Skip to content

Skip to content

Back in 2014, Forbes magazine wrote an article about Form 5471 which described it as the scariest US Tax Form – https://htj.tax/2014/03/the-scariest-us-tax-form-ever/

The author makes 3 important points:

- Firstly, the IRS normally gets three years to audit.

- Secondly, if you mess up with offshore account reporting, the IRS gets six years to audit.

- Thirdly, is that having a company that holds a foreign account is even more sensitive. Especially when it is a controlled foreign corporation, also called CFC. When a U.S. shareholder holds more than 50 percent of the vote or value of a foreign corporation, the company is a controlled foreign corporation or CFC. A U.S. shareholder is a U.S. person who owns 10 percent or more of the foreign corporation’s total voting power.

I remember in January 2018, I hosted a seminar in Singapore on international business expansion. There was one attendee who was so stressed out. Why? Because, as a US citizen who is the owner of overseas businesses, he realized that Tax Reform in the US made things more difficult than before! He was so right. The US has several anti-deferral rules. By this, I mean rules that make it very difficult for US taxpayers to invest in foreign entities.

These 3 rules are:

- Subpart F rules – https://htj.tax/2018/02/us-exposed-owner-of-international/

- PFIC rules – https://htj.tax/2015/08/what-is-pfic/

- GILTI tax rules –https://htj.tax/?s=gilti

Our team is qualified and experienced to not just report on foreign entities held by US persons but we can also share strategies for mitigating or potentially reducing these very taxes

Below, is everything else you could want to know about Form 5471

Purpose of Form

Form 5471 is used by certain U.S. persons who are officers, directors, or shareholders in certain foreign corporations. The form and schedules are used to satisfy the reporting requirements of sections 6038 and 6046, and the related regulations, as well as to report amounts related to section 965.

Who Must File

Generally, all U.S. persons described in Categories of Filers below must complete the schedules, statements, and/or other information requested in the chart, Filing Requirements for Categories of Filers, later. Read the information for each category carefully to determine which schedules, statements, and/or information apply.

Note:

When a schedule is required but all amounts are zero, the schedule should still be filed with one or more zero amounts. For schedules that are completed by category (that is, Schedule E, I-1, J, P and Q), inclusion of a single instance of that schedule for any separate category will meet the requirement.

If the filer is described in more than one filing category, do not duplicate information. However, complete all items that apply. For example, if you are the sole owner of a CFC (that is, you are described in Categories 4 and 5a), complete all six pages of Form 5471 and separate Schedules E, H, I-1, J, M, P, Q, and R.

Note:

Complete a separate Form 5471 and all applicable schedules for each applicable foreign corporation.

When and Where To File

Attach Form 5471 to your income tax return (or, if applicable, partnership or exempt organization return) and file both by the due date (including extensions) for that return.

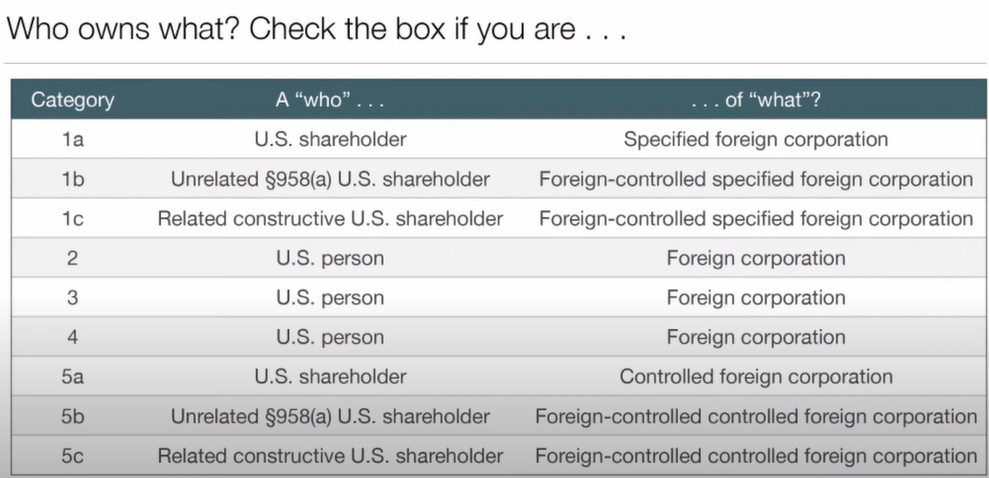

Categories of Filer

Category 1 Filers

These categories include a U.S. shareholder of a foreign corporation that is a section 965 specified foreign corporation (SFC) (defined below) at any time during any tax year of the foreign corporation, and who owned that stock on the last day in that year on which it was an SFC, taking into account the regulations under section 965. However, see Certain Category 1 and Category 5 Filers, later, which may apply.

U.S. shareholder

For purposes of Category 1 filers, a U.S. shareholder is a U.S. person who owns (directly, indirectly, or constructively, within the meaning of sections 958(a) and (b)) 10% or more of the total combined voting power of all classes of voting stock of a section 965 SFC or, in the case of a tax year of a foreign corporation beginning after December 31, 2017, 10% or more of the total combined voting power or value of shares of all classes of stock of a section 965 SFC.

U.S. person

See Category 5 Filers, later, for definition.

Section 965 specified foreign corporation (SFC).

For purposes of Category 1 filers, an SFC (as defined in section 965) is:

- A CFC (see Category 5 Filers, later, for definition), or

- Any foreign corporation with respect to which one or more domestic corporations is a U.S. shareholder.

However, if a passive foreign investment company (as defined in section 1297) with respect to the shareholder is not a CFC, then such corporation is not a section 965 SFC.

See section 965 and the regulations thereunder for exceptions.

Note:

A U.S. shareholder who is a Category 1 filer (defined above) must continue to file all information required (see below) as long as:

- The section 965 SFC has accumulated E&P related to section 965 that is reportable on Schedule J (Form 5471), or

- The U.S. shareholder has previously taxed E&P related to section 965 that is reportable on Schedule P (Form 5471).

Category 1a Filer

A U.S. shareholder who is a Category 1 filer (defined above) must complete Form 5471 and file all information required of a Category 1a filer if that U.S. shareholder does not qualify as a Category 1b or 1c filer.

Category 1b Filer

See Unrelated section 958(a) U.S. shareholder, later, for instructions pertaining to when Form 5471 may be completed as a Category 1b filer.

Category 1c Filer

See Related constructive U.S. shareholder, later, for instructions pertaining to when Form 5471 may be completed as a Category 1c filer.

Category 2 Filer

This category includes a U.S. citizen or resident who is an officer or director of a foreign corporation in which a U.S. person (defined below) has acquired (in one or more transactions):

- Stock which meets the 10% stock ownership requirement (described below) with respect to the foreign corporation, or

- An additional 10% or more (in value or voting power) of the outstanding stock of the foreign corporation.

A U.S. person has acquired stock in a foreign corporation when that person has an unqualified right to receive the stock, even though the stock is not actually issued. See Regulations section 1.6046-1(f)(1) for more details.

10% stock ownership requirement.

For purposes of Category 2 and Category 3, the stock ownership threshold is met if a U.S. person owns:

- 10% or more of the total value of the foreign corporation’s stock, or

- 10% or more of the total combined voting power of all classes of stock with voting rights.

U.S. person

For purposes of Category 2 and Category 3, a U.S. person is:

- A citizen or resident of the United States,

- A domestic partnership,

- A domestic corporation, and

- An estate or trust that is not a foreign estate or trust as defined in section 7701(a)(31).

See Regulations section 1.6046-1(f)(3) for exceptions.

Category 3 Filer

This category includes:

- A U.S. person (see Category 2 Filer above for definition) who acquires stock in a foreign corporation which, when added to any stock owned on the date of acquisition, meets the 10% stock ownership requirement (described above) with respect to the foreign corporation;

- A U.S. person who acquires stock which, without regard to stock already owned on the date of acquisition, meets the 10% stock ownership requirement with respect to the foreign corporation;

- A person who is treated as a U.S. shareholder under section 953(c) with respect to the foreign corporation;

- A person who becomes a U.S. person while meeting the 10% stock ownership requirement with respect to the foreign corporation; or

- A U.S. person who disposes of sufficient stock in the foreign corporation to reduce his or her interest to less than the 10% stock ownership requirement.

For more information, see section 6046 and Regulations section 1.6046-1.

