancies in which the taxpayer justifies the flagged nonconformities as he sees fit, allowing a detailed response from the customer, and can also attach documentation proof, which will later be analyzed by a technician, who will decide the steps subsequent actions, namely, when applicable, providing you with the necessary elements to regularize situations.

Alerts supporting voluntary compliance and divergences imply interaction between the AT and the taxpayers, with the purpose of remedying the flagged discrepancy, contrary to what happens with other tools to support voluntary compliance, namely information or warning alerts issued when completing some tax returns.

This interaction between the disagreement system and the taxpayer helps him to comply with more adequately fulfill its tax obligations, being aware that the regularization of the behavior will avoid further penalizing action by AT. The divergence system also allows recording cases in which the taxpayer believes that his behavior is in accordance with the law, presenting its justification. This, when accepted by AT, may prevent inspection actions, which may be unnecessary, from being triggered, reducing also litigation and enhancing the relationship with the taxpayer.

Finally, the record of the taxpayer’s interaction with the AT (whether response or absence of same) will allow the inspection, in its planning, to have an additional source of information, improving the efficiency of its operations.

Alerts are primarily measures to support voluntary compliance, whose main objective is to selected, due to the educational effect underlying them, at the same time that they call for the regularization of induce lasting future changes in taxpayer behavior on pre existing issues detected nonconformities.

In 2022, alerts were implemented in areas related to various taxes, namely:

- IRS:– Income earned abroad based on data reported through the Exchange Automatic Exchange of Information (AEOI);– Declared tax residence in Portugal;– Non-habitual resident with exemption method and income obtained abroad from categories B and E;– Imports that constitute evidence of the exercise of an economic activity.

- IRC:– Taxation of real estate capital gains arising from the sale of property investment;– Income resulting from the sale of properties;– Coefficient applicable in the Simplified Tax Regime (RST) to activities providing services similar to those provided for in article 151 of the CIRS.

- VAT:– Payment of VAT on intra-community acquisitions of goods and services;– Acquisition of electric or hybrid vehicles;– Inversion mechanism in the settlement of VAT on acquisitions of civil construction services;– Lack of regularization of VAT in favor of the State (Credit Notes);

– VAT wrongly deducted;

– Payment of VAT due for the import of goods in the periodic VAT declaration;

– Tax representatives: support for voluntary compliance with VAT and IR.

Below is a summary of the global results of the alerts implemented, reflecting the values indicated in the replacement declarations submitted by taxpayers, highlighting the regularizations carried out (some relating to previous years).

Table 26: Global assessment of the results of alerts implemented in 2022

Source: AT

Grades:

