Skip to content

Skip to content Introduction

Part 1

In this article, we’ll explore obtaining the IRS transfer certificate and explain how Form 706NA and form 5173 apply to these cases.

Obtaining the IRS transfer certificate is a crucial step in the process of handling estates with non-resident aliens. Form 706 NA is the United States Estate (and Generation-Skipping Transfer) Tax Return for estates of non-resident non-citizens, while Form 5173 is the request for a certificate of release of a federal estate tax lien.

Understanding the intricacies of these forms is essential for ensuring a smooth and compliant transfer of assets. This article will provide a comprehensive guide, shedding light on the nuances of these processes and helping you navigate the complexities of estate management for non-resident aliens.

Part 2

Introduction to IRS Transfer Certificate and Form 706 NA

When a non-US Person passes with US situs financial assets, it often creates issues for descendants.

1. They are unable to access the accounts until they have an IRS Transfer Certificate.

2. They cannot get an IRS Transfer Certificate until they have a closing letter.

3. They cannot get a closing letter until they file the Form 706 NA

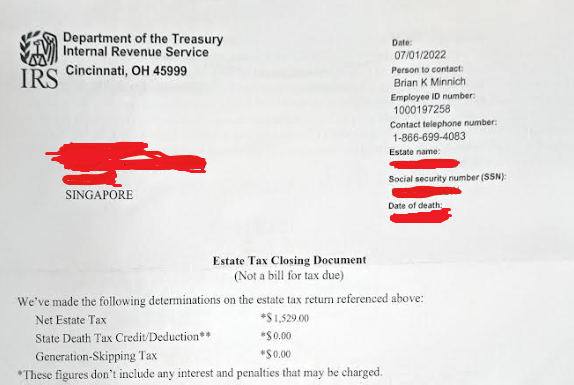

This is what a Closing Letter looks like

Let’s go through this step by step

The purpose of Form 706-NA

Internal Revenue Code (IRC) § 2101 imposes a transfer tax on the estate of any non-resident, non-citizen, of the U.S. Form 706-NA, United States Estate (and Generation Skipping Transfer) Tax Return, is used to compute estate- and generation-skipping transfer (GST) tax liability for all non-resident alien decedents. Form 706NA must be filed within nine months of the date of the decedent’s death. The taxpayer can request an automatic six-month extension by filing Form 4768 by the original due date. If Form 706 NA is not promptly filed, or the tax payment is not remitted by the original due date, penalties will be levied against the estate.

Form 706-NA is used to compute estate and generation-skipping transfer (GST) tax liability for nonresident not a citizen (NRNC) decedents. The estate tax is imposed on the transfer of the decedent’s taxable estate rather than on the receipt of any part of it.

For information about transfer certificates for U.S. assets, write to the following address.

Internal Revenue Service

Attn: E&G, Stop 824G

7940 Kentucky Drive

Florence, KY 41042-2915

Note:

In order to complete this return, you must obtain Form 706, United States Estate (and Generation-Skipping Transfer) Tax Return, and its instructions. You must attach schedules from Form 706 if you intend to claim a marital deduction, a charitable deduction, a qualified conservation easement exclusion, or a credit for tax on prior transfers, or if you answer “Yes” to question 5, 7, 8, 9a, 9b, or 11 in Part III. General Information. You will need the Instructions for Form 706 to explain how to value stocks and bonds. Make sure that you use the version of Form 706 that corresponds to the date of the decedent’s death.

Who must file Form 706-NA

Form 706-NA applies only to non-resident alien decedents – individuals whom, upon their death, are not U.S. residents or citizens. For purposes of determining estate and gift tax, residency is not determined by the residency rules for income-tax purposes (Sec. 7701(b)(6)). For estate and gift-tax purposes, U.S. residency requires physical presence at some place in the U.S., and the intention to make that place a fixed and permanent home (Christina de Bourbon Patino, 51-1 USTC ¶9123 (4th Cir.), aff’g, 13 T.C. 816 (1949)). If the facts and circumstances support the preceding notion of residence, the executor of the decedent’s estate must file Form 706.

The executor of a non-resident alien decedent’s estate must file Form 706-NA if the date-of-death value of the gross estate located in the U.S. exceeds the filing limit of $60,000.

