Skip to content

Skip to content

We have written dozens of articles on UK tax in the past –

We have even written about the ideas a non UK citizen should consider from a tax perspective when moving to the UK from a low tax jurisdiction –

https://htj.tax/2020/08/moving-from-singaporeto-uk/

But what if someone is a UK citizen who has lived outside of the UK for decades and is now considering a return?

Naturally their main concern would be their domicile as they would want to be taxed on the remittance basis – https://htj.tax/2018/03/uk-tax-arising-vs-remittance-basis/

But how would their domicile be determined? Domicile is a complex discussion that is beyond the scope of this article. However, we would try to provide a light introduction.

- What is domicile?

1.1 Domicile is a specific UK law concept which is different from US domicile or “domicile” in some European countries.

1.2 Your domicile affects your legal status, for example, your ability to make gifts and the law which applies to inheritances from your estate.

1.3 Domicile, along with residence, is also crucial in working out your UK tax liability. Special, beneficial rules apply to those who are not domiciled in the UK.

1.4 Everybody must have a domicile at all times and you can only have one domicile at a time (unlike residence where you may be resident in more than one country).

1.5 Domicile is associated with a particular system of law so, although, for convenience, we talk about “UK domicile” or “US domicile” you would be domiciled in, for example, England and

Wales or Scotland or the State of New York or the State of California.

Depending on your perspective, in England there are either 3 or 4 types of domicile – domicile of origin, choice, dependence and deemed domicile.

Domicile of origin

You acquire a domicile of origin at birth. This is usually the same as the domicile of your father at that time, that is, the country that your father considered to be his permanent home at the date of your birth. As a result, your domicile may not be the country where you were born.

If your parents were not married when you were born, you will take your domicile from your mother. If you are adopted, you take your domicile from your adopted father – if there is no adopted father, you take the domicile from your adopted mother.

It is very difficult to displace your domicile of origin. Indeed, your domicile of origin is retained permanently, unless it is superseded by a domicile of dependence or a domicile of choice. Your domicile of origin also returns if you acquire a domicile of choice which then ceases but you have not yet made a new domicile of choice.

Most migrants to the UK are likely to have a domicile of origin outside the UK, meaning that they are not domiciled in the UK (known as ‘non-dom’). Unless you choose to remain in the UK permanently or indefinitely, and sever ties with your original country of domicile or origin, you will probably continue to be not domiciled in the UK. However, if you were originally born in the UK or if you remain in the UK for more than 15 years, then you will be deemed to be domiciled in the UK.

Domicile of dependence

Until you reach the age of 16, your domicile follows that of the person on whom you are legally dependent – if that person changes their domicile (through choice) then yours will also change.

If you were married before 1 January 1974, the wife would automatically acquire the domicile of her husband.

Domicile of choice

From the age of 16 (earlier in Scotland), an individual may be able to acquire a new domicile. This is called a domicile of choice. In order to acquire a domicile of choice, you must demonstrate the following:

- You have settled permanently in the country in which you now consider yourself domiciled;

- You must intend to stay there for the rest of your life;

- Generally, you must break your ties with the country of your domicile of origin. You do not necessarily have to become a UK citizen or passport holder but these factors will be taken into account.

You will have to prove that you have chosen to live in the new country on a permanent basis and provide strong evidence of your intention to stay there permanently or indefinitely.

Factors such as your intentions (for example, where you intend to retire),

- your Will,

- your permanent place of residence, and

- your business, social and family commitments

will be taken into consideration when looking at whether you have acquired a domicile of choice.

In most cases it will be fairly obvious what your domicile status is, but it can be very complex in some cases. If a lot of tax is at stake, you should seek professional help.

You cannot abandon your domicile of origin. This is always there in the background.

You can abandon a domicile of choice by:

– Leaving the country of domicile.

– With the intention that it will no longer be your permanent home.

If you abandon a domicile of choice then one of two things will happen:

– If you immediately settle on a permanent basis in a new country you may acquire a new domicile of choice in that country.

