Skip to content

Skip to content

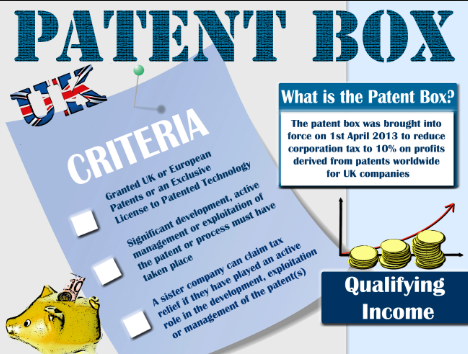

- What is a patent box? – A patent box (or IP box) is a tax incentive that allows business income from the sale of patented products to be taxed a lower rate than regular income.

- What kind of business income qualifies for the lower patent box tax rate? Most patent box nations allow income from more than just patented products to qualify. Some countries have gone further and established “innovation boxes” that allow income from designs, copyrights, models and trademarks to also be taxed at the lower patent box rate. And with the broadest definition of IP-sourced income, China extends its patent box to allow income from certain types of commercial “know-how”, such as process innovation, to qualify for the lower rate.

- Why haven’t I heard more about patent boxes? Patent boxes are relatively new. While Ireland was the first nation to develop a patent box in 1973, the other nations with them (Belgium, China, France, Luxembourg, Netherlands, Spain, Switzerland, UK) all put them in place in just the last few years.

- Why have so many nations adopted patent box regimes recently? Most nations with patent boxes established them in the mid- to late 2000s. They did so because they recognized that the race for global innovation advantage has heated up and that if they were to retain and grow innovation-based jobs, they needed to do more to make their countries attractive for innovation. Increasingly innovation is highly mobile as the talent and infrastructure to conduct innovation -based activities are available in many nations around the world. Because of this, these countries instituted patent box policies, plus a host of other innovation policies, including in most nations boosting government support for R&D.

- If a nation wants to better compete for innovation-based economic activities, why not just boost R&D incentives? R&D tax incentives are an important component of an effective national innovation strategy. Patent boxes differ from R&D incentives, though, because they provide firms with an incentive for commercialization of innovation, rather than just for the conduct of research. Commercialization of innovation, rather than the simple conduct of R&D, is a key driver of economic growth and jobs and therefore creating tax incentives linked to success at commercializing innovation is an important strategy for growth, competitiveness and job creation.

- Does the USA have a patent box? In a way – yes. A provision in the newly revised U.S. tax code slashes the income tax companies pay on royalties from the overseas use of intellectual property or so-called intangible assets, such as licenses and patents. The new tax break, for what is dubbed foreign-derived intangible income (also known as FDII), effectively reduces tax on foreign income from goods and services produced in the U.S. using patents and other intellectual property to 13.125% until the end of 2025, after which the rate rises to 16.4%. Previously, royalties paid to a unit in the U.S. would have been taxed similarly to other U.S. income, for which the top corporate tax rate was 35%. The new headline corporate rate is 21%. The deduction is meant to induce companies with large U.S. operations and significant foreign income from patent royalties to base more of those assets in the U.S. Such companies, especially in technology and pharmaceutical sectors, often hold foreign rights for their IP in a company based in a low-tax country.