Skip to content

Skip to content

Crypto in the UK, Singapore, New Zealand and the BVI

By: Mikhail Charles

Pupil Barrister (England and Wales)

Barrister (British Virgin Islands, St. Kitts and Nevis, St. Vincent, St. Lucia, Grenada)

Summary:

An understanding of cryptoassets and their correct legal and tax treatment has become increasingly important to businesses and their advisers. This note reviews, from a lawyer’s point of view, the nature, use and proper legal and tax treatment of cryptoassets in the UK and wider Commonwealth.

Cryptoassets may be held or received by a business in the course of trade or held as investments, with profits, losses, gains, and income being subject to tax in accordance with the normal principles of UK taxation.

There are a number of types of cryptoassets. The writer will focus on exchange tokens (or cryptocurrencies; the terms are used interchangeably). This is partly because exchange tokens are the most prevalent and familiar form of cryptoasset (for example, Bitcoin) and have been the subject of judicial consideration both in the UK and abroad, e.g., in the British Virgin Islands (“BVI”).

In the absence of an internationally agreed definition of cryptoasset, the UK Cryptoassets Taskforce has defined cryptoassets as:

”cryptographically secured digital representations of value or contractual rights that use [that is, are built on] some type of distributed ledger technology and can be transferred, stored or traded electronically.”

Further, HMRC’s published guidance focuses on exchange tokens.

A more detailed understanding of the legal and regulatory position is set out at:

- The Cryptoassets Taskforce (consisting of HM Treasury, the Financial Conduct Authority and the Bank of England) joint report, which considers the impact and use of cryptoassets, and distributed ledger technology.

- The UK Jurisdiction Taskforce’s legal statement (UKJT statement). This examines the legal status of cryptoassets and is referred to in this note. The UKJT statement does not have binding status but has already been considered and followed by the English courts and BVI courts.

Here at HTJ Tax, we handle 6,7 and 8 figure individuals and companies who engage in the business of cryptoassets, and we can do no better than adopting Rees and Streisand (when we speak to our clients), they suggest that a deep dive on a particular cryptoasset investment being considered needs to be undertaken.

They propose that in evaluating an investment, investors need to consider among others the following questions:

(a) What is the problem the cryptoasset is addressing?;

(b) What is the proposed solution to the problem?;

(c) Who is on the management team?;

(d) How large is the market?;

(e) Are there any existing competitors?

(f) What is the business plan?;

(g) How will investors see a return on investments?

(h) How transparent is the management team?; and

(i) How likely is the product to achieve critical mass?

All these are certainly sensible questions in evaluating an investment into cryptoassets.

HTJ Tax is accustomed to being deployed pre-, post- and during investment into cryptoassets.

Given the absence of specific statutory provisions for the tax treatment of cryptoassets, the writer draws heavily on HMRC guidance, in the form of its Cryptoassets Manual. However, HMRC guidance should not be weighted as heavily as legislation.

Uncertainty abounds in the tax treatment of cryptoassets, and it is likely that the courts will need to address increasing numbers of these issues as the use of cryptoassets becomes more widespread.

Thoughts

- What are the likely consideration for resident non domiciled individuals who hold crypto assets outside of England and Wales?

The writer thinks that once the wallet containing the assets are held outside of the UK, then once that value is not remitted back to the UK in any way shape or form, then no domestic tax exposure ought to occur.

This is subject to change and in all the circumstances it is expected to change in ensuing tax years. As it stands, HMRC has no fixed position apart from that articulated in the earlier mentioned ‘Cryptoassets Manual’.

Where income tax and CGT are concerned, the position differs very significantly between those foreign domiciliaries who are using the remittance basis and those who are not. The remittance basis is a special basis of taxation which is available to any UK resident foreign domiciliary who is not deemed domiciled in the UK, although use of this regime is elective for such individuals, rather than mandatory.

The essence of the remittance basis regime is that, although UK source income and UK gains are immediately taxable, non-UK source income and non-UK gains are taxed only if remitted to the UK. ‘Remitted to the UK’ means, essentially, ‘brought into the UK’. There is an elaborate code to determine whether foreign income or gains have been remitted to the UK, and the rules are not always intuitive.

Whether a foreign domiciliary is deemed domiciled or not is also of great importance for the IHT position. For an individual who is not deemed domiciled, the basic principle is that there is only exposure to IHT insofar as his assets are situated in the UK. With one qualification, which is discussed below, there is no exposure to IHT by reference to non-UK assets; such assets are effectively disregarded.

Once an individual has become deemed domiciled the remittance basis cannot be used. It follows that insofar as income and gains from personally held assets are concerned, a deemed domiciled individual is on the same footing as a UK domiciliary. In other words, the individual is immediately taxable on any income, whether the source is outside the UK or within it, and is immediately taxable on any gains, whether realised on the disposal of UK or non-UK assets.

The acquisition of a deemed domicile also has a serious impact on exposure to IHT. Once an individual is deemed domiciled, there is exposure to IHT on his personally held assets regardless of their situs. The only qualification here is that, in some situations, a double taxation treaty may limit the scope of IHT to assets situated in the UK

- Can a qualifying irrevocable foreign trust provide a planning opportunity in the UK / US?

Yes. The writer thinks that there is some scope for a trust to be used to hold crypto offshore and take some benefit (limited as it be may very well be).

US: Grantor trust status also applies to a trust from which, at all times by the terms of the trust, no person can benefit during the non-US settlor’s life other than the settlor and/or his spouse. These irrevocable trusts do offer an opportunity for current, tax-free distributions to the settlor and/or his wife. The settlor in particular may then make tax-free gifts to his US beneficiary family members. This type of trust is especially effective when structured as a completed gift trust as it will also avoid US transfer taxes and can directly acquire for value US estate sited property.

UK: It is usual for persons who are resident but neither domiciled nor deemed domiciled in the UK to consider settling their non-UK assets upon an Excluded Property Trust prior to becoming deemed domiciled in the UK. If the trust is to be established for the benefit of the settlor’s children or grandchildren and the settlor himself (and his spouse or civil partner) is excluded from benefiting, it may be possible to structure the accounts within the trust to ensure that income (if it is not taxed to the settlor) is segregated from capital for UK tax purposes. It may then be possible to ensure that income which is not properly defrayed to meet income expenses is distributed to beneficiaries who have lower tax rates. If income is retained within the trust, capital distributions or other benefits to a UK resident beneficiary will be treated as first made out of the retained income and the value of the distribution or other benefit will give rise to an income tax charge in the beneficiary’s hands. If the distribution is to a minor and unmarried child of the settlor, the income will be treated as that of the settlor and taxed in the settlor’s hands.

For both jurisdictions the key point is for clear and cogent advice to be taken in respect of the capital gains tax exposure, especially for the UK as this may erode any potential gains or savings to be made holding crypto, which is at best a volatile asset.

- When crypto is invested or traded using a company, there’s an opportunity to reduce taxable income with expenses that are wholly and exclusively attributable to the activity? Is there?

In the writer’s view yes, there may be an opportunity to reduce taxable income. You would recall that a business may buy and sell exchange tokens as part of its trade.

It may also supply goods or services and accept exchange tokens as payment, in the course of its trading activities, in which case the receipt of the tokens is a receipt in the course of trade and subject to income tax or corporation tax as such.

The question in that case is the computation of profits and the value of the receipt. The value of any profit or gain (or loss) will need to be converted into pounds sterling for the purposes of filling in a tax return.

Any profit or gain must be calculated by converting to pounds sterling using the appropriate rate at the time of each transaction. HMRC expects valuations to be carried out using a consistent methodology and for a record of the methodology to be retained with tax records (see Cryptoassets Manual, paragraph CRYPTO40100, section 28A, Income Tax (Trading and Other Income) Act 2005 (ITTOIA 2005) and section 49A, Corporation Tax Act 2009 (CTA 2009)).

This may be easier to achieve if an exchange token is traded on an exchange.

A tax liability may be triggered if cryptoassets are treated as held as part of a trade (as stock) and, for accounting purposes, are appropriated to fixed assets (or vice versa) (section 161, Taxation of Chargeable Gains Act 1992 (TCGA 1992)).

HMRC will only consider an individual to be trading in exceptional circumstances, having regard to the “frequency, level of organisation and sophistication” of the activity. (see Cryptoassets Manual, paragraph CRYPTO20250.)

The amount of tax a business must pay will therefore depend on its income, expenditure, profits and gains. These must be declared annually to HMRC.

HMRC will consider each case on the basis of its own facts and circumstances. It will apply the relevant legislation and case law to determine the correct tax treatment (including where relevant, the contractual terms regulating the exchange tokens).

- On the day of a fork, does an owner of the original asset recognize income for the new asset? What if there is no market for the new asset because, say, digital wallets do not support it? And at what value should the adjusted basis be calculated? If it’s the fair market value, at what date: that of the fork or the date on which it can be transacted? I know there has been push back from taxpayers against HMRC – what’s the latest?

Cryptoassets may be controlled by consensus within a community. Any differences of opinion within the community may lead to a soft or hard fork. Both are brought about by a change to the coding and protocols of the cryptocurrency. A soft fork is a change to the terms of the cryptoassets that affects all tokens. A hard fork may result in a new type or types of token. For example, a person holds 500 A tokens. After the fork, they hold 500 A tokens and 500 B tokens.