– If you do not immediately acquire a new domicile of choice, your domicile of origin will “revive” i.e. you will be regarded as domiciled in the country of your domicile of origin even if you have never lived there and have no connections with it.

Deemed domicile

Since 6 April 2017, HMRC treats some individuals who are not UK domiciled as if they are domiciled in the UK for income tax and capital gains tax purposes.

This affects you if:

- you are domiciled outside the UK, but you were born in the UK with a UK domicile of origin; or

- you have been resident for tax purposes in the UK for at least 15 of the previous 20 tax years.

The effect of being UK resident in a tax year and deemed domiciled in the UK for income tax and capital gains tax purposes is that you are chargeable to UK tax on your worldwide income and gains on the arising basis in the same way as individuals who are actually UK resident and UK domiciled.

Deemed domicile is a concept which applies for tax purposes only.

– If you are a UK domiciliary who wants to emigrate abroad, you will need to change your actual domicile by moving to the new country and making a life for yourself there.

– Even if you succeed in changing your actual domicile, you will be treated as remaining “deemed domiciled” for UK inheritance tax purposes for a further three years from the time of change.

– You should therefore avoid doing any estate planning in the early years after you have emigrated without obtaining UK advice. Planning which works in one country may create liabilities in another.

– If you are a person who is living in the UK but who is not actually domiciled in the UK you will become “deemed domiciled” for all tax purposes once you have been resident in the UK in at least 15 tax years out of the 20 tax years immediately before the year in question.

– In practice, this means that if you come to the UK and live here you will become deemed domiciled at the beginning of the 16th tax year from that time. Note that if you leave the UK in year 15 you will still become deemed domiciled in year 16.

– If you are a non-domiciliary who has become deemed domiciled through long residence, you can lose deemed domicile status for inheritance tax purposes by becoming non-resident for three complete tax years, provided you do not return in the fourth year. For income tax and capital gains tax purposes you would need to remain non-resident for six complete tax years.

Formerly domiciled residents

- If you were born in the UK and you had a UK domicile of origin but subsequently become domiciled in a country outside the UK, special rules apply. It does not matter whether you were

taken to live abroad by your parents when you were young or if you emigrated as an adult. - If you remain non-UK domiciled but become UK resident at any time, you are regarded as a “formerly domiciled resident” and none of the beneficial rules which normally apply to nondomiciliaries

apply to you whilst you are UK resident. - So if you become UK resident:

- You will immediately be subject to income and capital gains tax on your worldwide income and capital gains.

- If you set up a trust after becoming non-domiciled and you or your husband or wife can benefit from it, you will be subject to UK tax on all the trust’s income and capital gains.

- Inheritance tax consequences do not apply for the first tax year in which you are resident but will apply from the second tax year. From then on:

(a) In the event of your death whilst resident in the UK, your worldwide estate

would be subject to inheritance tax. Any assets held in a trust which you

created and from which you can benefit would be treated as if you still owned

them and would be taxable.

(b) Any trust you created would be subject to the normal trust charges [(see the

Appendix “Tax on trusts made by UK domiciled individuals”)] even if the

assets are non-UK assets.

Once you become non-resident again, your non-domiciled status is respected and you are taxed in the same way as any other non-resident non-domiciled individual.

How do I tell HMRC what my domicile status is?

In the UK, you self-assess your residence and domicile status. If you are someone who is required to submit a tax return, you will need to complete the SA109 ‘Residence, remittance basis etc.’ supplementary pages if your domicile status is relevant to the entries on your tax return (for example, if you are claiming the remittance basis and have left out your foreign income and gains on the basis that they have not been remitted).

You should note that you could be subject to a potential enquiry by HMRC if they wish to challenge the position you have taken.