The executor must file Form 706-NA if the date of death value of the decedent’s U.S.-situated assets, together with the gift tax-specific exemption and the amount of adjusted taxable gifts, exceeds the filing threshold of $60,000. The gift tax-specific exemption refers to the amount allowed for gifts made by the decedent between September 9, 1976, and December 31, 1976, inclusive. The amount of adjusted taxable gifts refers to the amount of adjusted taxable gifts made by the decedent after December 31, 1976.

Form 706 NA: United States Estate (and Generation-Skipping Transfer) Tax Return must be used to figure out the generation-skipping transfer tax (GSTT) liability for estates of non-residents of the United States. The generation-skipping tax is levied upon the transfer of the decedent’s estate rather than when it is received by a beneficiary.

A non-resident is someone who does not live in the United States and is not a citizen. The IRS has specific rules for how a person meets the criteria of a resident. Taxpayers are considered residents if they meet the green card test or if they fulfill the substantial presence test in the United States. Individuals who do not satisfy these requirements are considered non-residents.

U.S.-based assets that are considered part of an estate include things like:

- Real estate

- Physical personal property

- Securities of U.S. companies

- Debt obligations within the U.S.

- Bonds4

One important point to note is that any American-based stocks would be subject to U.S. estate taxes even if the certificates were physically stored outside of the country.

Important:

Although Form 706-NA: United States Estate (and Generation-Skipping Transfer) Tax Return must be filed within nine months following the person’s death, you may request a six-month deadline extension. This would allow the estate a total of 15 months to submit its tax return paperwork. Failure to file and remit payment on time may result in fines and penalties.

When To File Form 706NA

File Form 706-NA within 9 months after the date of death unless an extension of time to file was granted.

If you are unable to file Form 706-NA by the due date, use Form 4768, Application for Extension of Time To File a Return and/or Pay U.S. Estate (and Generation-Skipping Transfer) Taxes, to apply for an automatic 6-month extension of time to file. If you have already received a 6-month extension and are an executor who is out of the country, you may apply for an additional extension of time to file by filing a second Form 4768 and completing the form and attaching a written statement of explanation as instructed. For both extensions, check the “Form 706-NA” box in Part II of Form 4768.

US Estate Tax, the IRS & Form 706-NA

Form 706-NA: United States Estate (and Generation-Skipping Transfer) Tax Return is a tax form used to calculate tax liabilities for the estates with U.S.-based assets and generation-skipping transfers of non-resident decedents. Form 706-NA, which is distributed by the Internal Revenue Service (IRS), must be filed nine months after the death of the individual by their executor if the estate’s value exceeds the filing threshold of $60,000.

Determining the taxable estate

Gross estates of non-resident aliens with property located in the U.S., and valued at $60,000 or more, might be subject to estate tax. This is before taking into account any

“allowable deductions” or estate-tax treaties between the U.S. and the non-resident alien’s home country. The value of the decedent’s gross assets is determined at the date of the decedent’s death or, six months later, on the alternate valuation date.

Property located in the U.S., allowable deductions and credits

For real estate and tangible personal property, “located in the U.S.” is determined by physical presence in the U.S. (regardless of where the owner resides). If a non-resident alien buys stock in a U.S. corporation (e.g., General Electric), the stock is considered located in the U.S., regardless of where the stock certificates are held. Furthermore, any debt obligations that a U.S. citizen, corporation or governmental agency issues to a non-resident alien are treated as gross assets, which need to be included within the decedent’s gross estate.

From their gross assets, the decedent’s estate is entitled to deduct any and all “allowable deductions.” These include charitable contributions to U.S. charities designated as such by the IRC. The decedent’s estate also is entitled to certain expenses, losses, indebtedness or taxes incurred by the estate. These expenses must be prorated by the U.S.-share of the decedent’s worldwide estate. Assuming the decedent is not married to a U.S. resident, one deduction that is not allowed to a non-resident alien is the marital deduction, unless it meets the provisions of a Qualified Domestic Trust (Sec. 2056).

Non-resident aliens are entitled to a unified credit of $13,000, reduced by any lifetime gifts. Non-resident decedents whose gross assets are less than $60,000 upon their death may still have to file a Form 706-NA if they have used any part of the $13,000 unified credit during their lifetime.

Treaty versus non-treaty countries

When determining a non-resident decedent’s tax liability, the estate must take into account whether the decedent resided in a country governed by an estate-tax treaty with the U.S. If the non-resident alien is from a treaty-based country, he or she must attach a statement to Form 706-NA indicating the return was prepared based on a treaty with the U.S. (Reg. Sec. 301.6114-1). Non-treaty based estate tax returns (i.e., Form 706-NA) are governed by the estate-tax provisions for non-resident aliens in IRC § 2101-2108.

