Skip to content

Skip to content

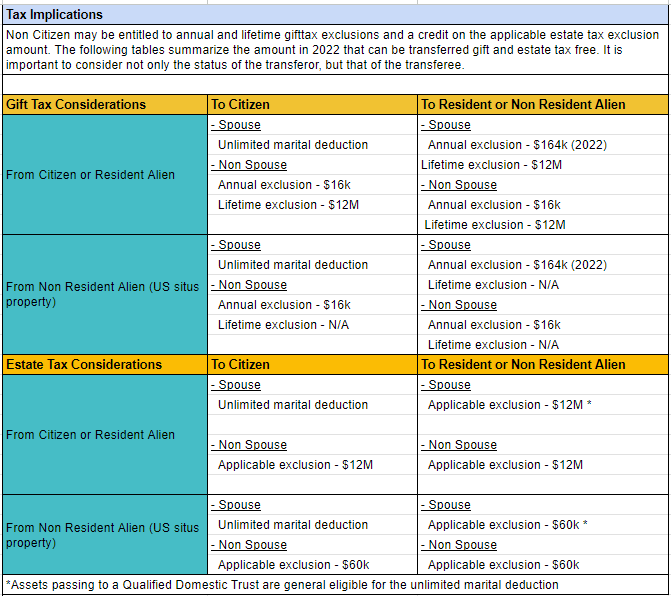

| Tax Implications | ||

| Non Citizen may be entitled to annual and lifetime gifttax exclusions and a credit on the applicable estate tax exclusion amount. The following tables summarize the amount in 2022 that can be transferred gift and estate tax free. It is important to consider not only the status of the transferor, but that of the transferee. | ||

| Gift Tax Considerations | To Citizen | Non Resident Alien”}”>To Resident or Non Resident Alien |

| From Citizen or Resident Alien | – Spouse | – Spouse |

| Unlimited marita deduction | Annual exclusion – $164k (2022) | |

| – Non Spouse | Lifetime exclusion – $12M | |

| Annual exclusion – $16k | – Non Spouse | |

| Lifetime exclusion – $12M | Annual exclusion – $16k | |

| Lifetime exclusion – $12M | ||

| From Non Resident Alien (US situs property) | – Spouse | – Spouse |

| Unlimited marital deduction | Annual exclusion – $164k (2022) | |

| – Non Spouse | Lifetime exclusion – N/A | |

| Annual exclusion – $16k | – Non Spouse | |

| Lifetime exclusion – N/A | Annual exclusion – $16k | |

| Lifetime exclusion – N/A | ||

| Estate Tax Considerations | To Citizen | To Resident or Non Resident Alien |

| From Citizen or Resident Alien | – Spouse | – Spouse |

| Unlimited marital deduction | Applicable exclusion – $12M * | |

| – Non Spouse | – Non Spouse | |

| Applicable exclusion – $12M | Applicable exclusion – $12M | |

| From Non Resident Alien (US situs property) | – Spouse | – Spouse |

| Unlimited marital deduction | Applicable exclusion – $60k * | |

| – Non Spouse | – Non Spouse | |

| Applicable exclusion – $60k | Applicable exclusion – $60k | |

| *Assets passing to a Qualified Domestic Trust are general eligible for the unlimited marital deduction | ||