A hard fork is a more radical change to the protocol governing the cryptoassets. In addition to it resulting in new types of token coming into existence, it may results in a second branch of the distributed ledger (and therefore a new type of cryptoasset) being created. Bitcoin, for example, has gone through several hard forks. One change, to Bitcoin XT, was to allow 24 transactions per second, as opposed to seven. Ethereum hard-forked to reverse the effect of a hack.

HMRC views forks as falling within the rules for assets derived from other assets (section 43, TCGA 1992) (as opposed to section 22, TCGA 1992).

After the fork, the new cryptoassets and the old cryptoassets each go into separate pools. Any allowable costs relating to the original cryptoassets are split between the pools for the original and new assets on a just and reasonable basis (section 52(4), TCGA 1992).

In some cases, an exchange will not recognise the cryptoassets created after a fork. HMRC says that it will consider such cases on their merits. It is possible that in such cases it becomes impossible to use the original or new cryptoassets and this may impact the value of the new or original cryptoasset, potentially rendering it of negligible value

- In order to tap into the value generated by cryptoassets, HMRC’s approach has been to treat cryptoassets as property in relation to IHT and as “assets” in relation to other taxes. This approach is potentially quite unclear for taxpayers if we consider that, there is no legislative basis (judicial or statutory) for the classification of cryptoassets as property. The fact that HMRC has recognized cryptoassets as property only in relation to IHT, and not for other UK taxes, adds to the uncertainty. This must have been challenged or in the process of being challenged. What is being said?

The writer acknowledges that there is a lack of publicly reported data in respect of current and ongoing tax challenges to the overall classification of, on one hand cryptoassets and on the other hand specific taxes applicable to specific crypto assets.

The current position seems to be one of ‘substance’ meaning the HMRC will look at how any transaction in or involving cryptoassets is treated.

So, on general principles: in particular, the substance of the transaction (what is actually happening), the nature of the cryptoasset in question and how existing general tax laws apply.

How the cryptoasset is labelled is not determinative of the tax treatment.

The status of the taxpayer determines which tax is in point. For example, an individual who is resident in the UK for tax purposes is subject to income tax and CGT, and a company that is resident in the UK for tax purposes, or a company trading in the UK through a branch or agency, is subject to corporation tax

No reported cases are to hand at the date of this Note.

- What is the UK tax treatment of:

- Options on tokens – will this mirror the taxation of options over shares?

Unlikely in the view of the writer, especially as HMRC does not have any guidance in respect of this.

What appears to be the current position is that for transfers of exchange tokens to fall within the scope of stamp duty or SDRT, they would need to meet the definition of ‘stock or marketable securities’ or ‘chargeable securities’, as defined for the purposes of those taxes. References: CRYPTO24000, CRYPTO44100

Where UK shares or certain other categories of asset (including some types of securities and some partnership interests) are sold for cash, there would, subject to any applicable relief or exemption, be a charge to stamp duty or SDRT. The question arises as to what happens if the consideration is not cash, but cryptoassets.

HMRC summarises the position as follows: ‘for stamp duty, chargeable consideration is “money”, “stock or marketable securities” or “debt”. For SDRT it is defined as “money or money’s worth”’.

References:

CRYPTO24000, CRYPTO44150

HMRC considers that exchange tokens (and, one would think, by extension, all cryptoassets) ‘would count as ‘money’s worth’ and so be chargeable for SDRT purposes. Tax will be due based on the pound sterling value of the exchange tokens at the relevant date’.

References:

CRYPTO24000, CRYPTO44150

As for stamp duty, ‘HMRC does not consider exchange tokens to be currency or money, so they do not meet the definition of ‘money’ for stamp duty consideration purposes. They will also generally not count as ‘stock or marketable securities.’

References:

CRYPTO24000, CRYPTO44150

The position with security tokens is less clear, as a security token may, depending on its precise characteristics, constitute ‘stock or marketable securities’ for these purposes.

As regards whether cryptoassets constitute ‘debt’ for these purposes, HMRC’s position is that ‘broadly, ‘debt’ counts as chargeable consideration for stamp duty in the following scenarios:

References:

CRYPTO24000, CRYPTO44150

- release of a debt—the seller has an outstanding debt to the purchaser (which could be in the form of exchange tokens). The seller transfers shares to the purchaser, and in consideration the purchaser releases the seller from the debt

- debt is assumed a third party has an outstanding debt to the purchaser (which could be in the form of exchange tokens). The seller transfers shares to the purchaser, and in consideration the seller is assigned the right to the debt from the third party.’

HMRC’s reasoning here is a little hard to follow (besides the fact that the second bullet appears to confuse an assumption of debt with an assignment of debt).

A transfer will only attract stamp duty if there is chargeable consideration. If shares (say) are sold in return for exchange tokens, and if those tokens are neither money, nor stock or marketable securities, then there will only be chargeable consideration if there is a release or assumption of debt.

In a straightforward sale of shares for exchange tokens, with no pre-existing debt involved, there would not appear to be a release or assumption of debt. If no stamp duty is chargeable on the relevant stock transfer form, there would also generally be no liability to SDRT.

It is therefore perhaps not surprising that HMRC does not elaborate on its analysis. It may be that if taxpayers were to try to argue that a sale of shares in exchange for cryptoassets does not attract stamp duty or SDRT, there would be likely to be evidence that the parties priced the transaction in money (e.g., sterling).

As a result, a court may be willing to analyse the consideration for the transfer as being, in reality, a sterling amount which was satisfied by a transfer of cryptoassets. In this case the transfer would attract stamp duty on the money consideration agreed between the parties.

- ICOs – will these be taxed in the same way as IPOs?

In a word No!

An ICO is often described (not entirely accurately) as a digital initial public offering (IPO), where instead of shares, tokens are issued. However, unlike shares, tokens do not generally represent an equity stake in the project that is the subject of the ICO or yield dividends. The characteristics of tokens vary from ICO to ICO. They may themselves be a new cryptocurrency, or they may give rights such as the right to:

- share in any future profits from the project;

- vote on specified matters affecting the project; or

- purchase goods or services within the environment created under the project.

The answer depends on the precise nature of the tokens he is acquiring.

There is a wide variety in the terms of an ICO and in the rights attaching to tokens which are issued. It is very common for the total supply of a token to be fixed from the outset. This harks back to one of the fundamental tenets of many cryptocurrencies which specifically reject the idea that, like fiat currency, the value of the cryptocurrencies can be manipulated by controlling their supply.

The total number of tokens generated as part of an ICO is typically a round, arbitrary number. This is hardwired into the smart contract by which they are created and cannot be subsequently changed. The creation of the entire supply of a token at the commencement of a project is known as the ‘pre-mine’.

The share of a pre-mine which is not allocated to the promoters or sold to the ICO participants is generally retained by the token-issuing entity to fund ongoing expenditure such as development, legal and marketing expenses. This supplements the proceeds from the subsequent sale of cryptocurrencies contributed as part of the ICO. In some cases where an ICO does not reach its hard cap, unsold tokens in excess of the tokens retained by the token issuing entity are burnt. This creates a permanent difference in the fixed and maximum circulating supply.

The taxation of their share of a pre-mine is perhaps one of the most significant tax issues faced by the promoters of an ICO. In the context of a traditional equity-based fundraising, the analytical pathway is usually set by specific employee share and option rules. These rules generally seek to align the point of derivation of these shares or options for tax purposes with the time that these interests become fully vested. This avoids a situation where an employee receives a tax bill for a valuable block of shares or options which they are unable to convert into cash.

In the absence of specific rules, the taxation of the promoter’s allocation of a pre-mine is left to be determined by general principles. The starting point is therefore that the value of the tokens forms part of the taxable income of a promotor at the time they are derived. If these tokens are issued outright to a promoter, then this point of derivation is clear. The more complicated question in this otherwise straightforward scenario is the value of these tokens on that day. The proximity of the date of grant of these tokens to the date of the ICO itself is likely to be highly relevant. It stands to reason that the value of tokens issued to a promoter the day before a public ICO, which has a set issue price and a long whitelist, should be higher than the value of tokens issued at the very early concept stage of a project which may not even materialise into a whitepaper.

The next consideration which is highly relevant is the vesting or escrow conditions which are imposed on the promoter’s allocation of a pre-mine. Depending on the mechanism used and the applicable rules of the jurisdiction in which the promoter may be resident, these conditions may be successful in deferring the point of derivation both economically and for tax purposes. This is more likely the answer than in relation to clawbacks and bad leaver provisions which may be used to take back tokens in limited circumstances. If the point of derivation of a pre-mine allocation is successfully deferred until after the ICO, the token will be more likely to have become tradeable. It will therefore have an objectively determinable market price which will be its average value on cryptocurrency exchanges or at which it may be swapped on a peer-to-peer basis. There is therefore no room to argue for a discount in the value of tokens based on the remoteness of the project launch.

- The transfer of tokenized shares – will these fall within the scope of stamp duty?

Stamp duty is charged on instruments that transfer stocks or marketable securities, and interests in partnerships (Schedule 13, Finance Act 1999). Stamp duty reserve tax (SDRT) is charged on agreements to transfer chargeable securities (section 99(3), Finance Act 1986).

HMRC’s view is that existing exchange tokens are not likely to meet the definition of stock or marketable securities or chargeable securities (see Cryptoassets Manual, paragraph CRYPTO24000).

HMRC does not consider other forms of token, but it is possible that some (particularly security tokens) may fall within the definition.

Where stock, securities or shares are sold for consideration consisting of tokens, this would be “money or money’s worth”, and SDRT would be due on the sterling value of the tokens on the date that the charge arose.

