Skip to content

Skip to content

In January 2018, I hosted a seminar in Singapore on international business expansion. There was one attendee who was so stressed out. Why? Because, as a US citizen who is the owner of overseas businesses, he realized that Tax Reform in the US made things more difficult than before!

Our Asia and UK practice is really built around business owners as opposed to employees. Most of our US exposed business owners reside outside of the US. So let’s cut to the chase, The Tax Cuts and Jobs Act hit many of our clients on two fronts:

(i) You must pay a 15.5% tax on part of your foreign retained earnings. This tax can be spread over 8 years.

(ii) Going forward, the ability of expats to retain profits in a foreign corporation is virtually eliminated. We must now pay US tax on our profits in excess of the Foreign Earned Income

Exclusion. Holding shares through Non US citizen spouses is a weak strategy. A business owner can earn $104,100 tax-free, or a husband and wife both working in the business can take out a combined $208,200 in 2018 free of Federal income tax.

On top of this, US tax breaks for “pass-through entities,” such as domestic LLCs and S-Corporations are not available to expats. Many are saying that the most practical step is to form a US

C-corporation and start over with a new offshore corporation. Pay the repatriation tax on previous years in your old corporation and start fresh with a structure designed for 2018. But expat entrepreneurs need to watch out for double taxation. When you take out retained earnings from your US corporation as a dividend, you’ll usually pay US tax on the distribution (on your personal return). Careful planning should go into building this structure and a long-term tax plan that minimizes double taxation must be developed.

If you wish to retain earnings offshore, you must avoid Subpart F, and the new anti-deferral mechanisms introduced under the new Act. The key to a successful offshore plan is to

maximize tax deferral in a compliant manner.

Strategies to consider include –

- Using the Foreign Earned Income Exclusion

- Note that Tested Income (basis for calculating

GILTI) does not include dividends received from a related person - Under the Act, US Shareholders who arenindividuals (e.g., partners of private equity funds) fare far worse than US Shareholders that are domestic corporations (e.g., a US Topco).

Exemption of dividends from foreign corporations. Most active foreign income of a CFC is not subject to current U.S. taxation. Under prior law, if the earnings of a CFC were actually paid out

