Skip to content

Skip to content

Tax year

The Portuguese tax year runs from 1 January to 31 December.

Basis of taxation – Charge to tax

- A charge to Portuguese tax is dependent on whether the income arises in Portugal and the extent of the charge will be determined by an individual’s tax residency status.

- A resident of Portugal is taxed on his worldwide income for the period of residency. A non-resident of Portugal is taxed on Portuguese source income only.

Residence and domicile

Exposure to Portuguese tax will be determined by the expatriate’s residence and domicile status. Tax residence in Portugal is determined by the expatriate’s actual presence within a tax year. The expatriate will be treated as Portuguese resident where:

- they spend 183 days or more in Portugal in any tax year

- they have stayed less than that period but on 31 December, live in Portugal and intend to continue doing so (eg own a dwelling in Portugal).

In both cases, it is important to note that once an individual becomes a Portuguese tax resident, their family (i.e. the spouse and dependent children) will also become Portuguese tax residents. If the spouse does not meet the conditions referred above, then the spouse must show proof that there is no connection between their majority of economical activity and the Portuguese territory. If this is the case, then they can be treated as a nonresident subject to taxation only for the income obtained in Portugal.

In this case the expatriate will file a tax return only with his/her Portuguese income and his/her part of the family income. Otherwise, they have to present joint tax returns.

NHR

Besides the above, the expatriate could opt to be considered as a non-habitual resident in Portugal, if meeting the following conditions:

- the expatriate must become a tax residence in Portugal, according to any of the criteria set out above

- obtain a tax residence certificate and also a certificate attesting the effective taxation abroad for the last five years

- the expatriate must not have been taxed in Portugal as a resident over the past five years.

The Portuguese Investment Tax Code (“Código Fiscal do Investimento”) was approved by Decree-Law no. 249/2009, of September 23. This diploma amended the Portuguese Individual Income Tax (“PIT”) Code establishing a favourable PIT regime for non-habitual resident individuals that qualify as resident for tax purposes in Portugal, and seeks to attract qualified expatriates to perform high added value activities, as well as other high net worth individual investors.

The habitual residents could benefit from a 20% rate on income from employment or self-employment (if it comes from the exercise of scientific or technical professions of high value) earned in Portugal, benefiting from exemption on the income earned abroad. This is provided that such income was subject to effective taxation at the state of source of that income, under the rules of the Double taxation agreement (DTA) between Portugal and the respective state of source. In relation to the passive income when earned abroad, it will be exempt from tax if

- it is not considered to be earned in Portugal,

- the source state is not included in the black-list and

- if it was subject to tax in the source state.

The tax regime applicable to the non-habitual residents in Portugal is applicable for a period of ten consecutive years.

A Portuguese tax charge arises on employment income derived from duties performed in Portugal. Income from employment includes all forms of remunerations as salary, wages, commissions, gratuities, overtime premiums bonuses, benefits in kind and other accessory fixed or variable remunerations of contractual nature or not.

I. INCOME FROM PORTUGUESE SOURCE

The non-habitual residents that obtain employment income (category A) and business or professional income (category B) in Portugal derived from high added value activities that are of a scientific, artistic, or technical nature are taxed at a flat rate of 20% applicable to the net amount of income earned. The taxpayers may exercise their option to subject this income to aggregation.

The Ministerial Dispatch no. 12/2010, of 7 January, defined what is to be understood by high added value activities of a scientific, artistic, or technical nature. As such, in the latter are included the activities developed by (i) architects, engineers and similar technicians; (ii) plastic artists, actors and musicians; (iii) auditors and tax consultants; (iv) doctors and dentists; (v) university professors; (vi) psychologists; (vii) liberal professionals, technicians and assimilated; and (viii) investors, administrators and company managers.

Remaining employment and business or professional income (not considered of high added value) and income of the remaining categories, shall be aggregated and taxed according to the PIT general rules.

There is also a requirement on the expatriate’s employer to deduct Portuguese payroll withholding tax from the assessable employment income.

Benefits (in kind)

In general, benefits in kind are subject to Portuguese tax (for the provision of a car to be taxable as the income of the worker, it is necessary that a written agreement attributing the benefit to the worker exists). Therefore, housing, meal allowances, provision of a car and relocation allowances will come within the charge to Portuguese income tax in addition to the individual’s salary. In the case of health or life insurance, those can be exempt if established for the majority of the employees and in an objective and identical criteria for all employees, while not belonging to the same professional class.