USA

When determining a non-resident decedent’s tax liability, the estate must take into account whether the decedent resided in a country governed by an estate-tax treaty with the U.S. If the non-resident alien is from a treaty-based country, he or she must attach a statement to Form 706-NA indicating the return was prepared based on a treaty with the U.S. (Reg. Sec. 301.6114-1). Non-treaty based estate tax returns (i.e., Form 706-NA) are governed by the estate-tax provisions for non-resident aliens in IRC § 2101-2108.

How to File Form 706-NA

Executors of estates that would be required to complete Form 706NA must file a tax return if the fair market value (FMV) of the “U.S.-situated assets, together with the gift tax specific exemption and the amount of adjusted taxable gifts, exceeds the filing threshold of $60,000.”6 In some cases, estates may still be required to file a tax return even if the estate value is less than that, namely if the deceased made large lifetime gifts of U.S. assets that took advantage of the unified credit exemption.

Several countries have death tax treaties with the United States, and executors reporting information on an estate from one of those countries may have to attach a statement stating that the death tax treaty is being applied.1

This form has been revised and updated numerous times since 1962. Form 706-NA is available to taxpayers by requesting Form 706: United States Estate (and Generation-Skipping Transfer) Tax Return.2 Citizens of U.S. possessions, such as the U.S. Virgin Islands, are not considered citizens in Form 706-NA.1

How To Complete Form 706-NA

Complete Form 706-NA in this order.

- Part I.

- Part III.

- Schedule A and B.

- Part II.

The estate tax is imposed on the decedent’s gross estate in the United States, reduced by allowable deductions. Figure the gross estate in the United States on Schedule A. Reduce the Schedule A total by the allowable deductions to derive the taxable estate on Schedule B, and figure the tax due using Part II. Tax Computation.

Download Form 706-NA

Here is the IRS link, which includes instructions as well as the downloadable Form 706-NA: United States Estate (and Generation-Skipping Transfer) Tax Return.

Private delivery services (PDSs)

You can use certain PDSs designated by the IRS to meet the “timely mailing as timely filing/paying” rule for tax returns and payments.

Where To File

File Form 706-NA at the following address.

Department of the Treasury

Internal Revenue Service Center

Kansas City, MO 64999

If using a PDS, use this address.

Internal Revenue Submission Processing Center

333 W. Pershing

Kansas City, MO 64108

Penalties

Section 6651 provides for penalties for both late filing of returns and late payment of tax unless there is reasonable cause for the delay. There are also penalties for willful attempts to evade or defeat payment of tax.

The law also provides for penalties for valuation understatements that cause an underpayment of tax. See sections 6662(g) and (h) for more details.

Reasonable-cause determinations

If you receive a notice about penalties after you file Form 706-NA, send an explanation, and we will determine if you meet reasonable-cause criteria. Do not attach an explanation when you file Form 706-NA. Explanations attached to the return at the time of filing will not be considered.

Return preparer

Estate tax return preparers who prepare any return or claim for refund that reflects an understatement of tax liability due to an unreasonable position are subject to a penalty equal to the greater of $1,000 or 50% of the income earned (or to be earned) for the preparation of each such return. Estate tax return preparers who prepare any return or claim for refund that reflects an understatement of tax liability due to willful or reckless conduct are subject to a penalty of $5,000 or 75% of the income earned (or income to be earned), whichever is greater, for the preparation of each such return. See section 6694(a) and 6694(b), the related regulations, and Announcement 2009-15, 2009-11 I.R.B. 687.

Death Tax Treaties

Death tax treaties are in effect with the following countries.

Australia | Ireland |

Austria | Italy |

Canada* | Japan |

Denmark | Netherlands |

Finland | South Africa |

France | Switzerland |

Germany | United Kingdom |

Greece |

*Article XXIX B of the United States–Canada Income Tax Treaty |

If you are reporting any items on this return based on the provisions of a death tax treaty or protocol, attach a statement to this return indicating that the return position is treaty based. See Regulations section 301.6114-1 for details.

What to do when the Form 706-NA is submitted

So once the Form 706 NA is submitted within 9 months of the passing, it takes a while to be processed. Sometimes 6 months or more.