Category 4 Filer

This category includes a U.S. person who had control (defined below) of a foreign corporation during the annual accounting period of the foreign corporation.

U.S. person

For purposes of Category 4, a U.S. person is:

- A citizen or resident of the United States;

- A nonresident alien for whom an election is in effect under section 6013(g) to be treated as a resident of the United States;

- An individual for whom an election is in effect under section 6013(h), relating to nonresident aliens who become residents of the United States during the tax year and are married at the close of the tax year to a citizen or resident of the United States;

- A domestic partnership;

- A domestic corporation; and

- An estate or trust that is not a foreign estate or trust as defined in section 7701(a)(31).

See Regulations section 1.6038-2(d) for exceptions.

Control

A U.S. person has control of a foreign corporation if, at any time during that person’s tax year, it owns stock possessing:

- More than 50% of the total combined voting power of all classes of stock of the foreign corporation entitled to vote, or

- More than 50% of the total value of shares of all classes of stock of the foreign corporation.

A person in control of a corporation that, in turn, owns more than 50% of the combined voting power, or the value, of all classes of stock of another corporation is also treated as being in control of such other corporation.

Example:

Corporation A owns 51% of the voting stock in Corporation B. Corporation B owns 51% of the voting stock in Corporation C. Corporation C owns 51% of the voting stock in Corporation D. Therefore, Corporation D is controlled by Corporation A.

For more details on “control,” see Regulations sections 1.6038-2(b) and (c).

Category 5 Filers

These categories include a U.S. shareholder who owns stock in a foreign corporation that is a CFC at any time during any tax year of the foreign corporation, and who owned that stock on the last day in that year on which it was a CFC. However, see Certain Category 1 and Category 5 Filers, later, which may apply.

U.S. shareholder

For purposes of Category 5 filers, a U.S. shareholder is a U.S. person who:

- Owns (directly, indirectly, or constructively, within the meaning of sections 958(a) and (b)) 10% or more of the total combined voting power of all classes of voting stock of a CFC or, in the case of a tax year of a foreign corporation beginning after December 31, 2017, 10% or more of the total combined voting power or value of shares of all classes of stock of a CFC; or

- Owns (either directly or indirectly, within the meaning of section 958(a)) any stock of a CFC (as defined in sections 953(c)(1)(B) and 957(b)) that is also a captive insurance company.

U.S. person

For purposes of Category 5 filers, a U.S. person is:

- A citizen or resident of the United States,

- A domestic partnership,

- A domestic corporation, and

- An estate or trust that is not a foreign estate or trust as defined in

section 7701(a)(31).

See section 957(c) for exceptions.

CFC

A CFC is a foreign corporation that has U.S. shareholders that own (directly, indirectly, or constructively, within the meaning of sections 958(a) and (b)) on any day of the tax year of the foreign corporation, more than 50% of:

- The total combined voting power of all classes of its voting stock, or

- The total value of the stock of the corporation.

Category 5a Filer

A U.S. shareholder who is a Category 5 filer (defined above) must complete Form 5471 and file all information required of a Category 5a filer if that U.S. shareholder does not qualify as a Category 5b or 5c filer.

Category 5b Filer

See Unrelated section 958(a) U.S. shareholder below for instructions pertaining to when Form 5471 may be completed as a Category 5b filer.

Category 5c Filer

See Related constructive U.S. shareholder below for instructions pertaining to when Form 5471 may be completed as a Category 5c filer.

Certain Category 1 and Category 5 Filers

Rev. Proc. 2019-40 provides relief for certain types of Category 5 filers. These instructions clarify that this relief is extended to similarly situated Category 1 filers.

Unrelated section 958(a) U.S. shareholder.

For purposes of Category 1 and Category 5 filers, an unrelated section 958(a) U.S. shareholder is a U.S. shareholder with respect to a foreign-controlled corporation (defined below) who:

- Owns, within the meaning of section 958(a), stock of a foreign-controlled corporation; and

- Is not related (using principles of section 954(d)(3)) to the foreign-controlled corporation.

A U.S. shareholder who is a Category 1 filer (defined previously) and who is an unrelated section 958(a) U.S. shareholder with respect to a foreign-controlled corporation (defined below) may complete Form 5471 for that foreign-controlled corporation and complete only the information required of a Category 1b filer. A U.S. shareholder who is a Category 5 filer (defined above) and who is an unrelated section 958(a) U.S. shareholder with respect to a foreign-controlled corporation (defined below) may complete Form 5471 for that foreign-controlled corporation and complete only the information required of a Category 5b filer.

Related constructive U.S. shareholder.

For purposes of Category 1 and Category 5 filers, a related constructive U.S. shareholder is a U.S. shareholder with respect to a foreign-controlled corporation who:

- Does not own, within the meaning of section 958(a), stock of the foreign-controlled corporation; and

- Is related (using principles of section 954(d)(3)) to the foreign-controlled corporation.

A U.S. shareholder who is a Category 1 filer (defined previously) and who is a related constructive U.S. shareholder with respect to a foreign-controlled corporation (defined below) may complete Form 5471 for that foreign-controlled corporation and complete only the information required of a Category 1c filer. The U.S, shareholder who is a Category 5 filer (defined above) and who is a related constructive U.S. shareholder with respect to a foreign-controlled corporation (defined below) may complete Form 5471 for that foreign-controlled corporation and complete only the information required of a Category 5c filer.

Foreign-controlled corporation

For purposes of Category 1 and Category 5 filers, a foreign-controlled corporation is a foreign corporation that is either:

- A section 965 SFC that would not be a section 965 SFC if the determination were made without applying subparagraphs (A), (B), and (C) of section 318(a)(3) so as to consider a U.S. person as owning stock that is owned by a foreign person (for purposes of Category 1 filers); or

- A CFC that would not be a CFC if the determination were made without applying subparagraphs (A), (B), and (C) of section 318(a)(3) so as to consider a U.S. person as owning stock that is owned by a foreign person (for purposes of Category 5 filers).

Filing Requirements for Categories of Filers

The Issue

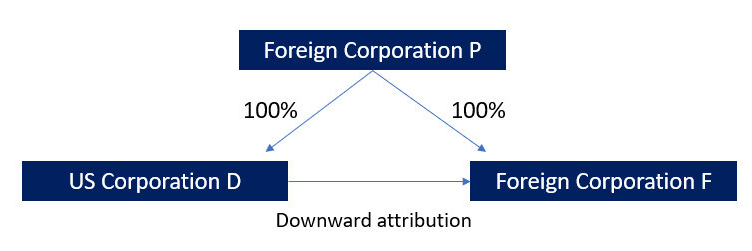

The Tax Cuts and Jobs Act (TCJA) of 2017 significantly expanded the constructive ownership rules for determining whether a foreign corporation is a controlled foreign corporation (CFC) and, thus, if Form 5471 needs to be filed or not. Overnight, thousands of foreign corporations became controlled foreign corporations (CFCs) according to the plain language of the Code. Downward attribution is the concept that stock ownership by a corporation’s owner is attributed as owned, for instance, by another corporation.

The following non-complex scenario is an example where the downward attribution is applicable. Foreign corporation P wholly owns two subsidiary corporations, foreign corporation F and U.S. corporation D. Attribution rules require P’s shares of F to be attributed downward to D, making D a U.S. shareholder and F a Controlled Foreign Corporation for D. With the repeal of the Code section that prevented this downward attribution, D is required to file Form 5471 with regard to F.

The Solution

- The Category 5 filer does not own a direct or indirect interest in a foreign corporation and

- The Category 5 filer is only required to file Form 5471 because of constructive ownership from a nonresident alien. This includes the constructive ownership based on the downward attribution rules, but would seem to apply only to ownership by foreign individuals.

- The filer is a U.S. shareholder that only owns stock, within the meaning of the constructive ownership rules in §958(b) in the foreign corporation;

- The filer is not related, using principles of §954(d)(3), to the foreign corporation; and

- The foreign corporation is a foreign-controlled corporation.

Exceptions From Filing

Multiple filers of same information

One person may file Form 5471 and the applicable schedules for other persons who have the same filing requirements. If you and one or more other persons are required to furnish information for the same foreign corporation for the same period, a joint information return that contains the required information may be filed with your tax return or with the tax return of any one of the other persons. For example, a U.S. person described in Category 5 may file a joint Form 5471 with a Category 4 or another Category 5 filer. However, for Category 3 filers, the required information may only be filed by another person having an equal or greater interest (measured in terms of value or voting power of the stock of the foreign corporation).

