Skip to content

Skip to content Let’s talk about Portfolio Interest Exemption

Fixed, Determinable, Annual, or Periodical (FDAP) income is all income, except:

- Gains derived from the sale of real or personal property (including market discount and option premiums, but not including original issue discount)

- Items of income excluded from gross income, without regard to the U.S. or foreign status of the owner of the income, such as tax-exempt municipal bond interest and qualified scholarship income

Income is fixed when it is paid in amounts known ahead of time. Income is determinable whenever there is a basis for figuring the amount to be paid. Income can be periodic if it is paid from time to time. It does not have to be paid annually or at regular intervals. Income can be determinable or periodic, even if the length of time during which the payments are made is increased or decreased.

Tax Treatment of FDAP Income Which is Not Effectively Connected Income (ECI)

Tax at a 30% (or lower treaty) rate applies to FDAP income or gains from U.S. sources, but only if they are not effectively connected with your U.S. trade or business. The 30% (or lower treaty) rate applies to the gross amount of U.S. source fixed or determinable, annual or periodical gains, profits, or income. Deductions and netting are not allowed against FDAP income.

The following items are examples of FDAP income:

- Compensation for personal services (such as commissions and gross proceeds from performances)

- Dividends

- Interest

- Original issue discount

- Pensions and annuities

- Alimony

- Real property income, such as rents, other than gains from the sale of real property

- Royalties

- Scholarships and fellowship grants

- Other grants, prizes and awards

- A sales commission paid or credited monthly

- A commission paid for a single transaction

- The distributable net income of an estate or trust that is FDAP income, and that must be distributed currently, or has been paid or credited during the tax year, to a nonresident alien beneficiary

- A distribution from a partnership that is FDAP income, or such an amount that, although not actually distributed, is includible in the gross income of a foreign partner

- Taxes, mortgage interest, or insurance premiums paid to, or for the account of, a nonresident alien landlord by a tenant under the terms of a lease

- Prizes awarded to nonresident alien artists for pictures exhibited in the United States

- Purses paid to nonresident alien boxers for prize fights in the United States

- Prizes awarded to nonresident alien professional golfers in golfing tournaments in the United States

- Payments to U.S. parties when a nonresident alien entertainer has rights to the performance

Social Security Benefits

U.S. source FDAP income includes 85% of any U.S. Social Security benefit (and the Social Security equivalent part of a Tier 1 railroad retirement benefit). This income is exempt under some tax treaties. Refer to Table 1 in Publication 901, U.S. Tax Treaties, for a list of tax treaties that exempt U.S. Social Security benefits from U.S. tax.

Capital Gains

If you were present in the United States for 183 days or more during the tax year, and you are still a nonresident alien, your net gain from sales or exchanges of capital assets is taxed at a 30% (or lower treaty) rate. For purposes of the 30% (or lower treaty) rate, net gain is the excess of your capital gains from U.S. sources over your capital losses from U.S. sources. This rule applies even if any of the transactions occurred while you were not in the United States. The183-day test mentioned above is not the same as the 183-day test used in the substantial presence test. See The Taxation of Capital Gains Of Nonresident Alien Students, Scholars and Employees of Foreign Governments for further information.

If you were in the United States for less than 183 days during the tax year, you will not be taxed on your capital gains, except for the following types of gains:

- Gains that are effectively connected with a trade or business in the United States during your tax year

- Gains on the disposal of timber, coal, or domestic iron ore with a retained economic interest

- Gains on certain contingent payments received from the sale or exchange of patents, copyrights, and similar property

- Gains on certain transfers of all substantial rights to, or an undivided interest in, patents

- Gains on the sale or exchange of original issue discount obligations

Many tax treaties contain provisions which reduce or eliminate taxation on capital gains.

What Capital Gains Are Taxed?

These rules apply only to those capital gains and losses from sources in the United States that are not effectively connected with a trade or business in the United States. They apply even if you are engaged in a trade or business in the United States. These rules do not apply to the sale or exchange of a U.S. real property interest, or to the sale of any property that is effectively connected with a trade or business in the United States.

Reporting Gains and Losses

Report your gains and losses from the sales or exchanges of capital assets that are not connected with a trade or business in the United States on Schedule NEC, Tax on Income Not Effectively Connected with a U.S. Trade or Business, of Form 1040-NR, U.S. Nonresident Alien Income Tax Return. Report gains and losses from sales or exchanges of capital assets (including real property) that are connected with a trade or business in the United States on a separate Form 8949, Sales and other Dispositions of Capital Assets, summarized on Schedule D (from Form 1040), Capital Gains and Losses, and page 1 of Form 1040-NR. Attach Form 8949 and Schedule D to Form 1040-NR.

