Skip to content

Skip to content

CHAPTER 1: CHOOSING A BUSINESS FORM: INTRODUCTION AND OVERVIEW

I.INTRODUCTION

Deciding to start a business is just the first in a series of important decisions. One of the most important questions the organizer or organizers must answer is “What is the best business form to choose?” The answer depends on a number of factors, including, but not limited to, the number of participants, concerns about taxes, and exposure to personal liability. Some issues will be more or less important to each individual or group. Key issues in the choice of entity include the following:

• Taxation

• State law treatment

• Nature of the assets

• Transferability of the business, both during life and upon death

• Estate planning

• Ease of management

• Number of owners/investors

• Number of owners who will be actively involved in managing the business

• Limited liability

• Retention of control

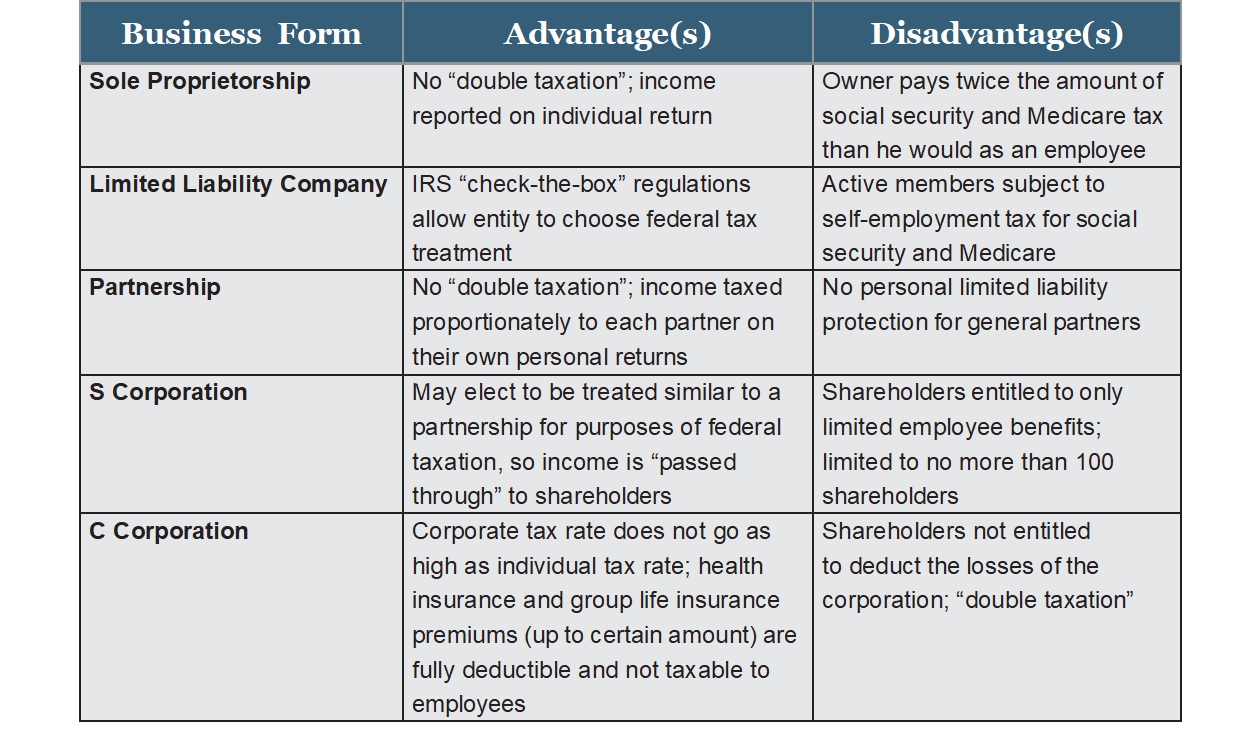

Today, there are more choices than ever in selecting the appropriate business entity. Historically, there were three choices: the sole proprietorship, the partnership and the corporation. Now there are a number of hybrids that combine various characteristics of each traditional entity, such as the limited liability company that combines the limited liability of a corporation with the flexibility and tax advantages of a partnership. All states offer limited liability companies as an option for most types of businesses. Another option is the limited liability partnership.

State law can also play an important role in determining the best entity. State law governs many important aspects of business entities, both tax and non-tax (i.e., in some states, an S Corporation is treated more favorably than in others).

It is important for a practitioner to offer advice to clients to understand both the tax and non-tax characteristics of each entity before opining on the best structure for any particular enterprise. This chapter will provide an overview of the major attributes of each type of entity. The subsequent chapters will provide a detailed look at a number of these issues, including formation, management, dissolution, and taxation.

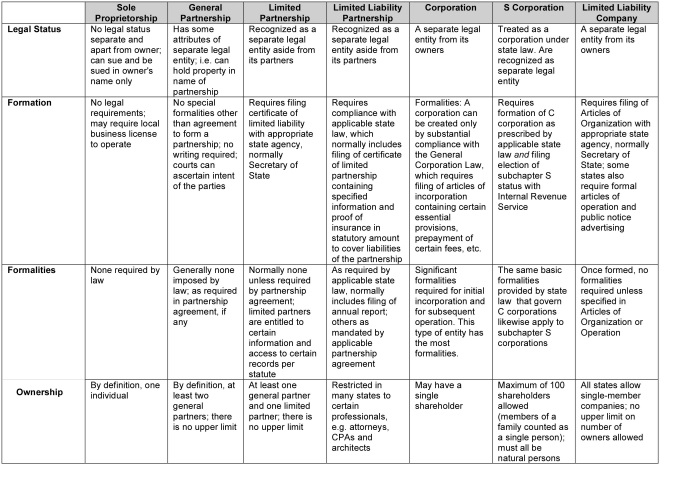

II. SOLE PROPRIETORSHIP

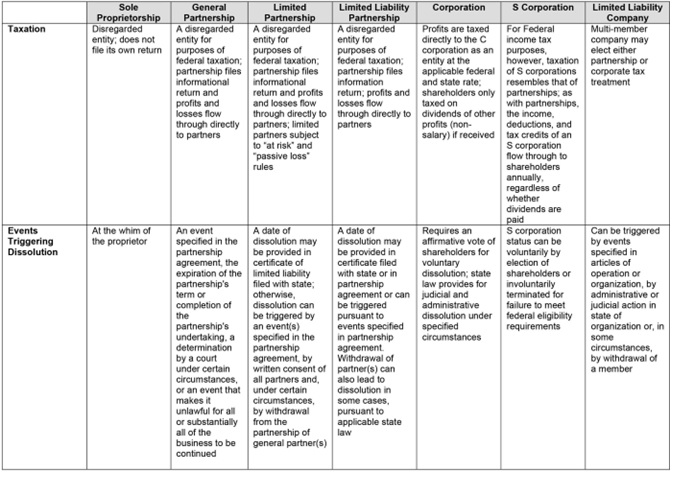

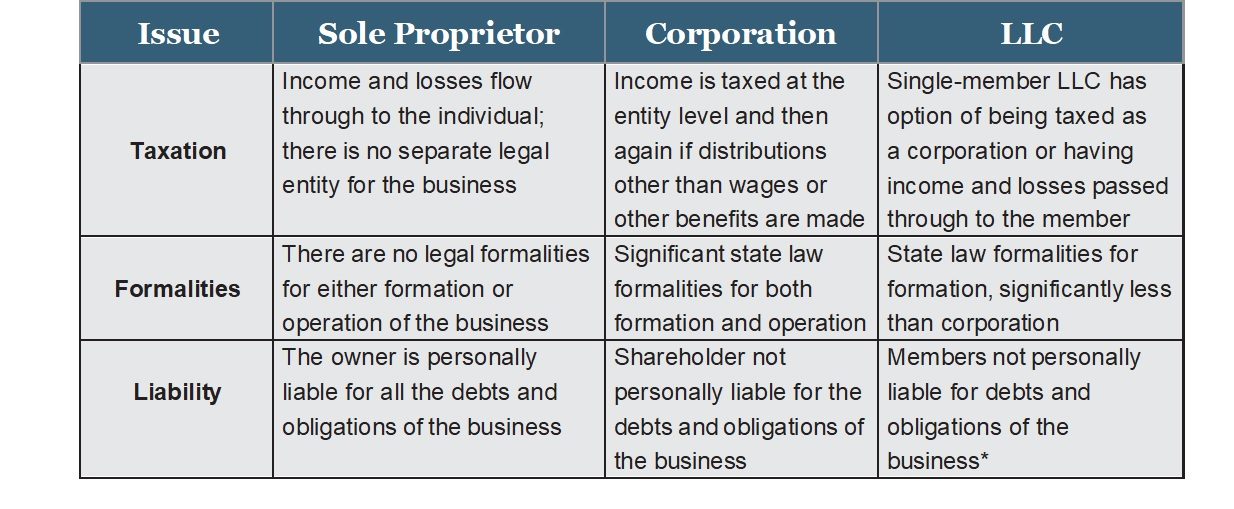

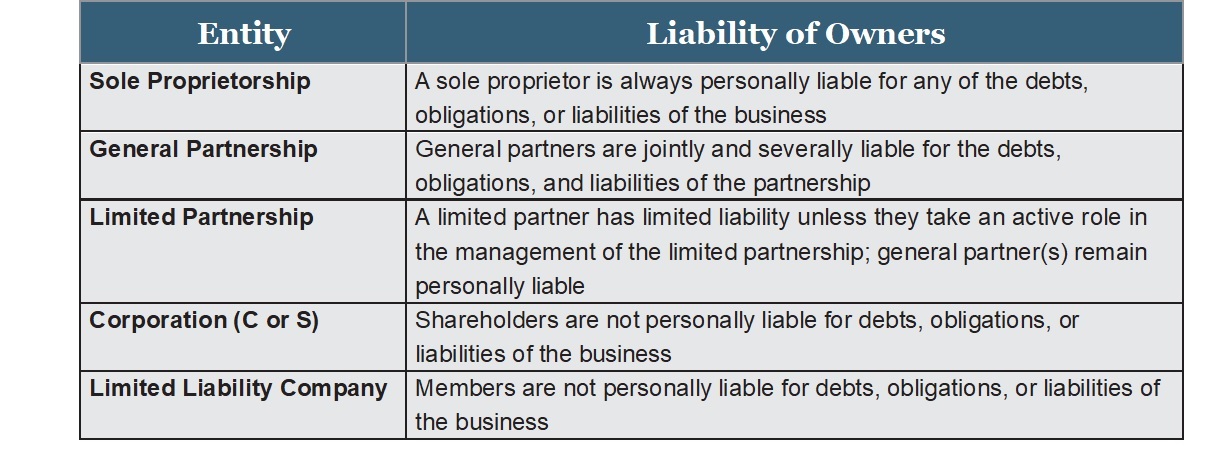

A sole proprietorship is an unincorporated business that is owned by one individual. It is the simplest form of business organization to start and maintain. There are no filing requirements – no partners with whom you have to agree. The business has no separate legal existence apart from its owner. Its liabilities are the personal liabilities of its owner. The income and losses of the business are included on the owner’s personal tax return.

Unlike partnerships and corporations – for which there are many, many statutory provisions – a sole proprietor is not subject to any separate set of laws. General business and tax laws apply, including those governing contracts and torts.