We have had issues where the estate tax check is cashed by the IRS but the funds are posted to some sort of suspense account as opposed to being matched to the correct taxpayer account. We then need to contact the IRS international line on 267-941-1000 where we are given another number such as +18593203456. On this second number, callers are invited to leave a message on the voice mail as the mailbox is cleared daily. However, there are times when the mailbox is unavailable. So we need to send an email to the IRS to ensure that the check is matched to the correct return – sbse.eg.intl (at) irs.gov

If everything goes well, the IRS may issue a letter explaining that it was processed. Sometimes it may not send any letter so one would need to contact them accordingly. If they send a letter, they may issue a temporary tax ID to use when communicating with them

Then the next step is to contact the IRS to request a Transfer Certificate. Here’s the process for requesting the Transfer Certificate is as follows – https://www.irs.gov/businesses/small-businesses-self-employed/transfer-certificate-filing-requirements-for-the-estates-of-nonresidents-not-citizens-of-the-united-states

Estates and their authorized representatives may request an account transcript by filing Form 4506-T, Request for Transcript of Tax Return. Currently, Form 4506-T can be filed with IRS via mail or facsimile (per the instructions on the form). Although account transcripts for estate tax returns are not currently available through IRS’s online Transcript Delivery System (TDS), the IRS website, www.irs.gov, will have current information should an automated method become operational.

To allow time for processing the estate tax return, requests should be made no earlier than four months after filing the estate tax return.

The IRS says that estates and their authorized representatives who wish to continue to receive estate tax closing letters may call IRS at (866) 699-4083 to request an estate tax closing letter no earlier than four months after the filing of the estate tax return.

Instead of securing a closing letter to send with the request for a transfer certificate, it is now possible to send a transcript – https://www.irs.gov/businesses/small-businesses-self-employed/transcripts-in-lieu-of-estate-tax-closing-letters

So in summary, you need:

Key Takeaways

- Form 706-NA is used to calculate tax liabilities for estates of individuals with U.S.-based assets that are part of their estate who are not citizens.

- U.S.-based assets that would be considered part of an estate include things like real estate, physical personal property, and securities related to U.S. companies.

- Executors of estates that would be required to complete Form 706-NA must file a tax return if the fair market value of the estate was at least $60,000.1

- The form must be filed within nine months of the death of the individual.

- The generation-skipping tax is imposed when the decedent’s estate is transferred rather than upon receipt of the beneficiary.

An estate tax return (Form 706) must be filed if the gross estate of the decedent (who is a U.S. citizen or resident), increased by the decedent’s adjusted taxable gifts and specific gift tax exemption, is valued at more than the filing threshold for the year of the decedent’s death, as shown in the table below.

Filing Threshold for Year of Death

An estate tax return also must be filed if the estate elects to transfer any deceased spousal unused exclusion (DSUE) amount to a surviving spouse, regardless of the size of the gross estate or amount of adjusted taxable gifts. The election to transfer a DSUE amount to a surviving spouse is known as the portability election.

An estate tax return may need to be filed for a decedent who was a nonresident and not a U.S. citizen if the decedent had U.S.-situated assets.

In order to elect portability of the decedent’s unused exclusion amount (deceased spousal unused exclusion (DSUE) amount) for the benefit of the surviving spouse, the estate’s representative must file an estate tax return (Form 706) and the return must be filed timely. The due date of the estate tax return is nine months after the decedent’s date of death, however, the estate’s representative may request an extension of time to file the return for up to six months. An automatic six month extension of time to file the return is available to all estates, including those filing solely to elect portability, by filing Form 4768 on or before the due date of the estate tax return.

If the estate representative did not file an estate tax return within nine months after the decedent’s date of death, or within fifteen months of the decedent’s date of death (if a six-month extension of time for filing the estate tax return had been obtained), the availability of an extension of time to elect portability of the Deceased Spousal Unused Exclusion (DSUE) amount depends on whether the estate has a filing requirement, based on the filing threshold provided under § 6018(a).

If the filing threshold has been met, or in other words, if, independent of the portability election, the estate is required to file an estate tax return based on the total value of the gross estate and the amount of any adjusted taxable gifts, no extension of time to elect portability is available and Revenue Procedure 2022-32 does not apply.