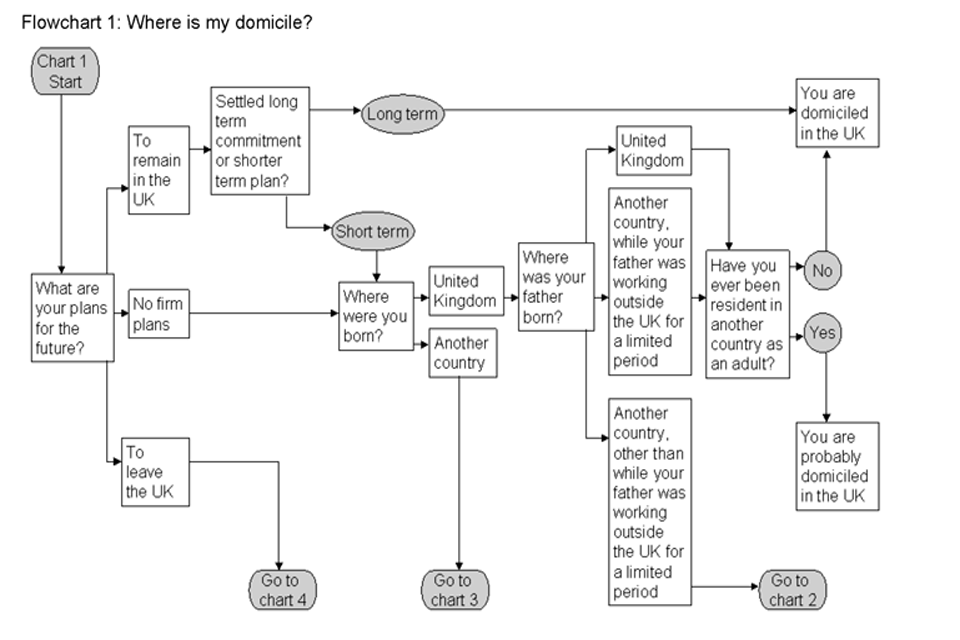

There are some helpful flowcharts on HMRC’s website. But please note that they are guidelines and not definitive given that rules around domicile are heavily influenced by case law as opposed to pure legislation.

Notes to domicile flowcharts

- Your domicile status depends on the facts of your individual case. The flowcharts will give as strong an indication as possible, based on various generic factors. However, if your affairs are more complicated the flowcharts may not provide a definitive answer.

- Your domicile status may be dependent on someone else’s domicile (usually your father’s). The flowcharts each provide a sequence of questions without reference to domicile itself to reach a conclusion showing what your likely status will be.

- If your parents were not married at the time of your birth, references in the flowcharts to ‘father’ should be read as ‘mother’.

- If you were adopted, ‘father’ should be read as ‘adopted father’.

- If your father’s domicile status changed when you were a child, you should not use the flowcharts, as the apparent conclusion could be misleading.

- If, when using the flowcharts, you arrive at the conclusion you’re ‘domiciled in the UK’ or ‘probably domiciled in the UK’ you may simply accept that conclusion. If you do, you should not tick the ‘non-domiciled’ box on form SA 109 (Residence, remittance basis etc. Self Assessment supplementary page). You will then be taxed on the arising basis.

- If the flowchart leads you to the conclusion that you’re ‘domiciled outside the UK’ or ‘probably domiciled outside the UK’, you may feel that this confirms your own view. Or, you may consider consulting the RDRMor a professional advisor.

- Your domicile relates to a particular territory. In most cases, this will be a country, but in federal countries, such as the USA and Australia, it relates to the individual state. Although the UK has 3 territories for domicile purposes, it does not operate as a federal system.

This image shows flowchart 1: where is my domicile?

