Skip to content

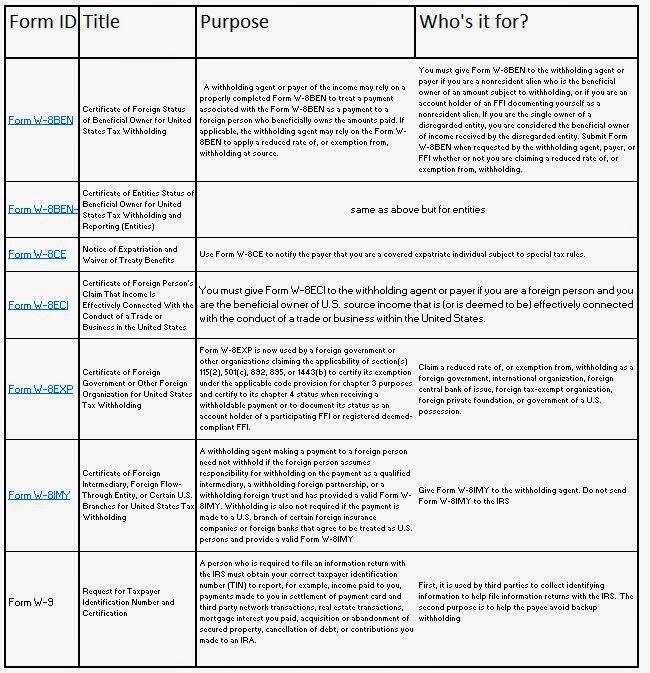

Skip to content One of the consequences of FATCA is that financial institutions and their (overseas) clients are struggling to come to terms with evolving form requirements.

One of the main purposes of the W-8 forms is to show financial institutions (e.g. brokers and mutual fund companies) and certain other US entities, that the foreign investor / payment recipient, is not subject to the typical taxation practice where tax is withheld from payments / investment income (e.g. dividends and coupon payments). If adequate documentation is not supplied with a W-8 form, the foreign investor will be subject to the normal rates of backup withholding.

I myself have spent far too much time on the phone trying to explain to front line staff (it’s not their fault, they are just trying to understand the cryptic instructions from their line manager) the difference between the W-8s and W-9. Unfortunately, I expect the confusion to get worse before it gets better…