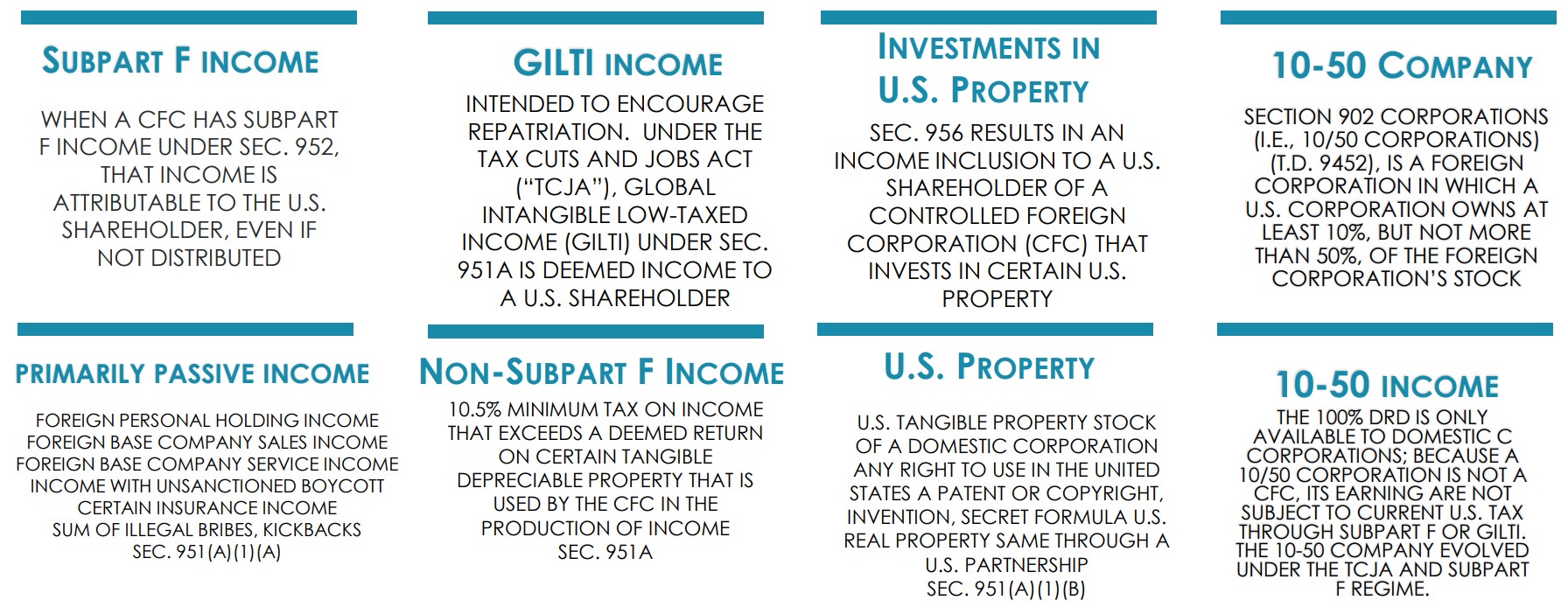

as a dividend, or deemed to be paid under special rules applicable to CFC investments in U.S. property, U.S. tax would be imposed on the dividend (or deemed dividend). For individual US Shareholders, this will remain true after the Act. But for US Shareholders that are domestic corporations, the Act puts into place a “participation exemption” in the form of a 100% dividends-received deduction for dividends from 10%-or-greater owned foreign corporations (including but not limited to CFCs).

The new “GILTI” tax. In an effort to ensure that some minimal amount of tax is paid by U.S. taxpayers on their low-taxed foreign income, the Act features a new tax on “global intangible low-taxed income” (“GILTI”). Every US Shareholder of a CFC will be required to include in gross income its GILTI for the taxable year. But whereas US Shareholders that are domestic corporations will pay the GILTI tax at half the rate of the regular tax, US Shareholders who are individuals will pay the tax at their top marginal rate (37% under the Act). And whereas domestic corporations will be eligible to claim foreign tax credits for 80% of foreign taxes paid on GILTI income, individuals will not be entitled to any foreign tax credits.

FDII. In addition to the benefits described above, domestic corporations may also benefit from a new tax incentive contained in the Act, for income referred to as “foreign-derived intangible income” (“FDII”). The Act allows a U.S. corporation to claim a 37.5% deduction with respect to its FDII, effectively reducing the tax rate thereon to 13.125%. Generally, FDII is intended to capture income, over a base return on tangible property, derived from property sold or services provided in foreign markets. While sometimes referred to as a “patent box,” it applies more broadly to foreign-derived income.

- CFC rule changes mean that now, shares owned by a non-resident will be attributed to a U.S. Person in determining CFC status.

- If you’re working with non-US persons abroad, you might restructure your business so it’s not a CFC. For example, a US company and a foreign company are working together on deals as separate entities. They might decide to join together in one corporation with each party owning 50% of the shares and having 50% control over the business.

- Consider Puerto Rico.

- All expat business owners should be operating inside an offshore corporation to eliminate the 15% Self Employment tax and to maximize the value of the Foreign Earned Income Exclusion. You then report your salary from this company on IRS Form 2555 attached to your personal return, Form 1040.

- Inserting a US Corp into your structure

- Checking the box on the CFC to make it a flow through

- Making a Section 962 election (very controversal!).

This is just the summary. For tax enthusiasts like myself, feel free to continue reading. Below, I go into some detail on the previous regime and how drastically things have changed…

—————————————————————–

Introduction

Public law no. 115-97, an Act to provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018, is a congressional revenue act originally introduced in Congress as the Tax Cuts and Jobs Act (TCJA). Public law no. 115-97 (“the Act”) amended the Internal Revenue Code of 1986 based on tax reform advocated by congressional Republicans and the Trump administration. Major elements include reducing tax rates for businesses and individuals; a personal tax simplification by increasing the standard deduction and family tax credits, but eliminating personal exemptions and making it less beneficial to itemize deductions; limiting deductions for state and local income taxes (SALT) and property taxes; further limiting the mortgage interest deduction; reducing the alternative minimum tax for individuals and eliminating it for corporations; reducing the number of estates impacted by the estate tax; and repealing the individual mandate of the Affordable Care Act (ACA or Obamacare).