Major Attributes: Sole Proprietorship

• No requirements for formation; no franchise fee or license to obtain (unless local entity requires business or professional license or fictitious name filing)

• No formalities required for operation, i.e., no meetings or corporate filings

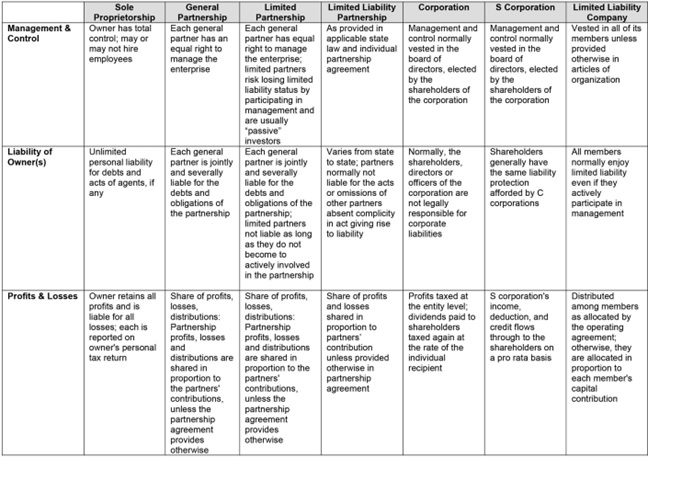

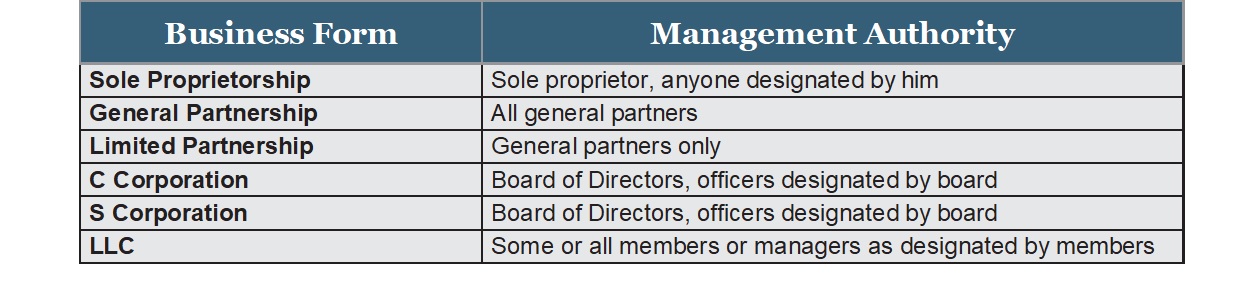

• Sole proprietor has complete management authority, may or may not utilize agents

• Owner personally liable for all debts and obligations of the business

• All profits and losses are included in the owner’s personal tax return; the entity is not recognized for tax purposes

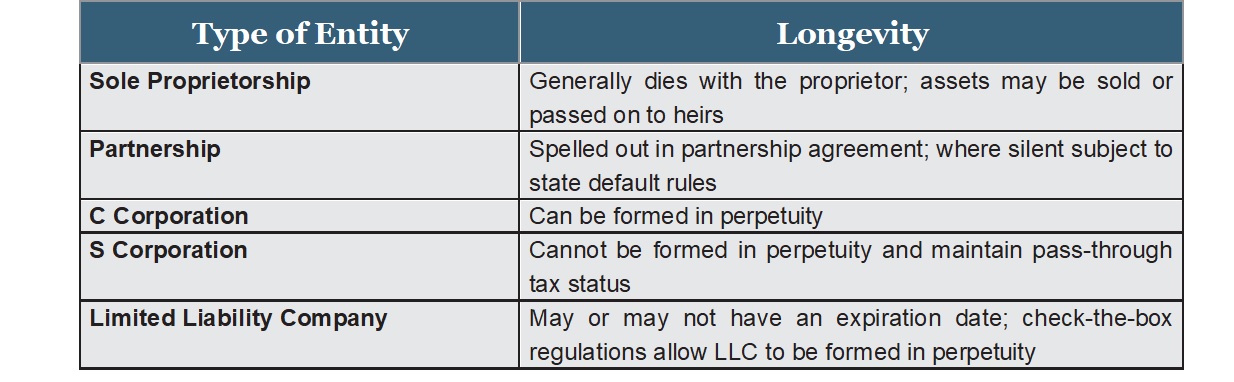

• Enterprise normally dies with the owner

• Business or assets thereof may be transferred or sold at the sole discretion of the owner

• Owner may decide to convert business to different type of entity, i.e., to form single-member LLC

• All judicial proceedings occur in the name of the owner

The major advantages and disadvantages of the sole proprietorship, like all types of entities, are based on its characteristics. The major advantage is probably its simplicity: there are no papers to file, and no meetings to hold. A sole proprietor may make decisions at any time about any matter. On the other side of the coin, the sole proprietor is personally liable for all the debts and obligations of the business. If a sole proprietor elects to engage agents in the operation of the business, including, but not limited to, employees, he or she is also vicariously liable for all of the agents’ actions committed in the scope of the business.

III. PARTNERSHIPS

A partnership is the relationship existing between two or more persons or entities that join together to carry on a trade or business. Each person or entity contributes money, property, labor, or skill, and expects to share in the profits and losses of the business.

There are now a number of different types of partnerships recognized by state law. The three major types will be briefly described next. This overview provides a general understanding only; individual states may have different rules.

A. GENERAL PARTNERSHIP

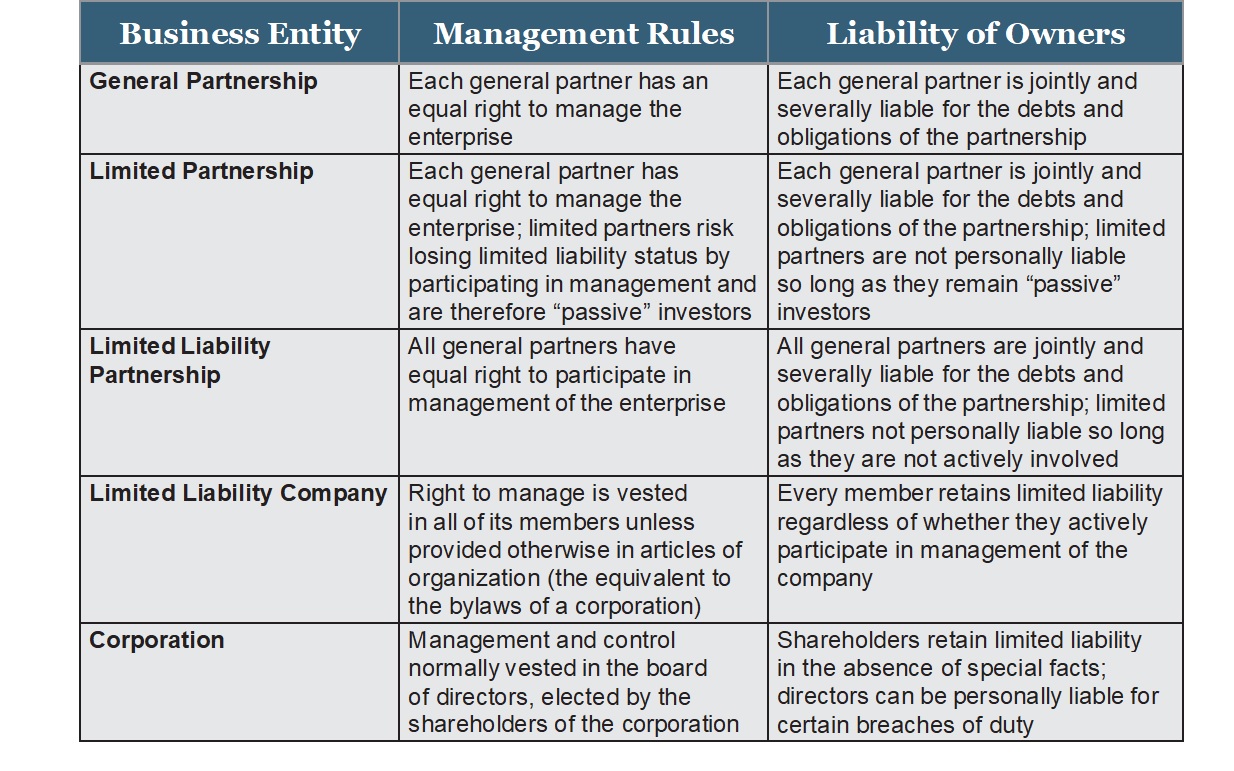

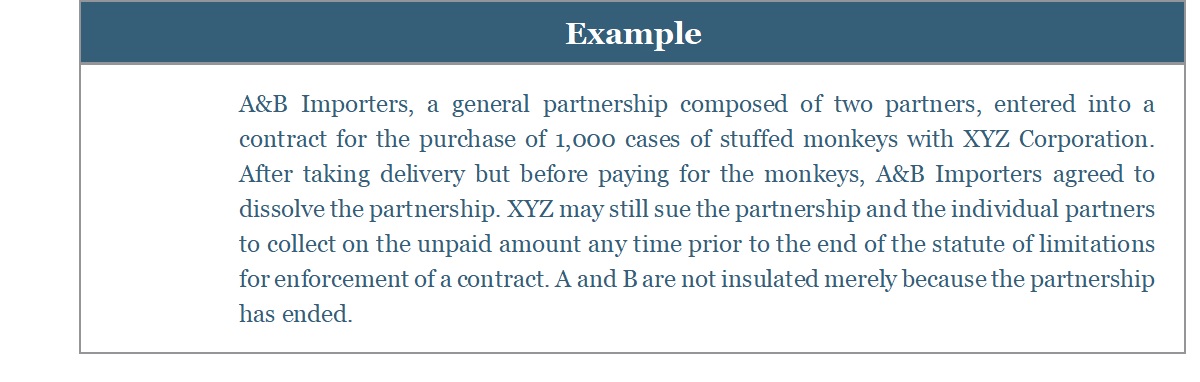

At common law, this was the only type of partnership recognized. Aside from the sole proprietorship, the general partnership is the easiest business entity to form. There are no legal requirements aside from the agreement of two or more people or entities to operate a business for profit. Each general partner is entitled to manage the enterprise and is jointly and severally liable for its debts and obligations.

There is no requirement that the partners execute a written partnership agreement (although it is strongly discouraged by the author) or register with a state agency. There are no other formalities required. This makes the general partnership the simplest type of business entity where there is more than one owner.

A general partnership is a disregarded entity for purposes of federal income tax. Profits and losses flow through to the partners. The partnership files an informational return only with the IRS.

Major Attributes: General Partnership

• Has some characteristics of a separate legal entity, i.e., can sue and be sued and hold property in its own name

• All general partners entitled to manage the enterprise

• Partnership profits, losses and distributions (including return of capital) are shared in proportion to the partners’ contributions, unless the partnership agreement provides otherwise

• Each general partner is jointly and severally liable for the debts and other obligations of the partnership

B. LIMITED PARTNERSHIP

A limited partnership is comprised of one or more “general” partners and one or more “limited” partners. The general partner or partners are responsible for managing the partnership and, like partners in a general partnership, are jointly and severally liable for all partnership debts and obligations. The general partner or partners need not be a natural person; a corporation, for example, may serve as the general partner.