The person that files Form 5471 must complete Form 5471 in the manner described in the instructions for Item F. All persons identified in Item F must attach a statement to their income tax return that includes the information described in the instructions for Item F.

Domestic corporations

Shareholders are not required to file the information checked in the chart, later, for a foreign insurance company that has elected (under section 953(d)) to be treated as a domestic corporation and has filed a U.S. income tax return for its tax year under that provision. See Rev. Proc. 2003-47, 2003-28 I.R.B. 55, available at IRS.gov/irb/2003-28_IRB#RP-

Certain constructive owners.

- A U.S. person described in Category 1, 3, 4, or 5 (“shareholder”) does not have to file Form 5471 if all of the following conditions are met.

- The shareholder does not own a direct interest in the foreign corporation.

- The shareholder is required to furnish the information requested solely because of constructive ownership (as determined under Regulations section 1.958-2, 1.6038-2(c), or 1.6046-1(i)) from another U.S. person.

- The U.S. person through which the shareholder constructively owns an interest in the foreign corporation files Form 5471 to report all of the required information.No statement is required to be attached to tax returns for persons claiming the constructive ownership exception.

- A Category 2 filer does not have to file Form 5471 if:

- Immediately after a reportable stock acquisition, three or fewer U.S. persons own 95% or more in value of the outstanding stock of the foreign corporation and the U.S. person making the acquisition files a return for the acquisition as a Category 3 filer; or

- The U.S. person(s) for which the Category 2 filer is required to file Form 5471 does not directly own an interest in the foreign corporation but is required to furnish the information solely because of constructive stock ownership from a U.S. person and the person from whom the stock ownership is attributed furnishes all of the required information.

- A Category 1, 4, or 5 filer does not have to file Form 5471 if the shareholder:

- Does not own a direct or indirect interest in the foreign corporation, and

- Is required to file Form 5471 solely because of constructive ownership from a nonresident alien.

- A Category 1 or 5 filer does not have to file Form 5471 if no U.S. shareholder (including such U.S. person) owns, within the meaning of section 958(a), stock in the foreign corporation on the last day in the year of the foreign corporation in which it was an SFC or CFC, and the foreign corporation is an SFC or CFC solely because one or more U.S. persons is considered to own the stock of the foreign corporation owned by a foreign person under section 318(a)(3). Furthermore, a Category 1 or 5 filer does not have to file Form 5471 if all of the following conditions are met.

- The filer is a U.S. shareholder that only owns stock, within the meaning of section 958(b), in the foreign corporation.

- The filer is not related, using principles of section 954(d)(3), to the foreign corporation.

- The foreign corporation is a foreign-controlled corporation. See Rev. Proc. 2019-40 for more details.

Additional Filing Requirements

Category 3 filers.

Category 3 filers must attach a statement that includes:

- The amount and type of any indebtedness the foreign corporation has with the related persons described in Regulations section 1.6046-1(b)(11); and

- The name, address, identifying number, and number of shares subscribed to by each subscriber to the foreign corporation’s stock.

Foreign sales corporations (FSCs).

- Category 2 and Category 3 filers who are shareholders, officers, and directors of a FSC (as defined in section 922, as in effect before its repeal) must file Form 5471 and a separate Schedule O to report changes in the ownership of the FSC.

- Category 4 and 5 filers are not subject to the subpart F rules for:

- Exempt foreign trade income;

- Deductions that are apportioned or allocated to exempt foreign trade income;

- Nonexempt foreign trade income (other than section 923(a)(2) nonexempt income, within the meaning of

section 927(d)(6), as in effect before its repeal); and - Any deductions that are apportioned or allocated to the nonexempt foreign trade income described above.

- Category 4 and 5 filers are subject to the subpart F rules for:

- All other types of FSC income (including section 923(a)(2) nonexempt income within the meaning of

section 927(d)(6), as in effect before its repeal); - Investment income and carrying charges (as defined in sections 927(c) and 927(d)(1), as in effect before their repeal); and

- All other FSC income that is not foreign trade income or investment income or carrying charges.

- All other types of FSC income (including section 923(a)(2) nonexempt income within the meaning of

- Category 4 and 5 filers are not required to file a Form 5471 (in order to satisfy the requirements of section 6038) if the FSC has filed a Form 1120-FSC. See Temporary Regulations section 1.921-1T(b)(3). However, these filers may be required to file Form 5471 if they are subject to the subpart F rules with respect to certain types of FSC income (see above).

Section 338 election.

If a section 338 election is made with respect to a qualified stock purchase of a foreign target corporation for which a Form 5471 must be filed:

- A purchaser (or its U.S. shareholder) must attach a copy of Form 8883, Asset Allocation Statement Under Section 338, to the first Form 5471 for the new foreign target corporation (see the Instructions for Form 8883 for details);

- A seller (or its U.S. shareholder) must attach a copy of Form 8883 to the last Form 5471 for the old foreign target corporation.

Reportable transaction disclosure statement.

If a U.S. shareholder of a CFC is considered to have participated in a reportable transaction under the rules of Regulations section 1.6011-4(c)(3)(i)(G), the shareholder is required to disclose information for each reportable transaction. Form 8886, Reportable Transaction Disclosure Statement, must be filed for each tax year indicated in Regulations section 1.6011-4(c)(3)(i)(G). The following are reportable transactions.

- Any listed transaction, which is a transaction that is the same as or substantially similar to one of the types of transactions that the IRS has determined to be a tax avoidance transaction and identified by notice, regulation, or other published guidance as a listed transaction.

- Any transaction offered under conditions of confidentiality for which the corporation (or a related party) paid an advisor a fee of at least $250,000.

- Certain transactions for which the corporation (or a related party) has contractual protection against disallowance of the tax benefits.

- Certain transactions resulting in a loss of at least $10 million in any single year or $20 million in any combination of years.

- Any transaction identified by the IRS by notice, regulation, or other published guidance as a “transaction of interest.” See Notice 2009-55, 2009-31 I.R.B. 170, available at IRS.gov/irb/2009-31_IRB#

NOT-2009-55.

For more information, see Regulations section 1.6011-4. Also see the Instructions for Form 8886.

Penalties.

The U.S. shareholder may have to pay a penalty if it is required to disclose a reportable transaction under section 6011 and fails to properly complete and file Form 8886. Penalties also may apply under section 6707A if the U.S. shareholder fails to file Form 8886 with its income tax return, fails to provide a copy of Form 8886 to the Office of Tax Shelter Analysis (OTSA), or files a form that fails to include all the information required (or includes incorrect information). Other penalties, such as an accuracy-related penalty under section 6662A, may also apply. See the Instructions for Form 8886 for details on these and other penalties.

Reportable transactions by material advisors.

Material advisors to any reportable transaction must disclose certain information about the reportable transaction by filing Form 8918, Material Advisor Disclosure Statement, with the IRS. For details, see the Instructions for Form 8918.

Reporting other foreign financial assets.

If you have other foreign financial assets, you may be required to file Form 8938, Statement of Specified Foreign Financial Assets. However, you are not required to report any items otherwise reported on Form 5471 on that form. See the Instructions for Form 8938 for more information.

Failure to file information required by section 6038(a) (Form 5471 and Schedule M).

- A $10,000 penalty is imposed for each annual accounting period of each foreign corporation for failure to furnish the information required by section 6038(a) within the time prescribed. If the information is not filed within 90 days after the IRS has mailed a notice of the failure to the U.S. person, an additional $10,000 penalty (per foreign corporation) is charged for each 30-day period, or fraction thereof, during which the failure continues after the 90-day period has expired. The additional penalty is limited to a maximum of $50,000 for each failure.

- Any person who fails to file or report all of the information required within the time prescribed will be subject to a reduction of 10% of the foreign taxes available for credit under sections 901, 902 (with respect to foreign corporate tax years beginning before January 1, 2018), and 960. If the failure continues 90 days or more after the date the IRS mails notice of the failure to the U.S. person, an additional 5% reduction is made for each 3-month period, or fraction thereof, during which the failure continues after the 90-day period has expired. See section 6038(c)(2) for limits on the amount of this penalty.

Failure to file information required by section 6046 and the related regulations (Form 5471 and Schedule O).