HMRC take the view that exchange tokens are not typically chargeable consideration for stamp duty purposes unless they are treated as debt. This distinction with the SDRT position (where exchange tokens are treated as consideration for SDRT purposes) may lead to difficulties where shares are sold intra-group for consideration consisting of tokens. In the absence of chargeable consideration for stamp duty purposes, stamp duty group relief may not be available. Accordingly, it may not be possible to “frank” the SDRT charge (see Cryptoassets Manual, paragraph CRYPTO44150).

Case Law Roundup 2021

The question of whether cryptocurrency (Bitcoin, in this case) was a chose in action (and, therefore, property) was considered by the High Court in AA v Persons Unknown [2019] EWHC 3556 (Comm).

The court considered whether Bitcoin was property and could, therefore, be the subject of a proprietory injunction. Referring to the reasoning set out in the UKJT statement, Bryan J adopted the analysis in the UKJT statement, and concluded that cryptoassets like Bitcoin are property (see paragraphs 57 to 59 of the judgment). Bryan J went on to say that cryptocurrencies meet the four criteria set out in Lord Wilberforce’s definition of property in National Provincial Bank v Ainsworth [1965] 1 AC 1175as being definable, identifiable by third parties, capable in their nature of assumption by third parties, and having some degree of permanence.

Similarly in Robertson v Persons Unknown (unreported – July 2019) the English Court considered the concept of bitcoin as property in an application for an injunction. In order to grant relief, the Court had to effectively recognise the cryptocurrency as something capable of being owned and it followed the lead of other jurisdictions in recognising that bitcoin could constitute personal property and therefore be subject to the relief sought.

One of the main ways fraud victims can seek protection is by obtaining freezing orders and other injunctive relief and so it was important for a cryptocurrency to be recognised in this context. The Court granted an asset preservation order to freeze bitcoin which had been spear phished away by a fraudster and a Bankers Trust order requiring the cryptocurrency exchange, Coinbase, to reveal the identity of the fraudster.

Also, in Toma V Murray [2020] EWHC 2295 (Ch) the court developed its thinking even further and recognised the unique characteristics of cryptocurrency and their volatility and potential to quickly change in value. The court decided that an injunction restraining dealing with bitcoin without consent was unworkable as any delay incurred in obtaining consent could result in significant drops in value. The significance of this is that the courts are developing an ever-sophisticated practice and knowledge base and recognising the practical considerations of dealing with cryptocurrencies. It should be noted however, especially with fraud cases that jurisdictional issues will need careful handling, including determining where the damage has been suffered.

In Ion Science Ltd v Persons Unknown (unreported, 21 December 2020) – , the court considered the lex situs of cryptoassets and stated that it is the place where the person or company who owns it is domiciled.

Let’s accept Crypto is an investment, where is it sited?

- Why is it important?

- RNDs – resident but not domiciled individuals

- NDs (IHT) – non-UK domiciled individuals

- Trusts

- HMRC say …… the UK

Situs

- Situs of is usually governed by Section 275A TCGA

- The situs is only in the UK if governed by a UK law

- If not subject to a UK law the asset is not UK-sited

- But HMRC say… the Private Key is the key

The Private Key is the key

- HRMC say crypto is sited where the owner is resident if they hold, or could obtain, the Private Key

- What about…….

- the law that governs the contract

- courts that have jurisdiction

- enforceability

- recoverability

- location of physical assets (stablecoins)

- the place where ownership is recorded or registered

- Ion Science Limited v Persons Unknown (2020) – where the owner is domiciled (not where the owner is resident) – an outlier

The UK Legislation

- If crypto is an ‘investment’ is it property?

- If crypto is ‘property’ is it an ‘asset’? *

- If crypto is an ‘asset’ is it an ‘intangible asset’?

- If crypto is an ‘intangible asset’ its situs is governed by Sections 275 & 275A

TCGA

- Therefore crypto can only be UK-sited if governed by a UK law

- If not governed by a UK law then it cannot be UK-sited

* Crypto must be ‘property’ to be liable to CGT on disposal. ‘Property’ is something which can be owned. Kirby v Thorn EMI 1987

- ‘Property’ is an asset that is definable, identifiable by 3rd parties, capable of being transferred to 3rd parties, permanent and stable. National Provincial Bank v Ainsworth1965

HMRC say…….

- Crypto is also ‘fungible’, like So the ‘pooling’ rules of Section 104

TCGA apply [30 day and Same Day rules]

- Tax is usually 20%

- Better than trading – 47% maximum income tax + NIC

Not as good as currency or gambling

Finally as at the date of this note (in England and Wales), Wang v Derby [2021] EWHC 3054 (Comm), it was common ground between the parties that the “entirely fungible character and non-identifiable status” of cryptocurrency did not prevent it from being the subject matter of a trust

In Singapore (more un US tax Singapore here) the legal status of cryptocurrency (to date, Bitcoin and Ethereum) as property has also been considered in the courts in Singapore (B2C2 Ltd v Quoine PTC Ltd [2019] SGHC (I) 03 [142]) where the courts concluded that cryptocurrency could be treated as property.

The defendant, Quoine, was a currency exchange platform. A series of overnight trades were executed by an electronic trading algorithm operated by Quoine. These trades resulted in a contract between computers (with no human intervention) at a price approximately 250 times the then going market rate, producing a windfall for the claimant, B2C2, of about US$30m. The following day, Quoine purported to reverse the contract on the grounds of mistake. B2C2 sued for breach of contract and/or breach of trust.

The Singapore Court of Appeal upheld the decision with regard to breach of contract, but held that no trust could have arisen “even assuming that the BTC could be the subject of a trust” because there was no certainty of intention to create a trust.

In New Zealand, in Ruscoe & Moore v Cryptopia Limited (in liquidation) [2020] NZHC 728, in the High Court of New Zealand. Cryptopia was a cryptocurrency exchange whose servers were hacked; cryptocurrencies of various denominations were stolen, valued at around NZ$30m.

Shortly afterwards, Cryptopia went into voluntary liquidation, whereupon the liquidators sought the directions of the court as to (inter alia) the legal status of the digital assets still held by them. In particular, they asked whether the various cryptocurrencies constituted “property” as defined in s 2 of the Companies Act 1993 (CA); and whether any or all of them were held on trust for the account holders.

The judge concluded that all of the various cryptocurrencies under consideration were “property” within the definition outlined in s 2 of the CA “and also probably more generally” – adding that they were also capable of forming the subject matter of a trust.

In the BVI; Philip Smith v Torque Group Holdings Limited et al BVIHC (COM) 0031: the BVI commercial court had to determine how cryptoassets should be characterised under BVI law. It also had to consider how such assets should be treated by a liquidator in an insolvent winding up.

Torque ran a Singaporean run cryptocurrency trading platform offering various crypto-related services. The majority of Torque’s cryptoassets were held in a wallet provided by Binance, an exchange located in Cayman (referred to in the judgment as the “Tran account”). Many customers had “user trading wallets” that allowed “access” to these assets by placing orders on Torque’s customer webpage/application. Other customers had “personal user wallets”, which were wallets provided by Torque but which contained just the customers’ own cryptoassets and which they could deal with directly.

Justice Wallbank, in following decisions from numerous other courts in Commonwealth jurisdictions, held that cryptoassets should be treated as its “assets or ‘property”. Just as the English Court had in the case of AA v Persons Unknown, the BVI Commercial Court relied on the guidance given by the UK Jurisdiction Taskforce in a Legal Statement on Cryptoassets and Smart Contracts which stated that cryptoassets are to be treated as “property” at common law and for the purposes of the English Insolvency Act.

The UKJT Statement – The Legal Statement has an explicitly commercial purpose. It anticipates the day when “investment grade” cryptoassets will be commonplace.

However, the statement identifies some issues, for example, adopting a strictly literal interpretation of Colonial Bank would be unduly rigid and doing so would not be in keeping with the flexibility of the English common law when dealing with novel issues. The problem with crypto assets is that they derive their status from the consensual cooperation and participation of the community of users who administer and deal in them.

Yet, in a wide range of international commercial activities English law is the most widely chosen governing law in the word, and it is nothing if not rooted in, and accommodating of, the changing realities of commercial enterprise. So, it is not surprising that English law should want to get ahead of the game. But it is the manner in which this has been attempted that is genuinely novel. The Legal Statement is not a piece of legislation nor a binding judicial decision. It is essentially a high-level legal opinion which, has been welcomed by the common law world.

Yonder lies tax!

In many ways, ‘investment’ will be the default position for someone buying and selling crypto as per Salt v Chamberlain [1979] STC 750. This presumption might be rebutted where the activities are so organised that they can be classed as a venture in the nature of trade.

Of course, where one’s activities are considered as investment then any profits or losses on disposals will fall within the capital gains regime.

HMRC’s internal Cryptoassets Manual (Manual) now also makes it clear that Capital Gains Tax is likely to apply:

“In the vast majority of cases, individuals hold cryptoassets as a personal investment, usually for capital appreciation or to make particular purchases. They will be liable to pay Capital Gains Tax when they dispose of their cryptoassets.”

Crypto is plainly an “asset” for the purposes of s 1 of the Capital Gains Tax Act 1979 in the UK.

The Manual also states that individuals will be liable to pay Income Tax and National Insurance contributions on cryptoassets that they receive from their employers (as a form of non-cash payment) or from “mining, transaction confirmation or airdrops”.