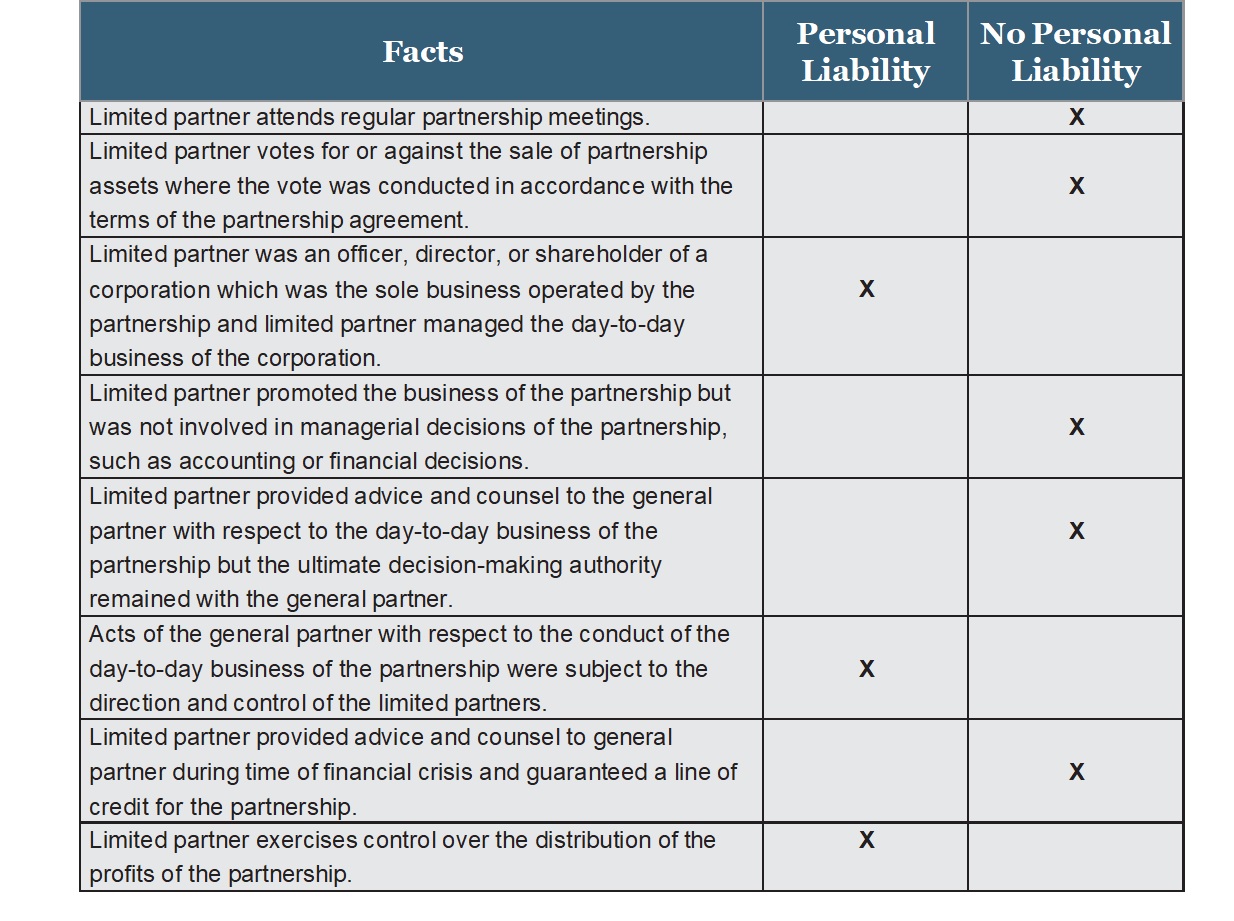

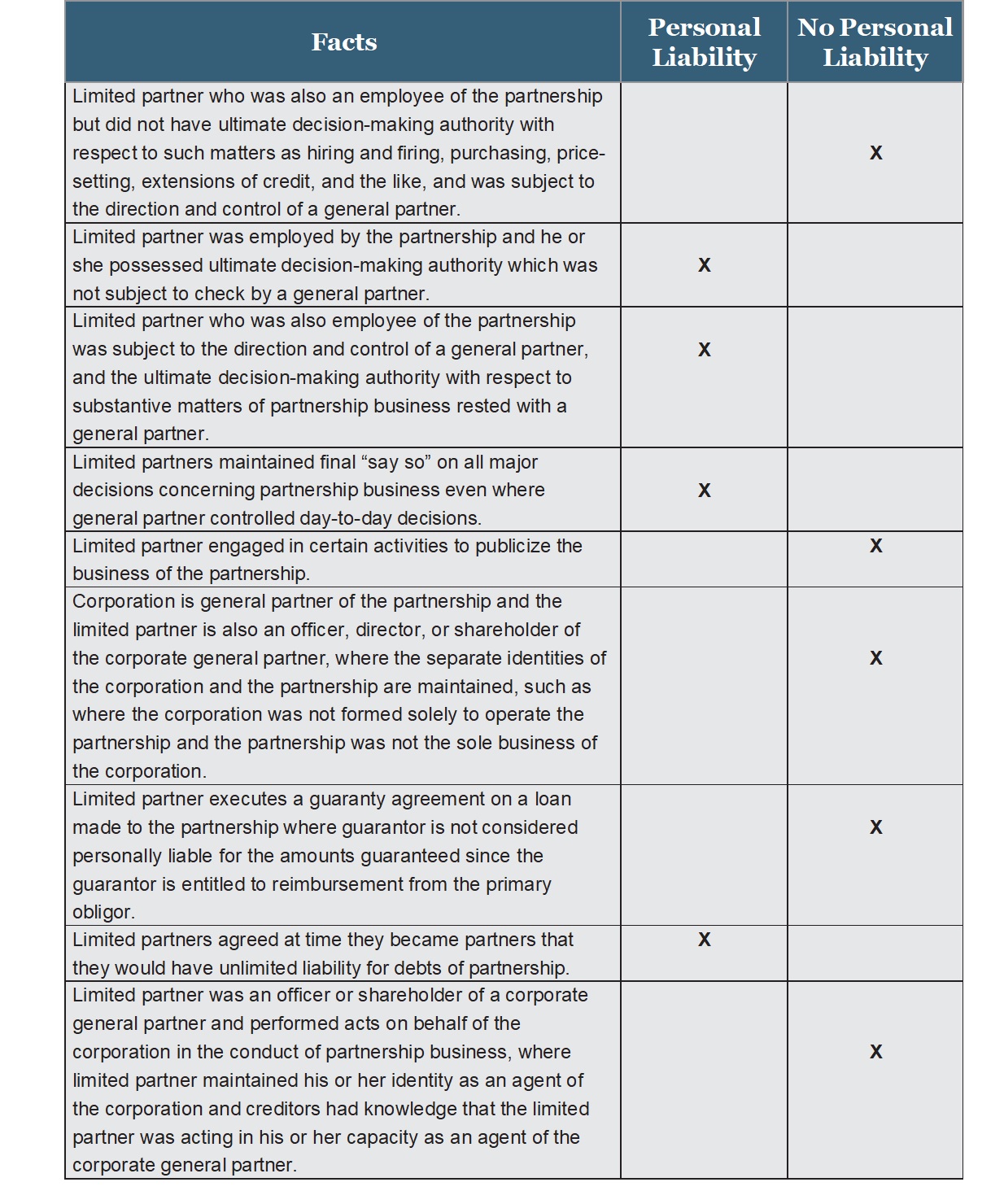

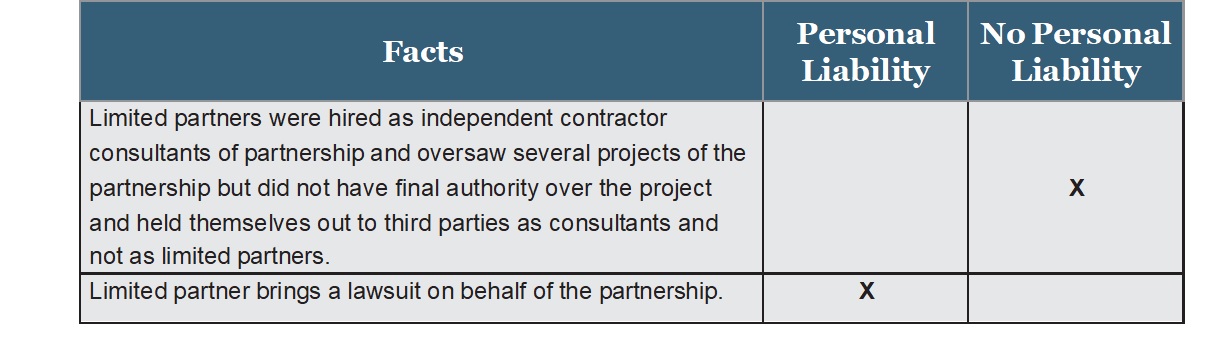

1. Passive Investors

Limited partners are passive investors who are not involved in management of the partnership and who, as a result, are not personally liable for the debts and obligations of the partnership beyond their capital contributions.

Every state has a body of law governing limited partnerships, many modeled after the Uniform Limited Partnership Act.

While not involved in day-to-day operations of the enterprise, limited partners are entitled to receive information, including an accounting, regarding the partnership and likewise have a right to inspect various partnership records.

2. Loss of Protection Against Personal Liability

Limited partners who become involved in the management of the partnership or involved in other ways, including being employed by the partnership, risk losing their limited liability status. As with limited liability companies, discussed later in this chapter, a limited partnership may have different classes of partners as set forth in a partnership agreement.

Major Attributes: Limited Partnership

• Comprised of one or more general partners and one or more limited partners

• General partner can be corporation or other entity; need not be natural person

• Limited partners are “passive” investors

• Limited liability status can be lost through active involvement in the enterprise

• Must file certificate of limited partnership with appropriate state agency; normally no other formalities are required, although a well drafted limited partnership agreement is critical to the successful operation of the business

• Limited partners entitled to accounting, inspection of records

Partnership profits, losses and distributions (including return of capital) are shared in proportion to the partners’ contributions, unless the partnership agreement provides otherwise.

3. Rights of Limited Partners

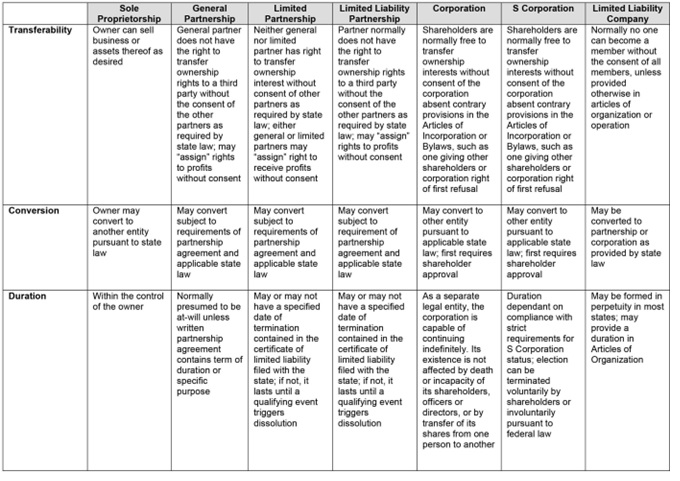

A limited partner has the right to assign his or her interest in whole or in part to a third person. However, such assignment merely transfers the right to receive distributions from the partnership; it does not entitle the transferee to become a partner unless provided in the partnership agreement or unless it is approved by all of the general partners.

Most states require a limited partnership to file a certificate of limited partnership with the appropriate state agency, normally the secretary of state. This formality is designed to give notice to prospective creditors of the limited liability status of the enterprise.

While a certificate is required, there is no legal requirement in most states that a limited partnership execute a written partnership agreement, although it is obviously advisable to do so.

The death, withdrawal, removal, incompetence, bankruptcy or dissolution of a general partner normally dissolves a limited partnership unless (1) the partnership agreement provides otherwise, or (2) all remaining general partners continue the business, or (3) where there is no remaining general partner, limited partners agree to continue the partnership according to the requirements of the applicable state law.

C. LIMITED LIABILITY PARTNERSHIP

A limited liability partnership is a hybrid of the limited partnership and must be registered as a limited liability partnership under the laws of the state of organization. Every state has its own technical requirements for formation, which normally include the appointment of an agent for receipt of service of process.

All of the partners in a limited liability partnership are typically entitled to limited liability status for the acts or omissions of the partnership – though not generally for his or her own acts or omissions. Again, state law varies considerably on this topic. Many states reserve limited liability partnership status for certain professional associations, for example, attorneys and certified public accountants.

IV. CORPORATIONS

The main characteristic of a corporation is that it is a separate legal entity with a life beyond that of its owners. A corporation is a creature of state law and is governed by the provisions of law in its state of organization (although it is obviously subject also to federal law, including the Internal Revenue Code).

Creating a corporation requires compliance with the corporate law of the state of organization. A corporation is the most complicated type of business to form and to operate due to the large number of formalities normally mandated. These include the filing of various documents with state agencies, the noticing and holding of meetings, and the maintenance of records. As a separate legal entity, a corporation may operate indefinitely. The death of a shareholder does not affect the legal status of a corporation.

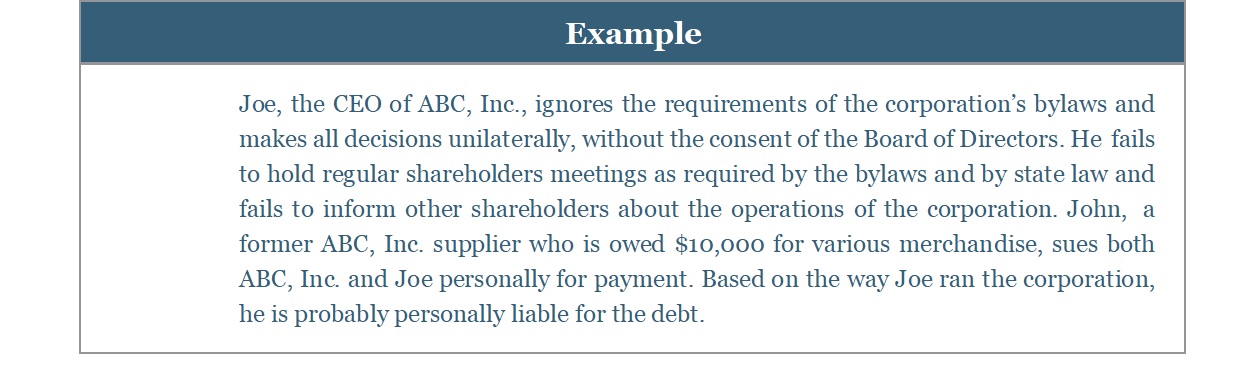

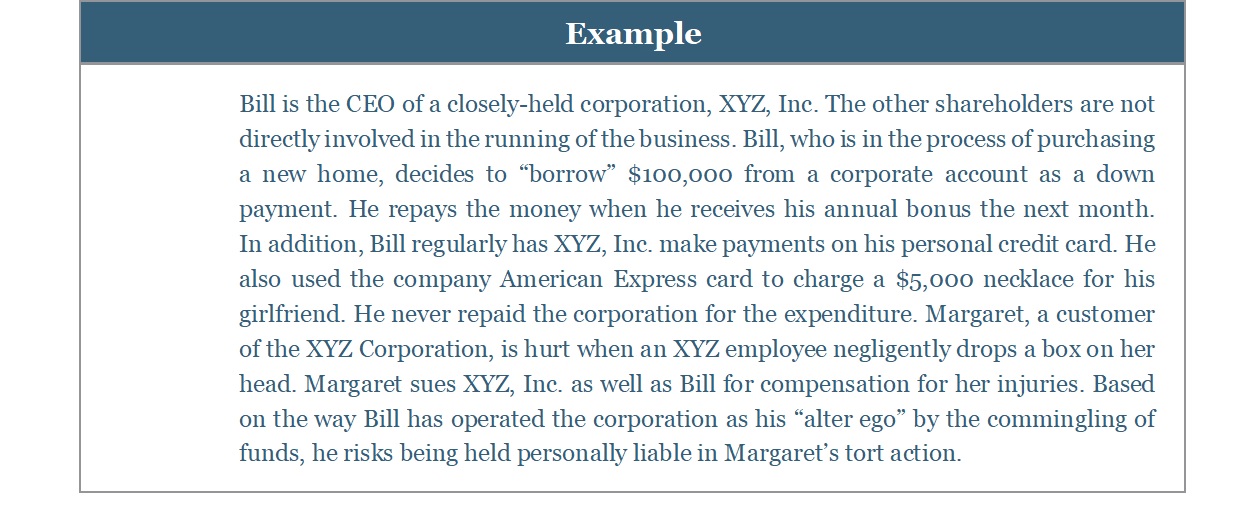

Because a corporation is a separate legal entity, it is responsible for its own debts. Shareholders, directors and officers are normally not legally responsible for corporate liabilities, and can only be held personally liable under one of the following situations (which will be explained in detail in Chapter 5):

• Where the shareholder, officer or director has personally guaranteed a corporate debt;

• Where a court finds that the individual has acted as the “alter ego” of the corporation and should therefore be held personally liable for a debt or other obligation; or

• Where such an individual has been determined to have violated certain laws, such as by authorizing corporate wrongdoing.

