Skip to content

Skip to content New European Commission proposals seek to crack down on the misuse of shell companies.

We have consistently warned against advisers who encourage structures with no commercial benefit. Structures that would be entered into solely for tax benefits. Such advisors are sadly out of touch and will cause their clients no end of pain

Just within the last few weeks, we’ve seen headlines like

- European General Court finds against Madeira Free Trade Zone scheme

- UK tables Economic Crime and Corporate Transparency Bill

- US issues final rule implementing the Corporate Transparency Act

- Hong Kong opens legislative process to implement OECD Multilateral Convention

- HMRC probes suspected tax evasion bank customers

Overview of the rules

The proposal sets out a series of tests and gateways that are intended to identify high risk entities that could be deemed ‘shell entities’. These are designed to establish whether an entity has a genuine economic link with its country of residence and sets a minimum level of activity to determine if there is misuse of an entity for tax avoidance purposes.

The European Union plans to introduce the Anti-Tax Avoidance Directive 3, or ATAD 3, early in 2024. That may seem some way off, but firms should start preparing now to avoid getting caught out.

Tax avoidance and evasion have come under intense EU scrutiny in recent years, particularly following the Panama Papers and other revelations, as well as Brexit.

The European Commission published a draft of ATAD 3 on 22 December 2021. It aims to prevent the use of shell companies for tax evasion and avoidance. The EU estimates that it loses about EUR 20 bn a year through misuse of shell companies.

As it stands, ATAD 3 will come into effect on 1 January 2024, but much is still unclear.

The proposals are expected to increase reporting requirements and compliance costs. They could affect holding companies resident in the EU that enjoy double tax treaty benefits but have only limited economic substance.

It’s important not to act prematurely by making sweeping changes until the directive’s final text becomes clearer. However, companies must make themselves aware of developments and determine whether their entities pass the “gateway tests” to identify whether they risk being classified as a shell company.

Broadly speaking, a shell entity is an entity lacking minimum economic substance which is misused for the purpose of obtaining tax advantages. The proposed directive is aimed at EU resident holding companies which claim benefits under double tax treaties and other EU directives but lack minimum economic substance. Consideration should be given to the new rules that ATAD 3 would introduce and their application to M&A transactions undertaken from 1 January 2022, as well as entities within current holding platforms and acquisition structures. This article summarises the key issues and their potential impact on current M&A activity and holding structures.

The proposed directive is aimed at EU resident holding companies claiming benefits under double tax treaties (DTTs) and other EU directives such as the Parent-Subsidiary and Interest and Royalty directives. In recent years, taxpayers have become familiar with an increased focus on a holding company’s purpose and its substance in, and nexus with, its territory of residence following the introduction of the Principal Purpose Test (PPT) into DTTs and recent EU case law in respect of access to the EU directives. Whilst these tests include an element of subjectivity, the ATAD 3 proposals attempt to apply a more prescriptive rule-based approach to assessing a company’s substance within a reporting framework.

Intro

Proposal

- Proposal for a Council Directive laying down rules to prevent the misuse of shell entities for tax purposes, COM(2021) 565 final

- Also called: “Unshell Directive” or “ATAD 3”

- Text was not carefully drafted

- Two-step “substance test” entailing denial of benefits under treaties, under the Parent/Subsidiary Directive and under the Interest/Royalty Directive as well as pass-through taxation at the level of shareholders

- Will cause great deal of effort also for companies that are not typical shell companies (allegedly only 0.3%), with only a small incremental benefit (cf. Judgement of 12 September 2006, Cadbury Schweppes, C-196/04, EU:C:2006:544: ATAD 1 and 2: MLI of the OECD); no de minimis-test

- Adoption by Member States by 30 June 2023, effective from 1 January 2024 (with a retroactive effect due to an observation period of two years); possibly one year later

- Legal basis: Art 115 TFEU (“approximation of such laws, regulations or administrative provisions of the Member States as directly affect the establishment or functioning of the internal market”) therefore unanimity requirement in ECOFIN; paradoxically, however, the functioning of the internal market will be hampered.