The Manual says nothing, however, about the payment of Income Tax on interest on cryptocurrency holdings. This may be because bitcoin does not generate any income, but it is notable that it is possible to earn interest on other forms of cryptocurrency, such as, for example, Ethereum. It is unlikely that this apparent lacuna will enable trusts to earn investment income free of tax, but trustees and other institutional investors will have to consider how such income is to be reported.

The Manual can be critiqued however, when one looks at the attempt of definition it tries. It identifies four different types of cryptoassets, which work in different ways: Exchange Tokens (of which bitcoin is an example); Utility Tokens (which give access to particular goods or services on a platform); Security Tokens (which provide particular rights or interests in a business); and Stablecoins (cryptoassets that are pegged to some other asset such as gold or a government-backed currency).

Overall, the residence and domicile of the UK tax is currently being determined on the basis of physical residence, but this is an uncertain position not derived from any ‘black letter’ legal basis. One may decide to use offshore structures to handle crypto to eliminate said uncertainties.

The writer believes that where the income is from crypto non-trading activities then it will be subject to tax as miscellaneous income. In respect of expenses, the starting point would be to follow the rules for trading expenses.

However, there won’t be any entitlement to capital allowances, in my view.

Where there is a trade then any profits arising to an unincorporated business would be subject to income tax.

Where activities were run through a company then profits would be subject to corporation tax.

The business should be able to deduct its revenue expenses. For example, what are likely to be high energy costs can be deducted from profits along with rent and staff costs. It is likely that one will be able to claim capital allowances on capital expenditure such as the mining rigs and other computer equipment used within the mining operation.

Readers should beware of the HMRC, in relation to cryptocurrency, the department is using its extensive information gathering powers to obtain details of cryptocurrency holders from various exchanges.

For example, Coinbase has confirmed that it provided details of all UK resident taxpayers who, in 2019/20, entered into cryptocurrency transactions worth more than £5,000.

HMRC’s cryptocurrency nudge letters target those who may need to pay tax on profits or gains made from disposals of cryptocurrencies. As we have outlined the tax treatment of cryptoassets is complicated and not straightforward.

While the writer hopes that you realisize sizeable gains in the current tax year, do not overlook fundamentals, such as when a gain might be realised, for example, when switching from one cryptoasset to another and be very careful in considering the residence and domicile of non-UK based crypto assets and whether any withdrawals are made.

Now, in HMRC’s view, asset-linked cryptoassets are situated where the asset they represent is located. For example, if a gold bar is held in a vault in Ruritania, then the token is a Ruritanian asset irrespective of the token holder’s location.

Yet for non-asset-linked cryptoassets, HMRC acknowledges that there are currently no statutory provisions for the taxation of cryptocurrencies and it will therefore treat the cryptoasset as being situated where the beneficial owner of that cryptoasset is resident.

HMRC claims that this provides a clear and objective rule which can be easily applied (see HMRC’s Cryptoassets Manual at CRYPTO22600).

HMRC’s position is, however, problematic, as the means by which a crypto asset is held e.g., in hot or cold wallets etc. varies wildly. Under HMRC’s recently updated manual concerning the tax treatment of cryptoassets, remittance basis taxpayers may cause a remittance by simply carrying a cold wallet back to the UK from abroad. Uncertainty abounds!

Worked Example

- If the investment has made a profit of over £12.3k you may be liable for tax in the UK.

If the crypto profit exceeds the capital gains tax allowance you will have to pay tax at the following rates:

| Tax rate | Taxable income |

| 10% | Basic Rate Income Band (up to £50,270) |

| 20% | Higher Rate Income Band (up to £150,000) |

| 20% | Additional Rate Income Band (more than £150,000) |

So, as you can see, you’ll pay either 10% or 20% tax on any crypto gains, depending on what your regular income is. If you earned less than £50,270 in 2021 – you’ll pay 10% on crypto gains. If you earned more than £50,279 in 2021 – you’ll pay 20% on crypto gains.

Over Yonder!

In its consultation paper dated July 2021, HM Treasury has stated that the time is now for the UK to begin planning for the implementation of the FATF recommendation on extending the scope of the Travel Rule so that transfers of cryptoassets are accompanied with identifiable information on the originator and the beneficiary of each transfer.

This is intended to apply to: (i) cryptoasset exchange providers (including cryptoasset ATMs, peer to peer providers, issuers of new cryptoassets); and (ii) custodian wallet providers (which includes safeguarding and administering cryptoassets and/or the private cryptographic keys on behalf of customers), that are carrying on business in the UK (together, “Cryptoasset Service Providers”).

In the UK, the proposed approach is to replicate the requirements under the UK Wire Transfer Regulation for the cryptoasset sector, insofar as is possible. However, HM Treasury notes that it would not be appropriate to simply extend the regime in the UK Wire Transfer Regulation, and so it proposed to modify the Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (MLR 2017).

At its core, Cryptoasset Service Providers will need to implement effective systems for providing certain information on the originator and beneficiary as part of transfer of cryptoassets and detecting whether the requisite information on the originator and beneficiary is missing.

Conclusion

The writer expects increased litigation and a potential expansion on the UKJT Legal Statement in common law countries around the world as the penetration and reliance on crypto currency intensifies.

Detailed and specific tax advice needs to be taken from the outset or when there is an increase in value of cryptoassets.

Mikhail Charles

Sources:

- Taxation of cryptoassets by Practical Law Tax

The contents of this presentation do not constitute legal advice and should not be relied upon as a substitute for legal counsel.

How did we get here?

• Silk Road

• Early adopters

• The crypto-winds have changed

• Great variety of projects

• Greater sophistication in the market

Part 1A: Government approach

The approach of Governments

• Most Governments caught napping around the world

• HMRC relatively quickly produced guidance in 2014 – however, limited and unhelpful in

many areas

• Further policy / guidance issued over next 7 years

HMRC’s guidance has evolved

• Original guidance 2014

• Policy papers:

– 2018

– 2019

• HMRC Cryptoassets Manuals published 2021

Original guidance

• Main target – use of BTC for criminal purposes (eg laundering illicit funds)

• Primary aim appears was not to develop a specific tax framework

• Included some poor messages including that transactions could be “so highly speculative

that it is not taxable or any losses available”

Cryptoasset Manual

• Thorough

• Some gaps – which will always be the case in such an evolving area

• Some ‘interesting’ interpretations

Part 1b: Buying, selling and holding ‘fungible’ tokens

Contents

• What is a fungible token?

• Are the activities of an investment nature?

• CGT treatment

• Non-CGT treatment

What is a fungible token?

• An unusual and ungainly term

• “being something (such as money or a commodity) of such a nature that one part or quantity may be replaced by another equal part or quantity in paying a debt or settling an account”

• Little in life is fungible

• Financial world – often used to make life easier

Are the activities of an investment nature?

• Default position…

• …but a rebuttal presumption (Salt v Chamberlain)

• HMRC agrees at CRYPTO200050

• So what?

– Where investment applies – subject to CGT regime

– Lower rates of tax

– Annual Exemption applies

Further CGT questions, issues and implications

- Is crypto treated as a foreign currency?

- What is a disposal?

- Pooling of coins / tokens

- Allowable costs

- Airdrops

- Capital losses

- Lost wallets, rug-pulls and scams

- Residence and domicile

What is a disposal?

• Not as profound as might appear!

• Exchange crypto for cash (Fiat)

• Exchange crypto for crypto

• Sending gift of crypto to another’s wallet

• Using crypto to purchase goods or services

What’s not a disposal?

- Exchanging cash for

crypto - Transfer crypto

from one wallet to

another (with same

beneficial owner) - Contribution to

partnership wallet?

Foreign currency?

• Adopted as legal tender in El Salvador… but the exception!!!

• Not considered as currency by vast majority of major economies

• Bank of England / European Central Bank etc

• As such, gains and losses not treated as gains / losses on foreign currency

• Again, perhaps contrary to 2014 guidance from HMR

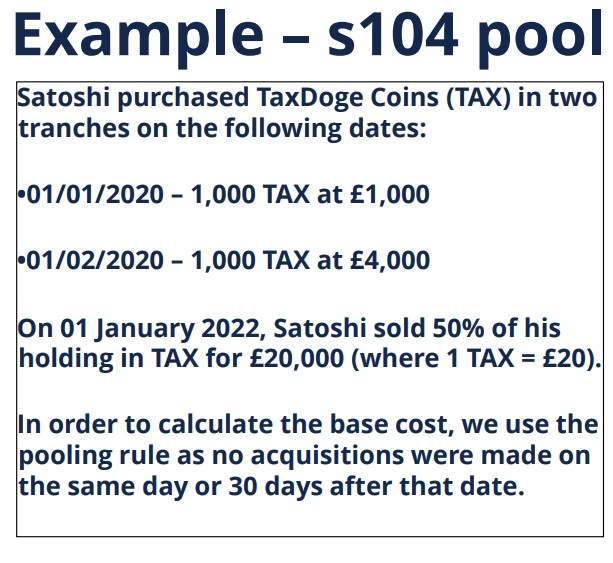

Pooling – general rule

• Individual tokens / coins will be placed in separate pools as ‘fungible’ assets

• See TCGA 1992, s104 (although entitled “shares and securities – clear applies to all

‘fungible’ assets)