Major Attributes: Corporations

• A legal entity separate and apart from its owners

• Has power to act in any way allowed by applicable state law and as provided in its Articles of Incorporation

• May only appear in court through a licensed attorney

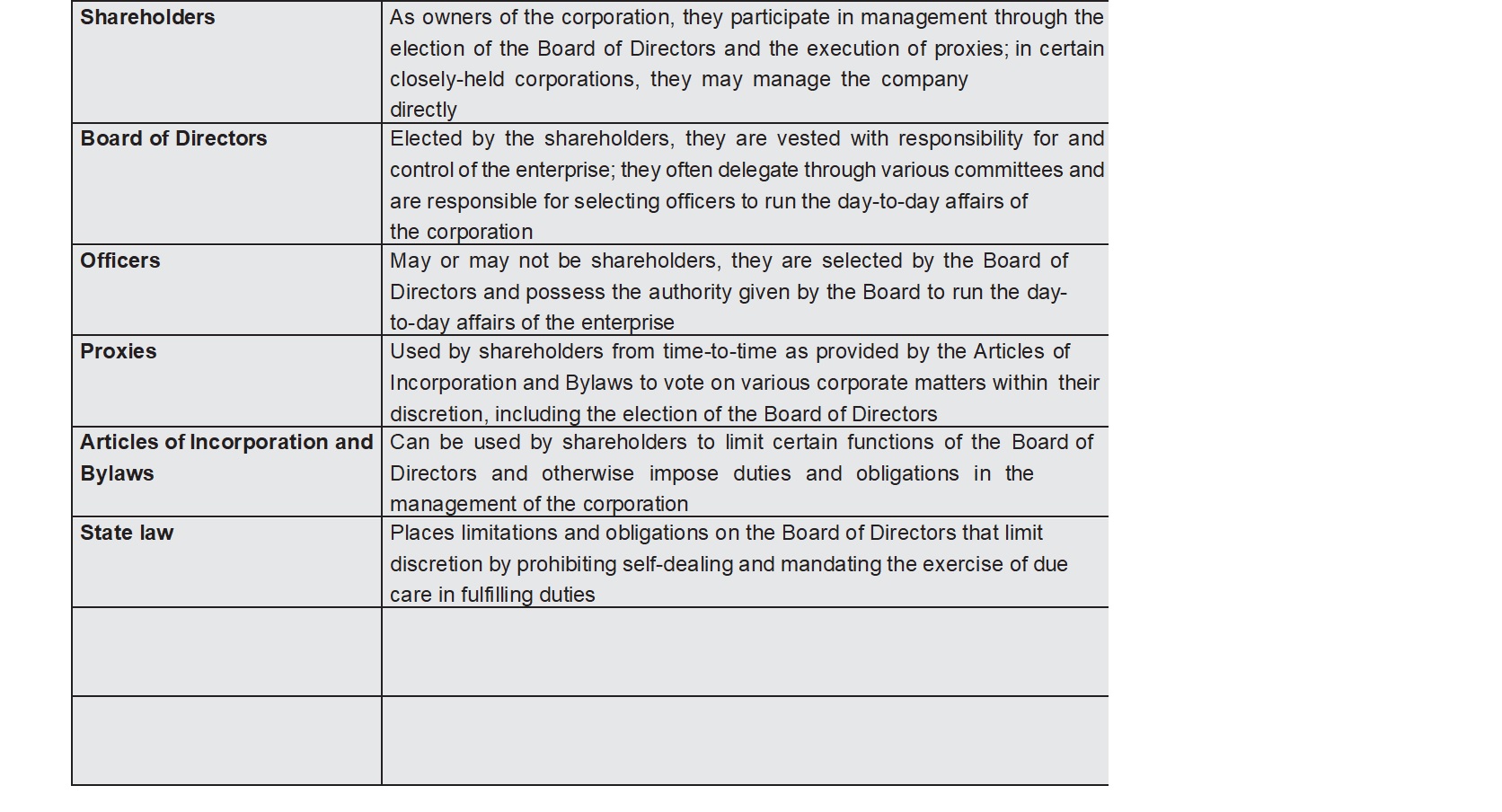

• Management and control are vested in the board of directors, elected by the shareholders of the corporation

• Shareholders, directors or officers of the corporation are normally not legally responsible for corporate liabilities

• Profits of the corporation are taxable by the corporation as well as shareholders when distributed via dividends

• Has an unlimited lifespan; not affected by the death of shareholders

Management and control of a corporation is vested in its board of directors, which is elected by the shareholders of the corporation. The board of directors normally appoints officers to run the day-to-day business of the corporation. Such officers may or may not also be shareholders (although as a practical matter they usually are).

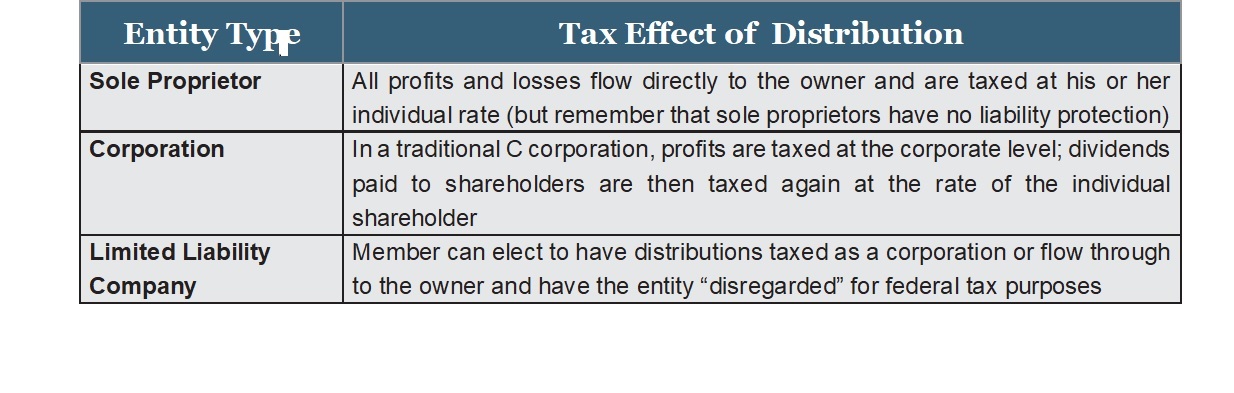

The profit of a corporation is taxed to both the corporation and to the shareholders when it is distributed as dividends. This so-called “double taxation” is often mentioned as a disadvantage of corporate status.

V. S CORPORATION

Originally created in 1958, an S corporation combines the limited liability of a classic C corporation with tax treatment similar to a partnership. S corporations are treated as corporations under state law. For purposes of federal income tax, however, S corporations are treated as partnerships. This means that the income, deductions, and tax credits of an S corporation flow through to the shareholders; income is taxed at the shareholder level and not at the corporate level. State taxation of S corporations varies. Some states, for example, treat an S corporation as a C corporation, and therefore impose an income or franchise tax.

The shareholders of a C corporation must “elect” to become an S corporation. There are a number of important restrictions placed on S corporations, including a cap on the number of shareholders (currently 100) and a requirement that there be only one class of stock. Failure to comply with the many IRS requirements will cause an S corporation to lose its status.

Major Attributes: S Corporation

• Shareholders enjoy same limited liability as shareholders of C corporation

• Treated as partnerships for purposes of federal taxation

• State taxation of S corporations varies

• Strict formalities for qualification and maintenance of tax status

• Maximum of 100 owners; only one class of stock allowed

A corporation will be eligible to be an S corporation if it:

• Is a domestic corporation;

• Has no more than 100 shareholders;

• Has as its shareholders only individuals, estates, or certain tax-exempt organizations;

• Has no nonresident aliens as shareholders;

• Has only one class of stock; or

• Is not an “ineligible” corporation as defined in federal law.

A corporation is ineligible to be an S corporation if it is:

• A financial institution that uses the reserve method of accounting for bad debts;

• An insurance company; or

• A corporation for which an election has been made to claim a possession tax credit.

VI. LIMITED LIABILITY COMPANY

Limited liability companies have been a popular business form in European and other countries for decades. The first state in the United States to recognize limited liability companies was Wyoming, which allowed them beginning in 1977. Florida followed suit in 1982. It was not until the IRS agreed in a 1988 Revenue Ruling (Rev. Rul. 88-76) to treat LLCs as partnerships for tax purposes that many businesses decided to utilize this form of entity. This triggered legislative activity throughout the nation and each state sought to give its businesses the opportunity to utilize this form. By 1996, all 50 states and the District of Columbia had passed laws recognizing limited liability companies and creating statutory frameworks covering their formation, operation and dissolution.

Although recognized by the IRS for tax purposes, limited liability companies are purely creatures of state law. A limited liability company is an entity formed by following the procedures required in the state of operation. The owners of an LLC are generally referred to as “members”.

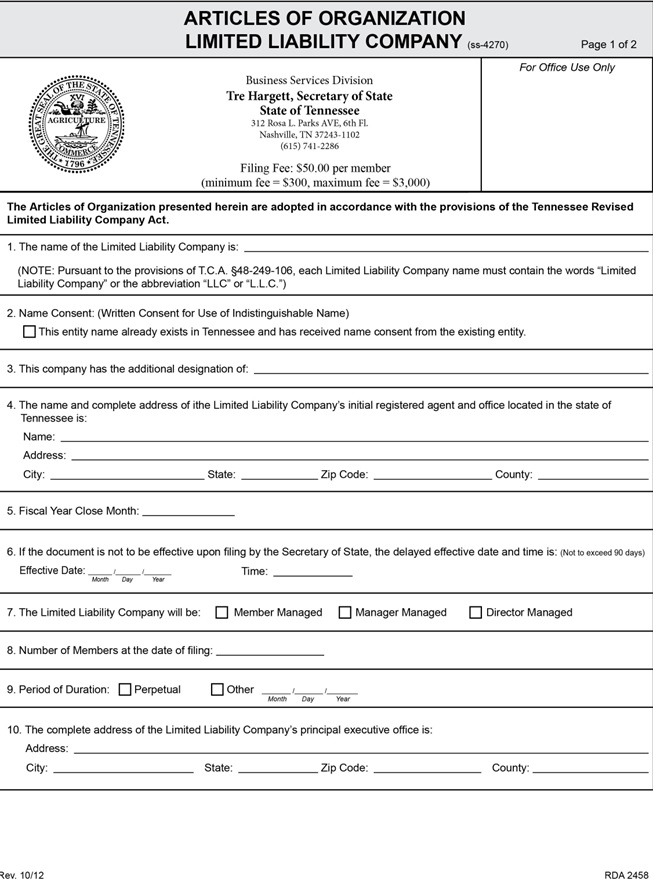

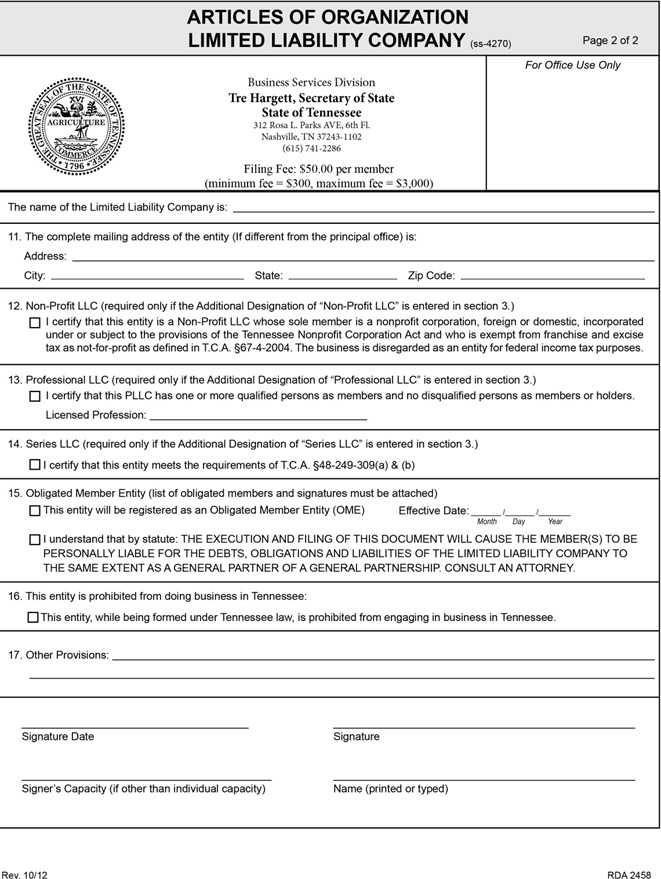

In most states, forming an LLC requires the preparation of only one document, the so-called Articles of Organization, which are filed with the Secretary of State or other designated state agency. This document, which is described in detail later in these materials, is usually brief and sets forth general information about the company, including its name, address, agent for service of process, term, and whether it will be run by the members or managers appointed by the members. Every state has detailed rules for what must be contained in this document and generally also offers a fill-in-the blank form that meets its statutory requirements.