II. INCOME FROM FOREIGN SOURCE

CATEGORY A INCOME

Exempt from taxation:

(i) If the same is taxed in the State of origin according to the Double Tax Treaty entered into between Portugal and that State; or

(ii) if Portugal has not entered into a Double Tax Treaty with that State of origin, the income will be taxed in that State as long as the income cannot be considered as obtained in Portugal according to domestic law.

CATEGORY B INCOME FROM HIGH ADDED VALUE ACTIVITIES OBTAINED ABROAD BY NON-HABITUAL RESIDENTS, OR FROM INTELLECTUAL OR INDUSTRIAL PROPERTY, AS WELL AS, FROM PROVIDING INFORMATION REGARDING AN EXPERIMENT CARRIED OUT IN THE COMMERCIAL, INDUSTRIAL OR SCIENTIFIC AREAS, CAPITAL INCOME (CATEGORY E), REAL ESTATE INCOME (CATEGORY F) AND CAPITAL GAINS (CATEGORY G)

Exempt from taxation:

(i) if the income may be taxed in the State of origin according to the Double Tax Treaty entered into between Portugal and the State concerned (for ease of reference we attach hereto the list of countries with whom Portugal has a Double Tax Treaty); or

(ii) in case Portugal has not entered into between a Double Tax Treaty with the State of origin, the income may be taxed in conformity with the OECD Model Tax Convention (in this case, this exemption shall only apply if the State of origin is not considered a black listed jurisdictions and as long as the income cannot be considered as obtained in Portugal according to domestic law.

Any other type of Category B income obtained and not comprised in the NHR regime abroad and not derived from high added value activities will be taxed in Portugal according to the PIT general rules.

PENSIONS INCOME (CATEGORY H)

Exempt from taxation:

(i) if the same is taxed in the State of origin according to the Double Tax Treaty entered into between Portugal and that State; or

(ii) provided the income cannot be considered as obtained in Portugal according to domestic law.

Expatriate concessions

The only expatriate concessions available are with respect to diplomatic missions and cooperation agreements with other countries.

Relief for foreign taxes

Where income has been simultaneously subject to tax in Portugal and in a foreign jurisdiction, relief will always be granted by the Portuguese tax authorities in a manner similar to what is provided for in the relevant DTA (around 60 are included in the Portuguese net treaty).

Deductions against income

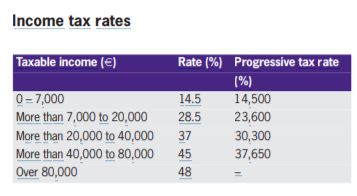

Certain expenses can be provided by an employer free of income tax up to a certain amount (e.g. meal and travel allowances). Limits are stipulated for the total amount deductible from taxable income as well as for the use of tax benefits contained in the tax benefits law. Both vary depending on the level of taxable income, as follows (please refer to income tax rates table):

- the limit on deductions from taxable income relates only to taxpayers whose taxable income is included in the last four income brackets being zero in the last one

- the limit with regard to tax benefits will apply from the second and following levels of income brackets.

What taxes?

Capital gains tax Capital gains are deemed to be the difference between the gains and the loss accomplished in the same year in respect of the same type of assets (real estate property, shareholding, etc.).

In the case of real estate property, capital gains earned by Portuguese tax residents will be taxed on only 50% of its amount, being subject to the progressive rates (from 14.5% up to 48%, plus a surcharge of 3.5%) depending on the level of the taxpayers income.

It must be stressed that capital gains obtained on selling immovable properties located outside Portugal are also subject to Portuguese personal income tax. Nevertheless, Portuguese net of tax treaties allows capital gains to be taxed in the country where the property is located, therefore taking those capital gains outside Portuguese taxation.

Capital gains obtained by non residents on the selling of Portuguese properties are subject to a flat rate of 28%. In both cases, the acquisition price is adjusted by a coefficient whenever 24 months have elapsed between the date of the sale and the date of the acquisition of the property.

Capital gains arising from disposal of shares are subject to a flat rate of 28%, applicable both to Portuguese tax residents and nonresidents.

Inheritance, Estate and Gift taxes

This tax has been abolished as from 1 January 2004. In some cases (not involving transmission from parents to children and vice versa), this tax was replaced by stamp duty at the rate of 10% applicable to the transmission of all types of assets.