Scope

- Directive applies for all entities that are:

-

- engaged in an economic activity (likely includes asset management activities),

- tax resident in a Member State (under domestic law); and

- eligible to receive a tax residency certificate.

-

- Entities which are tax resident outside the EU are not within scope but will be under a further instrument likely to be passed in mid-2022

- Irrelevant

-

- legal form (e.g., foundations, trusts, or partnerships- provided they are tax resident in a Member State)

- group affiliation (e.g., also entities with individuals as shareholders)

-

Substance test

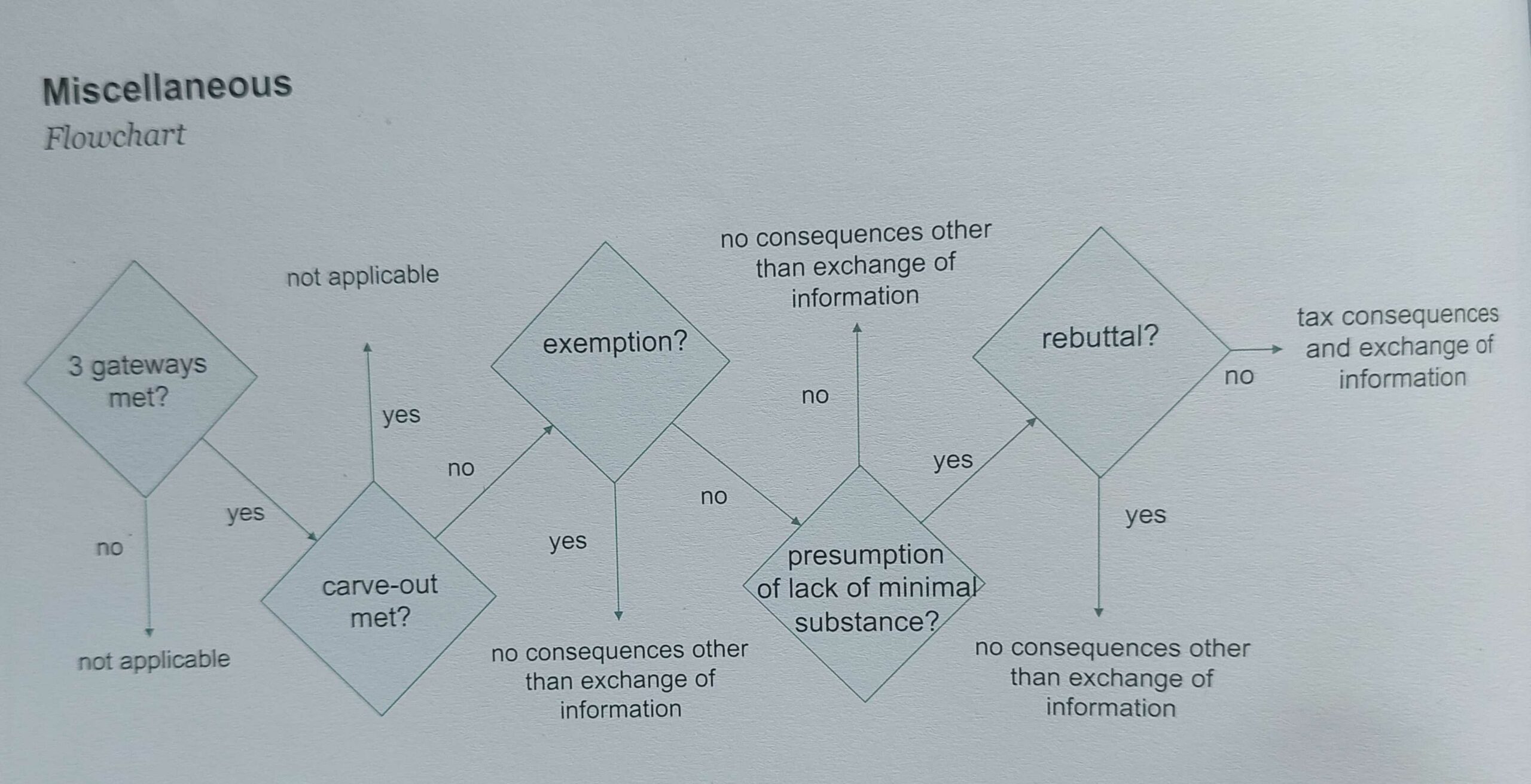

- Seven steps:

-

- undertakings that should report;

- reporting;

- presumption of lack of minimal substance for tax purposes.

- rebuttal;

- exemption for lack of tax motives;

- exchange of information

-

Step 1

Undertakings that should report – General

- An undertaking that should report (i.e., a risk case) exists if the following three criteria (so-called gateways) are cumulatively met:

-

- passive income;

- cross-border activities; and

- outsourced administration; and

-

- if the undertaking does not fall within the scope of the carve-out.

- Determination to be carried out by the taxpayer (= first step of the substance test).

Undertakings that should report – Gateway 1 (passive income)

- More than 75% of the revenues accruing to the undertaking in the preceding two tax years is relevant income

-

- interest or any other income generated from financial assets, including crypto assets, royalties or any other income generated from intellectual or intangible property or tradable permits, dividends and income from the disposal of shares, income from financial leasing, income from immovable property. income from movable property other than cash, shares or securities held for private purposes and with a book value of more than EUR 1 million, income from insurance, banking and other financial activities. income from services which the undertaking has outsourced to other associated enterprises.

- unclear: whether fulfilment is required in each of the two years or whether averaging is required (likely the latter), how to proceed in case of a newly established entity/migration and whether the term “tax year” is to be understood as the financial year.

-

- Furthermore, Gateway 1 is also considered to be fulfilled (note: book values under the following bullet points are not added) if:

-

- the book value of the following assets is more than 75% of the book value of the undertaking’s assets: immovable property and movable property other than cash, shares or securities held for private purposes (meaning basically every real estate company)

- the book value of the following assets is more than 75% of the book value of the undertaking’s assets: shares (meaning basically every holding company)

- unclear: basis for calculating the revenues and book value (local tax, local GAAP or IFRS)

-

Undertakings that should report – Gateway 2 (cross-border activities)

- Two alternative criteria:

-

- more than 60% of the book value of the undertaking’s immovable property and movable property other than cash, shares or securities held for private purposes was located outside the EU Member State the undertaking in the preceding two tax years; or

- at least 60% of the undertaking’s relevant income is earned or paid out via cross-border transactions (unclear whether the previous two tax years are also to be taken into account here)

-

- Purely domestic companies with no or little substance are therefore not within scope

Undertakings that should report – Gateway 3 (outsourced administration)

- In the preceding two tax years, the undertaking outsourced the administration of day-to-day operations and the decision-making on significant functions:

- the term “outsourced” is not defined in detail

- core activities appear to be relevant here and not ancillary activities (e.g., accounting should not be relevant)

- it appears irrelevant whether an undertaking’s administration is outsourced to affiliated companies of to external service providers

Undertakings that should report – Carve out

- Companies which have a transferable security admitted to trading or listed on a regulated market or multilateral trading facility – but not special purpose vehicles held by them;

- Regulated financial undertakings (banks, insurance companies pension funds, investment funds etc.) but not special purpose vehicles held by them;

- Undertakings that have the main activity (what is that?) of holding shares in operational businesses in the same (why is that?) EU Member State while their beneficial owners are also resident for tax purposes in the same (why is that?) EU Member State – shares may be held in other states provided they are predominantly held in companies of the same EU Member State;

- Undertakings with holding activities (what is that?) that are resident for tax purposes in the same EU Member State as the undertaking’s shareholder(s) or the ultimate parent entity (this is not the same as the above-mentioned “beneficial owner”) – this relates to e.g. sub-holdings in the same EU Member State:

- Undertakings with at least five own full-time equivalent employees or members of staff exclusively carrying out the activities generating the relevant income (apparently the employees’ tax residence is irrelevant)- it is unclear, whether ten 50% part-time employees would suffice.