However, if, the sum of the value of the decedent’s gross estate and the total amount of the decedent’s adjusted taxable gifts is less than the filing threshold, Revenue Procedure 2022-32 provides a simplified method for certain taxpayers to obtain an extension of time to make a “portability” election under § 2010(c)(5)(A) of the Internal Revenue Code. The simplified method under the revenue procedure to obtain an extension of time to make the portability election requires the filing of a complete and properly prepared estate tax return on or before the fifth annual anniversary of the decedent’s date of death and requires a notation on the estate tax return that the return is “FILED PURSUANT TO REV. PROC. 2022-32 TO ELECT PORTABILITY UNDER § 2010(c)(5)(A).” No user fee is required to use the simplified method under this revenue procedure. Estates that do not qualify for this relief, and do not have a filing requirement based on the filing threshold, may request an extension of time to make the portability election under § 2010(c)(5)(A) by requesting a letter ruling under the provisions of § 301.9100-3. The requirements for requesting a letter ruling are described in Revenue Procedure 2022-1 (or any successor revenue procedure).

Individuals taking advantage of the increased gift tax exclusion amount in effect from 2018 to 2025 will not be adversely impacted after 2025 when the exclusion amount is scheduled to drop to pre-2018 levels.

Final regulations establishing a new user fee of $67 for persons requesting the issuance of IRS Letter 627, Estate Tax Closing Letter (ETCL), became effective October 28, 2021 (User Fee for Estate Tax Closing Letter (TD 9957).

Yes. Notice 2017-12 explains that an account transcript issued by the Internal Revenue Service (IRS) can be used in lieu of Letter 627, Estate Tax Closing Letter. The Transcript Delivery Service (TDS), which provides authorized practitioners the ability to view and print instant account transcripts for estate tax returns, is now available on IRS.gov. In addition, hardcopy account transcripts are available to authorized taxpayers making valid requests via mail or facsimile using Form 4506-T, Request for Transcript of Tax Return.

There are two separate systems for making an electronic payment of estate or gift tax:

- The Electronic Federal Tax Payment System (EFTPS)

- Same-Day Wire Payment

Electronic Federal Tax Payment System (EFTPS)

Instructions on how to use the Electronic Federal Tax System (EFTPS) are found in Publication 4990 (do not use Publication 4990 for the same-day wire payment method).

What you need to know about EFTPS:

- To use EFTPS you must enroll and then wait for a Personal Identification Number (PIN) to arrive in the mail. Please consider that due to COVID-19-related office closures, delays in issuing PINs may occur.

- There is no fee to use EFTPS.

- Note that when using EFTPS you will not use the table of codes listed below.

- If you need assistance with using EFTPS contact EFTPS Tax Payment Customer Service at 800-555-4477 (Businesses) or 800-316-6541 (Individuals).

Same-Day Wire Payment

What you need to know about making a same day wire payment:

- You do not need to enroll to make a same-day wire payment, and no PIN is needed.

- Your financial institution may charge a fee for this service.

- The cutoff time to make a same-day wire payment is 5 p.m. Eastern Time. Your bank may have an earlier cutoff time.

- Download and complete page 1 of the Same-Day Taxpayer Worksheet, and provide pages 1 and 2 to your financial institution.