• Example 1

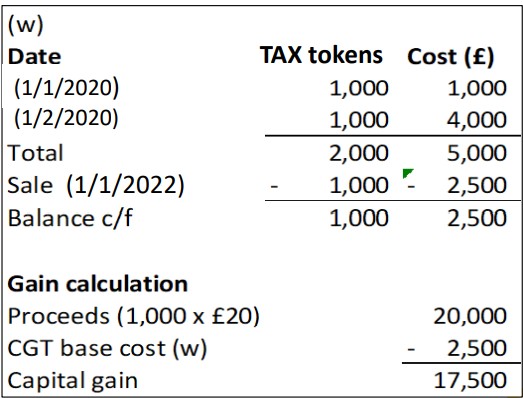

Pooling – exceptions

• Same day rule (TCGA 1992, s105)

• Bed and breakfasting rule (TCGA 1992, s106A)

• Blockchain forks

• Example

Allowable costs

• Transactions on Centralised Exchanges (Binance, Coinbase etc) and De-centralised

Exchanges (PancakeSwap, Uniswap) can be high

• There may be a cost where:

▪ Swapping fiat for crypto

▪ Swapping crypto for fiat

▪ Swapping crypto for crypto

• In respect of 3, the fees should be apportioned between the sale and purchase on a just and reasonable basis

Staking rewards

• For the purposes of this session… one can stake crypto on a CEX or DEX and earn rewards

• Usually in the form of tokens

• Analogous to the ‘interest’ on a bank account – often expressed as APY

• Taxed as miscellaneous income

Airdrops

• Marketing tactic to build crypto project / community

• Small amount of newly minted tokens

• Recent SOS token issued to users of Opensea NFT Platform

• Receipt (otherwise than as part of trade) not taxable

• Create new or add to existing s104 pool

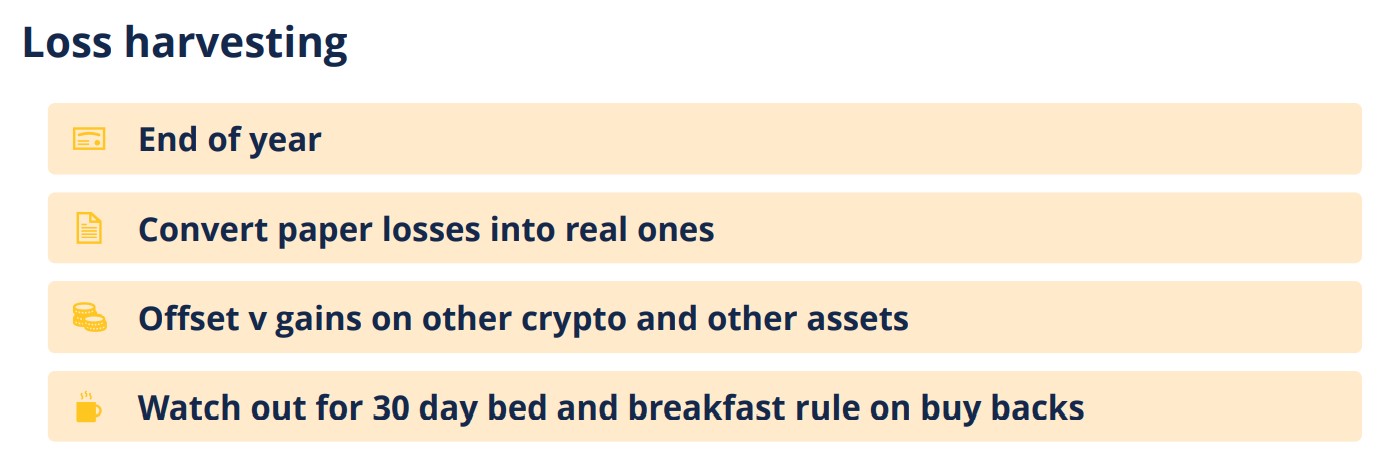

Capital losses

• If gains are chargeable then losses should be allowable

• Capital losses offset v:

– Current year gains; or

– Carried forward (indefinitely)

• As such, more limited than trading losses

Lost wallets, rug-pulls and scams

• Lost wallet – negligible value claim (under TCGA 1992, s25) if show unable to access / recover

• “Rug pulls”:

– New project

– Pump and dump by founders / early investors

– Utilise as a capital loss

• Scams

– Eg no token ever issued in exchange for investment

– No relief available

Residence

•General rule

•Only UK resident persons are subject to UK CGT

•Some exceptions – key being UK based real estate

•Anti-avoidance rules

•Selling whilst non-resident can be effective but watch 5-year rule

•Beware a leap from the ‘frying pan into the fire’!

Domicile (1)

•Remittance basis may apply where:

-

- Non-UK domiciled under general law; and

- Not deemed domiciled under UK tax rules

- What does the remittance basis actually mean?

•Income and gains from foreign assets can be left offshore

Domicile (2) – Is crypto a foreign asset?

• HMRC’s view

• Is there actually a statutory view?

• Ion Science v Persons Unknown (unreported)

• UK Jurisdiction Taskforce

• Fetch.ai v Persons Unknown [2021]

Are the activities of a trading nature?

• Where the default position is rebutted by…

– The taxpayer; or

– HMRC

• Does it matter?

– Higher rates of tax for an individual / unincorporated entity-

– NICs

– More flexible loss relief – including carry back up to three years v general income

– This last point means HMRC is likely to be reluctant to accept activities are trading in nature – even where activities appear organised, high frequency

Definition of trading activities (1)

• ITA 2007, s989: “Any venture in the nature of trade”

• Left largely to Courts

• Badges of Trade – Royal Commission, 1955

• Salt v Chamberlain

• Recent cases:

– Ali v HMRC [2016]

– Gill v HMRC [2018]

Definition of trading activities (2)

• In both cases the prima-facie presumption was rebutted by the FTT (fact-finding tribunal)

• Demonstrate a deliberate and organised way of operating

• Operate by reference to a business plan

Part 1c: Buying, selling and holding Non-Fungible Tokens (“NFTs”)

What is a Non-Fungible Token (“NFT”)?

• A NFT is simply a token that can be identified

• NFTs on Ethereum are issued as ERC-721 tokens (fungible tokens usually are issued as ERC-20)

• Usually identified by a number

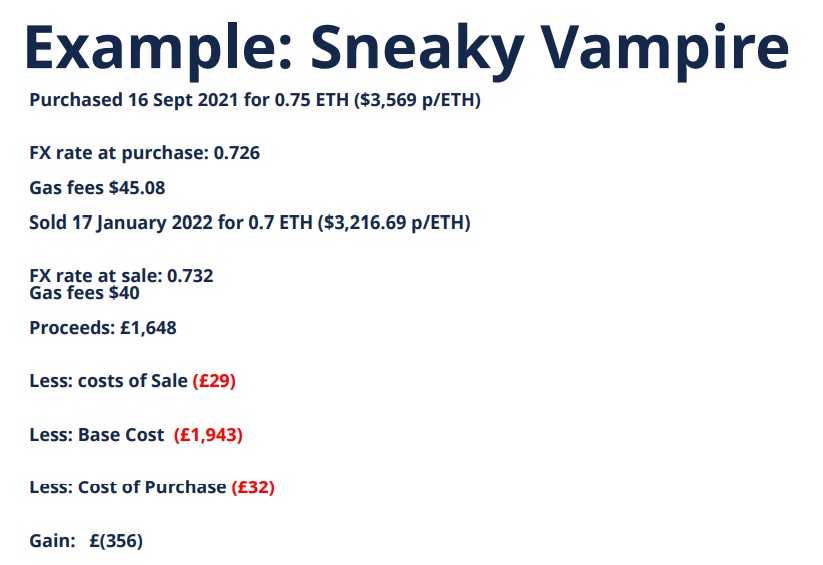

• This is Sneaky Vampire #4498 – 1/8,888

• Some analogy to ‘limited edition’ prints

• Not just art – NFTs include Music and other

Lifecycle of a piece of NFT artwork (1)

•More established eco-system for trading NFTs is Ethereum – though many others now available

•Opensea is perhaps the most popular platform for trading ETH NFT art

Step 1: Transfer ETH balance to Opensea

•If fiat to crypto: new purchase price relevant for CGT calc

•If fiat to fiat – disposal and new purchase

•Transfer of ETH from own wallet to Opensea account is not a disposal

Lifecycle of a piece of NFT artwork (2)

Step 2: Acquisition of NFT:

•Either:

– Newly minted token

– Secondary market purchase

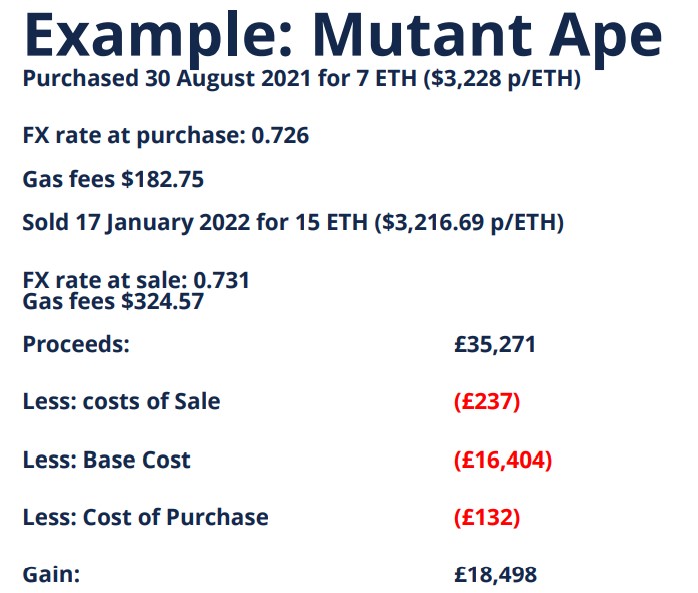

•Both will form the purchase price / base cost + gas fees

Step 3: Airdrops etc

•If another NFT token – separate asset with nil base cost

•If fungible tokens / crypto coin then add to new / existing s104 pool

Step 4: sale (see examples over)

Trading in NFTs

• Buying and selling like a dealer

– Hobby?

