Skip to content

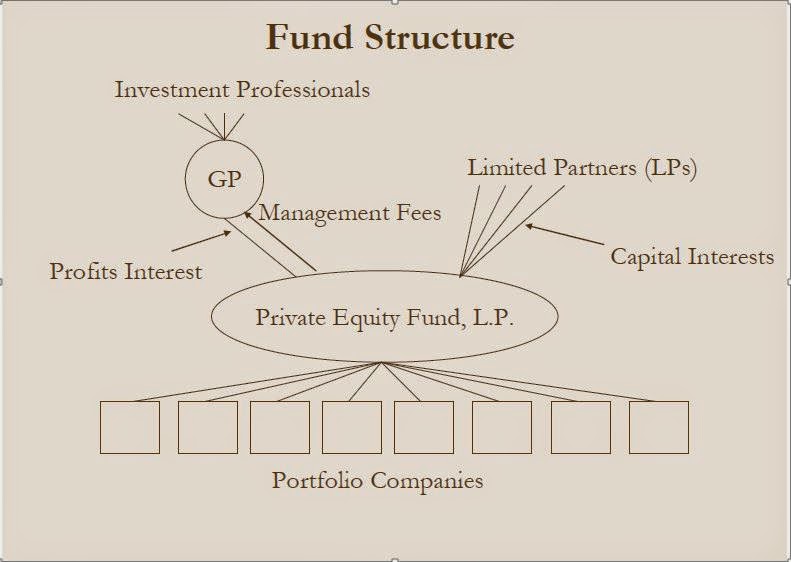

Skip to content So once upon a time, many of us were comfortable thinking that it was possible to have Private equity fund managers take a share of the profits of the partnership as the equity portion of their compensation. The tax rules for compensating service partners created a planning opportunity for managers who receive the industry-standard “two and twenty” (a two percent management fee and twenty percent profits interest).

By taking a portion of their pay in the form of partnership profits, fund managers deferred income derived from their labor efforts and converted it from ordinary income into long-term capital gain.

But now IRS Chief Counsel has issued ILM 201436049 dated 5/20/2014, released on 9/5/2014, which is based primarily on the ruling in the case of Renkemeyer vs Commissioner 136 TC 137 (2011). It suggests that “Partners earnings are not in the nature of a return on a capital investment, but rather are a direct result of the services rendered on behalf of a management company by its partners”.

The full ruling is available here http://www.irs.gov/pub/irs-wd/201436049.pdf but here are the key points –

1. The distributive share of partnership income allocated to members of an LLC was subject to self-employment tax. Under IRC Section 1401, “self-employment income” is taxed at 15.3%– 12.4% goes to the Old-Age, Survivors, and Disability Insurance tax, with the remaining 2.9% earmarked for the Hospital Insurance tax. In addition, beginning January 1, 2013, an extra 0.9% tax is tacked on to a taxpayer’s self-employment income in excess of $250,000 (if married filing jointly, $200,000 if single). Thus, the total self-employment tax burden under current law can reach as high as 16.2%, before considering the deduction for one-half of the self-employment tax (not including the new 0.9% surtax) as permitted by IRC Section 164(f).

2. It reminds us that an LLC is not recognized at federal level as a corp. One must elect to be treated as an S or C corp. The default treatment of an LLC at the federal level is to treat it (assuming it is owned by more than 1 person) as a partnership. Now let’s look at 2 recent cases.

3. In Renkmeyer, the Tax Court ruled that practicing lawyers in a law firm were subject to self-employment income on their distributive shares. In doing so, the court noted that all of the LLP’s income was generated by the services provided by its members, and thus it was clear that the partners’ distributive shares of the law firm’s income did not arise as a return on the partner’s nominal investment and were not “earnings which are basically of an investment nature.”

4. In Riether, a New Mexico district court granted the government’s motion for summary judgment on the issue of whether LLC members were subject to self-employment income on their distributive share of the LLC’s income. In that case, the LLC members, like the members of the LLC in the ILM, paid themselves a salary and received a W-2 from the LLC. This salary, they argued, made the LLC members employees rather than self-employed, and thus their distributive share of the LLC’s income, they reasoned, should escape self-employment tax. The district court was unconvinced, holding that the members’ treatment of some of the LLC’s income as wages did not change the character of the distributive share as self-employment income.

5. Furthermore, the court ruled that the exception found in IRC Section 1402(a)(13) did not apply to the LLC members because they “are not members of a limited partnership, nor do they resemble limited partners, which are those who lack management powers but enjoy immunity from liability for debts of the partnership.” Thus, the district court concluded, whether the LLC members were active or passive in the production of the LLC’s income, those earnings were self-employment income. As you can see, this approach was more expansive than the one taken by the Tax Court in Renkmeyer, where the court placed great weight on the amount of services provided to the LLP by its members. To the contrary, in Riether, it appears the district court was setting the tone that all LLC income should be subject to self-employment tax, regardless of the extent of the services provided by the LLC’s members.

6. Relying on the legislative history and the decisions in Renkmeyer and Riether, the IRS concluded in the ILM that the services provided by the management company LLC’s members were extensive, and that those services directly correlated to the income earned by the LLC from the funds. As a result, each member’s distributive share did not represent income which is basically of an investment nature that Congress intended to exclude from self-employment income when it enacted IRC Section 1402(a)(13). Thus, each LLC member was not a limited partners, and each member’s share of the distributive income was self-employment income.

Now what is interesting about this recent ruling is this. In the case that was considered in this ruling, the management company LLC had previously been an S corporation. Strangely enough, while both partnerships and S corporation are “flow-through entities” for tax purposes — i.e., the income of the entity is generally not taxed at the entity level, but rather at the partner/shareholder level on each investor’s distributive share– S corporations are treated differently for purposes of self-employment income.

Under Revenue Ruling 59-221, each shareholder’s distributive share of the S corporation’s income is not subject to self-employment income, regardless of the shareholder’s level of participation or services rendered. So in this case, the taxpayer argued that if the pass-through income of the predecessor S corporation management company had not been subject to self-employment tax, then why should the pass-through income of the LLC — which had the same role and business as the previous S corporation– be subject to self-employment tax? Hmmmmmm!

So while the ruling is specific to this case, there are some insights to be gained on the IRS’ new thinking on this. The take away is that if the LLC’s members provide significant services to the LLC, and it is those services that give rise to the majority of the LLC’s income, it is clear that the IRS is going to be prepared to argue that the LLC members are not limited partners for purposes of the exception from self-employment income found at IRC Section 1402(a)(13).

For more info visit us at –

http://advancedamericantax.com/irs-us-tax-singapore/ |