Any person who fails to file or report all of the information requested by section 6046 is subject to a $10,000 penalty for each such failure for each reportable transaction. If the failure continues for more than 90 days after the date the IRS mails notice of the failure, an additional $10,000 penalty will apply for each 30-day period, or fraction thereof, during which the failure continues after the 90-day period has expired. The additional penalty is limited to a maximum of $50,000.

Criminal penalties.

Criminal penalties under sections 7203, 7206, and 7207 may apply for failure to file the information required by sections 6038 and 6046.

Section 6662(j).

Penalties may be imposed for undisclosed foreign financial asset understatements. No penalty will be imposed with respect to any portion of an underpayment if the taxpayer can demonstrate that the failure to comply was due to reasonable cause with respect to such portion of the underpayment and the taxpayer acted in good faith with respect to such portion of the underpayment. See sections 6662(j) and 6664(c) for additional information.

Inapplicability of certain penalties.

Certain penalties under sections 6038 and 6662 may be waived for certain persons under Rev. Proc. 2019-40. See section 7 of Rev. Proc. 2019-40 for more details.

Other Reporting Requirements

Reporting exchange rates on Form 5471.

When translating amounts from functional currency to U.S. dollars, you must use the method specified in these instructions. For example, when translating amounts to be reported on Schedule E, you must generally use the average exchange rate as defined in section 986(a). But, regardless of the specific method required, all exchange rates must be reported using a “divide-by convention” rounded to at least four places. That is, the exchange rate must be reported in terms of the amount by which the functional currency amount must be divided in order to reflect an equivalent amount of U.S. dollars. As such, the exchange rate must be reported as the units of foreign currency that equal one U.S. dollar, rounded to at least four places. Do not report the exchange rate as the number of U.S. dollars that equal one unit of foreign currency.

You must round the result to more than four places if failure to do so would materially distort the exchange rate or the equivalent amount of U.S. dollars.

Example.

During its annual accounting period, the foreign corporation paid income taxes of 30,255,400 Yen to Japan. The Schedule E instructions specify that the foreign corporation must translate these amounts into U.S. dollars at the average exchange rate for the tax year to which the tax relates in accordance with the rules of section 986(a). The average exchange rate is 108.8593 Japanese Yen to one U.S. dollar or (0.009184) U.S. dollar to one Japanese Yen. The foreign corporation divides 30,255,400 Yen by 108.8593 to determine the U.S. dollar amount to enter in column (k) of Schedule E, Part I, Section 1, line 1. Line 1 of Schedule E, Part I, Section 1, is completed in relevant part as follows.

- Enter the name of the foreign corporation in column (a).

- Enter the foreign corporation’s EIN or reference ID number in column (b).

- Enter “JA” in column (c).

- Enter “JPY” in column (h).

- Enter “30,255,400 Yen” in column (i).

- Enter “108.8593” in column (j).

- Enter “277,931” in column (k).

Computer-Generated Form 5471 and Schedules

Generally, all computer-generated forms must receive prior approval from the IRS and are subject to an annual review. However, see the Exception below. Requests for approval may be submitted electronically to substituteforms@irs.gov, or requests may be mailed to:

Internal Revenue ServiceAttention: Substitute Forms Program

SE:W:CAR:MP:P:TP

1111 Constitution Ave. NW

Room 6554

Washington, DC 20224

Exception.

If a computer-generated Form 5471 and its schedules conform to and do not deviate from the official form and schedules, they may be filed without prior approval from the IRS.

Be sure to attach the approval letter to Form 5471. However, if the computer-generated form is identical to the IRS-prescribed form, it does not need to go through the approval process, and an attachment is not necessary.

Every year, the IRS issues a revenue procedure to provide guidance for filers of computer-generated forms. In addition, every year the IRS issues Pub. 1167, General Rules and Specifications for Substitute Forms and Schedules, which reprints the most recent applicable revenue procedure. Pub. 1167 is available at IRS.gov/Pub. 1167.

Dormant Foreign Corporations

Rev. Proc. 92-70, 1992-2 C.B. 435, provides a summary filing procedure for filing Form 5471 for a dormant foreign corporation (defined in section 3 of Rev. Proc. 92-70). This summary filing procedure will satisfy the reporting requirements of sections 6038 and 6046.

If you elect the summary procedure, complete only page 1 of Form 5471 for each dormant foreign corporation as follows.

- The top margin of the summary return must be labeled “Filed Pursuant to Rev. Proc. 92-70 for Dormant Foreign Corporation.”

- Include filer information such as name and address, Items A through C, and tax year.

- Include corporate information such as the dormant corporation’s annual accounting period (below the title of the form) and Items 1a, 1b, 1c, and 1d.

For more information, see Rev. Proc. 92-70.

File this summary return in the manner described in When and Where To File, earlier.

Treaty-Based Return Positions

You are generally required to file

Form 8833, Treaty-Based Return Position Disclosure Under Section 6114 or 7701(b), to disclose a return position that any treaty of the United States (such as an income tax treaty, an estate and gift tax treaty, or a friendship, commerce, and navigation treaty):

- Overrides or modifies any provision of the Internal Revenue Code; and

- Causes, or potentially causes, a reduction of any tax incurred at any time.

See Form 8833 for exceptions.

Failure to make a required disclosure may result in a $1,000 penalty ($10,000 for a C corporation). See section 6712.

Section 362(e)(2)(C) Elections

The transferor and transferee in certain section 351 transactions may make a joint election under section 362(e)(2)(C) to limit the transferor’s basis in the stock received instead of the transferee’s basis in the transferred property. The election is made by a statement as provided in Regulations section 1.362-4(d)(3).

. Do not attach the statement described above to Form 5471..

Do not attach the statement described above to Form 5471..

If the controlling domestic shareholder(s) of a CFC made an election in 2009 or 2010 to defer income from cancellation of debt in connection with the CFC’s reacquisition of an applicable debt instrument, a statement must be filed (in the manner specified in the Caution below) beginning with the tax year following the tax year for which the controlling domestic shareholder of the CFC made the election, and ending the first tax year all income deferred has been included in income. In addition, a copy of the election statement it filed to make the election to defer income must be filed annually (also in the manner specified in the Caution below). For details, see section 108(i) and Rev. Proc. 2009-37, 2009-36 I.R.B. 309, available at IRS.gov/irb/2009-36_IRB#RP-

.Do not attach the statements described above to Form 5471. Instead, if the foreign corporation is required to file a U.S. income tax return (for example, Form 1120-F), attach the statements to that return..

Corrections to Form 5471

If you file a Form 5471 that you later determine is incomplete or incorrect, file a corrected Form 5471 with an amended tax return, using the amended return instructions for the return with which you originally filed Form 5471. Write “Corrected” at the top of the form and attach a statement identifying the changes.

Specific Instructions

If the information required in a given section exceeds the space provided within that section, do not write “See attached” in the section and then attach all of the information on additional sheets. Instead, complete all entry spaces in the section and attach the remaining information on additional sheets. The additional sheets must conform with the IRS version of that section.

Identifying Information

Annual Accounting Period

Enter, in the space provided below the title of Form 5471, the annual accounting period of the foreign corporation for which you are furnishing information. Except for information contained on Schedule O, report information for the tax year of the foreign corporation that ends with or within your tax year. When filing Schedule O, report acquisitions, dispositions, and organizations or reorganizations that occurred during your tax year.

Section 898 specified foreign corporation (SFC).

The annual accounting period of an SFC (as defined in section 898) is generally required to be the tax year of the corporation’s majority U.S. shareholder. If there is more than one majority shareholder, the required tax year will be the tax year that results in the least aggregate deferral of income to all U.S. shareholders of the foreign corporation.

For these purposes, section 898(b) defines an SFC as any foreign corporation:

- That is treated as a CFC under subpart F, and

- In which more than 50% of the total voting power or value of all classes of stock of the corporation is treated as owned by a U.S. shareholder.

For more information, see section 898 and Rev. Proc. 2006-45, 2006-45 I.R.B. 851, available at IRS.gov/irb/2006-45_IRB#

Name of Person Filing This Return

The name of the person filing Form 5471 is generally the name of the U.S. person described in the applicable category or categories of filers (see Categories of Filers, earlier). However, in the case of a consolidated return, enter the name of the U.S. parent in the field for “Name of person filing this return.” Be sure to list each U.S. shareholder of the foreign corporation in Schedule B, Part I.

Name change.