Installment Payments

Income can be FDAP income whether it is paid in a series of repeated payments or in a single lump sum. For example, $5,000 in royalty income would be FDAP income whether paid in 10 payments of $500 each or in one payment of $5,000.

Insurance Proceeds

Income derived by an insured nonresident alien from U.S. sources upon the surrender of, or at the maturity of, a life insurance policy, is FDAP income. The proceeds are income to the extent they exceed the cost of the policy.

However, certain payments received under a life insurance contract on the life of a terminally or chronically ill individual before death (accelerated death benefits) may not be subject to tax. This rule also applies to certain payments received for the sale or assignment of any portion of the death benefit under contract to a viatical settlement provider. See Publication 525, Taxable and Nontaxable Income, for more information.

Racing Purses

Racing purses are FDAP income and racetrack operators must withhold 30% on any purse paid to a nonresident alien racehorse owner in the absence of definite information contained in a statement filed together with a Form W–8BEN, Certificate of Foreign Status of Beneficial Owner for United States Tax Withholding and Reporting (Individuals), that the owner has not raced, or does not intend to enter, a horse in another race in the United States during the tax year. If available information indicates that the racehorse owner has raced a horse in another race in the United States during the tax year, then the statement and Form W–8BEN filed for that year are ineffective. The owner may be exempt from withholding of tax at 30% on the purses if the owner gives you Form W–8ECI, Certificate of Foreign Person’s Claim That Income Is Effectively Connected With the Conduct of a Trade or Business in the United States, which provides that the income is effectively connected with the conduct of a U.S. trade or business and that the income is includible in the owner’s gross income.

Covenant Not to Compete

Payment received for a promise not to compete is FDAP income. Its source is the place where the promisor forfeited his or her right to act. Amounts paid to a nonresident alien for his or her promise not to compete in the United States are subject to withholding.

Signing On

A fee paid to a professional athlete, such as a soccer or hockey player for “signing on” with the effect of preventing any other team from negotiating with the player and preventing the player from negotiating with any other team is pay for a covenant not to compete. The source is the place where the right to play is given up. If a league is made up of both foreign and U.S. teams, the fee is from sources partly in and partly outside the United States. The part of the fee that is from U.S. sources is subject to withholding. If there is no reasonable basis for an allocation of the fee, the entire sign-on fee is income from the United States and is subject to withholding.

Summary on FDAP

The general rule is that the interest payments to the foreign parent are FDAP and subject to a 30% withholding tax. The 30% withholding is required to be paid directly to the IRS before the interest is paid offshore. Thus, the parent corporation would only receive 70% of any interest paid. There are two exceptions to the general rule, the portfolio debt exception and certain preferential tax treatment based on a treaty between the US and the jurisdiction of the parent corporation.