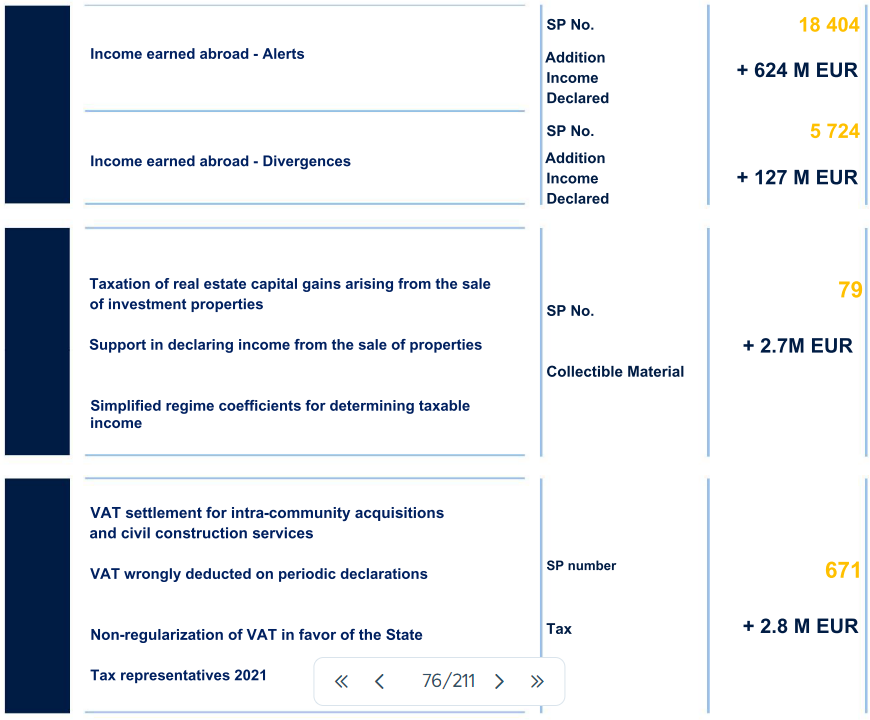

1. Alerts to support voluntary compliance relating to income obtained abroad concern the codes of

alert:

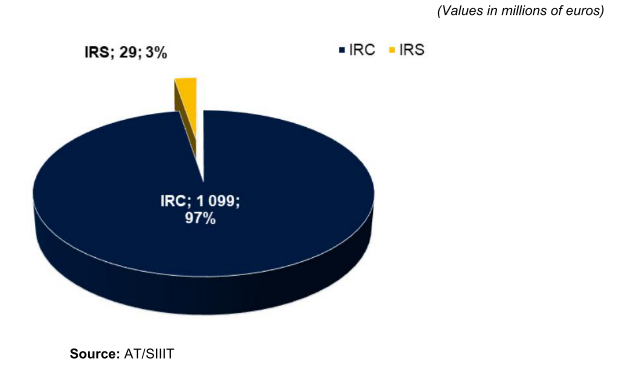

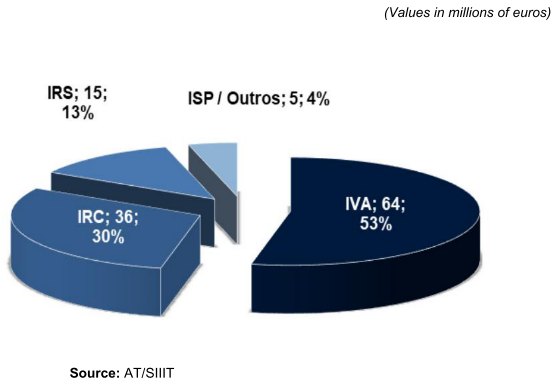

The. GR04 – Submission of the 2021 IRS declaration: The financial impact assessed by the increase in income obtained in foreign, declared in Annex J of IRS Model 3 for the years 2018, 2019, 2020 and 2021, was 586 million EUR. These voluntary regularizations were carried out by 18,380 taxpayers, representing 51% of the 36,205 SP selected;

B. GR31 – Specific item AEOI gross proceeds/redemptions: The financial impact assessed by the inclusion of this item in the Annex J of IRS Model 3 for the year 2019 was EUR 38 million. These regularizations were carried out by 24 taxpayers; w. R10 – Discrepancy resulting from the omission of income reported via DAC1 or DAC2/CRS/FATCA in Annex J addressed to 6,706 taxpayers: The financial impact assessed by the increase in income obtained abroad declared in Annex J of the Model 3 of IRS, referring to the year 2018, was 127 million EUR (70 million EUR resulting from voluntary regularizations made by 3,872 taxpayers and 57 million EUR resulting from unofficial corrections promoted by AT with 1,852 taxpayers).

2. Alerts relating to IRC concern alert codes GR36, 39, 40 and 41: The financial impact of these alerts, real estate gains and incorrect application of the simplified regime coefficients, assessed by the addition to the tax base, for the year 2020, it was 2.7 million EUR. These regularizations were carried out by 79 taxpayers representing 18% of the 433 contributors selected for these alerts.