Beginning in 2018, domestic corporations are entitled to a 100 percent Dividends-Received Deduction (DRD) for the non-U.S. source portion of dividends received from specified 10 percent owned non-U.S. corporations. A one-year holding period of the non-U.S. corporate stock is required to be eligible for this DRD. However, no foreign tax credit or deduction is allowed for any taxes paid. One more caveat: the 100% DRD only applies to C-corporation shareholders.

See more here – https://www.mooresrowland.tax/2018/01/an-act-to-provide-for-reconciliation.html

Previous rules on CFCs

Controlled foreign corporation (CFC) rules are features of an income tax system designed to limit artificial deferral of tax by using offshore low taxed entities. The rules are needed only with respect to income of an entity that is not currently taxed to the owners of the entity. Generally, certain classes of taxpayers must include in their income currently certain amounts earned by foreign entities they or related persons control.

These CFC rules generally define the types of owners and entities affected, the types of income or investments subject to current inclusion, exceptions to inclusion, and means of preventing double inclusion of the same income. Countries with CFC rules include the United States (since 1962), the United Kingdom, Germany, Japan, Australia, New Zealand, Brazil, Russia (since 2015), Sweden, and many others. Rules in different countries may vary significantly.

In the US –

- A Controlled Foreign Corporation is any corporation organized outside the U.S. (a foreign corporation) that is more than 50% owned by U.S. Shareholders.

- A U.S. Shareholder is any U.S. personb(individual or entity) that owns 10% or more of the foreign corporation. Complex rules apply to attribute ownership of one person to another person.

THE CONTROLLED FOREIGN CORPORATION (“CFC”) U.S. TAX REGIME – THE BEGINNING

- The CFC rules were enacted in 1962 to limit the deferral of tax by U.S. taxpayers using offshore low-tax jurisdictions to shield income from U.S. taxation.

- Prior to the first U.S. CFC rules, it was common for publicly-traded companies to form subsidiaries in tax havens, shift income to those subsidiaries, and avoid U.S. tax until such income were ever repatriated to its U.S. Parent.

- The CFC and Subpart F rules were intended to cause current taxation to the U.S. Parent Shareholder where income was of a sort that could be artificially shifted.

- The CFC rules were in no way intended to interfere with an active trade or business being carried on in such foreign jurisdiction.

U.S. CONTROLLED FOREIGN CORPORATION (“CFC”) DEFINED

- More than 50% Owned – Under Sec. 957(a), any foreign corporation, if more than 50% of (i) the total combined voting power of all classes of stock of such foreign corporation entitled to vote, or (ii) the total value of such shares in such foreign corporation, is owned in the aggregate, or is considered as owned by applying certain attribution rules, by United States Shareholders on any day during the tax year of such foreign corporation.

- U.S. Shareholder – Under Sec. 951(b), any U.S. Person (individual or entity) who owns, or is considered as owning, by applying certain attribution rules, 10% or more of the total voting power or the total value of stock in the foreign corporation.

• Complex rules apply to attribute ownership among related owners under Sec. 958(b) which requires application of Sec. 318(a).

• For example, stock owned by Mother is attributed to Son, unless one is U.S.

and the other is a non-resident alien.

Under prior and current law, a C.F.C. is any foreign corporation in which U.S. Shareholders (defined below) own more than 50% of the foreign corporation’s stock by value or vote.

Under prior law, a U.S. Shareholder was defined as a U.S. person that owned 10% or more of the foreign corporation’s voting stock. Under the new law, the definition includes a U.S. person that owns 10% or more of the foreign corporation’s stock by value. In addition, the attribution rules for determining constructive ownership of a foreign corporation by a U.S. person are expanded to include attribution from a foreign person to a U.S. person.