Major Attributes: Limited Liability Company

• Multi-member LLC may elect to be taxed as corporation or partnership

• Members normally have no personal liability for debts and obligations of the company

• All states allow single-member companies; there is no maximum number of owners

• More flexibility in management than corporation

• Few if any formalities required by state law

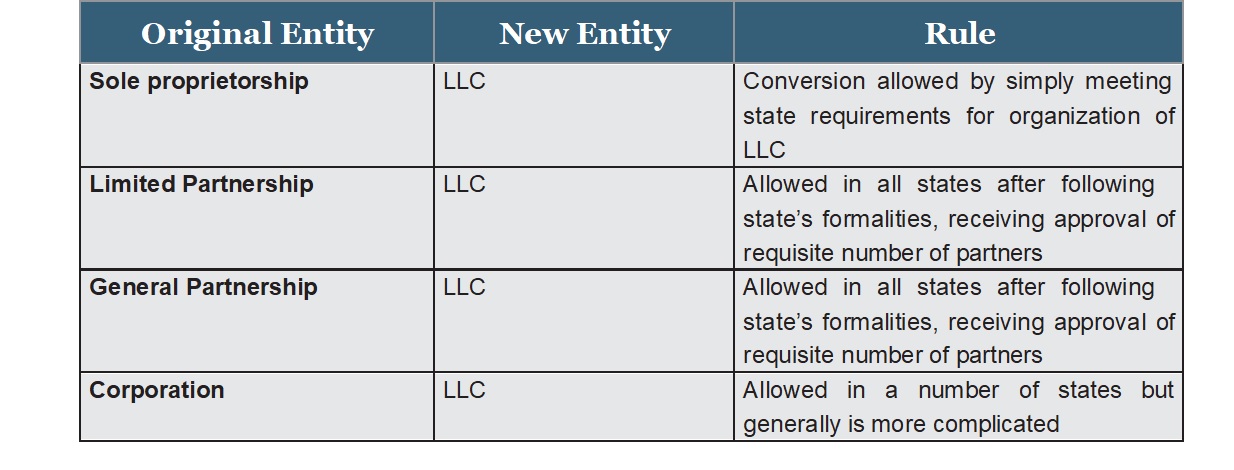

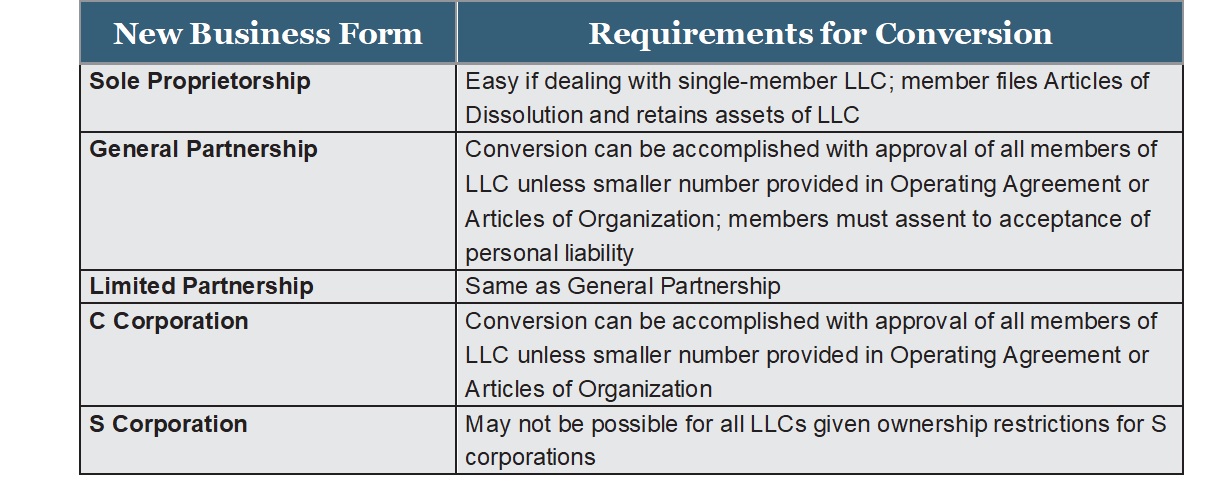

• Most states allow easy conversion to other business forms

• May not engage in certain businesses, including banking and insurance, in most states

• Most states expressly allow professional LLCs

In several states, LLCs are also required to file with the state an operating agreement, which, similar to a partnership agreement, provides a blueprint for how the LLC will be run, the financial obligations of the members, and how profits and losses will be divided. As a practical matter, almost every LLC will want to have a well-drafted operating agreement whether or not it is required. To the extent an operating agreement does not exist or is silent on a particular issue, courts will resolve disputes by referring to each state’s default statutory provisions governing operation of limited liability companies.

An LLC may be classified for Federal income tax purposes as either a partnership or a corporation. A domestic LLC with at least two members is automatically classified as a partnership for Federal income tax purposes unless it elects to be treated as a corporation. This is done by filing IRS Form 8832.

Unlike a partnership, none of the members of an LLC are personally liable for its debts. Practically, an LLC operates like a limited partnership without the requirement for a general partner. Unlike an S corporation, an LLC has no limits on the number of shareholders, classes of stock, or type of shareholders.

Because in most cases losses pass through to the members of an LLC, an LLC can be attractive to corporate investors and wealthy individuals. Other advantages to choosing this business form include:

• Limited liability for all owners;

• Flexibility in selecting a management structure; and

• Limited formalities, such as meetings and recordkeeping.

CHAPTER 2: FORMATION OF BUSINESS ENTITIES

CHAPTER OBJECTIVE:

After completing this chapter, you should be able to:

• Recognize the requirements for the formation of various types of entities.

I. INTRODUCTION

The first step after choosing the desired business entity is its formation. The simplest business to form is obviously the sole proprietorship. It has no legal existence beyond that of the individual owner. There is no government license required to operate as a sole proprietor, no paperwork to file with the Secretary of State and no other special requirements beyond any local rules that might, for example, mandate that the owner obtain a business license.

The most complex business entity, both in terms of formation and operation, is the corporation. That is because the corporation literally has a life of its own, and, as such, its organizers must go through the necessary steps to “give birth” to that entity and then to nourish it. Formalities of formation include filing various documents with the appropriate state agency, normally the Secretary of State.

In between the sole proprietorship and the corporation lies the traditional partnership and several hybrids of the partnership – the limited partnership and the limited liability partnership. Finally, there is the limited liability company, a construct of American law that is a hybrid of the traditional partnership and a corporation in which the owners, called members, have the benefits of partnership tax treatment and the protection of limited liability traditionally reserved for corporate shareholders.

This chapter will provide an overview of the major requirements for business entity formation. Keep in mind that as with most other laws governing business entities, they are largely creatures of state law. This means that each state has its own statutes and common law governing everything from formation to dissolution. One common link between the laws of many states are the so-called Uniform Laws. Uniform laws are promulgated by the National Conference of Commissioners on Uniform State Laws, whose purpose is to compose sample, non-binding laws that the authors believe are the best treatment of a particular legal subject. They are often very persuasive in influencing state laws; over the years many have been adopted in whole by various states.

There are two uniform laws that govern general partnerships. The Uniform Partnership Act (“UPA”) was initially promulgated in 1914; the Revised Uniform Partnership Act (“RUPA”) was initially promulgated in 1992 and amended in 1993, 1994, 1996 and 1997. RUPA is the basis of the general partnership statutes in a majority of the states.

There are also two model acts governing limited partnerships: the Uniform Limited Partnership Act (“ULPA”) initially promulgated in 1917; and the Revised Uniform Limited Partnership Act initially promulgated in 1976 and amended in 1985 and 2001.

There are also two model acts governing limited liability companies: the Uniform Limited Liability Company Act (“ULLCA”) was promulgated in 1995; and the Revised Uniform Limited Liability Company Act (“ULLCA”) was promulgated in 2006, and amended in 2011 and 2013.

Provisions from each of the above uniform laws will be mentioned from time-to-time as illustrative of state law treatment of various issues. Remember, however, that before providing any advice to clients to check the specific laws of the state in which you are practicing, as these laws are illustrative and may not actually reflect the law of the state in which you reside.

II. GENERAL PARTNERSHIP

A. COMMON LAW FORMULATION

Aside from the sole proprietorship, the general partnership is the easiest business entity to form. There are no legal requirements aside from the agreement of two or more people or entities1 to operate a business for profit. Traditionally, this was done without so much as a piece of paper. The partners merely shared the work and divided the profits. If there were losses, those were shared as well. To determine whether a partnership exists, courts must simply ascertain the intention of the parties, and in the absence of a written agreement, the requisite intention is that which is deducible from the parties’ actions. The agreement may be either expressed or implied.

1. We tend to think of people as forming partnerships. However, two companies, i.e., corporations or partnerships, could also elect to form a partnership, either general or limited.

The Revised Uniform Partnership Act (“RUPA”) § 101 defines a partnership as “an association of two or more persons to carry on as co-owners of a business for profit.” Pursuant to RUPA § 202, “the association of two or more persons to carry on as co-owners of a business for profit forms a partnership, whether or not the persons intend to form a partnership.”

In determining whether a partnership is formed, RUPA further provides that the following rules apply:

• Joint tenancy, tenancy in common, tenancy by the entireties, joint property, common property, or part ownership does not by itself establish a partnership, even if the co- owners share profits made by the use of the property;

• The sharing of gross returns does not by itself establish a partnership, even if the persons sharing them have a joint or common right or interest in property from which the returns are derived; and

• A person who receives a share of the profits of a business is presumed to be a partner in the business, unless the profits were received in payment:

- of a debt by installments or otherwise;

- for services as an independent contractor or of wages or other compensation to an employee;

- of rent;

- of an annuity or other retirement or health benefit to a beneficiary, representative, or designee of a deceased or retired partner;

- of interest or other charge on a loan, even if the amount of payment varies with the profits of the business, including a direct or indirect present or future ownership of the collateral, or rights to income, proceeds, or increase in value derived from the collateral; or for the sale of the goodwill of a business or other property by installments or otherwise.

Relationships that are called “joint ventures” are partnerships if they otherwise fit the definition of a partnership. A joint venture is normally a business that is formed for the purpose of a particular transaction. A common use is for the development of real estate. When the real estate is developed, the joint venture is normally dissolved.

An association is not classified as a partnership, however, simply because it is called a “joint venture.” An unincorporated nonprofit organization is not a partnership under RUPA, even if it qualifies as a business, because it is not a “for profit” organization.

Courts have commonly broken the concept of a partnership down into the following four elements: (1) community of interest in venture, (2) agreement to share profits, (3) agreement to share losses, and (4) mutual right of control or management of enterprise. As a result, the actual terminology used by the parties to describe their business relationship is of little import in determining whether a partnership exists.

By definition – and unless otherwise provided – a partnership is a general partnership and all partners are general partners. Compliance with various state laws is required to create a different type of partnership, including a limited partnership or a limited liability partnership. Those concepts are discussed later.

B. IRS CLASSIFICATION OF PARTNERSHIP

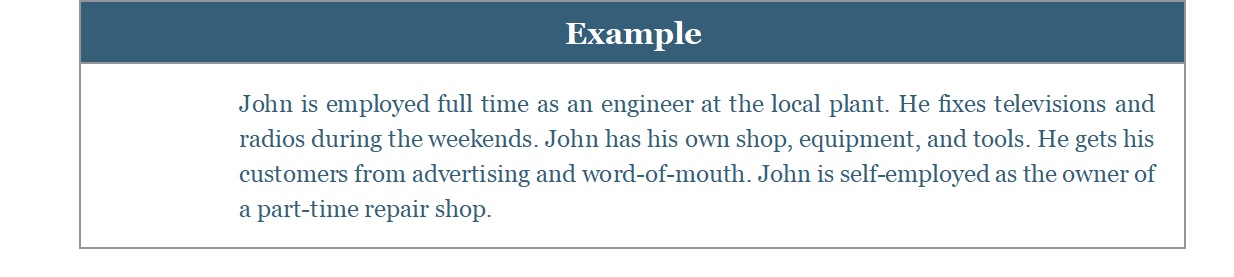

The fact that a business association is considered a partnership for state law purposes does not necessarily mean it will be recognized as such for IRS purposes. Due to the significance of partnership classification for purposes of federal income tax liabilities, it is important to understand how the IRS classifies business entities as partnerships.

An unincorporated organization with two or more members is generally classified as a partnership for federal tax purposes if its members carry on a trade, business, financial operation, or venture and divide its profits. However, a joint undertaking merely to share expenses is not a partnership. For example, co- ownership of property maintained and rented or leased is not a partnership unless the co-owners provide services to the tenants.

The IRS rules used to determine whether an organization is classified as a partnership changed for organizations formed after 1996.