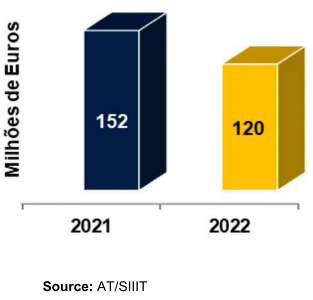

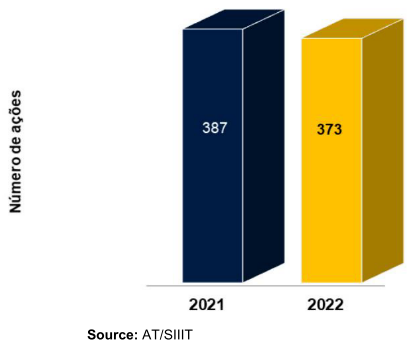

3. VAT-related alerts concern alert codes GR 25, 27, 28, 30, 34, 37 and 38: The financial impact of these alerts, VAT settlement on intra community acquisitions, civil construction services and undue deduction of VAT in periodic declarations, assessed by the additional tax for the years 2019, 2020 and 2021, it was EUR 2.8 million. These regularizations were made by 671 taxpayers representing 26% of the 2,615 taxpayers selected in these alerts.

It is also important to note that, in addition to the results indicated above obtained with the different alerts of support for voluntary compliance, greater declarative care was found when filling out different informative fields of the Simplified Business Information (IES), of the declarations periodic VAT and different registration and ancillary tax declarations, reducing discrepancies detected and translating into an “educational” effect of the alert on the different themes addressed, and so on, in the quality of the data, but which were not reflected in changes to the base taxable or tax, and are therefore not shown in the graphs above.

4.1.3.2. Alerts when filling out and receiving IRS model 3 declaration

In 2022, the alert system for filling out Model 3 declarations continued to intensify of IRS, delivered through the Finance Portal. This system is based on the crossing of information constant in the AT databases, namely in the monthly remuneration statements (DMR), in declarations Model 10, Model 44, among others, allowing to reduce settlement times, as well as litigation, simultaneously allowing more effective and effective control of the elements in-depth.

In the year under review, three new alerts were introduced, related to the income of the category G.

- Date of acquisition of shares and other securities inconsistent with the date of birth of the holder;

- Category G losses, arising from the sale of properties;

- Allocation of real estate to business and professional activities.

It should be noted that, in 2022, Model 3 declarations were presented exclusively via the Internet, totaling 6,137,163 declarations, as had been happening since 2018

4.1.4. Divergence control

4.1.4.1. IRS

CONTROL OF DIVERGENCES IN THE RECEIPT OF IRS MODEL 3 DECLARATIONS

In 2022, in the settlement of declarations relating to previous years, and similarly to what had already been carried out in previous years, automatic control of divergences was carried out, namely income, withholding taxes, personal elements, tax deductions, etc. In the total universe of 5,612,454 Model 3 declarations that were in the “current” state, relating to the year 2021, 158,530 divergences were detected (2.82% of the total).

This application made it possible to quickly and effectively resolve situations in which the declared elements by taxpayers differed from the elements known by AT, and which are normally provided by third parties. This fact can be proven by the reduced number of pending situations in 2022-12-31, which corresponded to 5,232, that is, 3.30% of the total

RELIQUIDATIONS DUE TO EXISTENCE OF DEBT

In 2022, 6,470 additional settlements of Model 3 declarations were made, relating to the years of 2018 to 2021, referring to taxpayers, whose right to tax benefits ceased due to not having the regularized tax situation. These additional settlements resulted in an increase in collections in the amount of 1,088,563 EUR, compared to the amount of 527,733 EUR, calculated in the previous year.

CONTROL OF REINVESTMENT RELATING TO PROPERTY GAINS

In 2022, AT carried out 6,598 additional settlements, referring to IRS Model 3 declarations, relating to the period 2018, due to the fact that taxpayers registered their intention to carry out the reinvestment, and have not carried out the total or partial reinvestment of the value of achievement obtained with the sale of properties, within the deadlines established by law. The aforementioned additional settlements resulted in increases in gross taxed income in the amount of 140,117,691 EUR. This amount is substantially higher than the increase in gross income taxed last year, for the same reason, and which corresponded to 93,409,214 EUR.