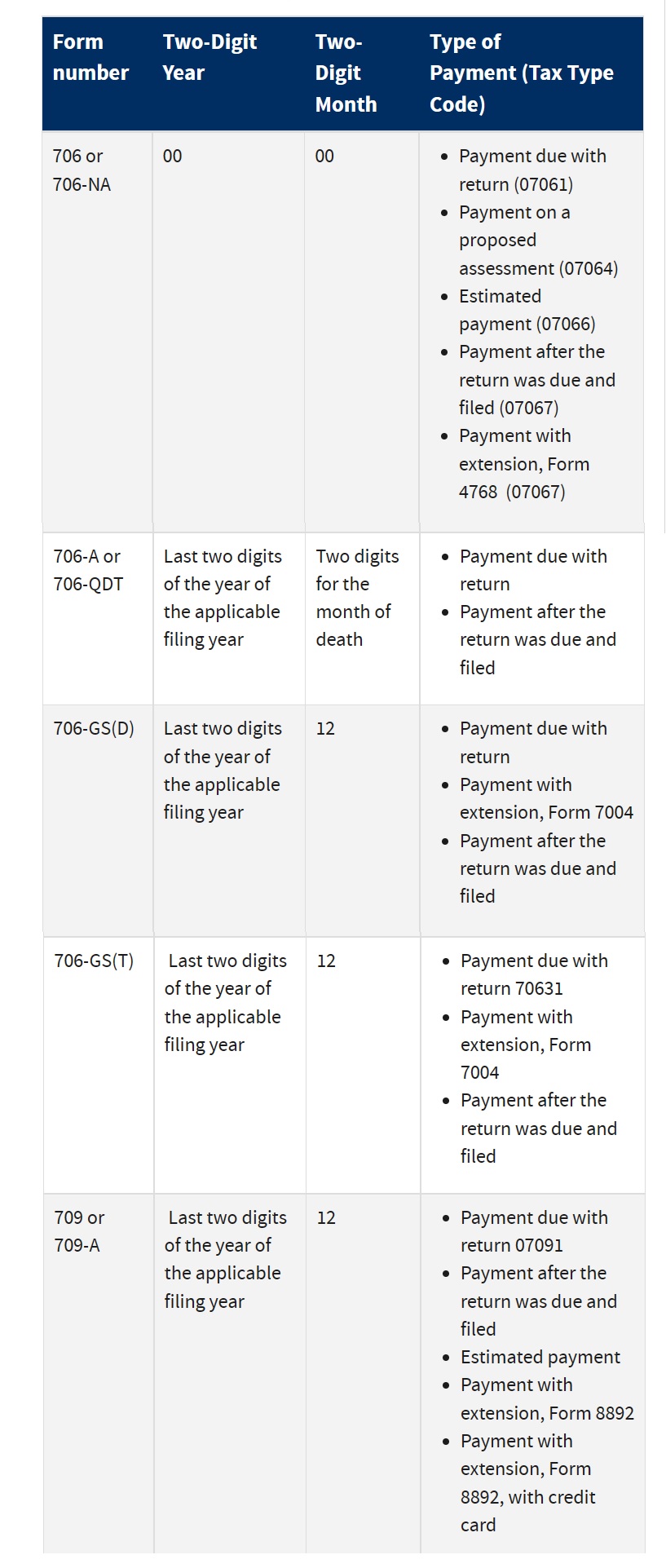

- When completing the Same-Day Taxpayer Worksheet, you will need a two-digit year, a two-digit month, and a five-digit tax type code, depending on the type of payment you are making (use the table of codes listed below).

The Gross Estate of the decedent consists of an accounting of everything you own or have certain interests in at the date of death (Refer to Form 706). The fair market value of these items is used, not necessarily what you paid for them or what their values were when you acquired them. The total of all of these items is your “Gross Estate.” The includible property may consist of cash and securities, real estate, insurance, trusts, annuities, business interests and other assets. Keep in mind that the Gross Estate will likely include non-probate as well as probate property.

Depending on how your 1/2 interest is held and treated under state law, and how it was acquired, you would probably only include 1/2 of its value in your gross estate. However, many other factors influence this answer, so you would need to visit with a tax or legal professional to make that determination.

Generally, the Gross Estate does not include property owned solely by the decedent’s spouse or other individuals. Lifetime gifts that are complete (no powers or other control over the gifts are retained) are not included in the Gross Estate (but taxable gifts are used in the computation of the estate tax). Life estates given to the decedent by others in which the decedent has no further control or power at the date of death are not included.

Marital Deduction: One of the primary deductions for married decedents is the Marital Deduction. All property that is included in the gross estate and passes to the surviving spouse is eligible for the marital deduction. The property must pass “outright.” In some cases, certain life estates also qualify for the marital deduction.

- Charitable Deduction: If the decedent leaves property to a qualifying charity, it is deductible from the gross estate.

- Mortgages and Debt.

- Administration expenses of the estate.

- Losses during estate administration.

In Schedule A of the return, list the estates U.S. assets, but show no values for those that are exempt from U.S. estate tax pursuant to a treaty. Attach a statement to the return that refers to the particular treaty applicable to the estate, and write that the estate is claiming its benefits. Entries for the gross estate in the U.S., the taxable estate, and the tax amounts, should be “0” if all of the decedents U.S. assets are exempt from U.S. estate tax pursuant to the applicable treaty. Attach to the Form 706-NA a copy of the return filed with the treaty partner. If no estate or inheritance tax return has been filed with the treaty partner, explain in your statement why no foreign return was due.

Most information for this page came from the Internal Revenue Code: Chapter 11–Estate Tax (generally Internal Revenue Code §2001 and following, related regulations and other sources.)