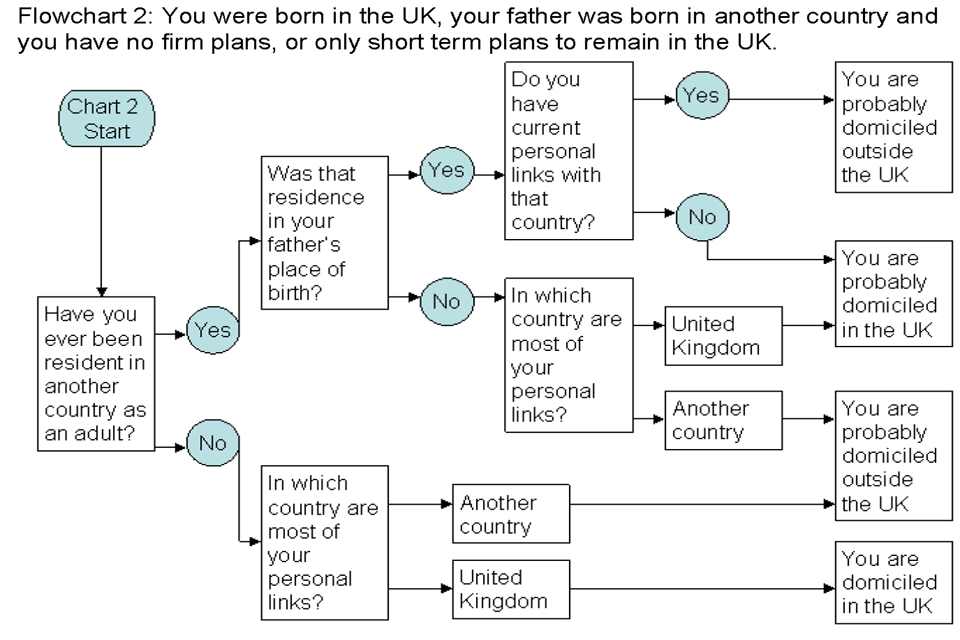

This image shows flowchart 2: you were born in the UK, your father was born in another country and you have no firm plans, or only short term plans to remain in the UK.

Example 5

Catherine is living in the UK and has no firm plans about where she will live in the future. She was born in Scotland. Her father was born in Sweden and her grandfather and ancestors were Swedish.

Catherine’s father was a business executive and the family lived in various countries, of which the UK was one. A musician, she has lived in several countries as an adult, but not yet in Sweden. Catherine is an only child. Her parents are dead and she has one surviving aunt. She rarely visits her family in Sweden. Her profession and lifestyle mean that she develops links with the place in which she is living.

Catherine uses flowchart 2 and concludes that she is probably domiciled in the UK. Given this, and the possibility that neither she nor her father ever settled anywhere outside Sweden, she might wish to consult more detailed guidance or seek the opinion of a professional adviser.

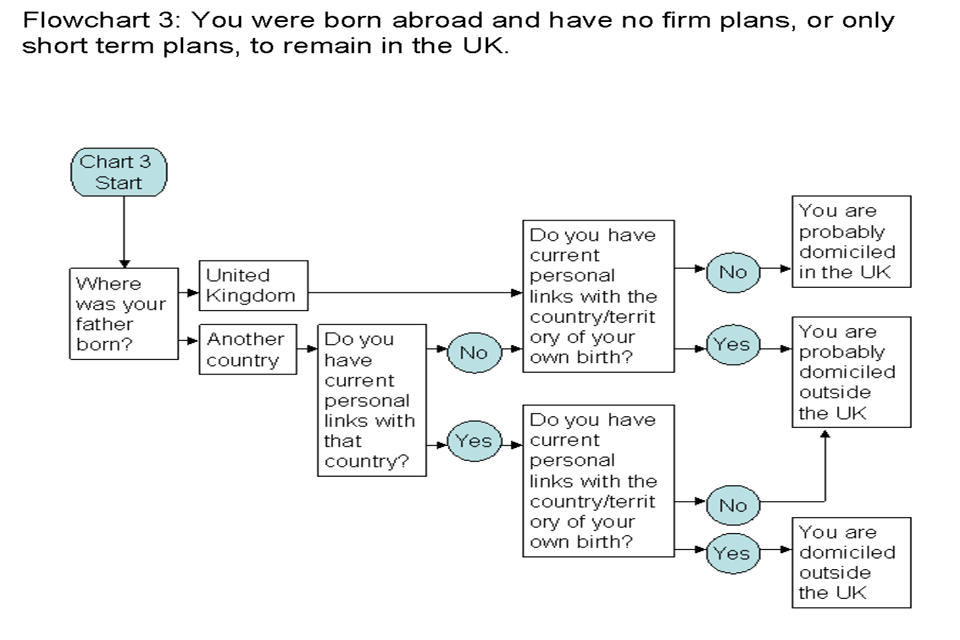

This image shows flowchart 3: you were born abroad and have no firm plans, or only short term plans, to remain in the UK.

