Skip to content

Skip to content

Please start by reading this – https://www.mooresrowland.tax/2014/03/the-scariest-us-tax-form-ever.html

In 2015, the IRS released a new International Practice Unit (IPU) providing guidance to its examiners on the penalties that apply if certain categories of U.S. shareholders fail to comply with the reporting requirements on Form 5471, Information Return of U.S. Persons With Respect to Certain Foreign Corporations. The IRS has stringent standards to determine when a Form 5471 is substantially complete and thus not subject to the $10,000 penalty (discussed below) under Sec. 6038(b).3

It is important to note that the statute of limitation remains open on the taxpayer’s entire tax return if Form 5471 is not filed, and does not expire until three years after the date on which the information required to be reported is filed and properly reported.

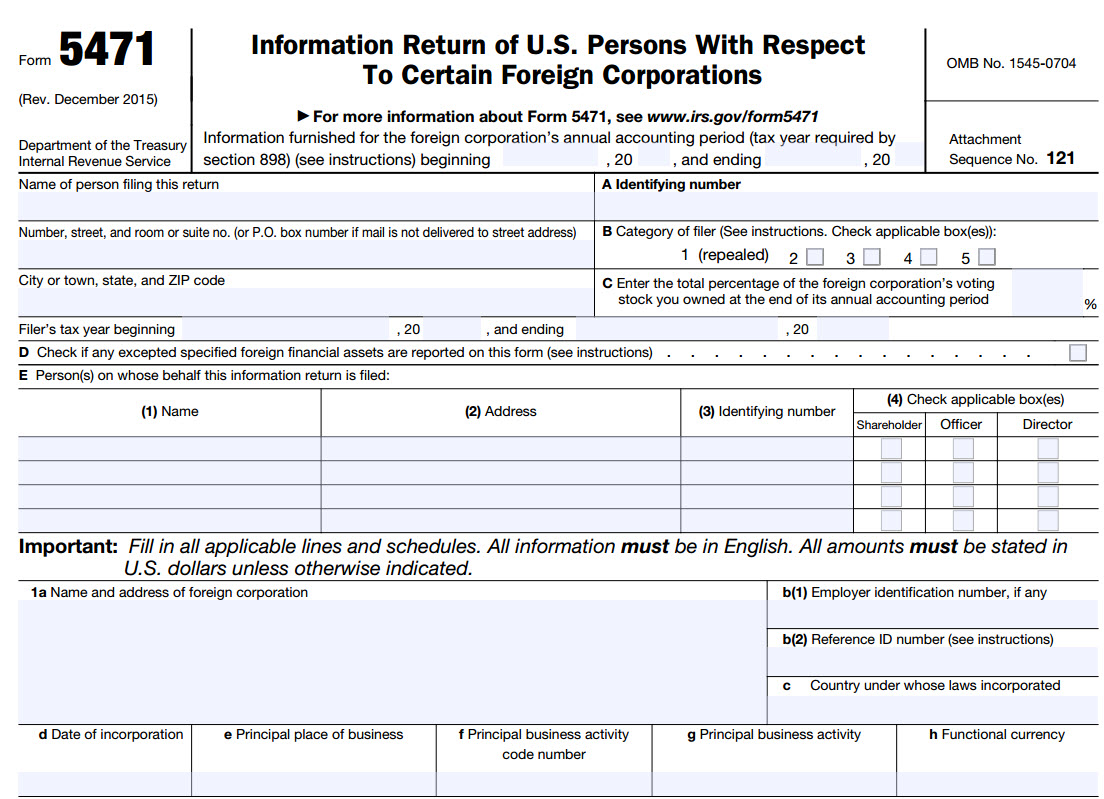

To adhere to the reporting requirements of Secs. 6038 and 6046, Form 5471 is required to be filed by certain U.S. persons who are officers, directors, or shareholders in certain foreign corporations.

Generally, certain U.S. persons must complete the schedules, statements, and/or other information requested. Four categories6 of U.S. persons7 are required to file Form 5471.8 Form 5471 is required to be attached to and filed with the income tax return that the particular person must file (Form 1040, U.S. Individual Income Tax Return; Form 1120, U.S. Corporation Income Tax Return; Form 1065, U.S. Return of Partnership Income; or Form 990, Return of Organization Exempt From Income Tax). The reporting period during which the required information is provided is the annual accounting period of the foreign corporation ending with or within the U.S. person’s tax year.9

Penalties

The IPU provides that penalties under Sec. 6038 may apply when a Form 5471 is filed late, is substantially incomplete, or is not filed at all. For any of these three types of failures, an initial penalty of $10,000 per Form 5471 per year may be assessed. Also, an additional penalty of $10,000 per Form 5471 per year may be assessed for every 30–day period (or fraction thereof) commencing 90 days after the U.S. person was notified that a failure exists.10 The maximum amount of that penalty is $50,000 per Form 5471 per year.11 These penalties may apply per Form 5471 required on an annual basis. (And the most significant penalty from a compliance standpoint is that the statute of limitation will not toll until the form is filed.)

Substantial Compliance

What is substantial compliance? Since a definition of “substantially complete” for Form 5471 reporting is not contained in the Code or the regulations, the IPU provides certain examples for IRS audit examiners where a Form 5471 may be considered not substantially complete. The IPU focuses on just two categories of Form 5471 filers: Category 4 and Category 5 filers.