If the name of either the person filing the return or the corporation whose activities are being reported changed within the past 3 years, show the prior name(s) in parentheses after the current name.

Address

Include the suite, room, or other unit number after the street address. If the post office does not deliver mail to the street address and the U.S. person has a P.O. box, show the box number instead.

Foreign address.

Enter the information in the following order: city, province or state, and country. Follow the country’s practice for entering the postal code, if any. Do not abbreviate the country name.

Item A—Identifying Number

The identifying number of an individual is his or her social security number (SSN). The identifying number of all others is their employer identification number (EIN). If a U.S. corporation that owns stock in a foreign corporation is a member of a consolidated group, list the common parent as the person filing the return and enter its EIN in Item A.

Item B—Category of Filer

Complete Item B to indicate the category or categories that describe the person filing this return. If more than one category applies, check all boxes that apply. See Categories of Filers, earlier.

Item C—Percentage of Voting Stock Owned

Enter the total percentage of the foreign corporation’s voting stock you owned directly, indirectly, or constructively at the end of the corporation’s annual accounting period.

Item D—Final Year

Check the Item D checkbox only if this is the final year of the foreign corporation’s existence as a corporation for federal tax purposes, for example, if a reorganization has occurred, a complete liquidation has occurred, or an election to treat the foreign corporation as a disregarded entity has been made. If this Item D is checked, complete Schedule O.

Item E—Excepted Specified Foreign Financial Assets

Check the Item E checkbox if any excepted specified foreign financial assets are reported on Form 5471. If this is the case, you do not have to also report these assets on Form 8938, Statement of Specified Foreign Financial Assets. It is only necessary to complete Form 8938, Part IV, line 3. For more information, see the Instructions for Form 8938, generally, and in particular, Duplicative Reporting and the specific instructions for Part IV, Excepted Specified Foreign Financial Assets.

Item F—Alternative Information Under Rev. Proc. 2019-40

Check the box on line F if Form 5471 has been completed using alternative information (as defined in section 3.01 of Rev. Proc. 2019-40).

Section 5 of Rev. Proc. 2019-40 provides a safe harbor for determining certain items, including taxable income and E&P, of certain CFCs based on alternative information. Specifically, in the case of a foreign-controlled CFC with respect to which there is no related section 958(a) U.S. shareholder, if information satisfying the requirements of Regulations sections 1.952-2(a), (b), and (c)(2) and section 964 and the regulations thereunder is not readily available to an unrelated section 958(a) U.S. shareholder or an unrelated constructive U.S. shareholder with respect to the foreign-controlled CFC, an amount reported on a Form 5471 may be determined by the unrelated section 958(a) U.S. shareholder or the unrelated constructive U.S. shareholder, as applicable, on the basis of alternative information (without adjustments other than those described in section 3.01(b) and 3.10 of the revenue procedure) with respect to the foreign-controlled CFC. See section 3 of Rev. Proc. 2019-40 for definitions of terms.

Section 6 of Rev. Proc. 2019-40 provides a safe harbor for determining certain items of certain SFCs based on alternative information. Specifically, in the case of an SFC, other than either a foreign-controlled CFC with respect to which there is no related section 958(a) U.S. shareholder or a U.S. controlled CFC, if information satisfying the requirements of section 964 and the regulations thereunder is not readily available to an unrelated section 958(a) U.S. shareholder or an unrelated constructive U.S. shareholder with respect to the SFC, an amount reported on a Form 5471 may be determined by the unrelated section 958(a) U.S. shareholder or the unrelated constructive U.S. shareholder, as applicable, on the basis of alternative information (without adjustments other than those described in sections 3.01(b) and 3.10 of the revenue procedure) with respect to the SFC. See section 3 of Rev. Proc. 2019-40 for definitions of terms.

Item G—Alternative Information Code

If the box on line F is checked, enter the applicable code from the list provided below.

| 01 | Audited separate-entity financial statements of the foreign corporation that are prepared in accordance with U.S. generally accepted accounting principles (U.S. GAAP). |

| 02 | Audited separate-entity financial statements of the foreign corporation that are prepared on the basis of international financial reporting standards (IFRS). |

| 03 | Audited separate-entity financial statements of the foreign corporation that are prepared on the basis of the generally accepted accounting principles of the jurisdiction in which the foreign corporation is organized (“local-country GAAP”). |

| 04 | Unaudited separate-entity financial statements of the foreign corporation that are prepared in accordance with U.S. GAAP. |

| 05 | Unaudited separate-entity financial statements of the foreign corporation that are prepared on the basis of IFRS. |

| 06 | Unaudited separate-entity financial statements of the foreign corporation that are prepared on the basis of local-country GAAP. |

| 07 | Separate-entity records used by the foreign corporation for tax reporting. |

| 08 | Separate-entity records used by the foreign corporation for internal management controls or regulatory or other similar purposes. |

Information described in a code listed above qualifies as alternative information only if information described in any preceding code is not “readily available” (as defined in section 3.04 of Rev. Proc. 2019-40). For example, information described in code “03” above qualifies as alternative information only if information described in code “01” and “02” is not readily available.

For more information, see Rev. Proc. 2019-40, available at IRS.gov/irb/2019-43_IRB#

Item H—Person(s) on Whose Behalf This Information Return Is Filed

One person may file Form 5471 and the applicable schedules for other persons who have the same filing requirements. See Multiple filers of same information , earlier. The person that files the required information on behalf of other persons must complete a joint Form 5471 according to the applicable column(s) of the Filing Requirements for Categories of Filers, earlier. This includes completing Item H on page 1 of the form. When completing Item H with respect to members of a consolidated group, identify only the direct owners in Item H (constructive owners are not required to be listed).

A separate Schedule I must be filed for each person described in Category 4, 5a, or 5b. For each Category 4, 5a, or 5b filer that is required to file a Schedule I, send a copy of their separate Schedule I to them to assist them in completing their tax return.

Filing requirements for persons identified in Item H.

Except for members of the filer’s consolidated return group, all persons identified in Item H must attach a statement to their tax returns that includes the following information.

- The name, address, and EIN (or reference ID number) of the foreign corporation(s).

- A statement that their filing requirements with respect to the foreign corporation(s) have been or will be satisfied.

- The name, address, and identifying number of the taxpayer on the return with which the information was or will be filed.

- The IRS Service Center where the return was or will be filed. If the return was or will be filed electronically, enter “e-file.”

Exception.

If the person who is filing Form 5471 on behalf of others is married to a person identified in Item H and they are filing Form 1040 jointly, the statement described above does not have to be attached to the jointly filed Form 1040.

.All persons identified in Item H must complete a separate Schedule P (Form 5471) if the person is a U.S. shareholder described in Category 1a, 1b, 4, 5a, or 5b. In such a case, the Schedule P must be attached to the statement described above..

Item 1b(2)—Reference ID Number

A reference ID number (defined below) is required on line 1b(2) only in cases where no EIN was entered on line 1b(1) for the foreign corporation. However, filers are permitted to enter both an EIN on line 1b(1) and a reference ID number on line 1b(2). If applicable, enter the reference ID number you have assigned to the foreign corporation identified on line 1a.

A “reference ID number” is a number established by or on behalf of the U.S. person identified at the top of page 1 of the form that is assigned to a foreign corporation with respect to which Form 5471 reporting is required. These numbers are used to uniquely identify the foreign corporation in order to keep track of the corporation from tax year to tax year.

The reference ID number must meet the requirements set forth below.

Because reference ID numbers are established by or on behalf of the U.S. person filing Form 5471, there is no need to apply to the IRS to request a reference ID number or for permission to use these numbers.

The reference ID number assigned to a foreign corporation on Form 5471 generally has relevance only on Form 5471, its schedules, and any other form that is attached to or associated with Form 5471, and generally should not be used with respect to that foreign corporation on any other IRS forms. However, the foreign corporation’s reference ID number should also be entered on Form 8858 if the foreign corporation is listed as a tax owner of a foreign disregarded entity (FDE) or foreign branch (FB) on Form 8858. See the instructions for Form 8858, line 3c(2), for more information.

Requirements.

The reference ID number that is entered in Item 1b(2) must be alphanumeric (defined later) and no special characters or spaces are permitted. The length of a given reference ID number is limited to 50 characters.