Example 6

Daniel was born in New South Wales. He lives in England and intends to stay for at least another 2 years. Daniel follows the link from flowchart 1 to flowchart 3.

Daniel’s father was Greek. Daniel has retained few links with Greece; he visits his family once every 2 or 3 years. His 2 sisters have lived in Western Australia for many years and his widowed mother lives there with his elder sister. Daniel owns property in Western Australia and has an interest in a business there. The family has little connection with New South Wales, although Daniel is in touch with a couple of childhood friends there.

Daniel finds it difficult to reach a conclusion about his domicile, as he has links with Australia but not specifically with New South Wales. He consults detailed guidance and realises that his current intentions cannot be considered in isolation. Daniel realises that his residence in the UK for over 30 years and his intentions during that period have to be taken into account.

Daniel concludes that he is domiciled in the UK (the result flowchart 1 would have given him if he had considered his long-term UK commitment from the outset). This is reinforced by Daniel’s relative lack of links with the territory of his birth.

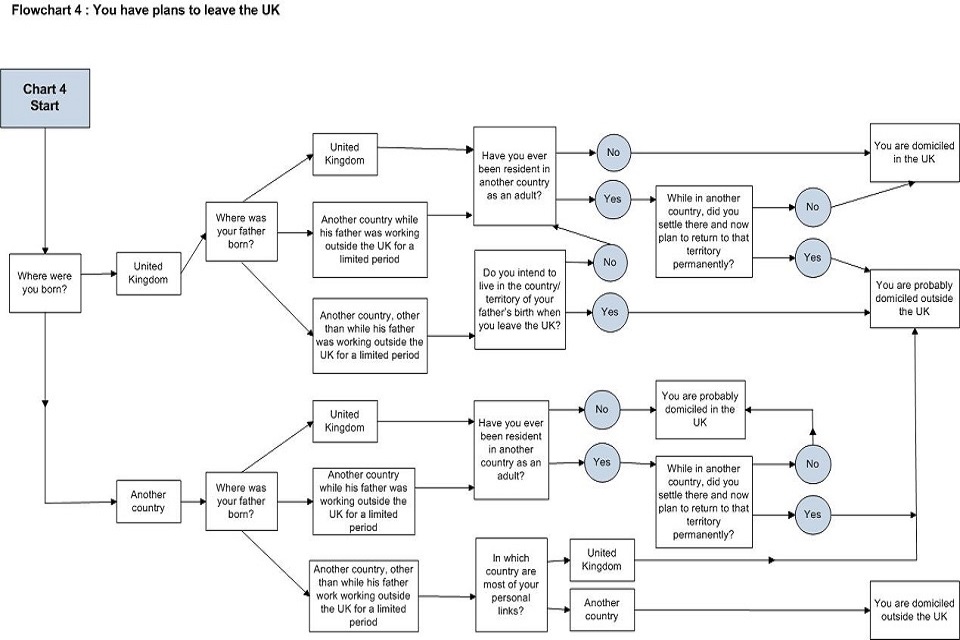

This image shows flowchart 4: you have plans to leave the UK.

Example 7

Aleksy, an electrician, was born in Poland and intends to return there in 3 or 4 years. His family background is Polish and his immediate family live in Poland.

Brian, an investment banker, was born in New York and intends to retire to France at the age of 60, just over 5 years from now. He has lived in London for much of his life, although he has spent several periods living abroad because of his employment.

Both Aleksy and Brian consider flowchart 1 and conclude that they should go to flowchart 4.