Step 2

Reporting

- Reporting undertakings (ie., all three gateways are fulfilled and there is no carve-out) shall declare in their annual tax returns whether they meet the following indicators of minimum substance (= second step of the substance test):

-

- the undertaking has own premises in the EU Member State or premises for its exclusive use

- the undertaking has at least one own and active bank account in the EU

- one of the following indicators is given:

-

- one or more directors of the undertaking (i) are resident for tax purposes in the EU Member State of the undertaking, or at no greater distance from that EU Member State insofar as such distance is compatible with the proper performance of their duties; (ii) are qualified and authorized to take decisions in relation to the activities that generate relevant income for the undertaking or in relation to the undertaking’s assets; (iii) actively and independently use the authorization referred to above on a regular basis; (iv) are not employees of an enterprise that is not an associated enterprise; and do not perform the function of director or equivalent of other enterprises that are not associated enterprises, or

- the majority of the full-time equivalent employees of the undertaking are resident for tax purposes in the EU Member State of the undertaking, or at no greater distance from that EU Member State insofar as such distance is compatible with the proper performance of their duties, and such employees are qualified to carry out the activities that generate relevant income for the undertaking.

- Documentary evidence must be provided regarding:

-

- address and type of premises;

- amount of gross revenue and types thereof;

- amount of business expenses and types thereof;

- types of business performed to generate the relevant income;

- number of directors, their qualifications, authorizations and place of residence for tax purposes or the number of full-time employees performing the business activities generating relevant income and their qualifications and their place of residence for tax purposes;

- outsourced business activities; and

- bank account number, any mandates granted to access the bank account and to use or issue payment instructions and evidence of the account’s activity.

-

Step 3

Presumption of lack of minimal substance for tax purposes

- Presumption of existing substance: in the case of a reporting undertaking that

-

- declares in its annual tax return that it meets all the indicators for minimum substance, and

- provides satisfactory supporting documentary evidence

- Note: This presumption is not intended to prevent a Member State from applying other abuse rules

-

- Presumption of lack of minimal substance: in all other cases

Step 4

Rebuttal

- Possibility of rebutting the presumption by providing (at least) the following documents:

-

- a document allowing to ascertain the commercial rationale behind the establishment of the undertaking:

- Information about the employee profiles, including the level of their experience, their decision-making power in the overall organization, role and position in the organization chart, the type of their employment contract, their qualifications and duration of employment; and

- concrete evidence that decision-making concerning the activity generating the relevant income is taking place in the EU Member State of the undertaking.

-

- The presumption shall be deemed rebutted (for one and a maximum of another five years) if there is evidence that the undertaking has performed and continuously had control over, and borne the risks of the business activities that generated the relevant income or, in the absence of income, the undertaking’s assets

Step 5

Exemption for lack of tax motives

- Reporting undertakings can obtain an exemption from the obligations of the directive (for one and a maximum of another five years) if the undertaking provides sufficient and objective evidence that its interposition does not lead to a tax benefit for its beneficial owner(s) or the group as a whole.

- Such evidence shall include information on:

- the structure of the group and its activities; and

- a comparison of the tax burden with/without the intermediation of the reporting entity.

Step 6

Consequences – in the EU Member State of the undertaking

- The EU Member State shall deny a request for a certificate of tax residence to the undertaking for use outside the jurisdiction of this EU Member State.

- However, the undertaking is still considered resident for tax purposes and is subject to the domestic tax laws of this EU Member State (which is somehow also logical, because the non-issuance of a certificate of tax residence – only a means of proof – does not eliminate the status as a resident).

Consequences – in all other EU Member States

- Benefits from double taxation treaties (DTTs), from the Parent/Subsidiary Directive (PSD) and from the Interest/Royalties Directive (IRD) are to be disallowed to the extent that they apply due to the undertaking being deemed a resident for tax purposes (relevant for source state and residence state; concerns not only the relevant income, but also all other income – which seems excessive).