The same reference ID number must be used consistently from tax year to tax year with respect to a given foreign corporation. If for any reason a reference ID number falls out of use (for example, the foreign corporation no longer exists due to disposition or liquidation), the reference ID number used for that foreign corporation cannot be used again for another foreign corporation for purposes of Form 5471 reporting.

For these purposes, the term “alphanumeric” means the entry can be alphabetical, numeric, or any combination of the two.

There are some situations that warrant correlation of a new reference ID number with a previous reference ID number when assigning a new reference ID number to a foreign corporation. For example:

- In the case of a merger or acquisition, a Form 5471 filer must use a reference ID number that correlates the previous reference ID number with the new reference ID number assigned to the foreign corporation; or

- In the case of an entity classification election that is made on behalf of a foreign corporation on Form 8832, Regulations section 301.6109-1(b)(2)(v) requires the foreign corporation to have an EIN for this election. For the first year that Form 5471 is filed after an entity classification election is made on behalf of the foreign corporation on Form 8832, the new EIN must be entered on line 1b(1) of Form 5471 and the old reference ID number must be entered on line 1b(2). In subsequent years, the Form 5471 filer may continue to enter both the EIN on line 1b(1) and the reference ID number on line 1b(2), but must enter at least the EIN on line 1b(1).

You must correlate the reference ID numbers as follows: New reference ID number [space] Old reference ID number. If there is more than one old reference ID number, you must enter a space between each such number. As indicated above, the length of a given reference ID number is limited to 50 characters and each number must be alphanumeric and no special characters are permitted.

Items 1f and 1g—Principal Business Activity

Enter the principal business activity code number and the description of the activity from the list at the end of these instructions.

Item 1h—Functional Currency

Enter the applicable three-character alphabet code for the foreign corporation’s functional currency using the ISO 4217 standard. These codes are available at www.iso.org/iso-4217-

Special rules apply for foreign corporations that use the U.S. dollar approximate separate transactions method of accounting (DASTM) under Regulations section 1.985-3. See the instructions for Schedule C and Schedule H.

Schedule B

Part I

Category 3 and 4 filers must complete Schedule B, Part I, for U.S. persons that owned (at any time during the annual accounting period), directly or indirectly through foreign entities, 10% or more in value or voting power of any class of the foreign corporation’s outstanding stock.

Column (e).

Enter each shareholder’s allocable percentage of the foreign corporation’s subpart F income.

Part II

Category 1a, 1c, 3, 4, 5a, and 5c filers must complete Part II.

Report the direct shareholders of the foreign corporation. In the case of a CFC owned by a foreign disregarded entity (FDE), please include the information of the FDE and the regarded entity owner. Indicate the regarded entity owner’s name in parentheses after the FDE’s name. If there is more than one regarded entity owner, use separate lines for each, listing each regarded entity owner in column (a) and reporting the information requested in columns (b), (c), and (d) for each such regarded entity owner.

Category 4 filers should list all direct owners of the CFC. Category 1a, 3, and 5a filers should list all direct owners of the SFC or CFC through which such filer indirectly owns the SFC or CFC as described in section 958(a)(2). Category 1c and 5c filers should list all direct owners of the SFC or CFC from which such filer is attributed ownership in the SFC or CFC as described in section 958(b). If the filer is a direct owner, include the filer’s direct ownership.

Schedule C

Report all information in the foreign corporation’s functional currency in accordance with U.S. GAAP and translate using U.S. GAAP translation principles.

If the foreign corporation uses the DASTM under Regulations section 1.985-3, the functional currency column should reflect local hyperinflationary currency amounts computed in accordance with U.S. GAAP. The U.S. dollar column should reflect such amounts translated into dollars under U.S. GAAP translation rules. Differences between this U.S. dollar GAAP column and the U.S. dollar income or loss figured for tax purposes under Regulations section 1.985-3(c) should be accounted for on Schedule H. See Schedule H, Special rules for DASTM , later.

Line 8.

Enter foreign currency transaction gain or loss reported on the income statement. For amounts included in Other Comprehensive Income (OCI), see the instructions for Lines 23 and 24. Enter unrealized gain or loss on line 8a and realized gain or loss on line 8b.

Line 16.

Enter transactional taxes excluding items reportable in income tax expense (benefit). Report income taxes on line 21.

Line 20.

The term “unusual or infrequently occurring items” is defined by U.S. GAAP (see FASB Accounting Standards Codification (ASC) Topic 220 (Income Statement), Subtopic 220-20 (Extraordinary and Unusual Items) or subsequent guidance). If “prior period adjustments” are not reported separately on the income statement, do not report such amounts on this line item (see ASC 250 (Accounting Changes and Error Corrections) or subsequent guidance).

Line 21.

Enter income tax expense (benefit) reported in accordance with U.S. GAAP (ASC 740 (Income Taxes)). Income tax expense (benefit) includes current and deferred income tax expense (benefit). It may also reflect uncertain tax positions (ASC 740-10) and would not include taxes paid in respect of uncertain tax positions recorded in prior years. Enter the current income tax expense (benefit) on line 21a and deferred income tax expense (benefit) on line 21b.

If there is an income tax expense amount on line 21a or 21b, subtract that amount from the line 19 net income or (loss) amount in arriving at line 22 current year net income or (loss) per the books. If there is an income tax benefit amount on line 21a or 21b, add that amount to the line 19 net income or (loss) amount in arriving at line 22 current year net income or (loss) per the books.

Lines 23 and 24.

Enter amounts defined in ASC 220 (Comprehensive Income).

Enter foreign currency translation adjustments before the income tax expense (benefit) is allocated.

Enter other comprehensive income such as foreign currency gains or losses on certain hedging transactions, pensions and other post-retirement benefits, and certain investments available-for-sale.

Enter the income tax expense (benefit) allocated to OCI items in the intraperiod allocation.

Important.

Differences between the functional currency amount of income tax expense (benefit) reported on line 21 and the amount of taxes that reduce or increase U.S. earnings and profits (E&P) should be accounted for on line 2g of Schedule H.

Schedule F

Report all information in the foreign corporation’s functional currency in accordance with U.S. GAAP and translate using U.S. GAAP translation rules. If the foreign corporation uses DASTM, the tax balance sheet on Schedule F should be prepared and translated into U.S. dollars according to Regulations section 1.985-3(d), rather than U.S. GAAP.

Lines 3 and 17.

Enter the total asset amount of derivatives on line 3 and total amount of liability on line 17 reported in accordance with ASC 815 (Derivatives and Hedging). Do not net positions.

Include all derivatives, both short-term and long-term.

Schedule G

Category 1b and 5b filers are not required to file Schedule G for foreign-controlled corporations.

If the foreign corporation owned at least a 10% interest, directly or indirectly, in any foreign partnership, attach a statement listing the following information for each foreign partnership.

- Name and EIN (if any) of the foreign partnership.

- Identify which, if any, of the following forms the foreign partnership filed for its tax year ending with or within the corporation’s tax year: Form 1042, 1065, or 8804.

- Name of the partnership representative (if any).

- Beginning and ending dates of the foreign partnership’s tax year

Check the “Yes” box if the foreign corporation is the tax owner of an FDE or FB. The “tax owner” of an FDE is the person that is treated as owning the assets and liabilities of the FDE for purposes of U.S. income tax law.

If the foreign corporation is the tax owner of an FDE or FB and you are a Category 4, 5a, or 5c filer of Form 5471, you are required to attach Form 8858 to Form 5471.

If the foreign corporation is the tax owner of an FDE or FB and you are not a Category 1b, 4, or 5 filer of Form 5471, you must attach the statement described below in lieu of Form 8858.

Statement in lieu of Form 8858.

This statement must list the name of the FDE or FB, country under whose laws the FDE or FB was organized, and EIN (if any) of the FDE or FB.

Complete lines 4b and 4c if:

- The foreign corporation is a related party to the U.S. filer within the meaning of section 59A(g); and

- The U.S. filer made or accrued a base erosion payment to, or has a base erosion tax benefit with respect to, the foreign corporation.

The term “base erosion payment” generally means any amount paid or accrued by the U.S. filer to a foreign corporation that is a related party to the U.S. filer within the meaning of section 59A(g) and with respect to which a U.S. deduction is allowed under chapter 1 of the Code. See section 59A(d)(1). Base erosion payments also include amounts received or accrued by the foreign corporation in connection with the acquisition of depreciable or amortizable property (section 59A(d)(2)), reinsurance payments (section 59A(d)(3)), and certain payments relating to expatriated entities (section 59A(d)(4)).