4.1.4.2. IRC

CONTROL OF TAX LOSSES DEDUCTIBLE UNDER ARTICLE 52 OF THE CIRC

The procedure for declarative control of tax losses deducted, in accordance with article 52 of the CIRC, to declared taxable profits, was subject to control for many years after the validation of the income declarations Model 22, by issuing notifications to replace the declaration, whenever the values did not correspond to the existing balance in the tax loss current account. Since 2019, control has been carried out through the central validation system, with the creation of central error codes and notification to taxpayers to correct them within a period of 30 days, as provided for in Ordinance No. 1339/2005 of December 30th.

This system allows correction of the submitted declaration itself, instead of replacing it. Like this new procedure, efficiency gains were obtained, as it was no longer possible to validate declarations with divergences in the amounts of losses, thus avoiding an analysis subsequent declarations. However, procedures were still introduced for periods prior to 2021, through the central system. The cases analyzed, in 2022, are essentially relating to the periods from 2018 to 2020, and smaller amounts of divergences. were carried out during 2022 the following corrections:

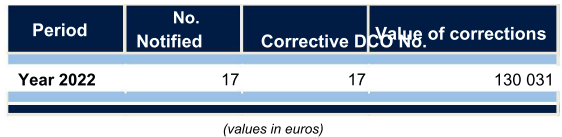

Table 25 – Control of deductible tax losses

Source: AT/IR

During 2022, only 17 taxpayers were notified, with discrepancies between the amounts deducted and those contained in the current account of tax losses.

17 Model 22 declarations were officially corrected through an unofficial correction document (DCO) and the respective corrective settlements were extracted. The value of the corrections amounted to 130,031 EUR, which correspond to the difference between the value of the tax losses declared by the taxpayer, in the field 309, in table 09 of the Model 22 declaration, and the tax losses corrected by services in the same field.

CESSATION OF DEDUCTION OF TAX BENEFITS IN CASE OF DEBT

In 2022, the Model 22 declarations submitted by taxpayers who deducted tax benefits and had debts at the end of the tax period in which the the tax event, which resulted in the reinstatement of the taxation rule. During the year 2022

The following corrections were made:

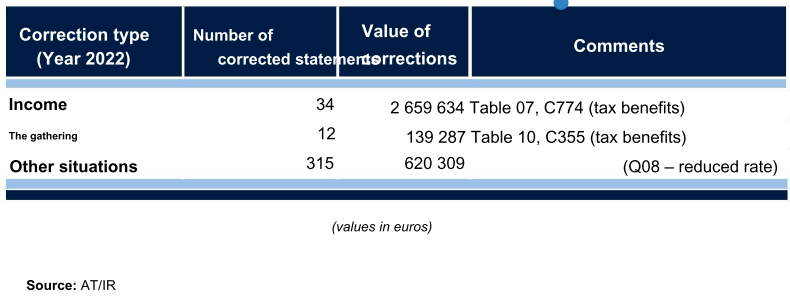

Table 26 – Cessation of deduction of tax benefits in case of debt

Tax benefits (namely income deductions, tax deductions and rate reduction schemes) in 361 IRC declarations.

Regarding tax benefits that operate by deduction from income, in 2022, 34 declarations not accepted, amounting to 2,659,634 EUR (field 774 of table 07 of Model 22).

Regarding tax benefits that operate by deduction from tax collection, 12 declarations that were not accepted, in the amount of 139,287 EUR (field 355 of table 10 of Model 22).

315 declarations were also corrected for other reasons, in most cases due to failure to acceptance of the preferential rate (reduced rate), the value of the corrections of which was 620,309 EUR. The biggest part of the cases had to do with the cessation of benefits to companies based in inland regions (art. 41.º-B of the Tax Benefits Statute (EBF)) and the remainder to entities licensed to operate in the Madeira Free Trade Zone taxed under the regimes of articles 36 and 36-A of the EBF.