1. Organizations Formed After 1996.

An organization formed after 1996 is classified as a partnership for federal tax purposes if it has two or more members and it is none of the following:

• An organization formed under a federal or state law that refers to it as incorporated or as a corporation, body corporate, or body politic;

• An organization formed under a state law that refers to it as a joint-stock company or joint-stock association;

• An insurance company;

• Certain banks;

• An organization wholly owned by a state or local government;

• An organization specifically required to be taxed as a corporation by the Internal Revenue Code (for example, certain publicly traded partnerships);

• Certain foreign organizations;

• A tax-exempt organization;

• A real estate investment trust;

• An organization classified as a trust under section 301.7701-4 of the regulations or otherwise subject to special treatment under the Internal Revenue Code; or

• Any other organization that elects to be classified as a corporation by filing Form 8832.

2. Family Partnership

Members of a family can be partners. However, family members (or any other person) will be recognized as partners only if one of the following requirements are met:

• If capital is a material income-producing factor, they acquired their capital interest in a bona fide transaction (even if by gift or purchase from another family member), actually own the partnership interest, and actually control the interest; or

• If capital is not a material income-producing factor, they joined together in good faith to conduct a business. They agreed that contributions of each entitle them to a share in the profits, and some capital or service has been (or is) provided by each partner.\

a. Capital Interest – A capital interest in a partnership is an interest in its assets that is distributable to the owner of the interest in either of the following situations:

• The owner withdraws from the partnership; or

• The partnership liquidates.

The mere right to share in earnings and profits is not a capital interest in the partnership.

b. Gift of Capital Interest

If a family member (or any other person) receives a gift of a capital interest in a partnership in which capital is a material income-producing factor, the donee’s distributive share of partnership income is subject to both of the following restrictions.

• It must be figured by reducing the partnership income by reasonable compensation for services the donor renders to the partnership; and

• The donee’s distributive share of partnership income attributable to donated capital must not be proportionately greater than the donor’s distributive share attributable to the donor’s capital.

For purposes of determining a partner’s distributive share, an interest purchased by one family member from another family member is considered a gift from the seller. The fair market value of the purchased interest is considered donated capital. For this purpose, members of a family include only spouses, ancestors, and lineal descendants (or a trust for the primary benefit of those persons).

3. Husband-wife Partnership

If spouses carry on a business together and share in the profits and losses, they may be partners whether or not they have a formal partnership agreement. If so, they should report income or loss from the business on Form 1065 rather than on Form 1040.

Each spouse should carry his or her share of the partnership income or loss from Schedule K-1 (Form 1065) to their joint or separate Form(s) 1040. Each spouse should include his or her respective share of self-employment income on a separate Schedule SE (Form 1040), Self-Employment Tax. This generally does not increase the total tax on the return, but it does give each spouse credit for social security earnings on which retirement benefits are based.

III. LIMITED PARTNERSHIPS

The formation of a limited partnership is regulated by statute in each state. It normally requires more formality than a general partnership. The formation of a limited partnership must be evidenced by a written agreement. It also requires the filing of a certificate of limited partnership with the appropriate state agency. Many states also require formal public notice of the formation of the limited partnership as well as payment of a fee.

The procedure for formation of a partnership under the Uniform Limited Partnership Act entails the execution of a certificate containing certain prescribed information, and the filing and publication of such certificate in accordance with statutory requirements before the limited partnership begins to do business. Thus, a limited partnership cannot normally be created orally.

In order to form a limited partnership in California, the general partners must execute, acknowledge, and file a Certificate of Limited Partnership (LP-1) with the Secretary of State. In addition, before or after the filing of a certificate, the partners must have entered into a partnership agreement. The filing fee for filing either a Certificate of Limited Partnership (LP-1) or an Application for Registration (LP-5) is $70.00.

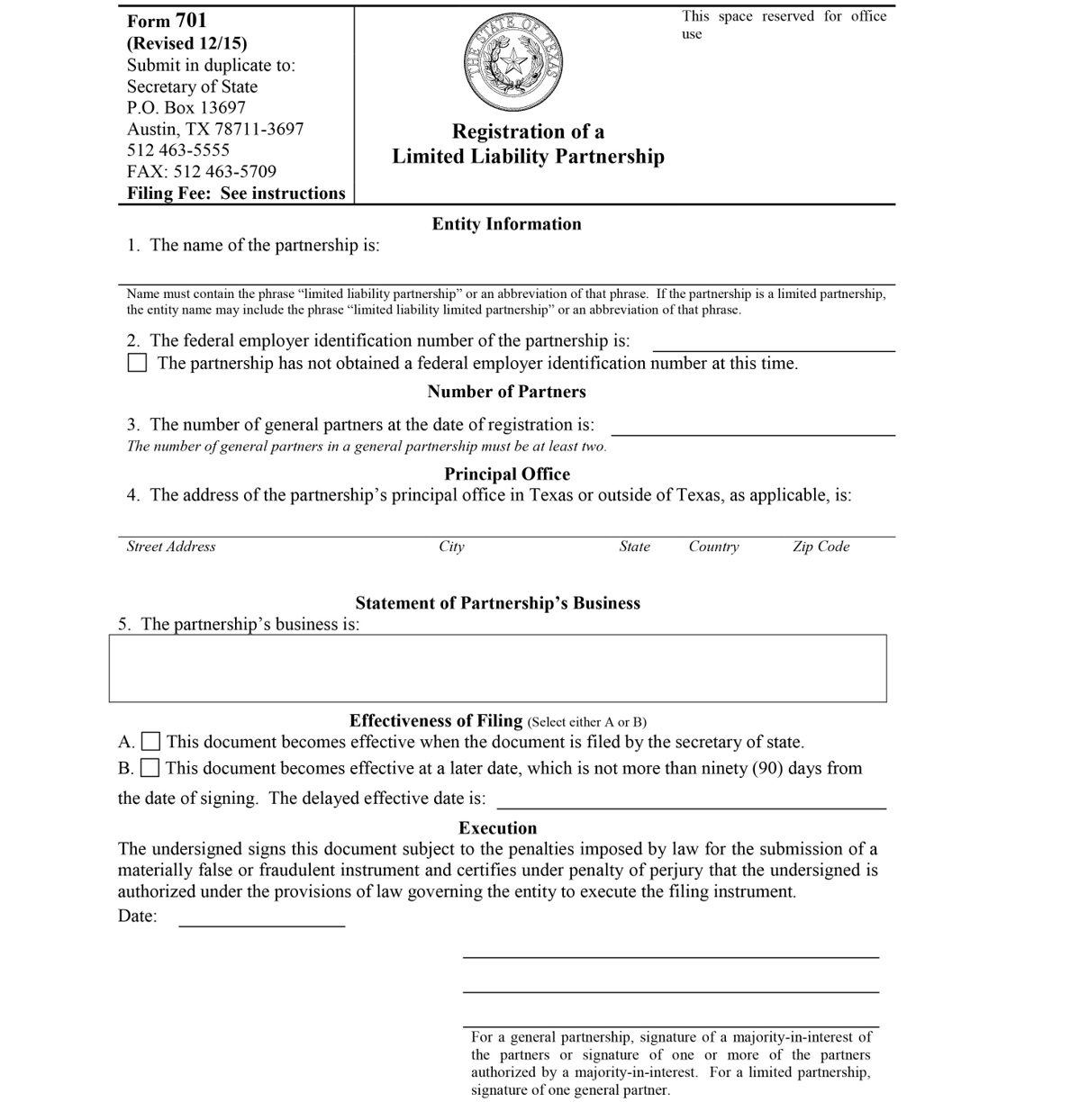

Also note that the Revised Uniform Limited Partnership Act (RULPA) and state statutes based on RULPA contain name requirements. Typically, the name of a limited partnership must contain the words “limited partnership” or some abbreviation thereof (and often times as the last words or letters in the name). Also, the name of a limited partnership may not be the same as, or deceptively similar to, the name of another entity organized or doing business in the state of formation. Texas, for example, requires the filing of the following certificate of formation of a limited partnership with the Secretary of State:

IV. LIMITED LIABILITY PARTNERSHIP

The limited liability partnership is a concept now recognized by every state. Each state has its own version of this entity and its own requirements for formation.

In Texas, for example, the law requires every proposed limited liability partnership to file an application with the Secretary of State stating its name, the address of its principal office, the number of partners and a brief statement of its business. The application must be signed by or on behalf of a majority in interest of its partners and must be accompanied by a fee of $200 for each partner. The registration by the Secretary of State is for one year, unless voluntarily withdrawn sooner, and may be renewed.

Texas law further requires the name of the registered limited liability partnership must end with the words “limited liability partnership” or “LLP.”

The objective of the limited liability partnership is basically to provide that a partner in such partnership is not liable individually for partnership liabilities arising from errors, omissions, negligence, incompetence, or malfeasance in the course of the partnership business by another partner or a representative of the partnership not working under the supervision or direction of the first partner at the time, unless the first partner was directly involved in the specific activity or had notice or knowledge of the errors, omissions, negligence, incompetence or malfeasance. All partners remain jointly and severally liable for all other debts and obligations of the partnership, and the partnership assets are liable for all debts and obligations of the firm. These issues will be discussed in more detail in Chapter 5, Liability of Owners.

Most states require a limited liability partnership to renew its status annually. Many states require the registration to contain the name of each partner. Other states, including Alabama, do not require the name of each partner to be disclosed. At a minimum, however, every state requires the partnership to appoint an in-state agent for receipt of service of process.

In many jurisdictions, the limited liability partnership is available only to so-called “professional” partnerships, e.g., accountants, attorneys and physicians. New York law, for example, § 121-1500, provides, in part:

(a) Notwithstanding the education law or any other provision of law, (i) a partnership without limited partners each of whose partners is a professional authorized by law to render a professional service within this state and who is or has been engaged in the practice of such profession in such partnership or a predecessor entity, or will engage in the practice of such profession in the registered limited liability partnership within thirty days of the date of the effectiveness of the registration provided for in this subdivision or a partnership without limited partners each of whose partners is a professional, at least one of whom is authorized by law to render a professional service within this state and who is or has been engaged in the practice of such profession in such partnership or a predecessor entity, or will engage in the practice of such profession in the registered limited liability partnership within thirty days of the date of the effectiveness of the registration provided for in this subdivision, (ii) a partnership without limited partners authorized by, or holding a license, certificate, registration or permit issued by the licensing authority pursuant to the education law to render a professional service within this state, which renders or intends to render professional services within this state, or (iii) a related limited liability partnership may register as a registered limited liability partnership by filing with the department of state.Each partner in a registered limited liability partnership must be duly licensed in the profession.

Many states require limited liability partnerships to maintain insurance to cover potential liabilities of the partnership. For example, California Corporations Code Section 16956 provides, in part:

(1) For claims based upon acts, errors, or omissions arising out of the practice of public accountancy, a registered limited liability partnership or foreign limited liability partnership providing accountancy services shall comply with one, or pursuant to subdivision (b) some combination, of the following:

(A) Maintaining a policy or policies of insurance against liability imposed on or against it by law for damages arising out of claims; however, the total aggregate limit of liability under the policy or policies of insurance for partnerships with five or fewer licensed persons shall not be less than one million dollars ($1,000,000), and for partnerships with more than five licensees rendering professional services on behalf of the partnership, an additional one hundred thousand dollars ($100,000) of insurance shall be obtained for each additional licensee; however, the maximum amount of insurance is not required to exceed five million dollars ($5,000,000) in any one designated period, less amounts paid in defending, settling, or discharging claims as set forth in this subparagraph. The policy or policies may be issued on a claims-made or occurrence basis, and shall cover: (i) in the case of a claims-made policy, claims initially asserted in the designated period, and (ii) in the case of an occurrence policy, occurrences during the designated period. For purposes of this subparagraph, “designated period” means a policy year or any other period designated in the policy that is not greater than 12 months. The impairment or exhaustion of the aggregate limit of liability by amounts paid under the policy in connection with the settlement, discharge, or defense of claims applicable to a designated period shall not require the partnership to acquire additional insurance coverage for that designated period. The policy or policies of insurance may be in a form reasonably available in the commercial insurance market and may be subject to those terms, conditions, exclusions, and endorsements that are typically contained in those policies. A policy or policies of insurance maintained pursuant to this subparagraph may be subject to a deductible or self-insured retention.

Upon the dissolution and winding up of the partnership, the partnership shall, with respect to any insurance policy or policies then maintained pursuant to this subparagraph, maintain or obtain an extended reporting period endorsement or equivalent provision in the maximum total aggregate limit of liability required to comply with this subparagraph for a minimum of three years if reasonably available from the insurer.