Under prior law, a foreign corporation was required to be controlled for 30 days before the Subpart F rules applied. Under the new law, the 30-day requirement is no longer in effect.

Subpart F

The CFC rule that most US Tax practitioners know would arguably be the Subpart F rules.

Enacted in 1962, these rules incorporate most of the features of CFC rules used in other countries. Subpart F was designed to prevent U.S. citizens and resident individuals and corporations from artificially deferring otherwise taxable income through use of foreign entities.

The rules require that:

- A U.S. Shareholder of a Controlled Foreign Corporation (“CFC”) must include in his/its income currently

- His/its share of Subpart F Income of the CFC and

- His/its share of earnings and profits (“E&P”) of the CFC that are invested in United States Property, and further exclude from his/its income any dividends distributed from such previously taxed income.

Subpart F income includes the following:

- Foreign personal holding company income (FPHCI), including dividends, interest, rents, royalties, and gains from alienation of property that produces or could produce such income. Exceptions apply for dividends and interest from related persons organized in the same country as the CFC, active rents and royalties, rents and royalties from related persons in the same country as the CFC, and certain other items.

- Foreign base company sales income from buying goods from a related party and selling them to anyone or buying goods from anyone and selling them to a related party, where such goods are both made and for use outside the CFC’s country of incorporation. A branch rule may cause transfers between a manufacturing branch of a CFC in one country and a sales branch in another country to trigger Subpart F income.

- Foreign base company services income from performing services for or on behalf of a related person. A substantial assistance rule can cause services performed for unrelated parties to be treated as performed for or on behalf of a related party.

- Foreign base company oil-related income from oil activities outside the CFC’s country of incorporation.

- Insurance income from insurance or annuity contracts related to risks outside the CFC’s country of incorporation.

but it does not include:

- Items of income which (after considering deductions, etc., under U.S. concepts) were subject to foreign income tax in excess of 90% of the highest marginal U.S. tax rate for the type of shareholder;

- De minimis amounts of Subpart F income in absence of other Subpart F income in the period;

- Such income if the CFC has a deficit in E&P, in which case it is deferred from recognition until the CFC has positive E&P.

- Any dividend received which is considered paid from amounts previously taxed under Subpart F.

Corporate U.S. shareholders are entitled to a foreign tax credit for their share of the foreign income taxes paid by a CFC with respect to E&P underlying a Subpart F inclusion.

To prevent avoidance of Subpart F, U.S. shareholders of a CFC must recharacterize gain on disposition of the CFC shares as a dividend. In addition, various special rules apply.

Introducing GILTI

The Tax Cuts and Jobs Act (TCJA) includes a general cap on net business interest expense equal to 30% of adjusted taxable income (ATI). It also extends the anti-deferral provisions under Subpart F and creates something called “global intangible low-taxed income” (GILTI).

Very broadly, GILTI is the excess of the U.S. shareholder’s share of each CFC’s non‐subpart F / non‐ECI income over a 10% return on tangible depreciable property

The G.I.L.T.I. regime is designed to decrease the incentive for a U.S. group to shift corporate profits to low-tax jurisdictions. In this way, it protects the new participation exemption regime by preventing mobile intangible income from being used to reduce U.S. taxable income for the payer while preventing the payer’s group from obtaining the benefit of the dividend received deduction (DRD) for dividends from a C.F.C. that received G.I.L.T.I.

As stated in the Conference Committee Report:

Changing the U.S. international tax system from a worldwide system of taxation to a participation exemption system of taxation exacerbates the incentive under present law to shift profits abroad. Specifically, under present law, most foreign profits earned through a subsidiary are not subject to current taxation but will eventually be subject to U.S. taxation upon repatriation. Under the participation exemption system provided for in the bill, however, foreign profits earned through a subsidiary generally will never be subject to U.S. taxation. Accordingly, new measures to protect against the erosion of the U.S. tax base are warranted.