CONTROL OF WITHHOLDINGS DEDUCTED FROM IRC COLLECTION

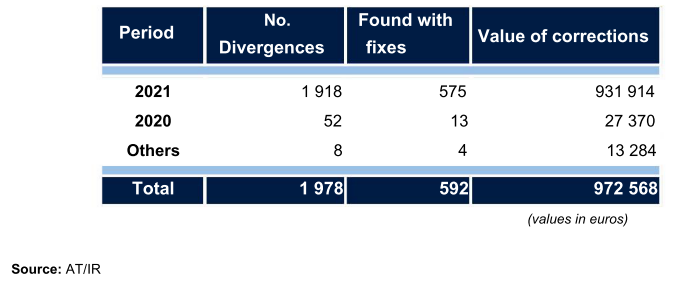

Regarding the control of the deduction of withholding taxes from IRC collection, which consists of detecting of divergences between the deductions shown in table 12 of the income declaration Model 22 and the withholding taxes shown in the Model 10 declarations, submitted by the debtor entities of income subject to withholding at source, the following were carried out during 2022 fixes:

Table 27 – Control of withholding taxes deducted from IRC collection

During 2022, 1,978 declarations with discrepancies in withholding taxes were processed deducted, of which 592 were subject to correction of the amount deducted in favor of the State, totaling 972,568 EUR. Most of the corrections were made to Models 22 from the 2021 period, whose campaign reception took place during 2022.

4.1.4.3. VAT

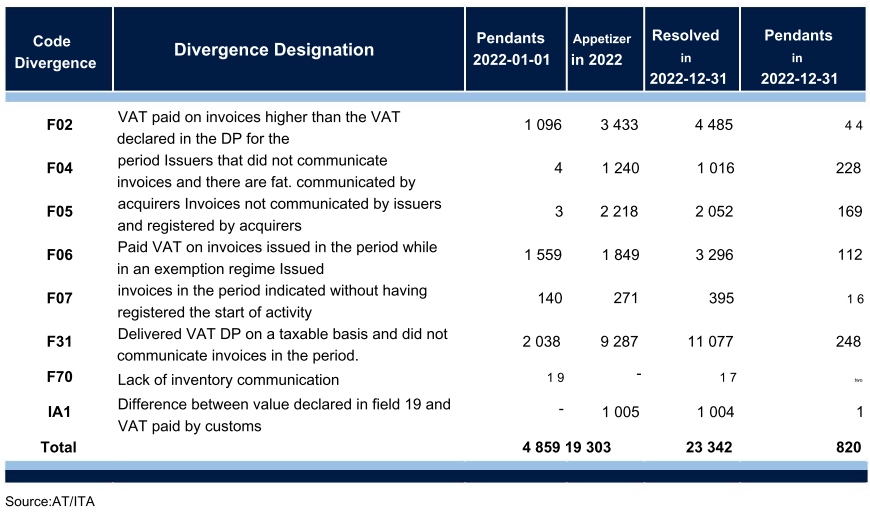

During 2022, the information received through e-invoice continued to be used for control of the VAT values declared in periodic declarations. 3,433 situations were detected for analysis, in which the VAT declared in the periodic declaration was lower than the VAT reported in the invoices (F02). 2,120 situations of non-delivery of VAT mentioned on invoices were also detected by taxpayers not registered to carry out any activity (F06), or by taxpayers registered in an activity, but under a VAT exemption regime (F07).

A new divergence procedure (IA1) was also initiated in 2022, aimed at controlling VAT declared in field 19 of the DP and the VAT paid by customs, on taxpayers who, by choice, fell under this regime10. In this procedure, 1,005 situations were detected.

10 With the changes introduced to articles 27 and 28 of the VAT Code (CIVA), by Law no. 42/2016, of December 28 (LOE 2017), taxpayers covered by the monthly periodicity regime began to be able to choose to pay the VAT due on imports of goods, through the periodic declaration referred to in subparagraph c) of paragraph 1 of article 29 of the CIVA, provided that the conditions set out in subparagraphs a) to d) of the CIVA are met. paragraph 8 of the aforementioned article 27, in its initial wording.

4.1.4.4. Invoice communication

With regard to monitoring compliance with the obligation to communicate invoices, 12,745 discrepancies due to lack of communication of invoices (F04, F05 and F31). The following table summarizes the results relating to VAT, e-invoice and inventory communication divergences:

Table 28 – VAT discrepancies, lack of communication of invoices and inventories11

4.1.5. Prior transfer pricing agreements