Investment income

Dividends, interest and other financial incomes are subject to taxation once they become due or assumed to be due or when they are at the holder’s disposal. Such incomes are in many cases subject to withholding tax, which is always a final tax for non residents. It is important to note that dividends paid by Portuguese companies to Portuguese tax resident individuals, if aggregated with all other incomes, are taxed at only 50% of its amount. In this case, it is mandatory to aggregate all other financial income even subject to the flat rate. Otherwise, dividends are subject to a flat rate of 28%.

Local taxes – IMI

(municipal property tax)

Same rules as for IMT

(see ‘real estate tax’ below) are also applicable to IMI, which only considers immovable properties located in Portugal. Tax rates are 0.8% for non-urban properties and between 0.3% and 0.8% for urban properties.

Real estate tax – IMT (real estate transfer tax)

Any immovable property located in Portugal is subject to IMT, whether purchased by a resident or not. The purchase of urban property for dwelling purposes is not subject to IMT for values up to €92,407. For higher values, rates can go up to 6%. The purchase of non-urban properties is taxed on a 5% rate and other urban properties purchases are taxed on a 6.5% rate.

Social security taxes

Where duties are performed in Portugal, generally a charge to Portuguese Social Security (PSS) will arise. The expatriate will be treated as an employee and subject to PSS at 11%. The employer will also be required to contribute 23.75% of the relevant income and benefits to PSS. A new ‘Social Security Contributions Code’ entered into force on 1 January 2011, which expands the basis of the contributions and aligns the social security legislation more closely with the Personal Income Tax Law (IRS).

Travelling

expenses, representation expenses, personal use of the car, transport expenses, compensation due to contract termination are now subject to social security contributions. There are some specific provisions of the IRS on which social security contributions are calculated. Certain changes included in the social security law were postponed to 2014 in relation to certain provisions, namely the provision regarding different employer’s contribution rates (which currently stand at 23.75%), according to the kind of the employment contract.

This deferral includes an increase of the contribution rate by 3% (to 26.75%) for fixed term employment contracts and the reduction of the contribution rate by 1% (to 22.75%) for permanent employment contracts. There are some components of contributory base that started being considered in 2011, as provided for in the initial version of the law, but was implemented progressively: 33% in 2011; 66% in 2012 and 100% in 2013. PSS must be collected at source along with payroll taxes.

Where the expatriate is transferring from a EU jurisdiction and holds the relevant documentation an exemption to PSS will apply. Where the expatriate is transferring from a jurisdiction outside the EU with which Portugal holds a bi-lateral agreement and the expatriate holds the relevant documentation an exemption to PSS will apply. Where the expatriate is transferring from a jurisdiction that does not fall into one of the above categories, the PSS rules will determine their liability.

Stock options

Stock options can be taxed in the following moments:

- moment of acquisition – if the price of acquisition benefits the employee vis a vis third parties

- moment when the option is exercised or when the stocks are sold or the employee renounces to the right of such option in favour of the employer, if a gain is obtained (i.e. whenever there is a difference between the price of exercising or alienating such right and the price of the stock).

The Portuguese law considers that the worker’s income includes the benefits or privileges conferred by the employer to any of the worker’s family members.

Wealth tax

There is no wealth tax in Portugal.

Tax planning opportunities

Most tax planning involves the structuring of employment arrangements to take advantage of various tax concessions.

Other European Countries

Italy is very keen on well off non-doms, for example. Move there, and, while you have to pay ordinary income tax on income actually generated in Italy, the rest can be dealt with by one single lump sum payment of €100,000 a year regardless of how much you as a non-dom might actually have made. No income taxes, wealth taxes or local taxes due. The best bit is that you can hang on to this generous tax avoidance scheme for 15 years and (unlike in the UK regime) remit both assets and income to Italy anytime without incurring any new tax liabilities.

On to famously high-tax France. Anyone who relocates there to work and, in doing so, makes France their primary residence can end up partially exempt from French income tax for eight years. They are also exempt from the French wealth tax on all assets held outside France for the first five years for their residence.

Finally, I would point you to Denmark. You might think of it as a Scandi people’s paradise – a semi-socialist country always wise to rich people and their nasty tax avoiding tendencies. Not so. Move there and you can cut a deal too. How does a six-year flat rate of income tax at 32.84% sound? Its not as good as Portugal (nor as easily accessible) but meet the criteria and it will still leave you an awful lot better off than living in Corbyn’s Britain.

But please don’t be deceived by unqualified persons making sweeping statements about “no tax”. The fine print is very important. Get proper advice before making important decision.

Our US tax specialists in Portugal will be happy to answer any questions you may have.