The term “base erosion tax benefit” generally means any U.S. deduction that is allowed under chapter 1 for the tax year with respect to any base erosion payment. See section 59A(c)(2)(A) and (B) for further details.

If the foreign corporation paid or accrued any interest or royalty (including in the case of a foreign corporation that is a partner in a partnership, the foreign corporation’s allocable share of interest or royalty paid by the partnership) for which a deduction is disallowed under section 267A, check “Yes” for question 5a and enter the total amount for which a deduction is not allowed on line 5b. The amount reported on line 5b should not include disallowed deductions attributable to interest or royalty paid or accrued by a U.S. taxable branch of the foreign corporation; such amounts are reported on Form 1120-F.

Interest or royalty paid or accrued by a foreign corporation (including through a partnership) is subject to section 267A, provided in general that the foreign corporation is a CFC (and there are one or more U.S. tax residents that own directly or indirectly at least 10% of the stock of the CFC). Section 267A disallows a deduction for certain interest or royalty paid or accrued pursuant to a hybrid arrangement, to the extent that, under the foreign tax law, there is not a corresponding income inclusion (including long-term deferral). For more detailed instructions, see the instructions for Form 1120, Schedule K, Question 21.

Check the “Yes” box on line 6a if the filer of this Form 5471 is claiming a deduction under section 250 with respect to foreign-derived intangible income (FDII), and enter the amounts requested on lines 6b, 6c, and 6d. Enter U.S. dollar amounts on lines 6b, 6c, and 6d, translated from functional currency at the average exchange rate for the foreign corporation’s tax year (see section 989(b)). See Form 8993 and its instructions for information on the section 250 deduction. If no deduction is being claimed, check the “No” box and go to line 7.

Enter the foreign corporation’s reasonably anticipated benefits (RAB) share of the total present value of all platform contributions made by the U.S. taxpayer during the tax year with respect to the foreign corporation, even if only a portion (or none) of the value of those platform contributions was included in the U.S. taxpayer’s taxable income as platform contribution transaction (PCT) payments during the tax year. If possible, include a reasonable present value estimate for any PCTs that are priced using a method that does not involve the calculation of a present value. Otherwise, attach a brief statement of the reason(s) it is not possible to include a present value estimate for one or more PCTs (for example, no revenue projections for a PCT that is priced based on a sales-based royalty from a comparable uncontrolled transaction).

If the U.S. taxpayer engaged in multiple PCTs during the tax year with the foreign corporation and used different methods to price the PCTs, then check the appropriate boxes to indicate which methods were selected as the best method for one or more of the PCTs reported in the tax year. See Regulations section 1.482-7(g) for more information on the methods applicable to PCTs.

Under section 367(d), a U.S. transferor must report an annual income inclusion attributed to the intangible property transferred to a foreign corporation over the useful life of the property. Check “Yes” if the foreign corporation received any intangible property in a prior year or the current tax year in an exchange under section 351 or section 361 from a U.S. transferor that is required to report a section 367(d) annual income inclusion for the tax year. If “Yes,” complete line 14b.

Enter the amount of the E&P reduction made by the foreign corporation for the current tax year that equals the amount required to be included in the income of the U.S. transferor. See section 367(d). This amount should also be entered on Schedule H, Current Earnings and Profits, as a net subtraction on line 2i.

A foreign corporation may qualify as an expatriated foreign subsidiary under Regulations section 1.7874-12(a)(9) if such foreign corporation is a CFC with respect to which an expatriated entity as defined in Regulations section 1.7874-12(a)(8) is a U.S. shareholder. Certain transactions involving an expatriated foreign subsidiary and/or its U.S. shareholders may be subject to special rules. If the answer to Question 15 is “Yes,” attach a statement providing the name and EIN of the domestic corporation or partnership as defined in Regulations section 1.7874-12(a)(6) and the relationship of the foreign corporation to the domestic corporation or partnership.

Check the “Yes” box on line 19 if you answer “Yes” to any of the 22 questions in the Schedule G, Line 19 table below. If “Yes,” enter the Corresponding Code(s) from the table in the entry space provided on line 19 of the form. Enter the applicable corresponding code in capital letters. Enter a space between each code. Also attach the statement described in the table below.

Form 5471

| Question | See Worksheet A in the Schedule I instructions | If “Yes,” Corresponding Code to enter on Schedule G, line 19 | Code Description | If “Yes,” content of statement to be attached to Form 5471 | |

| 1 | During the tax year, was the sum of the CFC’s foreign base company income (determined without regard to deductions) and gross insurance income less than the lesser of 5% of gross income or $1 million? | In other words, is line 7 less than line 8 and less than $1 million? | DM | De minimis | Amount excluded by reason of the de minimis rule (but only to the extent not already included in amounts below) |

| 2 | During the tax year, did the CFC receive any item of income that was subject to an effective rate of income tax imposed by a foreign country greater than 90% of the maximum rate of tax specified in section 11? | In other words, is line 13g, 14d, 15d, 16d, 18d, or 19d of Worksheet A greater than zero? | HT | High Tax | Sum of the amounts from lines 13g, 14d, 15d, 16d, 18d, and 19d |

| 3 | During the tax year, was the CFC’s foreign personal holding company income, foreign base company sales income, or foreign base company services income reduced so as to take into account any deductions (including taxes)? | In other words, is line 13b, 13d, 13e, 14b, 15b, or 16b of Worksheet A greater than zero? | DED | Deductions taken into account | Sum of the amounts from lines 13b, 13d, 13e, 14b, 15b, and 16b |

| 4 | During the tax year, did the CFC have any gains or losses that (i) arise out of commodity hedging transactions, (ii) are active business gains or losses from the sale of commodities (and substantially all of the corporation’s commodities are property described in section 1221(a)(1), (2), or (8)), or (iii) are foreign currency gains or losses (as defined in section 988(b)) attributable to any section 988 transactions? | In other words, are any amounts described in section 954(c)(1)(C)(i), (ii), or (iii) excluded from line 1c of Worksheet A? | AHC | Active/hedging commodities | Sum of the excluded amounts described in section 954(c)(1)(C)(i), (ii), and (iii) |

| 5 | During the tax year, did the CFC have excess foreign currency gains over foreign currency losses as defined in section 988(b) attributable to any section 988 transaction directly related to the business needs of the foreign corporation? | In other words, are any amounts excluded from line 1d of Worksheet A by reason of being attributable to a transaction(s) directly related to the business needs of the foreign corporation? | BN | Business needs | Amount excluded |

| 6 | During the tax year, did the CFC receive, from a person other than a related person within the meaning of section 954(d)(3), rents or royalties that were derived in the active conduct of a trade or business? | In other words, are any amounts described in section 954(c)(2)(A) excluded from line 1a of Worksheet A? | ARR | Active rents/royalties | Amount excluded |

| 7 | During the tax year, did the CFC derive, in the conduct of a banking business, interest that is export financing interest? | In other words, are any amounts described in section 954(c)(2)(B) excluded from line 1a of Worksheet A? | EF | Certain export financing | Amount excluded |

| 8 | During the tax year, was the CFC a regular dealer in property described in section 954(c)(1)(B), forward contracts, option contracts, or similar financial instruments (including notional principal contracts and all instruments referenced to commodities)? If so, did the foreign corporation derive any item of income, gain, deduction, or loss (other than any item described in section 954(c)(1)(A), (E), or (G)) from any transaction entered into in the ordinary course of its trade or business as a regular dealer? | In other words, are any amounts described in section 954(c)(2)(C)(i) excluded from line 1a of Worksheet A? | RD | Regular dealers | Amount excluded |

| 9 | During the tax year, was the CFC a securities dealer within the meaning of section 475? If so, did the foreign corporation derive any interest or dividend or equivalent amount described in section 954(c)(1)(E) or (G) from any transaction entered into in the ordinary course of its trade or business as a securities dealer? | In other words, are any amounts described in section 954(c)(2)(C)(ii) excluded from line 1a of Worksheet A? | SD | Securities dealers | Amount excluded |