– Trade?

– VAT

• NFT Creator

– Hobby?

– Trade?

• Capital allowances – Wacom, Macbook etc

Part 2. Crypto mining and similar activities

Mining – Introduction

• Mining is the process of adding transactions to the blockchain

• Transaction or “Gas” fee is paid to the miners for doing that work

• Miners also add completed ‘blocks’ of data to the chain

• A reward is paid for that as well

• Decentralised maintenance of the blockchain

• Reward in return for work done suggests income

Mining – Principles (1)

• Trade or Miscellaneous Income?

• Back to the badges of trade

• Individual with a ‘rig’ or an organised and substantial operation?

• An individual with 6 mining ‘rigs’ in their garage? Or 24?

Mining – Principles (2)

• Expenditure

– Electricity usage directly related to income – allowable

– ‘Rigs’ – capital expenditure – disallowed

– Trade – capital allowances – AIA 100% / £1 million

– Company – super deduction – 130% / £1 million

Mining – Planning Points

• Incorporation

– Income tax rates

– If trade – capital allowances / super deduction

• Don’t forget:

– Trading allowance – £1,00

StrongBlock – Case Study (1)

• For the purpose of this session – akin to mining

• Stake 10 STRONG (current price c. £418 each)

• Operate a node – in most cases, StrongBlock do that for you

• Pay a monthly maintenance fee (nominal)

• Each node rewards c. 0.1 STRONG per day (gross yield c. 365%

StrongBlock – Case Study (2)

• Rewards are paid daily

• Must be collected

• ‘Gas’ fee for each collection

• If monthly maintenance is not paid – the node disappears

• Can not reclaim 10 STRONG

• Can not collect unclaimed rewards

• This can not be reversed – in the smart contract / the code

StrongBlock – Considered

• Daily rewards – clearly income

• Again, trade or miscellaneous? Badges of trade

• What is the tax point?

• When claimed? The income could disappear

• As it arises? So long as node exists, entitled to claim at any time

• Monthly upkeep

• No enduring benefit

• Revenue expenditure – allowable if a trade

• If miscellaneous – not directly related to the daily income received

StrongBlock – Capital Assets

• 10 STRONG initial cost

• What have you acquired – it will disappear if payments not maintained

• Likely capital expenditure – enduring benefit

• Trade (badges of trade?)

• Operators reinvest – often 100% reinvestment – cashflow

• May be an arguable case for trade

• Capital assets?

• Identifiable

• Enduring benefit

StrongBlock – Capital Allowances

• Assuming satisfied there is a trade:

• Plant? CAA 2001, s.71: “… computer software is treated as plant…”

• HMRC guidance says:

• “You should treat computer programs of any type and data of any kind as

computer software.” [CA23410]

• Capital Allowances may be claimed (main pool rate 18%)

• Can we go further?

• Annual Investment Allowance

• If a company – super deduction

StrongBlock – Capital Allowances

• Assuming satisfied there is a trade:

• Plant? CAA 2001, s.71: “… computer software is treated as plant…”

• HMRC guidance says:

• “You should treat computer programs of any type and data of any kind as

computer software.” [CA23410]

• Capital Allowances may be claimed (main pool rate 18%)

• Can we go further?

• Annual Investment Allowance

• If a company – super deduction

DeFi (Decentralised Finance)

- A brief mention:

- DeFi is also burgeoning

- Many transactions possible – including staking

- Cuts out the middle-man in many transactions – fast, secure and cheap

- Many different platforms

- Can give rise to complex transactions – will consider later in ‘Compliance’

Part 3. Gaming and play to earn activities

Axie Infinity – Case Study

• Base of game is Axies – each Axie is a unique NFT

• Not just an image – interacts with the Axie DApp on the Ronin blockchain

• Buy and sell Axies

• Breed Axies – new unique Axies generated by breeding

• Play Axie Infinity

• Use Axies to battle other Axies for rewards of “Smooth Love Potion” (SLP)

• Scholarship Programmes

• Hire people to play for you – scalability

• Profits can be very large (£100,000’s)

Axie Infinity – Considered

• Buying and Selling

• Capital gains / losses

• Breeding Axies

• Casual, or organised?

• Revenue expenditure on Axies for breeding?

• Profit on sale as income?

• Playing Axie Infinity

• Casual, or organised?

• Miscellaneous income or trade?

• Scholarship Programme

• Certainly a trade and many issues arise

Axie Infinity – Scholarships (1)

• Case Study

• Scholars receive a share of SLP earne

• Deductible against profits

• 280 scholars (mostly in the Phillipines)

• Breeding Axies for use in game

– Only some Axies are retained – the right qualities needed

– The rest are sold immediately

Axie Infinity – Scholarships (2)

• Cost of Axies (either breeding or purchasing)

• In this case – not known whether Axie will be a capital asset until it is ‘born’ –

5 days after expenditure

– Important for cash flow (reinvestment)

– Capital or revenue

– Capital – capital allowances / AIA / super deduction

Call the Midwife

Case Study in an unusual case

• CryptoKitties is an early blockchain game – like Axies, they could be ‘bred’

• The breeding required a ‘Midwife’ to ‘call’ a function on the blockchain to ‘give birth’

– Any blockchain interaction has a ‘gas’ fee

– Only one attempt could succeed – for a paid reward

• Client (and others) wrote an algorithm to ‘compete’ for the reward

– Each transaction either made a small loss (the fee) or a larger ‘win’

• A rare case where profits are arguably gambling

• Technical understanding of the transactions and the technology

Play-to-Earn Games – Don’t put the ‘phone down

• Play to Earn gaming is a ballooning market and in some cases, a lot of money is being made

• Mainstream game developers?

• In one case we have, we are putting in place an international corporate group… for people playing a game

• This area is bound to give rise to novel transactions

Part 4. Planning issues and opportunities

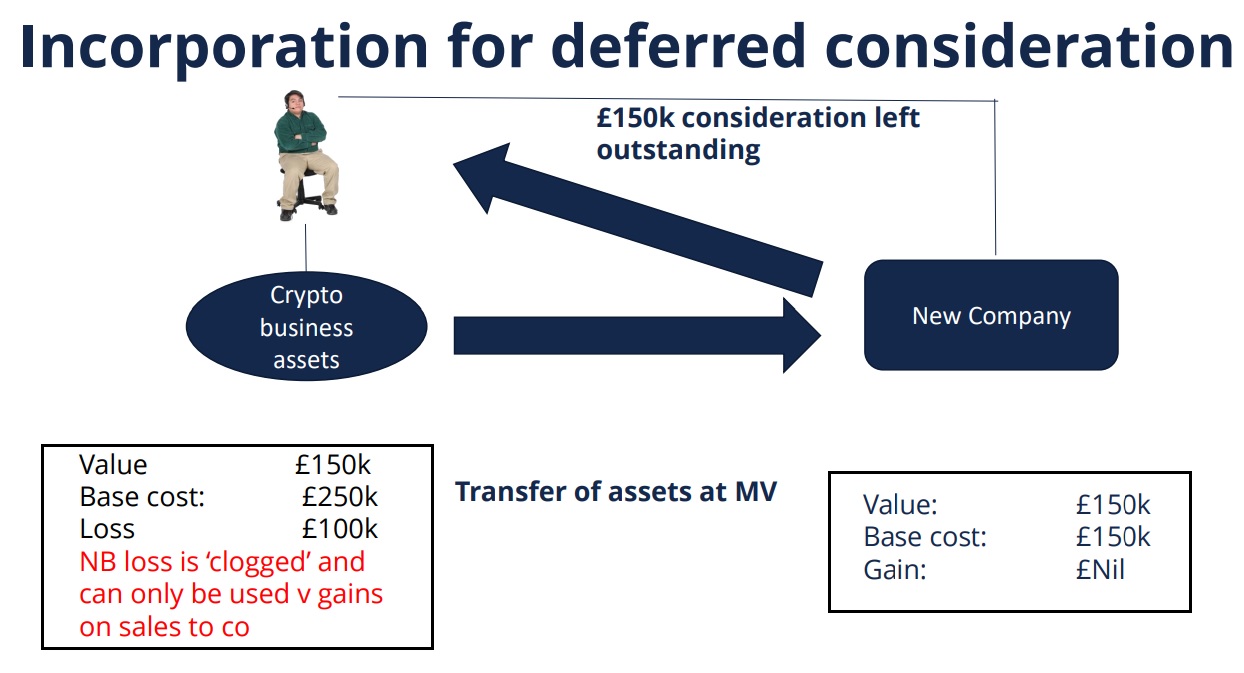

Incorporation for deferred consideration

• Unincorporated entity

• Transfer to a Company at MV with consideration left outstanding

• Disposal for CGT purposes – Any CGT payable 31 Jan following tax year

• Create tax paid loan account for the value of the portfolio

• Note problem with ‘clogged losses’ on sale to connected company

• Uplift in base cost on transfer of the assets to the Company – historic gains ‘washed out’

• Non-UK company?