- The EU Member State of the undertaking’s shareholder(s) (this also applies to shareholders who are natural persons) shall (under treaty override) tax the relevant income earned by the undertaking at the shareholder level (arguably on a pro-rata basis) and deduct any tax paid on such income at the EU Member State of the undertaking. However, there is no credit if the payer of the income is not resident in an EU Member State (unclear why this should be so, and contradictory to the explanations).

- If the shareholders are not tax resident in the EU and the payer of the income is tax resident in the EU, then the source state has to levy taxes according to domestic tax laws taking into account a DTT that exists with the state of residence of the shareholders.

Consequences – in all other EU Member States

- In the case of immovable property held by an undertaking in an EU Member State as well as movable property held for private purposes, the following procedure must be followed (relevant for any wealth taxes):

-

- The EU Member State in which immovable property is located may tax it (treaty override) as if it were held by the shareholders.

- The EU Member State in which the shareholders are resident for tax purposes may tax immovable assets and movable assets held for private purposes (treaty override) as if they were held by the shareholders.

-

Consequences – Examples

Scenario 1: Debtor of payment in a third country, company and shareholders in the EU

EU

- The state of residence of the shareholders has to include the relevant income received by the company in the taxable income and to relieve the income originating from the source state on the basis of a DTT existing between the state of residence of the shareholders and the source state. Taxes paid by the company are not credited.

EU

- The company established in an EU member state is considered resident for tax purposes and is subject to domestic tax laws.

THIRD COUNTRY

- The source state is not bound by the directive and can therefore apply its domestic tax laws or a DTT existing with the shareholder’s state of residence to the outgoing payments.

Consequences – Examples

Scenario 2: Debtor of payment, company and shareholders in the EU

EU

- The state of residence of the shareholders has to include the relevant income received by the company in the taxable income and relieve the income originating from the source state on the basis of a DTT existing between the state of residence of the shareholders and the source state or the PSD or the IRD. The taxes paid by the company are to be credited.

EU

- The company established in an EU member state is considered resident for tax purposes and is subject to domestic tax laws.

EU

- The source state taxes the outgoing payments according to its domestic tax laws, taking into account a DTT that exists with the state of residence of the shareholders, the PSD or the IRD.

Consequences – Examples

Scenario 3: Debtor of payment and company in the EU, shareholders in a third country

THIRD COUNTRY

- The state of residence of the shareholders is not bound by the directive; but may apply a DTT in force with the source state.

EU

- The company established in an EU member state is considered resident for tax purposes and is subject to domestic tax laws.

EU

- The source state taxes the outgoing payments according to its domestic tax laws, taking into account a DTT existing with the state of residence of the shareholders.

Consequences – Examples

Scenario 4: Debtor of payment and shareholder in a third country, company in the EU

THIRD COUNTRY

- The state of residence of the shareholders is not bound by the Directive but may apply a DTT in force with the source state.

EU

- The company established in an EU member state is considered resident for tax purposes and is subject to domestic tax laws.

THIRD COUNTRY

- The source state is not bound by the directive and can, therefore, apply its domestic tax laws or a DTT existing with the shareholder’s state of residence to the outgoing payments.

Step 7

Exchange of information

- Automatic exchange of information with all other Member States regarding:

- the minimum substance indicators reported in the tax return;

- the rebuttal of the presumption; and

- the exemption.

Miscellaneous

Tax audit upon request/Penalties

Tax audit upon request

- the competent authorities of a Member State may initiate a tax audit in another Member State if there is reason to believe that an undertaking established there has not complied with the requirements of the directive.

- the tax audit must be initiated within one month of receipt of the request, and the result must be reported within one month of completion of the audit.

Penalties

- At least 5% of the turnover (i.e. not only the relevant income) of the undertaking subject to the reporting requirement in the relevant financial year.