(B) Maintaining in trust or bank escrow, cash, bank certificates of deposit, United States Treasury obligations, bank letters of credit, or bonds of insurance or surety companies as security for payment of liabilities imposed by law for damages arising out of all claims; however, the maximum amount of security for partnerships with five or fewer licensed persons shall not be less than one million dollars ($1,000,000), and for partnerships with more than five licensees rendering professional services on behalf of the partnership, an additional one hundred thousand dollars ($100,000) of security shall be obtained for each additional licensee; however, the maximum amount of security is not required to exceed five million dollars ($5,000,000). The partnership remains in compliance with this section during a calendar year notwithstanding amounts paid during that calendar year from the accounts, funds, Treasury obligations, letters of credit, or bonds in defending, settling, or discharging claims of the type described in this paragraph, provided that the amount of those accounts, funds, Treasury obligations, letters of credit, or bonds was at least the amount specified in the preceding sentence as of the first business day of that calendar year. Notwithstanding the pendency of other claims against the partnership, a registered limited liability partnership or foreign limited liability partnership shall be deemed to be in compliance with this subparagraph as to a claim if within 30 days after the time that a claim is initially asserted through service of a summons, complaint, or comparable pleading in a judicial or administrative proceeding, the partnership has provided the required amount of security by designating and segregating funds in compliance with the requirements of this subparagraph.

(C) Unless the partnership has satisfied subparagraph (D), each partner of a registered limited liability partnership or foreign limited liability partnership providing accountancy services, by virtue of that person’s status as a partner, thereby automatically guarantees payment of the difference between the maximum amount of security required for the partnership by this paragraph and the security otherwise provided in accordance with subparagraphs (A) and (B), provided that the aggregate amount paid by all partners under these guarantees shall not exceed the difference. Neither withdrawal by a partner nor the dissolution and winding up of the partnership shall affect the rights or obligations of a partner arising prior to withdrawal or dissolution and winding up, and the guarantee provided for in this subparagraph shall apply only to conduct that occurred prior to the withdrawal or dissolution and winding up. Nothing contained in this subparagraph shall affect or impair the rights or obligations of the partners among themselves, or the partnership, including, but not limited to, rights of contribution, subrogation, or indemnification.

(D) Confirming, pursuant to the procedure in subdivision (c), that, as of the most recently completed fiscal year of the partnership, it had a net worth equal to or exceeding ten million dollars ($10,000,000).

North Carolina, among other states, also requires a limited liability partnership to file an annual report with the Secretary of State (§ 59-84.4). The report must set forth the following:

1. The name of the registered limited liability partnership or foreign limited liability partnership and the state or country under whose law it is formed;

2. The street address, and the mailing address if different from the street address, of the registered office, the county in which the registered office is located, and the name of its registered agent at that office in this State, and a statement of any change of the registered office or registered agent, or both;

3. The street address and telephone number of its principal office;

4. A brief description of the nature of its business; and

5. The fiscal year end of the partnership.

If the information contained in the most recently filed annual report has not changed, a certification to that effect may be made instead of setting forth the information required by subdivisions (2) through (4) of this subsection. The Secretary of State shall make available the form required to file an annual report.

V. LIMITED LIABILITY COMPANIES

The limited liability company, while recognized by the Internal Revenue Service for tax purposes, is still a product of applicable state law. Thus, in determining the mechanism required to form a limited liability company, organizers must examine the law of the state in which they wish to operate. All 50 states and the District of Columbia recognize limited liability companies and have statutory schemes governing their creation and operation. By way of illustration, we will examine the formation requirements in California and compare and contrast its requirements to other states where appropriate.

The first step in every state is the filing of Articles of Organization with the Secretary of State (this is similar to the requirements for the formation of a corporation, which begins with the filing of Articles of Incorporation, also with the Secretary of State). Persons organizing the limited liability company may be, but are not required to be, members of the entity. This is generally true of all states. In addition to Articles of Organization, California expressly requires limited liability companies to execute an Operating Agreement. Although most states do not have such a requirement, as a practical matter, almost all entities will need such a document to govern their affairs. The Operating Agreement and its importance will be discussed in connection with other topics.

While an LLC can be formed in many states solely through the filing of Articles of Organization, a few states, including Arizona, Nebraska, and New York, require the extra step of public notice advertising. The purpose of public notice advertising is to alert members of the public who might engage in business with the entity that it will be operating as a limited liability company. In New York, for example, the advertisement must be published in two different newspapers in which the business will operate weekly for six successive weeks.

Public notice advertisements must be published in a newspaper of general circulation in the county in which the business will be operated. A newspaper of general circulation is one which has been adjudicated as such by the local courts. Since not all newspapers meet this requirement, organizers need to be careful that the newspaper they choose meets the legal requirements. As always, look to the statute of each state to determine what, if any, public notice advertisement is required.

Each state, including California, has specific requirements for the type of information that must be included in the Articles of Organization. Most, if not all, states make the process simple by providing fill-in-the blank sample forms. Each state also spells out in statute the specific information that must be included in the Articles of Organization, as well as the information it has the option to include.

Pursuant to Code of Corporations Section 17051, California requires the articles to include (among other items), all of the following:

• The name of the limited liability company;

• This following statement: “The purpose of the limited liability company is to engage in any lawful act or activity for which a limited liability company may be organized under the Beverly-Killea Limited Liability Company Act”;

• The name and address of the initial agent for service of process on the limited liability company who meets certain statutory qualifications or, in the alternative, a designated corporate agent;

• If the limited liability company is to be managed by one or more managers and not by all its members, the articles of organization must contain a statement to that effect. Neither the names nor numbers of the managers need to be included; and

• If the limited liability company is to be managed by only one manager, the articles of organization shall contain a statement to that effect.

California, like many other states, does not require the articles to set forth any of specific powers of a limited liability company. California also provides that, at their election, organizers may include any other information not specifically prohibited by law, including the following:

• A provision limiting or restricting the business in which the limited liability company may engage or the powers that the limited liability company may exercise or both;

• Provisions governing the admission of members to the limited liability company;

• The time at which the limited liability company is to dissolve;

• Any events that will cause a dissolution of the limited liability company;

• A statement of whether there are limitations on the authority of managers or members to bind the limited liability company, and, if so, what the limitations are; and

• The names of the managers of the limited liability company.

Other information can be included, including provisions governing the admission of members into the limited liability company, at the election of the organizers.

Remember also that many states have different requirements, including different forms, that must be used for professional limited liability companies.

VI. CORPORATIONS

Like the other business entities discussed above, corporations are creatures of state law. This section will focus on California law as an example of how state law governs corporate creation.

The first step in creating a corporation is the filing of Articles of Incorporation with the Secretary of State. In addition, every domestic stock corporation in California is required to file a Statement of Information – Domestic Stock Corporation (Form SI-200 C or Form SI-200 N/C) with the Secretary of State, within 90 days after filing of its original Articles of Incorporation, and annually thereafter during the applicable filing period (statutory filing provisions are found in California Corporations Code § 1502).

The applicable filing period for a domestic stock corporation is the end of the calendar month during which its original Articles of Incorporation were filed and the immediately preceding five calendar months. If the name and/or address of the agent for service of process have changed, a corporation must file a complete statement. A corporation is required to file a statement even though it may not be actively engaged in business at the time this statement is due.

Every domestic stock corporation that is a “publicly traded company” must also file a Corporate Disclosure Statement with the required Statement of Information and a copy of the latest report prepared for the corporation by the independent auditor. “Publicly traded company” means a company with securities that are either listed or admitted to trading on a national or foreign exchange, or is the subject of two-way quotations, such as both bid and asked prices, that are regularly published by one or more broker-dealers in the National Daily Quotation Service or a similar service.

Changes to the information contained in the last filed Statement of Information or Corporate Disclosure Statement can be made any time outside of the applicable filing period by filing a complete Statement of Information and, if applicable, a complete Corporate Disclosure Statement. If the corporation is a publicly traded company and there has been any change to the last Statement of Information or Corporate Disclosure Statement filed with the Secretary of State, the Statement of Information and the Corporate Disclosure Statement must be completed in their entirety.

The fee for filing the initial or annual Statement of Information is $20.00. In addition, all domestic stock corporations must pay a $5.00 disclosure fee at the time of filing the initial or annual statement, for a total of $25.00. A credit card is required to file online. If a statement is filed outside the applicable filing period to amend any information on a previously filed statement, and is not an initial or annual filing, no fee is required.

A blank Statement of Information and a self-addressed envelope are provided to the corporation at the time of filing the original Articles of Incorporation. A preprinted Statement of Information and self- addressed envelope are mailed to each active corporation, to the last address of record, prior to the applicable due date. The corporation’s failure to receive the form is not an excuse for failure to comply with the filing requirements.

If there has been no change in the information contained in the last Statement of Information and the last Corporate Disclosure Statement, if any, filed with the Secretary of State, the corporation may file a “no change” statement during the applicable filing period indicating that no changes in the required information have occurred.

Under California law, one or more persons, partnerships, associations or other corporations may form a corporation by first filing with the Secretary of State Articles of Incorporation.

A corporation is deemed to exist in perpetuity unless a termination provision is included in the Articles of Incorporation. A corporation is born when the articles are filed.

As with limited liability companies and certain partnerships, state law restricts the types of names that can be used by a corporation. For example, there are restrictions on the use of the words “bank” and “trust” and a general prohibition on the use of any name that is substantially similar to a preexisting corporation or the use of any name likely to mislead the public.

California and most other states have provisions allowing organizers to reserve a corporate name for up to 60 days prior to the filing of Articles of Incorporation.

California Corporations Code § 202 requires articles of incorporation to include the following:

• The name of the corporation, which generally must include the word “corporation”, “incorporated” or “limited” or an abbreviation of one of such words; and

• The applicable one of the following statements:

The purpose of the corporation is to engage in any lawful act or activity for which a corporation may be organized under the General Corporation Law of California other than the banking business, the trust company business or the practice of a profession permitted to be incorporated by the California Corporations Code; or

The purpose of the corporation is to engage in the profession of (with the insertion of a profession permitted to be incorporated by the California Corporations Code) and any other lawful activities (other than the banking or trust company business) not prohibited to a corporation engaging in such profession by applicable laws and regulations.

• The name and street address in this state of the corporation’s initial agent for service of process;

• If the corporation is authorized to issue only one class of shares, the total number of shares which the corporation is authorized to issue. If the corporation is authorized to issue more than one class of shares, or if any class of shares is to have two or more series:

- The total number of shares of each class the corporation is authorized to issue, and the total number of shares of each series which the corporation is authorized to issue or that the board is authorized to fix the number of shares of any such series;

- The designation of each class, and the designation of each series or that the board may determine the designation of any such series; and

- The rights, preferences, privileges and restrictions granted to or imposed upon the respective classes or series of shares or the holders thereof, or that the board, within any limits and restrictions stated, may determine or alter the rights, preferences, privileges and restrictions granted to or imposed upon any wholly unissued class of shares or any wholly unissued series of any class of shares. As to any series the number of shares of which is authorized to be fixed by the board, the articles may also authorize the board, within the limits and restrictions stated therein or stated in any resolution or resolutions of the board originally fixing the number of shares constituting any series, to increase or decrease (but not below the number of shares of such series then outstanding) the number of shares of any such series subsequent to the issue of shares of that series. In case the number of shares of any series shall be so decreased, the shares constituting such decrease shall resume the status which they had prior to the adoption of the resolution originally fixing the number of shares of such series.

• In case the corporation is a corporation subject to the Banking Law, the articles shall set forth a statement of purpose which is prescribed in the applicable provision of the Banking Law;

• In case the corporation is a corporation subject to the Insurance Code as an insurer, the articles shall additionally state that the business of the corporation is to be an insurer; and

• If the corporation is intended to be a “professional corporation” within the meaning of the Moscone-Knox Professional Corporation Act (Part 4 (commencing with Section 13400) of Division 3), the articles shall additionally contain the statement required by Section 13404.

Unless expressly prohibited in the Articles of Incorporation, a corporation will have the same powers and authority to carry on business as an individual. As a practical matter, most corporations include a broad provision in their Articles of Incorporation authorizing the company to engage in any lawful enterprise. This saves time later if the company elects to get into a new line of business.

If initial directors have not been named in the articles, the incorporator or incorporators, until the directors are elected, may, under California law, do whatever is necessary and proper to perfect the organization of the corporation, including the adoption and amendment of bylaws of the corporation and the election of directors and officers. The bylaws may be adopted, amended or repealed either by approval of the outstanding shares (Section 152) or by the approval of the board, except as provided in Section 212.

Subject to subdivision (a)(5) of Section 204, the articles or bylaws may restrict or eliminate the power of the board to adopt, amend or repeal any or all bylaws. The bylaws set forth the rules for the daily operation of the corporation, including provisions governing:

• The time, place and manner of calling, conducting and giving notice of shareholders’, directors’ and committee meetings;

• The manner of execution, revocation and use of proxies;

• The qualifications, duties and compensation of directors; the time of their annual election; and the requirements of a quorum for directors’ and committee meetings;

• The appointment and authority of committees of the board;

• The appointment, duties, compensation and tenure of officers;

• The mode of determination of holders of record of its shares; and

• The making of annual reports and financial statements to the shareholders.

California Corporations Code § 213 provides that “every corporation shall keep at its principal executive office in this state, or if its principal executive office is not in this state at its principal business office in this state, the original or a copy of its bylaws as amended to date, which shall be open to inspection by the shareholders at all reasonable times during office hours. If the principal executive office of the corporation is outside this state and the corporation has no principal business office in this state, it shall upon the written request of any shareholder furnish to such shareholder a copy of the bylaws as amended to date.”

