Skip to content

Skip to content

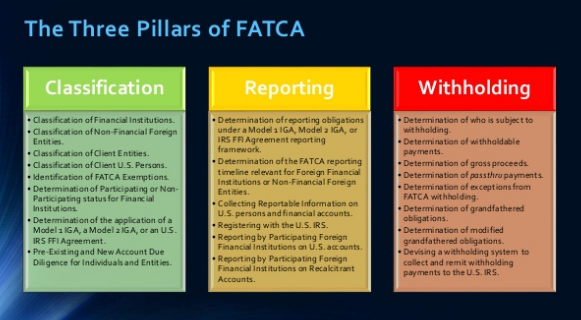

The US tax code at the Federal level has over 8 million words. It’s therefore easy for someone to look at one small part while being unaware of how it fits into the wider picture. One area that has received much scrutiny and been the subject of much discussion is the definition of a Foreign Financial Institution or FFI for FATCA purposes.

According to 26 CFR § 1.1471-1, an FFI is –

(50) Financial institution. The term financial institution has the meaning set forth in 1.1471-5(e) and includes a financial institution as defined in an applicable Model 1 or Model 2 IGA.

So we need to look at BOTH the Regs and the IGA to truly understand the mechanics of FATCA classifications and definitions.

The Final Regulations generally define an FFI as any foreign entity that is a “financial institution” (Treas. Reg. § 1.1471-5(d)). One category of financial institution, in turn, is an “investment entity,” which means: “any entity that is described in paragraph (e)(4)(i)(A), (B), or (C) of this section.

(A) The entity primarily conducts as a business one or more of the following activities or operations

for or on behalf of a customer—

(1) Trading in money market instruments (checks, bills, certificates of deposit, derivatives, etc.); foreign currency; foreign exchange, interest rate, and index instruments; transferable securities;

or commodity futures;

(2) Individual or collective portfolio management; or

(3) Otherwise investing, administering, or managing funds, money, or financial assets on behalf of other persons.

(B) The entity’s gross income is primarily attributable to investing, reinvesting, or trading in

financial assets (as defined in paragraph (e)(4)(ii) of this section) and the entity is managed

by another entity that is described in paragraph (e)(1)

(i) [depository bank],

(ii) [custodian],

(iv) [specified insurance company], or

(e)(4)(i)(A) of this section. For purposes of this paragraph (e)(4)(i)(B), an entity is managed by another entity if the managing entity performs, either directly or through another third-party service provider, any of the activities described in paragraph (e)(4)(i)(A) of this section on behalf of the managed entity.

(C) The entity functions or holds itself out as a collective investment vehicle, mutual fund, exchange traded fund, private equity fund, hedge fund, venture capital fund, leveraged buyout fund, or any similar investment vehicle established with an investment strategy of investing, reinvesting, or

trading in financial assets” (Treas. Reg. § 1.1471-5(e)(4)(i).)

—————-

The Preamble indicates that one of Treasury’s and the IRS’s goals in drafting the definition of investment entity was generally to follow the approach taken in the IGAs to defining this term. In paragraph (A) of the definition, the Final Regulations do correspond fairly closely to the IGAs’ approach, using wording that largely follows that of the IGAs. However, the Final Regulations contain examples of the application of paragraph (A) that appear possibly to be at odds with the substantive requirements of that paragraph and of the IGAs.

In addition, paragraphs (B) and (C) represent a departure from the definition used in the IGAs, in

ways that it is not clear are intended. Under the Final Regulations, it is not entirely clear whether an entity must have authority to make binding investment decisions on behalf of customers whose financial assets it manages, in order to fall within paragraph (A) of the definition of investment entity. It seems that the corresponding portion of the IGAs’ definition of investment entity does require such authority, and paragraph (A) can reasonably be read as requiring such authority.

Clause (1) refers to the manager “trading in” financial assets for customers;

clause (2) refers to “management” of customers’ portfolios; and

clause (3) refers to “otherwise investing, administering or managing” financial assets on behalf of other persons. Collectively, the quoted words can be read as emphasizing the ability of a manager to decide whether to acquire or dispose of financial assets for customers.

For an example of such wording in the IGA, have a look at page 2 of the IGA between the USA and Singapore –

In the UK, the tax authority made it even clearer. In HM Revenue and Customs’ Guidance Notes concerning the implementation of the Model 1 IGA between the United Kingdom and the United States, a similar question is addressed: whether an independent financial advisor that provides advice to clients about whether to invest in a fund, but does not itself own and sell interests in that fund, is considered an investment entity. The Guidance Notes conclude it is not. Please see – HM Revenue and Customs, Implementation of International Tax Compliance (United States of America), Regulations 2013: Guidance Notes, paragraph 2.18 (Advisory-only distributors).

In addition, a reading of paragraph (A) that requires an entity to have authority to make investment decisions could be seen as fitting well with other, related provisions of the Final Regulations. Paragraph (B) of the definition of “investment entity” includes an investment fund or collective investment vehicle that owns financial assets managed by an entity described in paragraph (A) or other financial institution. Such a fund or vehicle would generally have a manager with authority to make investment decisions. Furthermore, this reading of paragraph (A) also would fit naturally with

the “sponsored entity” rules in the Final Regulations, pursuant to which an investment vehicle that has a manager with authority to manage and enter into contracts on behalf of the vehicle can opt to be treated as a deemed-compliant FFI and to have the manager perform the same reporting under FATCA as the investment vehicle would need to do if it were a participating FFI (Treas. Reg. § 1.1471-5(f)(1)(i)(F)(3), (f)(2)(iii). )

In the context of the FATCA regime, limiting paragraph (A) to managers that have investment authority over the financial assets owned by customers has a logic to it: such managers are relatively likely to have (and be able to report, under the sponsored entity rules or otherwise) useful information

about the types of assets owned by, and the types of income received by, their customers; additionally, if the manager’s customer is an investment fund described in paragraph (B) of the

definition of investment entity, there might be concerns that the manager could conceivably direct the flow of income earned on the fund’s financial assets in a manner that would avoid the intent

of FATCA, if the manager was not itself treated as a financial institution.

Thus, there are reasons in favor of construing paragraph (A) as referring only to managers that have investment authority over their customer’s assets. If paragraph (A) were read more broadly (as not requiring investment discretion), then it could include any entity that executed trades on its client’s instructions, even a brokerage firm. This would lead to an extremely expansive definition of investment entity, especially because of the interplay between paragraphs (A) and (B): for example, an entity with brokerage accounts that the entity (rather than the broker) managed would qualify as an investment entity under paragraph (B). In our view, it is clear that paragraph (A) is not intended to be read so broadly.

The Preamble states that passive entities that are not “professionally managed” are treated as NFFEs under the Final Regulations, rather than as FFIs. That statement would prove largely meaningless as a practical matter, if every passive entity that held its financial assets in brokerage accounts had to be treated as an investment entity under paragraph (B) (and thus as a financial institution), because the brokerage firm was an investment entity described in paragraph (A). The same point applies to a passive entity that receives other standard types of ministerial or support services from a service

provider that has only limited involvement with, and information about, the entity (for example, preparation of a passive entity’s financial statements by an accounting firm): the Final Regulations appear clearly not to be designed to cause every investment vehicle that receives such services to be an investment entity under paragraph (B), and every company that provides such services to be an investment entity under paragraph (A).

The above includes an extract from the –

NEW YORK STATE BAR ASSOCIATION,

TAX SECTION REPORT ON THE FINAL FATCA REGULATIONS:

DEFINITIONS OF “FFI,” “FINANCIAL ACCOUNT” AND RELATED TERMS, April 29, 2013