Under new Section 951A of the Act, a 10% US shareholder of a CFC must include in income for a taxable year its share of the CFC’s GILTI. Key provisions of the tax are:

- GILTI will generally equal

(i) the aggregate net income of the CFCs reduced by

(ii) 10% of the CFCs’ aggregate basis in associated tangible depreciable business property minus certain interest expense allocable to (i)

- With respect to 10% shareholders that are corporations, FTCs, in a separate basket, will generally be available for 80% of the foreign taxes imposed on the income included as GILTI. No carryover is allowed for excess credits.

- While a GILTI inclusion by a US shareholder is taxable at the regular 21% corporate rate, the amount of the inclusion is equal to 50% of GILTI, thus resulting in an effective rate of 10.5%. The new tax benefits available for certain foreign-derived intangible income, described below, provide the mechanism for this computation, by essentially providing for a deduction equal to 50% of GILTI, to be reduced after 2025. This GILTI regime is effective for taxable years beginning after December 31, 2017

How is it triggered

In comparison to the traditional approach (Subpart F) that looks for specific items of tainted income, the G.I.L.T.I. provision provides a “safe zone” for a portion of the entire pool of C.F.C. earnings. The safe zone is based principally on a hypothetical yield generated by the C.F.C. on its Qualified Business Asset Investment (“Q.B.A.I.”), determined on a pre-tax basis. Once the safe zone is computed, all additional earnings of the C.F.C. not otherwise taxed under Subpart F or specifically excepted by the statute are considered to be attributable to G.I.L.T.I.

Under Code 951A(a), each person that is a U.S. Shareholder of a C.F.C. for any tax year is the U.S. person that must include in gross income such shareholder’s G.I.L.T.I. for such tax year. In Code 951A(e)(3), the statute provides that a foreign corporation is treated as a C.F.C. for any tax year if it is a C.F.C. at any time during such tax year. The statute provides, in Code 951A(e)(2), that a person is treated as a U.S. Shareholder of a C.F.C. for a given tax year only if it owns stock in the foreign corporation on the last day in the tax year of the foreign corporation on which it is a C.F.C. Ownership includes direct ownership and indirect ownership under Code 958(a).

Under Code 951A, a U.S. Shareholder of a C.F.C. must include in its gross income its G.I.L.T.I. inclusion in a manner similar to inclusions of Subpart F income. In broad terms, this means that a U.S. Shareholder must include in income the amount of income that would have been distributed with respect to the stock that it owned (within the meaning of Code 958(a)) in the C.F.C. if on the last day in its tax year on which the corporation is a C.F.C., it had distributed pro rata to its shareholders an amount equal to the amount of its G.I.L.T.I.

ATTRIBUTION AFTER TCJA – AND FINAL REGULATIONS

Section 958(b) sets forth rules for purposes of applying the tests of tests of Subpart F.

These rules generally incorporate the attribution rules of §318 with several modifications. Section 318 provides rules that attribute the stock to certain family members, between certain entities and their owners, and to holders of options to acquire stock.

Upward Attribution – In the case of entity attribution, under §318(a)(2), stock can be attributed from partnerships, estates, trusts, and corporations to partners, beneficiaries, owners, and shareholders.

Downward Attribution – Under §318(a)(3), stock can be attributed from a person to a partnership, estate, trust, or corporation in which the person has an interest.

Questions Determined: The constructive ownership rules apply for purposes of determining whether:

(1) A U.S. person is a U.S. Shareholder

(2) A foreign corporation is a CFC

(3) The stock of a domestic corporation is owned by a U.S. Shareholder of a CFC for purposes of §956(c)(2), and

(4) A corporation or other person is related to the CFC.

Note: The constructive ownership rules do not apply for purposes of determining the amount included in a U.S.

Shareholder’s gross income under §§951(a) or 951(A).

FAMILY ATTRIBUTION AFTER TCJA

• An individual is deemed to own stock owned, directly or indirectly, by or for the individual’s spouse, children, grandchildren, and parents. (§ 318(a)(1); Reg. § 1.958-2(b)(1)(i))

• Stock of grandchildren is treated as owned by their grandparents, stock held by grandparents is not attributed to their grandchildren. (Cf. Prop. Reg. §1.898-3(a)(4)(iii) Exs. 1, 2.)