VII. SUBCHAPTER S CORPORATION

S Corporations are created when a duly constituted and eligible corporation elects S Corporation status by filing Form 2553 with the Internal Revenue Service.

A corporation may elect S Corporation status only if it meets all of the following requirements:

• It is a domestic corporation;

• It has no more than 100 shareholders (members of a family are treated as one shareholder for purposes of this requirement);

• Its only shareholders are individuals, estates, or certain exempt organizations;

• It has no nonresident alien shareholders;

• It has only one class of stock; and

• It is not one of the following ineligible corporations:

▫ A bank or thrift institution that uses the reserve method of accounting for bad debts under section 585;

▫ An insurance company subject to tax under the rules of subchapter L of the Code;

▫ A corporation that has been treated as a possessions corporation under section 936; or

▫ It has a permitted tax year as required by section 1378 or makes a section 444 election to have a tax year other than a permitted year.

Each shareholder must consent to the election of subchapter S status.

A parent S corporation can elect to treat an eligible wholly-owned subsidiary as a qualified subchapter S subsidiary (Qsub). If the election is made, the assets, liabilities, and items of income, deduction, and credit of the Qsub are treated as those of the parent.

CHAPTER 3: RIGHTS AND DUTIES OF BUSINESS OWNERS

Chapter Objective

After completing this chapter, you should be able to:

• Identify the rights as well as the obligations of owners in multi-owner businesses.

The person who chooses to go into business as a sole proprietor has few issues to worry about in this area. They must certainly comply with all applicable local, state, and federal laws in conducting their business. A sole proprietor cannot, therefore, engage in legally prohibited anti-competitive practices in an effort to destroy a competitor. However, because a sole proprietor has no partners, they may make decisions for the business that benefit only themselves.

With businesses that have more than one owner, whether they are partners, members of a limited liability company or shareholders of a corporation, there are laws that govern the manner in which these co-owners can and must relate to one another and limit the bases upon which business decisions are made. This chapter discusses these areas, focusing on the rights as well as the obligations of owners in the following multi-owner businesses: partnerships, limited liability companies and corporations.

I. PARTNERSHIPS

Both state law and written partnership agreements govern the conduct of partners, both as they relate to each other and to the partnership as a whole. State law often establishes default rules, that govern partnerships in the event an issue is not addressed in a partnership agreement. In some cases, those default rules are deemed so important that they cannot be changed through a written partnership agreement. Some of these rules deal with the rights or duties of partners.

A. RIGHTS OF PARTNERS

As set forth in § 401 of the Uniform Partnership Agreement (UPA) and provided for under every state law, each partner has the following basic rights (subject to modification in a written partnership agreement):

• The right to share in the profits (the default rule provides that partners share profits in equal amounts; this topic is discussed in detail in Chapter 6 – Distributions to Owners);

• The right to be reimbursed for an advance to the partnership beyond the amount of capital the partners agreed to contribute;

• The right to equal participation in the management of partnership business; and

• The right of access to the books and records of the partnership. This right may not be unreasonably restricted. Under the UPA, a partner’s right to inspect books and records may not be unreasonably limited in a written partnership agreement.

Partners do not have the right:

• To use partnership property for anything other than partnership business;

• To demand remuneration for services performed for the partnership except as otherwise provided in the partnership agreement; or

• To transfer his or her partnership to a third party without the consent of the other partners (the simple right to receive profits can be transferred without the consent of the other partners)

B. DUTY OF PARTNERS

The duties of partners can be broken down into two general categories:

• Duty of Loyalty: The duty of loyalty generally includes a duty to avoid self-dealing and a duty not to compete with the company.

• Duty of Care: This duty requires partners to make prudent, well-informed decisions regarding the partnership.

These twin duties have been codified in a number of ways. The provisions of Texas law are provided as illustrative of state law treatment on this subject:

Sec. 152.204. General Standards of Partner’s Conduct

(a) A partner owes to the partnership, the other partners, and a transferee of a deceased partner’s partnership interest as designated in Section 152.406(a)(2):

(1) a duty of loyalty; and

(2) a duty of care.

(b) A partner shall discharge the partner’s duties to the partnership and the other partners under this code or under the partnership agreement and exercise any rights and powers in the conduct or winding up of the partnership business:

(1) in good faith; and

(2) in a manner the partner reasonably believes to be in the best interest of the partnership.

(c) A partner does not violate a duty or obligation under this chapter or under the partnership agreement merely because the partner’s conduct furthers the partner’s own interest.

(d) A partner, in the partner’s capacity as partner, is not a trustee and is not held to the standards of a trustee.

Sec. 152.205. Partner’s Duty of Loyalty

A partner’s duty of loyalty includes:

(1) accounting to and holding for the partnership property, profit, or benefit derived by the partner:

(A) in the conduct and winding up of the partnership business; or

(B) from use by the partner of partnership property;

(2) refraining from dealing with the partnership on behalf of a person who has an interest adverse to the partnership; and

(3) refraining from competing or dealing with the partnership in a manner adverse to the partnership.

Sec. 152.206. Partner’s Duty of Care

(a) A partner’s duty of care to the partnership and the other partners is to act in the conduct and winding up of the partnership business with the care an ordinarily prudent person would exercise in similar circumstances.

(b) An error in judgment does not by itself constitute a breach of the duty of care.

(c) A partner is presumed to satisfy the duty of care if the partner acts on an informed basis and in compliance with Section 152.204(b).

Section 152.205 provides three specific areas included in a partner’s duty of loyalty:

• First, a partner is required to account to the partnership and hold for it any benefit derived by the partner in the conduct and winding up of the partnership business or from the use of partnership property. This requirement does not apply in the formation of the partnership. Negotiations for the formation of a partnership thus begin at arm’s length. If they involve a special relationship, or if in the course of negotiations, a special relationship may develop, that intensifies the obligation of good faith;

• Second, a partner is required to refrain from dealing with the partnership on behalf of a party having an interest adverse to the partnership; and

• Third, a partner must refrain from competing with the partnership or dealing with the partnership in a manner adverse to the partnership.

These rules are all designed to avoid a conflict of interest in the minds of a partner who has a duty of loyalty to the partnership and any of the partners. The first and third areas together cover “partnership opportunities.”

Section 152.206 defines the partner’s duty of care as that of negligence. This section, together with §152.204 (b), incorporates the so-called “business judgment rule,” under which a partner is presumed to satisfy the duty of care if the partner acts on an informed basis, in good faith, and in honest belief that the action is in the best interests of the partnership. The business judgment rule is described in greater detail in the portions of this chapter dealing with limited liability companies and corporations.

Pursuant to Texas Business Organizations Code §152.002, the duties set forth above may not be waived or eliminated entirely in a written partnership agreement.

Sec. 152.002. Effect of Partnership Agreement; Nonwaivable and Variable Provisions

(a) Except as provided by Subsection (b), a partnership agreement governs the relations of the partners and between the partners and the partnership. To the extent that the partnership agreement does not otherwise provide, this chapter and the other partnership provisions govern the relationship of the partners and between the partners and the partnership.

(b) A partnership agreement or the partners may not:

(1) unreasonably restrict a partner’s right of access to books and records under Section 152.212;

(2) eliminate the duty of loyalty under Section 152.205, except that the partners by agreement may identify specific types of activities or categories of activities that do not violate the duty of loyalty if the types or categories are not manifestly unreasonable;

(3) eliminate the duty of care under Section 152.206, except that the partners by agreement may determine the standards by which the performance of the obligation is to be measured if the standards are not manifestly unreasonable;

(4) eliminate the obligation of good faith under Section 152.204(b), except that the partners by agreement may determine the standards by which the performance of the obligation is to be measured if the standards are not manifestly unreasonable;

(5) vary the power to withdraw as a partner under Section 152.501(b)(1), (7), or (8), except for the requirement that notice be in writing;

(6) vary the right to expel a partner by a court in an event specified by Section 152.501(b)(5);

(7) restrict rights of a third party under this chapter or the other partnership provisions, except for a limitation on an individual partner’s liability in a limited liability partnership as provided by this chapter;

(8) select a governing law not permitted under Sections 1.103 and 1.002(43)(C); or

(9) except as provided in Subsections (c) and (d), waive or modify the following provisions of Title 1:

(A) Chapter 1, if the provision is used to interpret a provision or to define a word or phrase contained in a section listed in this subsection;

(B) Chapter 2, other than Sections 2.104(c)(2), 2.104(c)(3), and 2.113;

(C) Chapter 3, other than Subchapters C and E of that chapter; or

(D) Chapters 4, 5, 10, 11, and 12, other than Sections 11.057(a), (b), (c)(1), (c)(3), (d), and (f).

(c) A provision listed in Subsection (b)(9) may be waived or modified in a partnership agreement if the provision that is waived or modified authorizes the partnership to waive or modify the provision in the partnership’s governing documents.

(d) A provision listed in Subsection (b)(9) may be waived or modified in a partnership agreement if the provision that is modified specifies:

(1) the person or group of persons entitled to approve a modification; or

(2) the vote or other method by which a modification is required to be approved.

The above section is intended to ensure a fundamental core of partner responsibility. None of the duties of loyalty, care, and good faith under Section 152.204 may be eliminated entirely. Nevertheless, the partners may identify specific types or categories of activity that do not violate the duty of loyalty or may determine the standards by which the duty of care and the obligation of good faith are to be measured. These limitations or standards will be given effect if they are not manifestly unreasonable. Therefore, the partners can negotiate and draft specific contractual provisions favorably to their particular needs, but blanket waivers and those limitations or standards that a court finds to be manifestly unreasonable are not enforceable.

C. PARTNERS’ LEGAL RIGHTS

A partnership is normally authorized to bring legal action against a partner who has violated applicable rules of conduct, including a breach of loyalty. Under the Uniform Partnership Act, a partner may also bring a suit directly against another partner for almost any cause of action arising out of the conduct of the partnership business. In addition to a formal account, the court may grant any other appropriate legal or equitable remedy.

The Uniform Partnership Act also makes it clear that a partner may recover against the partnership and the other partners for personal injuries or damage to the property of the partner caused by another partner.

II. LIMITED LIABILITY COMPANIES

A. RIGHTS OF MEMBERS

Similar to shareholders of a corporation, members of a limited liability company have certain rights, including rights to notice of meetings of the organization and rights to inspect the entity’s books and other financial records, including tax returns. Membership rights can be particularly crucial in situations where that member holds a minority interest in the company and is at odds with those holding majority ownership. Each state’s statutory schemes sets forth the specific rights of members, which generally includes the right to liquidate their investment.

Under the Uniform Limited Liability Company Act, members have the following rights to information:

ULLCA § 408. Member’s right to information.

(a) A limited liability company shall provide members and their agents and attorneys access to its records, if any, at the company’s principal office or other reasonable locations specified in the operating agreement. The company shall provide former members and their agents and attorneys access for

proper purposes to records pertaining to the period during which they were members. The right of access provides the opportunity to inspect and copy records during ordinary business hours. The company may impose a reasonable charge, limited to the costs of labor and material, for copies of records furnished.

(b) A limited liability company shall furnish to a member, and to the legal representative of a deceased member or member under legal disability:

(1) without demand, information concerning the company’s business or affairs reasonably required for the proper exercise of the member’s rights and performance of the member’s duties under the operating agreement or this [Act]; and

(2) on demand, other information concerning the company’s business or affairs, except to the extent the demand or the information demanded is unreasonable or otherwise improper under the circumstances.

(c) A member has the right upon written demand given to the limited liability company to obtain at the company’s expense a copy of any written operating agreement.

One of the significant areas of the law of limited liability companies that has yet to be developed relates to the rights of minority members. This issue can arise in many ways, including situations where a minority member or members is being “squeezed out” of the company’s decision-making by those with a controlling interest in the entity. The law of corporations, which is much more developed, is often used to resolve disputes involving minority owners of limited liability companies in the absence of defined law governing LLCs. Some states also allow members to seek judicial dissolution of a limited liability company in certain situations where the interests of a minority owner are being harmed.

B. DUTIES OF MEMBERS

Under common law, and as provided for in statute, directors and officers of a corporation have a duty to the corporation and to the other shareholders to put personal interests aside and act in the best interests of the entity and its other owners. This is often referred to as a director’s or officer’s duty of loyalty. In addition, in executing their duties, directors and officers are likewise required to make well-informed decisions about the business. This is commonly referred to as a director’s or officer’s duty of care. Both of these common law principles of corporate law have been carried over to the limited liability company.

As corporate law is often used to resolve disputes in limited liability companies, its principles relating to a director’s duty of loyalty and duty of care are commonly carried over in determining whether a member of a limited liability company has breached their duties to the other members or the company as a whole. As a result, a general understanding of these principles of corporate law can be important in understanding the responsibilities of a member of a limited liability company, particularly a member- managed company.

Remember, however, that one of the hallmarks of the limited liability company is its flexibility. As a result, a limited liability company’s operating agreement can set forth specific rules governing the duties and obligations of its members in detail. Each state also generally provides specific rules in statute that set forth minimum standards of conduct by members. In some cases, standards will differ between member- anaged and non-member-managed companies. As long as the standards set forth in an operating agreement do not violate state statute, courts will uphold them in the event of a litigated dispute.