Both were born in another country; each must consider his father’s place of birth. Aleksy’s father was born in Poland; his grandfather lived his entire life in Poland, just as several generations of his family had done. Brian’s father was born in Ireland, into a wealthy family the members of which divided their time between Ireland and England.

Aleksy believes that most of his personal links are with Poland and concludes that he is domiciled outside the UK. (Aleksy is typical of the majority of individuals who come to live and work in the UK without intending to remain here indefinitely).

Brian has personal links with England, Ireland, France and New York. He thinks that, on balance, most of his personal links are with England but reaches the conclusion that he is probably domiciled abroad. Brian recognises that this is an indication of his domicile status and, because of his more complex circumstances, consults HMRC’s more detailed guidance and then seeks the views of a professional adviser.

Example 8

Ethan was born in the UK and has lived here all his life apart from a year spent travelling around Europe and annual holidays spent abroad. His father was also born in the UK. Ethan plans to retire to France and has already purchased a house there which he, and his entire family visit whenever they can.

While Ethan has clear and firm plans to move to France he is currently domiciled in the UK and flowchart 4 leads him to that answer.

RESIDENCE

UK Tax Residence

1.1 Residence for tax purposes in the UK is determined under the “Statutory Residence Test”, which was introduced with effect from 6 April 2013.

1.2 Before 2013, residence was a matter of case law and HMRC practice and the position could be uncertain.

1.3 It is important to pinpoint exactly when you become UK resident as this can have a knock-on effect on your future tax liabilities. It is particularly important to get advice on this if you came to, or left, the UK before April 2013.

2 How the Statutory Residence Test works

2.1 There are three separate parts to the Statutory Residence Test. Each part has to be applied in order. If a particular part determines your residence, you do not need to consider anything else. The parts are:

2.2 Part 1: Are you automatically non-resident?

2.3 Part 2: Are you automatically UK resident?

2.4 Part 3: If you are not automatically non-resident and not automatically UK resident, do you pass the “sufficient ties test”? (If you pass the sufficient ties test, you are UK resident.)

3 Points to note

3.1 The UK tax year runs from 6 April in one year to the following 5 April.

3.2 Strictly, you are either resident for the whole tax year or not resident for the whole year. If you come to the UK or leave the UK part-way through a year, you may be eligible for “split year treatment”. If you satisfy the conditions for split year treatment, you are treated as resident during the period when you are in the UK and not resident for the part of the year when you are not in the UK.

3.3 The conditions are complex and split year treatment is not available to everyone so you will need advice about your particular circumstances.

3.4 You might also be resident in another country as well as the UK. In most cases, there will be a double tax agreement between the UK and the other country which will contain rules which will allocate your residence to one country or the other. The double tax agreement also contains rules which prevent you paying tax in both countries or, at least, allows you to deduct the tax paid in one country against the tax payable in the other. Relief under a double tax agreement must be claimed so it is important to know whether you are resident in another country and what your potential tax liabilities might be.

3.5 The Statutory Residence Test applies in a different way to “arrivers” and “leavers”.

3.6 You will be an “arriver” if you have not been resident in the UK in any of the three tax years before the one when you arrive.

3.7 You will be a “leaver” if you have been resident in any of the three previous tax years.

3.8 The number of “days” you spend in the UK is critical. For this purpose, a “day” is a day when you were in the UK at midnight. So if you arrive at 10 a.m. on Monday and leave at 11 p.m. on Tuesday, you have been in the UK for one day. If you arrive at 10 a.m. on Monday and your flight leaves at 11.45 p.m. on Monday, you have not spent a day in the UK at all. Midnights spent in transit e.g. in an airport hotel do not count.

4 The Automatic Non-Residence Test

4.1 An arriver who spends up to 45 days in the UK in a tax year is automatically non-resident.

4.2 An arriver who spends 46 or more days in the UK and who does not “work full time abroad” must apply the other parts of the test.