A Category 4 filer includes a U.S. person who controlled a foreign corporation for at least 30 days during the tax year.12 A U.S. person is a citizen or resident of the United States, domestic corporation, domestic partnership, or estate or trust that is not a foreign estate or trust.13 A U.S. person that owns more than 50% of the combined voting power of all classes of stock entitled to vote or 50% of the value of all classes of stock of a foreign corporation has a controlling interest in that foreign corporation.14

A Category 5 filer includes a U.S. shareholder who owned at least 10% of a foreign corporation considered a controlled foreign corporation (CFC) for at least 30 days during the tax year and who owned the stock on the last day of the year.15 A U.S. shareholder is a U.S. person who owns 10% or more of the combined voting power of all classes of voting stock of a foreign corporation.16 For Category 5 filers, the definition of “U.S. person” is similar to that used for Category 4 with exceptions as provided by Sec. 957(c).17

The IPU discusses two types of errors that may cause a Form 5471 to not be substantially complete: (1) errors apparent on the face of the form and (2) errors beyond the face of the return.

Errors Apparent on the Face of Form 5471

The IPU provides that if a Form 5471 contains the following errors on page one of the form, it does not comply with the Sec. 6038 reporting requirements.

First is item B: Category of filer. If the category of filer is left blank or is incorrect, then the schedules of Form 5471 required to be completed cannot be determined.

Next is item C: Total percentage of the foreign corporation’s voting stock owned at the end of the annual accounting period. When Item C is omitted or incorrect, there is again no way to determine which schedules of the form must be completed.

Then the IPU discusses item 1a: When the name and address of the foreign corporation is omitted, other information on the form cannot be associated with a specific foreign corporation. Finally, items 1b(1) and 1b(2) involve the employer identification number (EIN) and reference ID number being omitted. When these are missing, information provided on the form cannot be associated with a specific foreign corporation.

The IPU also instructs IRS agents to review “Form 5471(s) for any schedule required (based on the filing category)” that is not prepared, e.g., Schedule J, Accumulated Earnings and Profits (E&P) of Controlled Foreign Corporation, or Schedule M, Transactions Between Controlled Foreign Corporation and Shareholders or Other Related Persons. Each tax year, the instructions to Form 5471 include a chart titled “Filing Requirements for Categories of Filers” that lists schedules18 required by category of filer to be completed. If a Form 5471 does not contain a required schedule, the IPU provides that Sec. 6038 is not “substantially complied” with.19

The most common reasons for noncompliance with Sec. 6038 that are cited in the IPU are:

- Stating that required information will be furnished upon request or audit;

- Providing computer-generated Forms 5471 that were not IRS-approved and did not conform to requirements;

- Failing to provide financial statements for CFCs; and

- Providing consolidated financial statements of two or more foreign corporations.

Errors Beyond the Face of Form 5471

The IPU describes errors beyond the face of the form as ones that a reviewing agent generally would notice after having researched information and/or obtained documentation while working through issues on the form.

The IPU refers to a 1997 field service advice (FSA)20 addressing if there was substantial compliance with Sec. 6038 when significant understatements of related–party purchases and/or sales were reported and significant inconsistencies were reported for earnings and profits.21 The IPU noted that the FSA states “that Congress did not intend that providing more of the required information than not (an aggregate approach) met substantial compliance. It was more important to determine substantial compliance on a significant item by significant item basis.”22 The IPU refers to Chief Counsel Advice (CCA) 200429007, which “provided a facts and circumstances analysis for ‘substantially incomplete’ in contrast to a strict interpretation of the regulations that any over–reported or underreported transaction amount meant the form was ‘substantially incomplete.'”23

The CCA provided seven factors, enumerated below, for IRS agents to use in that analysis.24 Another CCA25 and its summary advised that significant pieces of required information included (1) balance sheet and income statement amounts not in accord with U.S. GAAP and (2) income statement and income tax amounts that were not in both functional and U.S. currencies (Schedules C, Income Statement, and E, Income, War Profits, and Excess Profits Taxes Paid or Accrued, of Form 5471). Accordingly, the Form 5471 was not in compliance with Sec. 6038.

The IPU provides “[b]oth the 1997 FSA and CCA 200645023 focused on the significance of the required information. Depending on the complexity and magnitude of the error, . . . an analysis using the seven factors in CCA 200429007 might be useful in determining whether the [U.S. person] substantially complied with [Sec.] 6038.”26

The seven factors stated in CCA 200429007 are:

- The magnitude of the underreporting, or of the over-reporting, of the erroneous reported transaction in relation to the actual total amount of that reported type of transaction(s);

- Whether the reporting corporation has reportable transactions other than the erroneous reported transaction(s) with the same related party and correctly reported those other transactions;

- The magnitude of the erroneous reported transactions in relation to all of the other reportable transactions as correctly reported;

- The magnitude of the erroneous reported transactions in relation to the reporting corporation’s volume of business and overall financial situation;

- The significance of the erroneous reported transactions to the reporting corporation’s business in a broad functional sense;

- Whether the erroneous reported transactions occur in the context of a significant ongoing transactional relationship with the related party; and

- Whether the erroneous reported transactions are reflected in the determination and computation of the reporting corporation’s taxable income.27

Finally, an important item contained in the IPU that taxpayers should be aware of is that Forms 5471 are required to be filed for dormant corporations.28

Conclusion

Taxpayers and practitioners should pay close attention to how Form 5471 and the related schedules are completed, including reviewing Forms 5471 from prior years. Failure to properly complete the forms and schedules can have significant penalty and perhaps other income tax ramifications for taxpayers in years ahead, not the least of which is the statute of limitation not running until the forms are filed, all of which could be difficult to resolve.

Full article here – https://www.thetaxadviser.com/issues/2016/jun/form-5471-substantial-compliance.html