Skip to content

Skip to content

We have podcast interviews with thought leaders like Dan on our main website – www.htj.tax

I have mentioned Estonia before – https://www.mooresrowland.tax/?s=estonia

One thing missing from most discussions is economic substance. Setting up a shell company in Estonia may not be helpful in the long term as another jurisdiction may be able to tax your Estonia company as if it were an entity domestic to their jurisdiction. You strengthen the case for your company being taxable in Estonia if you have “Economic Substance” in Estonia.

What do I mean by substance? I have discussed it before – https://www.mooresrowland.tax/?s=economic+substance

In Estonia, factors would include –

- Office space. This may be your own office or a rented room;

- Appropriate organizational facilities, equipment, computers, furniture must be in the office depending on the specifics of the company;

- A functioning website of the organization is must; there should be attributes due to which it can be identified as belonging to the company. It is important that it contains an e-mail with the domain of the company’s registration area;

- Contact information. A phone number, fax, other contact information regarding the company relate to it;

- An open functioning bank account. It must be registered in the country of residence of a company and its management is also carried out on the spot. This account carries out transactions, money transfer transactions etc.;

- Managing Director. It is important that this is not a Nominee Director, but a person who is involved in the activities of a company and is legally responsible for its affairs. This is an extremely important aspect of Substance in Estonia;

- Other staff. This is necessarily a qualified, local accountant who keeps records and stores the document flow. Other professionals whose duties apply to the specifics of a company;

- Accounting entries for payroll, social contributions and other tax costs, including income tax, if such are provided by law.

- availability of partners (customers, suppliers) in Estonia

- the documented business revenue and the relevant taxes paid in Estonia (VAT, payroll taxes, etc.)

- a VAT number

- local employees

- Estonian citizenship or residence permit of at least one Board member

- a lease of a real office and/or a warehouse in Estonia

- availability of a startup visa

- a functioning localized business website in Estonia

- shipment of goods through the territory of Estonia.

- records of meetings held on Estonia soil

Statutory requirements

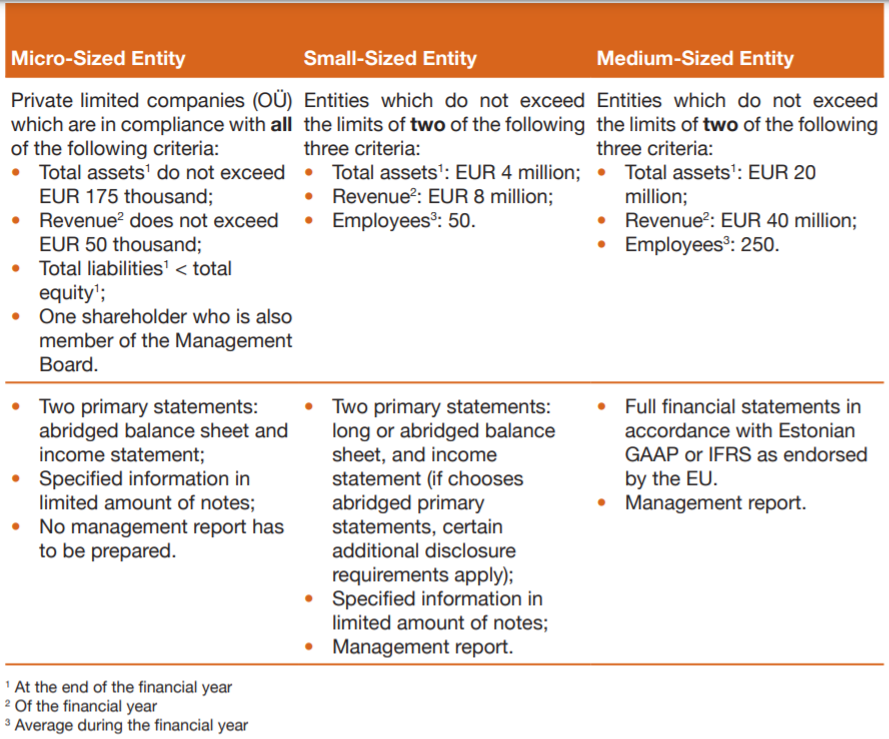

The length of a financial year is twelve months. In the event of an accounting entity being founded or terminated or the date of the commencement of its financial year being changed, or in other cases prescribed by law, the financial year of the accounting entity may be shorter or longer than twelve months but shall not exceed 18 months. At

the end of each financial year, an accounting entity (public limited company, private limited company) is required to prepare an annual report. The content and volume of the annual report depends on the size of a company. The size groups and applicable requirements are defined by the Accounting Act as follows

Annual report is to be submitted to the Commercial Register within six months of the end of the financial year.

All annual reports prepared under Estonian GAAP, except for consolidated annual reports, are to be submitted electronically in XBRL format through Company Registration Portal https://ettevotjaportaal.rik.ee/.

Other annual reports are to be submitted in pdf format. Consolidated annual reports prepared under Estonian GAAP and annual reports prepared under IFRS can voluntarily be submitted in XBRL format. Entries in the Commercial

Register are public. Everyone has the right to examine the card register and the business fi les, and to obtain copies of registry cards and of documents in the business files.

Branches of foreign companies need not to prepare annual reports. Instead, an unattested copy of the audited and approved annual report of the company is submitted to the Commercial Register of the location of the branch no later than one month after approval of the annual report or seven months after the end of the financial year. This requirement does not apply to companies of states which are Contracting Parties to the EEA Agreement if the legislation of the country of the registered office of the company does not require the annual report to be

disclosed.

Obligation to preserve accounting documents:

� accounting source documents – for seven years from the end of the financial year during which

the source document was recorded in the accounts;

� accounting ledgers, journals, contracts, financial statements, reports and other business documents which are necessary for reconstructing business transactions during audits – for seven

years from the end of the corresponding financial year;

� business documents relating to long-term rights or obligations – for seven years after the expiry

of their term of validity;

� accounting rules and procedures – for seven years after the amendment or replacement thereof;

� the above data should be preserved in machine-processable format. The ability to reproduce,

the legibility and evidential value of the data should be ensured within the retention period.

Get professional advice when dealing with Estonia…