4.3 A leaver who spends no more than 15 days in the UK will automatically be non-resident for the tax year. A leaver who spends more time than this in the UK and who does not work full time abroad will also need to consider the other parts of the test.

4.4 An arriver or leaver who works full time abroad will automatically be non-resident.

4.5 “Full time work abroad” has a technical meaning but, very broadly, the individual must work, on average, at least 35 hours a week abroad and must spend no more than 90 days in the UK of which no more than 30 days can be spent working in the UK. Any break from work must not exceed 30 consecutive days.

5

Automatic UK Residence

5.1 A person who spends 183 days or more in the UK during a tax year will always be resident here.

5.2 A person who “works full time” in the UK will also be resident. Again, this involves a technical definition which has to be considered carefully. The requirements are similar to overseas work but it is assessed over a one-year period of which only one day needs to fall within the tax year being assessed and at least 75% of the total work days in the year must be spent working in the UK.

5.3 A person who has their “only home” in the UK will be UK resident if they visit it on at least 30 days in the tax year. For this purpose, a visit of any length counts as a day. So a visit to pick up post or check on the central heating would count.

5.4 If you also have a home outside the UK you could still be automatically UK resident if you visit your overseas home on fewer than 30 days in the tax year.

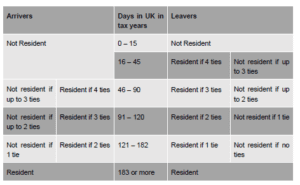

6 The Sufficient Ties Test

6.1 The Sufficient Ties Test looks as a combination of the number of specified “ties” and the number of days spent in the UK. Only the statutory ties matter so any other connections with the UK are ignored, however strong.

6.2 The statutory ties are as follows:

6.2.1 You will have a “work tie” if you work in the UK on 40 or more days in the tax year. For this purpose, a day’s work means at least three hours. “Work” is not defined but can include dealing with work emails, making phone calls, reading papers before a

meeting, attending meetings and travelling to them, training and so on.

6.2.2 You will have a “family tie” if your spouse or civil partner, unmarried partner of either sex or child under the age of 18 is resident in the UK. There are additional rules about children who attend school or university in the UK or where you see your child mostly outside the UK.

6.2.3 You will have a “90 day tie” if you have spent more than 90 days in the UK in either of the previous two tax years.

6.2.4 You will have an “accommodation tie” if you have accommodation in the UK which is available to you for at least 90 days and if you in fact spend at least one day (midnight) at the accommodation. You do not need to own or necessarily rent the property for it to be “accommodation”. For example, if a room were available in your parent’s or child’s house, that could be accommodation. However, you are allowed to spend up to a fortnight at the home of a close relative without it counting as a tie. If you take a

three month block booking on a room in a hotel, that could be accommodation.

6.2.5 You will have a “country tie” if you are a leaver and you spend more days in the UK in the tax year than in any other country.

6.3 Having established how many ties you have and how many days you have spent in the UK, you can establish your residence status from the following table. The day counts are more generous

for arrivers than leavers.

7 Company Residence

7.1 If you are the only/dominant shareholder or director of a company you also need to consider whether your residence status could affect the residence of the company.

7.2 If you are the sole shareholder or director of a non-UK company and you become UK resident it is likely that the company will become UK resident also, unless you carry out careful planning

before you arrive.

7.3 This is important because:

7.3.1 if a UK company becomes non-resident it is treated as selling all its assets at market value and may be subject to corporation tax on any capital gains arising;

7.3.2 if the company is a non-UK company and it becomes resident, it will become subject to UK corporation tax on its profits and gains.

7.4 In each case, the company may also be taxable elsewhere and it might need to claim double tax relief. In some cases, double tax relief may not be available.

7.5 There is no Statutory Residence Test for a company. A company is regarded as resident where its “central management and control” is situated.

7.6 Central management and control refers to the strategic decisions of the company rather than its day to day running so the question is who makes the strategic decisions and where does that person/those people make them? Normally one would expect the strategic decisions to be made by the board of directors but that is not always the case.