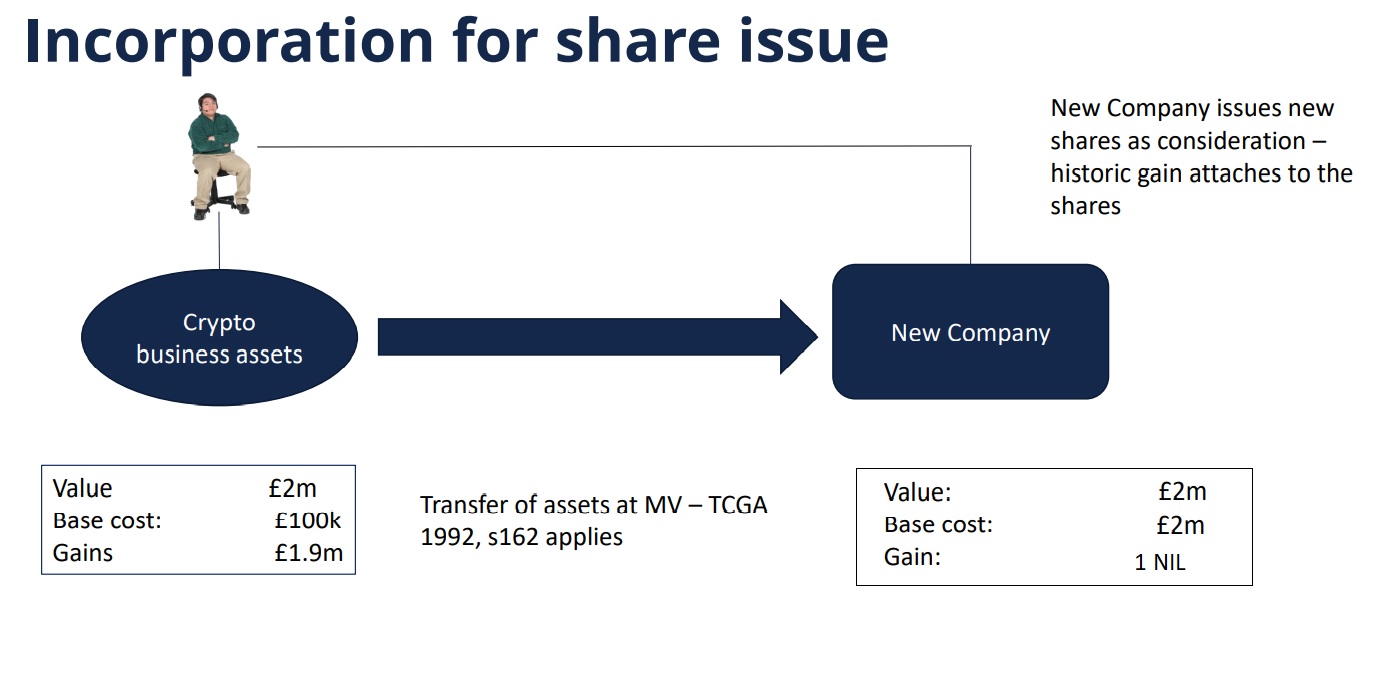

Incorporation for share issue

• Unincorporated entity

• Transfer to a Company = disposal for CGT purposes

• Where an investment business then incorporation relief would apply

• Scenarios where relief might apply?

• Uplift in base cost on transfer of the assets to the Company – historic gains ‘washed out’

• Non-UK company?

Becoming non-UK resident

Becoming non-UK resident

• As discussed, there is no UK CGT if sell crypto in a year of non-residence

• Mind 5 year temporary non-residence rule

• Important for new jurisdiction to be benign – ie, not jumping out of the frying pan into the fire!

• Usual suspects – Gib, Monaco, UAE etc

• Portugal

• Tax nomads?

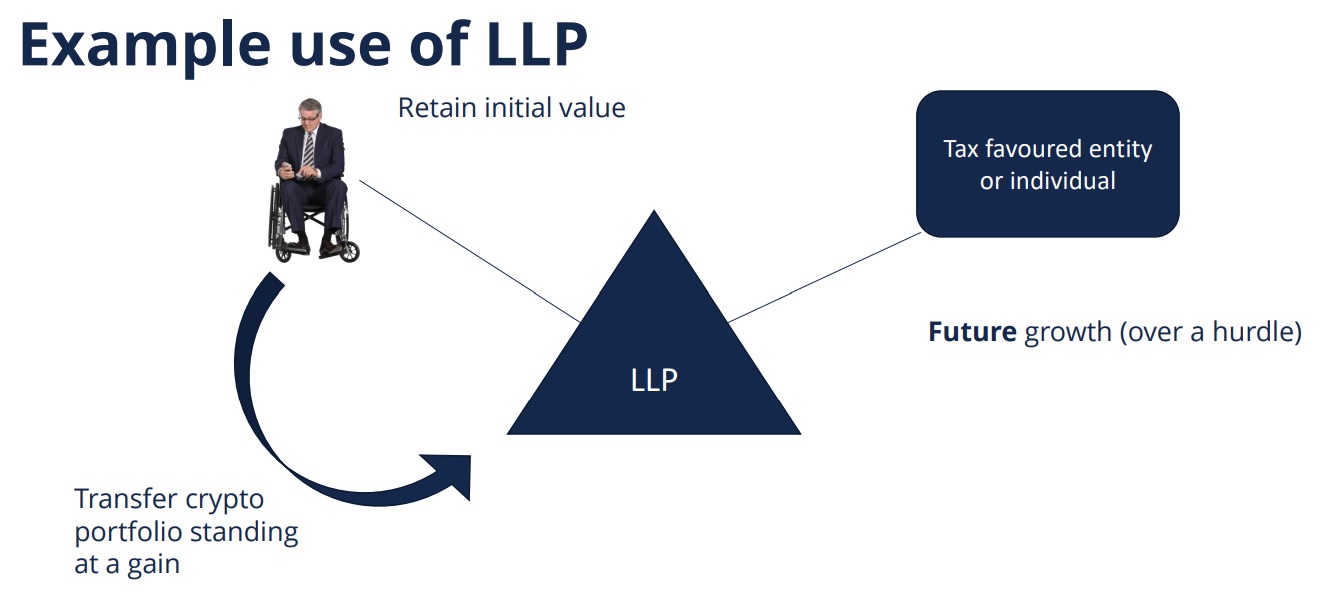

Use of LLP

• LLPs are a useful general tool

• Specifically, where one wishes to protect future growth from tax but sitting on

prohibitive inherent gains

• Where no scope for s162

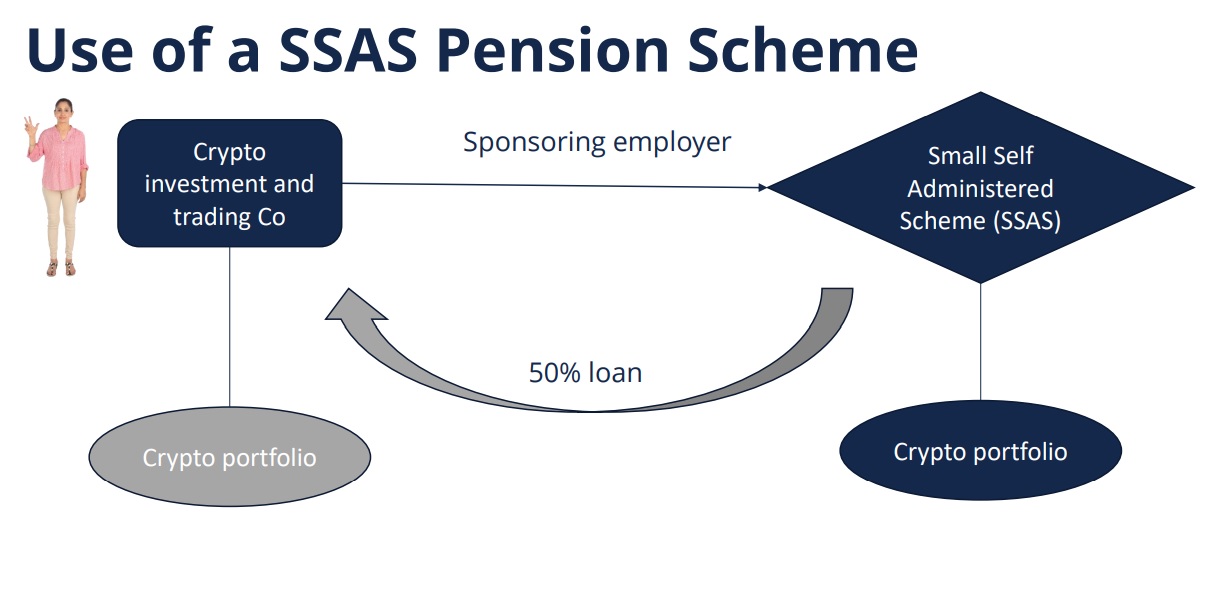

Use of Pension Schemes

• Registered pension schemes and Overseas Pension Schemes benefit from statutory exemption from CGT

• Unlikely to find an independent trustee of UK pension scheme who will hold crypto assets – SIPP unlikely to be viable