• Stock that is treated as constructively owned by an individual through family attribution is not treated as actually owned by the

individual in order to make another individual a constructive owner of that stock.

Example: An individual, H; his wife, W; his son, S; and his grandson (S’s son), G, own the 100 outstanding shares of stock of corporation C, each owning 25 shares. H, W, and S are each considered as owning 100 shares of C, and G is considered as owning 50 shares (his own and his father’s). G is not considered as owning his grandparent’s stock, even though his father constructively owns that stock. (Reg. §1.318-2(b) Ex.)

• In general, family attribution does not extend to attributing stock owned by a nonresident alien individual (other than a foreign trust or estate) to an individual U.S. citizen or resident. (§958(b)(1))

• This limitation does not apply for purposes of determining whether stock of a domestic corporation is owned or considered as owned by a U.S. Shareholder for the purpose of taxation of investments in U.S. property under §956(c)(2)(F).

Example: U.S. citizen E owns 15% of the one class of stock in foreign corporation Y. U.S. citizen F, E’s spouse, owns 5% of such stock. E and F’s four nonresident alien grandchildren each owns 20% of the stock of Y. Under the constructive attribution rules, E is considered as owning the stock owned by F in Y; however, E would not be considered as owning any of the stock owned by the grandchildren because of their nonresident alien status. (Reg. §1.958-2(g)(5) (Ex. 5))

THE EVOLUTION OF THE CFC TAX REGIME 1962 – Present

When a U.S. Shareholder is a corporation, several rules apply in addition to the income inclusion.

- First, a deemed-paid foreign tax credit is allowed under Code 960 for foreign income taxes allocable to G.I.L.T.I. at the level of the C.F.C.

- Second, the Code 951A inclusion includes a “gross-up” under Code 78 for the foreign income taxes claimed as a credit.

- Third, the U.S. corporation is entitled to a 50% deduction (reduced to 37.5% in later tax years) based on the G.I.L.T.I. included in income. As a result, a corporate U.S. Shareholder’s effective tax rate on G.I.L.T.I. plus the gross-up will be 10.5% (increased to 13.125% in later tax years).

How is it calculated

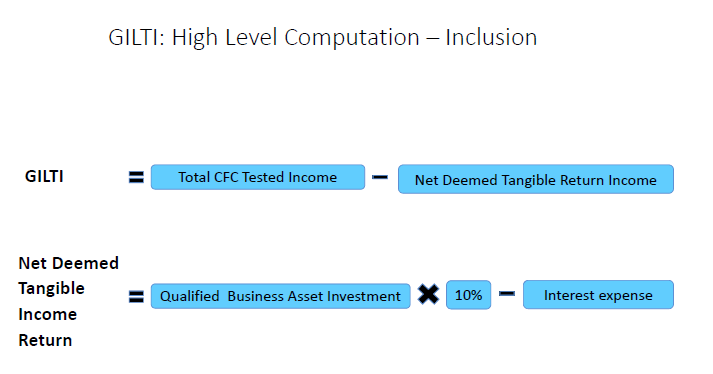

G.I.L.T.I. is determined through several computations that appear in Code 951A. G.I.L.T.I. Defined – With respect to a U.S. Shareholder of a C.F.C., G.I.L.T.I. means the excess of

(i) the shareholder’s “net C.F.C. tested income” for the shareholder’s tax year over

(ii) the “net deemed tangible income return.” This is expressed in the following formula: G.I.L.T.I. = Net C.F.C. Tested Income – Net Deemed Tangible Income Return

Where a U.S. Person is a U.S. Shareholder of several

C.F.C.’s, G.I.L.T.I. is computed on an aggregate basis that takes into account all its C.F.C.’s. The positive net tested income of each C.F.C. within the group that has positive income is added

together to arrive at aggregate positive net tested income. At the same time, the net tested loss of each C.F.C. within the group within the group that has a loss is added together to arrive at aggregate net tested loss. The aggregate positive net tested income is reduced by the aggregate net tested loss to determine G.I.L.T.I.