7.7 Again, this is an area where you will need specific advice.

A Trust

A popular discussion point is of course, the use of foreign trusts to shield foreign assets from UK taxes. The rules are quite complex but it is a strategy worth exploring.

Non-resident trusts are usually:

- if none of the trustees are resident in the UK for tax purposes

- where only some of the trustees are resident in the UK and the settlor of the trust was one of the following:

- not resident

- not normally resident

- domiciled in the UK when the trust was set up or funds added

Non-resident trusts and Income Tax

The tax rules for non-resident trusts are very complicated. Although there are general rules that apply to all non-resident trusts, each trust is different and is treated separately depending on:

- whether it’s a discretionary trust or an interest in possession trust

- the residence status of the settlors or beneficiaries

Guidance for trustees

Trustees of non-resident trusts do not pay UK tax on foreign income they receive. For most discretionary or accumulation trusts, trustees pay tax at:

- the standard rate on the first £1,000 of taxable income

- 1% on dividend income from stocks and shares

- 45% on UK interest (including ‘free of tax to residents abroad’ securities) if a beneficiary, or someone who might become one, is resident in the UK

- 45% on all other non-dividend income arising in the UK

For interest in possession trusts, trustees pay tax at the:

- dividend ordinary rate (7.5%) on trust dividend income

- basic rate (20%) on all other types of income

Guidance for settlors

You’ll have to pay tax on your trust’s income as if it’s your own income if the following apply:

- you’re the settlor (the person who puts assets into a trust)

- you, your spouse or civil partner can benefit from the income or capital of a non-resident trust

The income of the trust is not treated as yours if you (or your spouse or civil partner) cannot benefit from it. However, you’ll also have to pay Income Tax if the:

- beneficiaries include your children

- trust makes any payments to childrenof yours who are unmarried and below the age of 18

Guidance for beneficiaries

If you’re a UK resident beneficiary of a non-resident trust you may have to complete a Self Assessment tax return and the SA107 supplementary pages. The guidance notes for these pages tell you how to complete them.

If you’re a UK resident and get income from a non-resident discretionary trust, you can get tax relief if the trustees have already paid tax on the income. This relief is given under ESC B18. Read page 11 of Income Tax and Capital Gains Tax for non-resident trusts (PDF, 370KB, 21 pages) for more guidance.

If you’re a non-resident beneficiary of a non-resident income in possession trust, you only need include income from a UK source on your tax return.

Read Income Tax and Capital Gains Tax for non-resident trusts (PDF, 370KB, 21 pages) for more guidance.

Non-resident trusts and Capital Gains Tax

Capital Gains Tax is a tax on the gain in the value of assets such as shares, land or buildings. A trust may have to pay Capital Gains Tax if assets are sold, given away or exchanged (disposed of) and they’ve gone up in value since being put into the trust.

Non-resident trustees do not usually pay UK Capital Gains Tax. Instead, the settlor or the beneficiaries may have to pay tax on gains made by the non-resident trustees. But if you’re a non-resident trustee and dispose of a UK residential property you may be liable to pay Capital Gains Tax. The tax rate for non-resident trustees is the same as for resident trustees and the annual exempt amount is also available.

You must report the disposal of a UK residential property to HMRC within 60 days of the disposal using the online form.

Read HS299 Self Assessment helpsheet to help you decide whether you have taxable capital gains as settlor of a non-resident trust.

Non-resident trusts and Inheritance Tax

Trusts, including non-resident trusts may have to pay Inheritance Tax on assets in the trust. Non-resident trusts will only have to pay it on assets situated outside the UK if the settlor was domiciled (or deemed domiciled) in the UK when the assets were put into the trust.

Depending on the value of the assets in the trust, Inheritance Tax may be due when:

- assets are put into the trust

- the trust reaches a ten-year anniversary

- assets are taken out of the trust or the trust ceases

It does not matter if the trustees or beneficiaries are resident in the UK or not.

Bottom line?

Get professional advice.