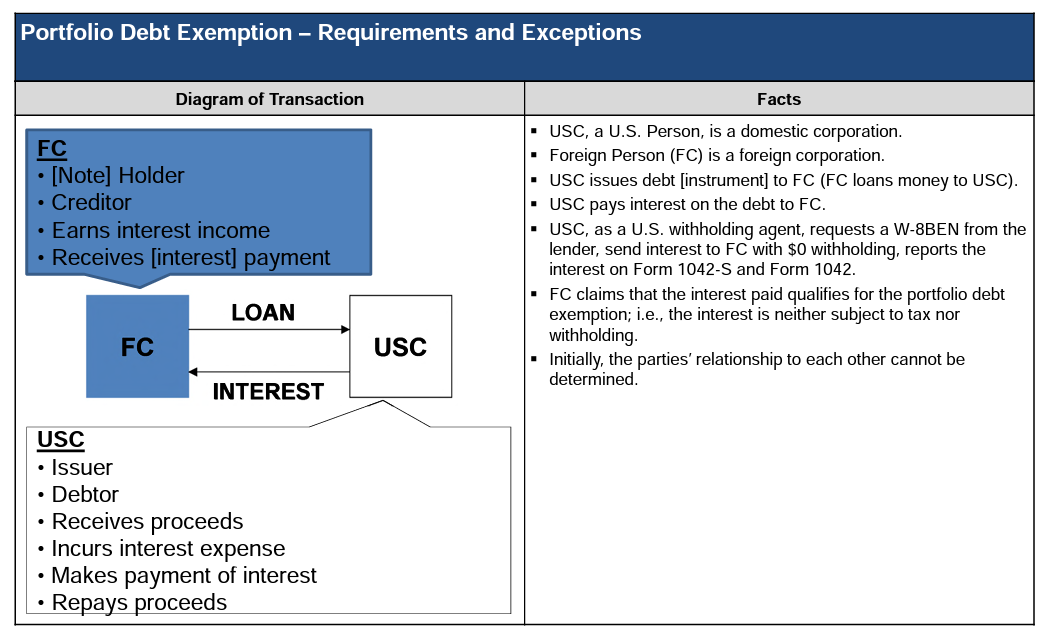

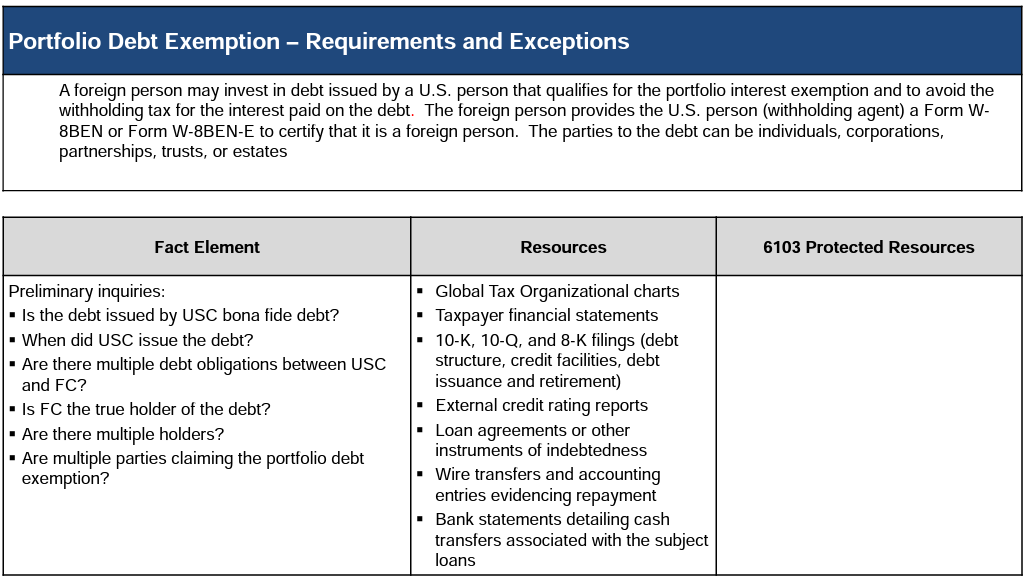

Portfolio Debt Exception

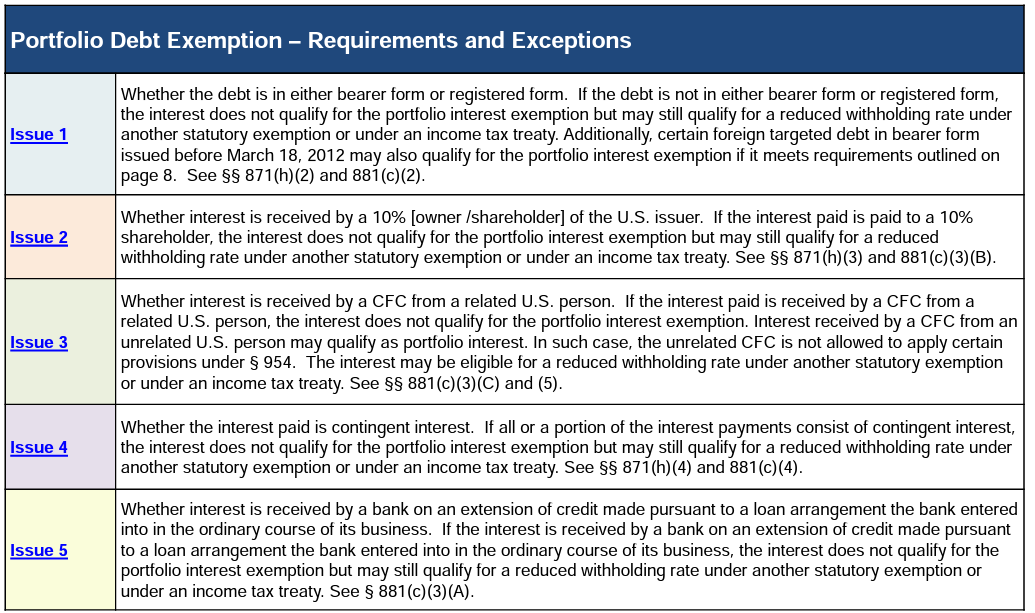

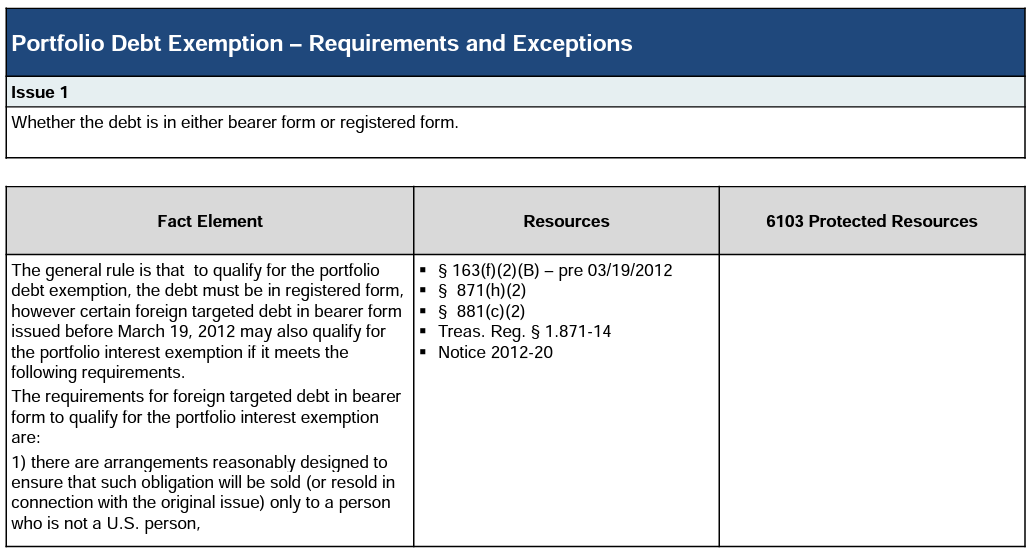

Portfolio interest is entirely exempt from the 30% US withholding tax. To qualify as portfolio interest, the loan must be from a foreign lender and the following requirements must be met:

- The interest is paid on debt that is in registered form.

- The loan cannot be from a bank lending in the ordinary course of business.

- The foreign lender does not own 10% or more of the voting stock of the blocker corporation directly or indirectly.

- The interest payments cannot be contingent.

The portfolio debt exception does not rely on any treaty. Therefore, it applies to lenders from any foreign country.

Ten Percent Voting Stock Ownership Rule.

Most of the structuring to qualify for the portfolio exemption revolves around making sure that the foreign lender does not own 10% or more of the voting stock of the blocker corporation either directly or indirectly. The 10% testing is done at the shareholder level of the foreign parent and the shareholders are considered to proportionately own stock held by that corporation. In testing for ownership, there are attribution rules that apply and can make the calculations quite complex. For example, a son is deemed to own the stock held by his father, any person holding options to purchase stock are treated as owning the stock, partners in a partnership are deemed to hold a ratable share of the stock held by the partnership, etc.

For planning it is essential that the blocker receive a schedule prepared by the owner of the voting shares at the inception of the transaction and annual updates to assure the foreign lender does not own 10% of the voting shares directly or indirectly. If it later turns out that the foreign lender owns 10% of the voting shares of the blocker, then the blocker will have secondary liability for taxes not withheld.

Contingent Interest

If all or a portion of the interest payments consist of contingent interest, the interest does not qualify for the portfolio debt exception, but may still qualify for a reduced withholding rate under an income tax treaty.

Contingent interest is defined as any interest if the amount of such interest is determined by reference to:

- Any receipts, sales, or other cash flow of the blocker

- Any income or profits of the blocker

- Any change in value of any property owned directly or indirectly by the blocker

- Any partnership or LLC distributions received by the blocker

Treaty Exception

The interest may still be exempt or subject to a reduced tax rate under an income tax treaty even if the portfolio debt exception does not apply. If a treaty provision is used, the foreign corporate lender can own 10 percent or more of the voting stock of the blocker. Contingent interest does not qualify under the portfolio interest exception. However, some treaties allow contingent interest to be tax free.

FDAP and FATCA IRS Foreign Status Forms

The blocker needs to receive a completed and signed Form W-8-BEN-E from the foreign lenders notifying it of the lenders foreign status to comply with the FDAP withholding rules and the FATCA requirements. Under the FATCA rules, the 30% withholding tax is required unless the W-8BEN-E form has been properly filled out and provided to the withholding agent prior to the interest being paid. Some of the information that must be provided on the form are the foreign lenders FDAP and FATCA status codes, and their global identification number. The withholding agent does not file this form with the IRS, but they will keep it in their files in case audited by the IRS. The W-8BEN-E also needs to be updated every three years. If the blocker cannot produce the W-8BEN-E on audit, the IRS will assess the 30% withholding tax.

Annual Tax Forms for Foreign Person’s US Source Income Subject to Withholding

The blocker will prepare and file IRS Forms 1042 and 1042S annually, informing the IRS of the amount of interest it paid the foreign lenders. Any exemption or reduced rate of withholding will be noted on the form when filed. The forms also provide the IRS the FATCA information that it requires.

Conclusion

Foreign corporate parent lenders to inbound US real estate blockers can avoid withholding tax under the portfolio debt exception or a tax treaty with proper tax structuring, documentation and compliance. It is important to make sure everything is in order and properly documented prior to any interest payment being made.

source: https://www.irs.gov/pub/int_