Net Deemed Tangible Income Return Defined – The U.S. Shareholder’s net deemed tangible income return is

(i) 10% of the aggregate of the shareholder’s pro rata share of the Q.B.A.I. (defined below) of each of its C.F.C.’s, reduced by

(ii) the interest expense of each C.F.C. that is taken into account in determining the shareholder’s net C.F.C. tested income. Here, interest expense means the C.F.C.’s interest expense minus its interest income. This is expressed in the following formula: G.I.L.T.I. = Net C.F.C. Tested Income – ( 0.1 Q.B.A.I. ) – NetnInterest Expense Allocated to Net Tested Income

In making the computation, the full amount equal to 10% of Q.B.A.I. cannot be reduced below zero by net interest expense. Stated differently, the net interest expense allocated to 10% of Q.B.A.I. is capped at 10% of Q.B.A.I.

Net C.F.C. Tested Income Defined – Net C.F.C. tested income is the aggregate of

(i) the U.S. Shareholder’s pro rata share of the “tested income,” if any, of each of its C.F.C.’s, reduced by

(ii) the U.S. Shareholder’s pro rata share of the “tested loss,” if any, of each of its C.F.C.’s. This is expressed in the following formula: Net C.F.C. Tested Income = Sum of C.F.C. Tested Income – Sum of C.F.C. Tested Loss

Tested income of a C.F.C. consists of

(i) its gross income, excluding certain exceptions, reduced by

(ii) its deductions (including taxes) that are properly allocable to such gross income. The exceptions to gross income are as follows:

· An item of income of a C.F.C. from sources within the U.S. that is effectively connected with the conduct of a trade or business within the U.S.

· Gross income of a C.F.C. taken into account in determining Subpart F income

· Gross income excluded from foreign base company income or insurance income by reason of the high-tax exception under Code 954(b)(4) for income subject to an effective rate imposed by a foreign country greater than 90% of the maximum rate of tax specified in Code 11 (which is 21%)

· Dividends received from a related person

· Foreign oil and gas extraction income and foreign oil-related income

The income from sources within the U.S. that is effectively connected with the conduct of a U.S. trade or business must be taxed in the U.S. in order for it to be removed from gross income. Consequently, if the effectively connected income is exempt from U.S. tax or is subject to a reduced U.S. tax rate, it is removed from the list of exceptions to the extent of the benefit. Thus, if a treaty fully exempts the income, the income is fully removed from the exception. On the other hand, if the treaty merely reduces U.S. tax, only a pro rata portion of the income is removed from the list of exceptions, based on the percentage by which U.S. tax is reduced.

Tested loss of a C.F.C. is the excess of (i) deductions (including taxes) properly allocable to the corporation’s gross income, not including the tested income exceptions, reduced by (ii) the amount of such gross income. Q.B.A.I. Defined – Q.B.A.I. means, with respect to a C.F.C., the average of the aggregate of the adjusted bases in specified tangible property used in a trade or business and of a type for which a deduction for depreciation generally would be allowable under Code 167. In terms typically used by corporate management, Q.B.A.I. means investment in property, plant, and equipment adjusted to reflect depreciation expense using longer lives set forth in Code 168(g). Under that provision of U.S. tax law, an alternative depreciation system is applied, inter alia, to tangible property used predominantly outside the U.S. The average bases of the assets in the computation is determined by reference to the adjusted bases as of the close of each quarter of the tax year. This reduces the positive and negative effects of asset acquisitions or dispositions during the year.

Specified tangible property means any property used in the production of tested income. Where property is used in part for the production of tested income and in part for the production of excepted income, the adjusted basis must be allocated between the two in the same proportion that the tested income bears to the total gross income arising from the use of the property.

If a C.F.C. holds an interest in a partnership, the C.F.C.’s distributive share of the aggregate of the partnership’s adjusted bases in its assets must be taken into account for purposes of computing the Q.B.A.I. for the year.