• Small Self-Administered Scheme (“SSAS”) – no need for independent trustee

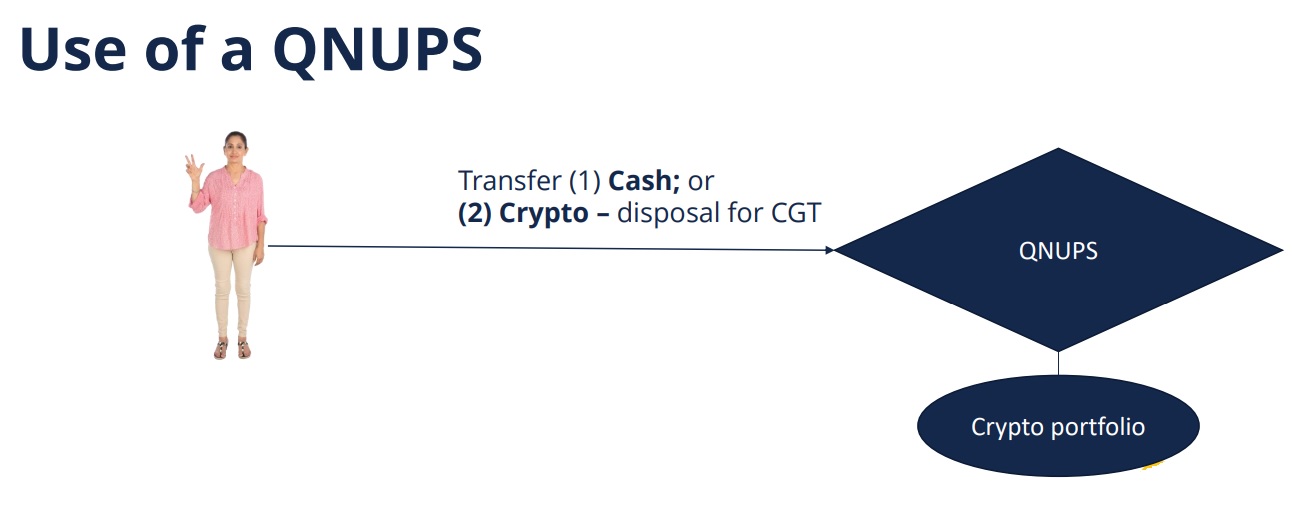

• Qualifying Non-UK Pension Scheme (“QNUPS”)

• Still benefit from CGT exemption

• More scope for investment flexibility

• Also should be outside of UK IHT net

Part 5. Compliance

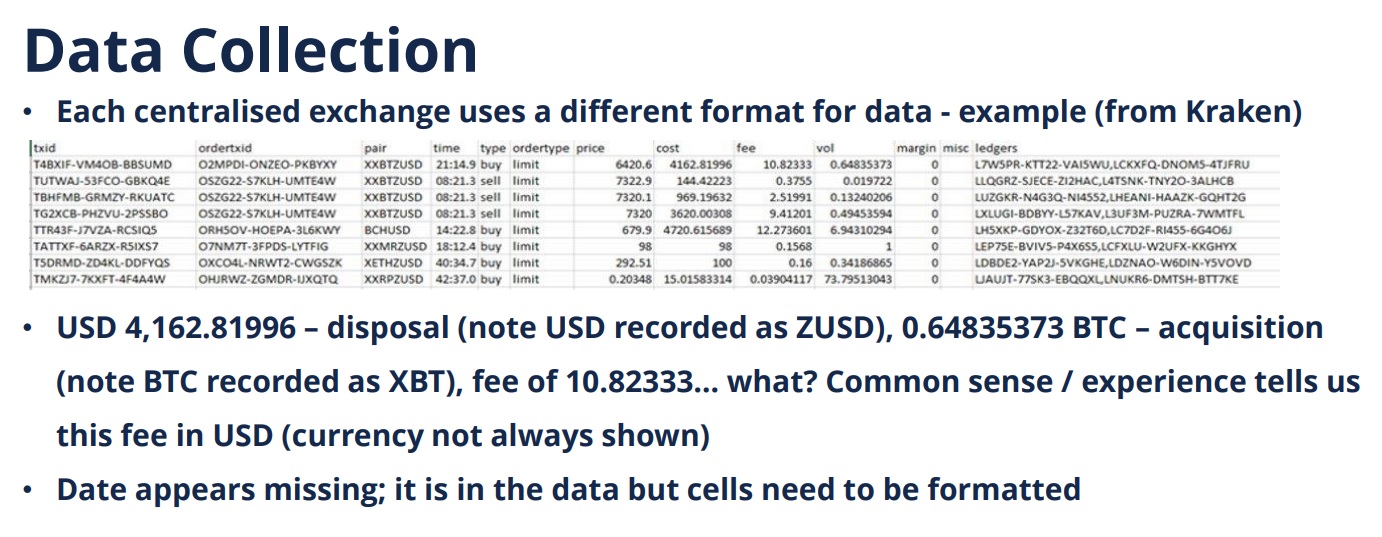

Practicalities

- A lot of data

- Our record is a .CSV file with c. 750,000 lines of data

- Software essential for pooling calculations

- Ambiguous data – unregulated, so ‘ticker symbols’ may be used more than once:

- 1 Pancake Bunny (BUNNY) = c. £0.65, 1 BunnyToken (BUNNY) = c. £0.000039, 1 Rocket Bunny (BUNNY) = c. £0. 000000000001

- Inconsistent data

• BitCoin on ledgers from Binance = BTC

• BitCoin on ledgers from Kraken = XBT

Plan Ahead

- Each CEX has different rules for downloading data

- Binance – only 4 downloads per month

• Trades, deposits, withdrawals etc., all are on different ledgers

• Maximum 3 months per ledger downloaded

• If left until January…

• Pooling calculations may need data from previous years to establish base cost

A Matter of Public Record

• DEX’s literally a law unto themselves

• May not even know who is behind / built / owns / maintains a platform

• No requirement to provide help or data?

• No ‘help desk’

• Often only records are from the blockchain itself

• EtherScan, BSCScan etc – online portals that allow anyone to ‘read’ the blockchain

• Remember – the blockchain is a public and transparent record of all transactions

• Only a user’s public key is (broadly) anonymous

Data Compilation

Option 1 – Automatic Compilation

• Primarily concerned here with multiple trades of cryptocurrencies

• All data must be amalgamated into one set

• The pooling calculation will treat all assets as a whole e.g. BTC held in two different wallets will be in the same pool

• Connect wallets and CEX platforms to software (e.g., Koinly)

• Data is drawn out, compiled and calculations completed

• Pros: Faster v Cons: Errors are common and can be difficult to identify

Data Compilation

Option 2 – Manual Compilation

• Strip out unnecessary data

• Regularise formats

• Regularise ticker symbols

• Bring all data together in a single body in the format expected by the software used

• Upload to software

• Pros: Most reliable output v Cons: Time consuming

Missing Data

- Issues we face:

• Clients with large volumes of trades…. And a low volume of organisation!

• Missing wallets (e.g private key lost) – so missing transactions

• Platforms no longer exist - Common for there to be missing data

• Assume base cost of zero

• Make a best guess estimate – record this

Complex Transactions

• Some DeFi platforms give rise to transactions with multiple elements e.g staking in the ETH-BNB liquidity pool on Pancake Swap

• Authorisation (a gas fee)

• Disposal of ETH (plus gas fee)

• Disposal of BNB

• Acquisition of ETH-BNB LP token

• Remembering that a gas fee is also a disposal [CRYPTO22280]

• Software may not be able to deal with these

• May require manual manipulation

Compliance – Conclusion

• Adopt a methodology

• Balance time vs. accuracy

• One size may not fit all

• Identify and understand any odd transactions

• If using software – check for errors

• Be prepared to manually override entries

• Be in a position to demonstrate to HMRC how you reached your conclusion and why it is reasonable

Disclosures

• Myth: no tax if not ‘withdrawn’ into fiat

• Penalties and reasonable excuse

• Not taken advice

• HMRC guidance unhelpful – not a ‘get out of jail free card’

• There are no special settlement opportunities for crypto profits

• Usual route for disclosure of previous non-compliance

• Note: HMRC guidance may be helpful for UK residents

• HMRC regard all crypto as situate with the owner

• Offshore non-compliance rules ought not to apply

Crypto’s anonymous isn’t it?

• The anonymity of crypto is largely a myth

• All transactions on the blockchain are recorded and easily viewable

• The identity of a wallet owner may be opaque… BUT transactions may link to: CEX, NFT purchases, real world purchases etc.

• Once a public key can be linked to its owner – the transaction history is open

HMRC interventions

• HMRC sending ‘nudge letters’ re. crypto

• HMRC have sent an information notice requesting data from CoinBase and similar

• Sample e-mail from CoinBase to customer “We’re writing to let you know about a notice HMRC have issued to Coinbase under Paragraph 1, Schedule 23 to the Finance Act 2011. This notice requires us to provide information on your Coinbase account to HMRC.

• The notice requires the disclosure of customers with a UK address who received more than £3,000 worth of crypto assets from Coinbase from April 6, 2020 – December 31, 2020…”

Money Laundering

• Blockchain transactions very transparent – individual public keys are opaque

• Most clients able to demonstrate all profits from original investment

• Example of suspicious transaction:

• CryptoKitty ‘Dragon’ sold for 600 ETH, double the record price at the time

• At the time c. US$ 170,000

• It had no rare or desirable features

• Transaction not consistent with other sales at the time

• Understand what is going on to identify risk