Form 5471, Schedule G, Line 19, continued

| Question | See Worksheet A in the Schedule I instructions | If “Yes,” Corresponding Code to enter on Schedule G, line 19 | Code Description | If “Yes,” content of statement to be attached to Form 5471 | |

| 10 | During the tax year, did the CFC receive dividends* or interest** from a related person that (i) is a corporation created or organized under the laws of the same country under the laws of which the CFC is created or organized, and (ii) has a substantial part of its assets used in its trade or business located in the same foreign country? *Dividends (other than dividends with respect to any stock, which is attributable to earnings and profits of the distributing corporation, accumulated during any period during which the person receiving such dividend did not hold such stock directly or indirectly through a chain of one or more subsidiaries each of which meets the requirements (i) and (ii)). **Interest (other than interest that reduces the payor’s subpart F income or creates or increases a deficit that may reduce the subpart F income of the payor or another CFC). | In other words, are any amounts described in section 954(c)(3)(A)(i) excluded from line 1a of Worksheet A? | SCDI | Same country dividends/interest | Amount excluded |

| 11 | During the tax year, did the CFC receive, from a corporation that is a related person, rents or royalties* for the use of, or privilege of using, property within the country under the laws of which the CFC is created or organized? *Rents or royalties (other than rents or royalties that reduce the payor’s subpart F income or create or increase a deficit that may reduce the subpart F income of the payor or another CFC). | In other words, are any amounts described in section 954(c)(3)(A)(ii) excluded from line 1a of Worksheet A? | SCRR | Same country rents/royalties | Amount excluded |

| 12 | During the tax year, did the CFC receive or accrue from a related CFC dividends, interest (including factoring income treated as income equivalent to interest for purposes of section 954(c)(1)(E)), rents, or royalties attributable or properly allocable to income of the related person which is neither subpart F income nor income treated as effectively connected with the conduct of a trade or business in the United States? | In other words, are any amounts excluded from line 1a of Worksheet A by reason of the look-through rule described in section 954(c)(6)? | LT | Look through | Amount excluded |

| 13 | During the tax year, did the CFC derive income (either directly or through a branch or similar establishment, for example, disregarded entity) in connection with the purchase or sale from, to, or on behalf of a related person, of agricultural commodities not grown in the United States in commercially marketable quantities? | In other words, are any amounts excluded from line 3 of Worksheet A by reason of the special rule in Regulations section 1.954-3(a)(1)(ii)? | AC | Agricultural commodities | Amount excluded |

| 14 | During the tax year, did the CFC derive income (either directly or through a branch or similar establishment, for example, disregarded entity) in connection with the purchase or sale from, to, or on behalf of a related person, of personal property manufactured in the same country under the laws of which the CFC is created or organized? | In other words, are any amounts that are derived in connection with property that does not satisfy section 954(d)(1)(A) excluded from line 3 of Worksheet A (that is, income excluded by reason of Regulations section 1.954-3(a)(2))? | SCM | Same country manufacturing | Amount excluded |

| 15 | During the tax year, did the CFC derive income (either directly or through a branch or similar establishment, for example, disregarded entity) in connection with the purchase or sale from, to, or on behalf of a related person, of personal property purchased or sold for use or consumption in the same country under the laws of which the CFC is created or organized? | In other words, are any amounts that are derived in connection with property that does not satisfy section 954(d)(1)(B) excluded from line 3 of Worksheet A (that is, income excluded by reason of Regulations section 1.954-3(a)(3))? | SCSU | Same country sales/use | Amount excluded |

| 16 | During the tax year, did the CFC derive income (either directly or through a branch or similar establishment, for example, disregarded entity) in connection with the purchase or sale from, to, or on behalf of a related person, of personal property manufactured by the CFC within the meaning of Regulations section 1.954-3(a)(4)(ii) or (iii)? | In other words, are any amounts excluded from line 3 of Worksheet A by reason of Regulations section 1.954-3(a)(4)(ii) or (iii)? | PM | Physical manufacturing | Amount excluded |

Form 5471, Schedule G, Line 19, continued

| Question | See Worksheet A in the Schedule I instructions | If “Yes,” Corresponding Code to enter on Schedule G, line 19 | Code Description | If “Yes,” content of statement to be attached to Form 5471 | |

| 17 | During the tax year, did the CFC derive income (either directly or through a branch or similar establishment, for example, disregarded entity) in connection with the purchase or sale from, to, or on behalf of a related person, of personal property manufactured by the CFC within the meaning of Regulations section 1.954-3(a)(4)(iv)? | In other words, are any amounts excluded from line 3 of Worksheet A by reason of Regulations section 1.954-3(a)(4)(iv)? | SC | Substantial contribution | Amount excluded |

| 18 | (a) During the tax year, did the CFC derive income in connection with the purchase from or sale to a related or unrelated person of personal property manufactured or sold for use outside the country under the laws of which the CFC is created or organized (for example, property manufactured or sold by a disregarded entity of the CFC)? (b) During the tax year, did the CFC derive income (either directly or through a branch or similar establishment, for example, disregarded entity) in connection with the purchase or sale from, to, or on behalf of a related party (for example, purchase or sales commission income)? | In other words, are any amounts excluded from line 3 of Worksheet A by reason of disregarding a branch or similar establishment (including a disregarded entity) of the CFC as separate from the CFC? | BR | Branch | Amount excluded |

| 19 | During the tax year, was the CFC an eligible CFC (as defined in section 954(h)(2)) that derived qualified banking or financing income (as defined in section 954(h)(3))? | In other words, are any amounts excluded from lines 1a–1i of Worksheet A by reason of the special rule described in section 954(h)? | AF | Active financing | Amount excluded |

| 20 | During the tax year, was the CFC a qualifying insurance company (as defined in section 953(e)(3)) that derived qualified insurance income (as defined in section 954(i)(2))? | In other words, are any amounts excluded from lines 1a–1i of Worksheet A by reason of the special rule described in section 954(i)? | AI | Active insurance | Amount excluded |

| 21 | During the tax year, did the subpart F income of the CFC exceed the earnings and profits of such corporation? | In other words, is line 36 of Worksheet A greater than line 37c? | EP | Earnings & profits limitation | Excess of line 36 over line 37c |

| 22 | Is the U.S. person filing this return relying on any exception(s), exclusion(s), or other provision(s) not listed above to reduce or exclude any amounts reported or reportable as subpart F income (of or with respect to the CFC)? | XX | Other | Amount excluded, reduction amount, or other amount not reported or reportable |

For the foreign corporation’s annual accounting period with respect to which reporting is being made on this Form 5471, if the foreign corporation is required to file a U.S. income tax return (for example, Form 1120‐F), check the “Yes” box if the foreign corporation has interest expense disallowed under section 163(j). If “Yes,” enter the amount from the current year Form 8990, line 31.

For the foreign corporation’s annual accounting period with respect to which reporting is being made on this Form 5471, if the foreign corporation is required to file a U.S. income tax return (for example, Form 1120‐F), check the “Yes” box if the foreign corporation has previously disallowed interest expense under section 163(j) carried forward to the current tax year. If “Yes” enter the amount from the prior year Form 8990, line 31.

Check the “Yes” box on line 22a if there was an extraordinary reduction with respect to any controlling section 245A shareholder of the foreign corporation, as defined in Regulations section 1.245A-5(i)(2), during the tax year of the foreign corporation. See Regulations section 1.245A-5(e)(2)(i) for the definition of extraordinary reduction.

If the answer to the question on line 22a was “Yes,” complete the question on line 22b. Check the “Yes” box on line 22b if any controlling section 245A shareholder (as defined in Regulations section 1.245A-5(i)(2)) made an election to close the tax year of the foreign corporation such that no amount is treated as an extraordinary reduction amount or tiered extraordinary reduction amount as to any U.S. shareholder of the foreign corporation. See Regulations section 1.245A-5(e)(3)(i) for further guidance regarding the election to close the tax year. If the “Yes” box on line 22b has been checked and the U.S. shareholder filing the Form 5471 is a controlling section 245A shareholder of the foreign corporation, the U.S. shareholder filing this Form 5471 must attach an Elective Section 245A Year-Closing Statement pursuant to Regulations section 1.245A-5(e)(3)(i)(C) containing the information required under Regulations section 1.245A-5(e)(3)(i)(D).

Schedule I

Use Schedule I to report in U.S. dollars the U.S. shareholder’s pro rata share of income from the foreign corporation reportable under subpart F and other income realized from a corporate distribution.

Certain filers may be able to use alternative information (as defined in section 3.01 of Rev. Proc. 2019-40) to determine certain amounts in this schedule. See the specific instructions for Item F, earlier, for more details.