Skip to content

Skip to content

Andorra is an interesting low tax jurisdiction but it is not a tax haven. At least not any longer.

Andorra is a small country located in Europe between France and Spain. Although the country is not part of the European Union, it uses the euro as its national currency

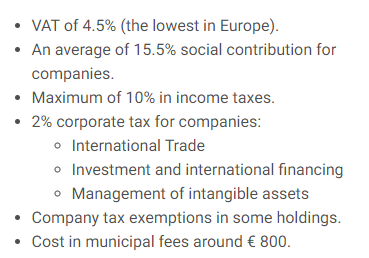

Historically, Andorra had no income, capital gains, sales, gift, or inheritance tax, and gaining residency was relatively simple. But that all changed after 2015, when the country introduced its own taxation system. This was a direct result of pressure from the rest of the EU, which felt Andorra was being used by wealthy individuals and corporations to avoid paying taxes

Unlike most other tax havens, Andorra does not provide for the easy creation of offshore companies, so it is better suited to wealthy individuals who need offshore banking services than to businesses looking to hide assets in Andorran-based subsidiaries.

Nonresidents must request approval from the Ministry of Economy to own more than 10% of an Andorra-based company. But this often proves to be difficult. It is possible for a foreigner to form a company after attaining residency, but the company’s net profits are subject to the 10% corporate tax applicable to resident businesses

Personal income tax in Andorra

Through personal income tax, all income subject to tax is taxed regardless of where it was produced and the state where its payer is established. That is, the worldwide Income obtained by the Andorran resident taxpayer.

A tax resident is considered the natural person who, in a simple way, fulfills one of the two:

- Live more than 183 days in the Andorran territory during the calendar year.

- Settles in Andorra on main core of their economic activities or their economic interests, directly or indirectly.

Thus, for example, border workers, whose incomes are subject to the income tax of non-tax residents (in special regime) are not considered tax residents in Andorra.

Income tax declaration and types of income

Tax resident physical persons in Andorran territory have the obligation to file the declaration of the tax, in the following cases:

- If income is obtained from economic activities.

- If the income from real estate capital and / or income from work obtained is a full amount equal to or greater than 24,000 euros.

- If the income obtained from the movable capital has not been withheld and exceeds 3,000 euros.

- If capital gains and losses are obtained.

Europe and tax efficiency rarely go hand in hand. However, Andorra is indeed an interesting jurisdiction for the higher net worth individual looking for a base in Europe.