Skip to content

Skip to content

I’ve written about tax planning in Singapore previously – https://www.mooresrowland.tax/2019/11/tax-planning-in-singapore.html

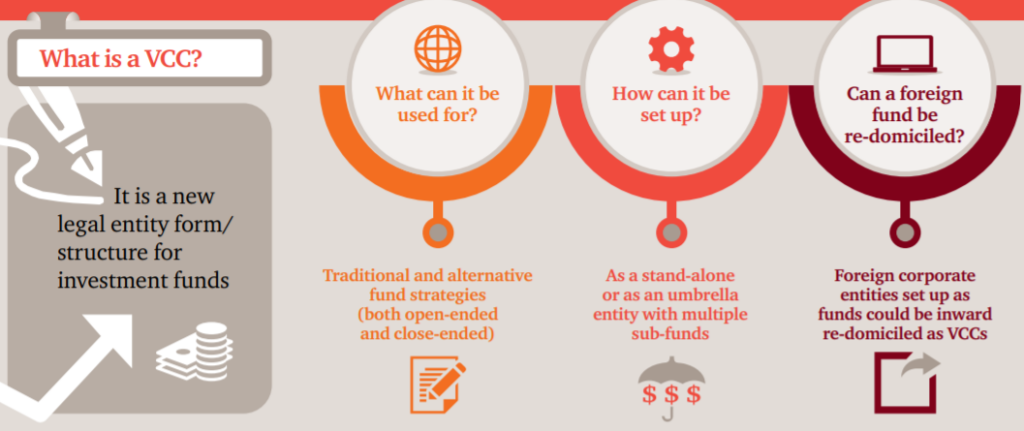

Today we’re going to take a deeper dive into VCCs which were first mentioned in the article mentioned above. The VCC’s aim is to position Singapore as a leading fund domiciliation hub. It also helps Singapore to catch up with market (and we talk more about US tax Singapore here)

leaders, following the launch of the Asia Region Funds Passport scheme as well as the European Union’s successful funds passporting scheme, known as the Undertakings for Collective Investments in Transferable Securities (UCITS).

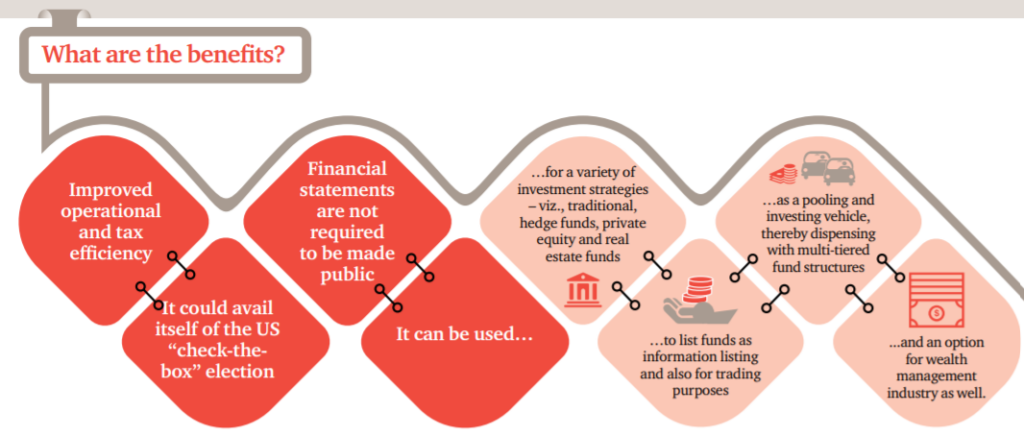

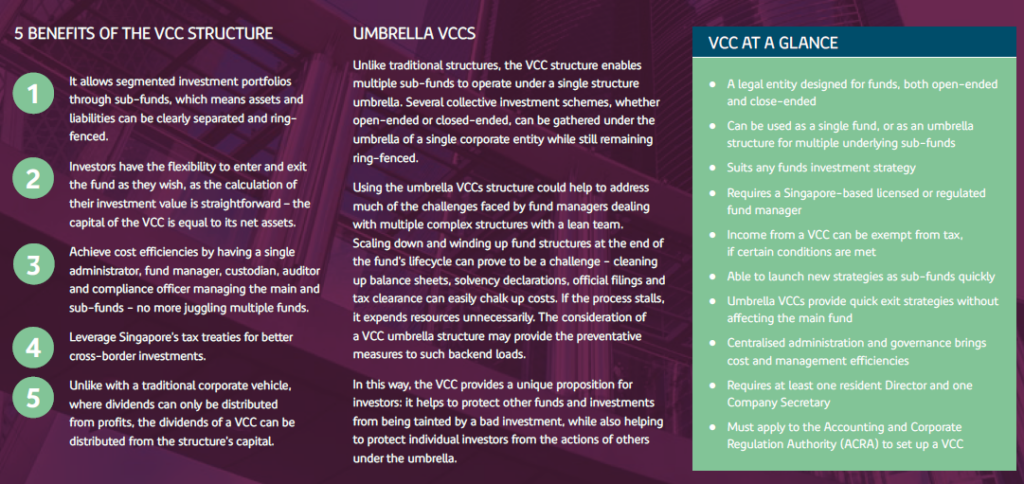

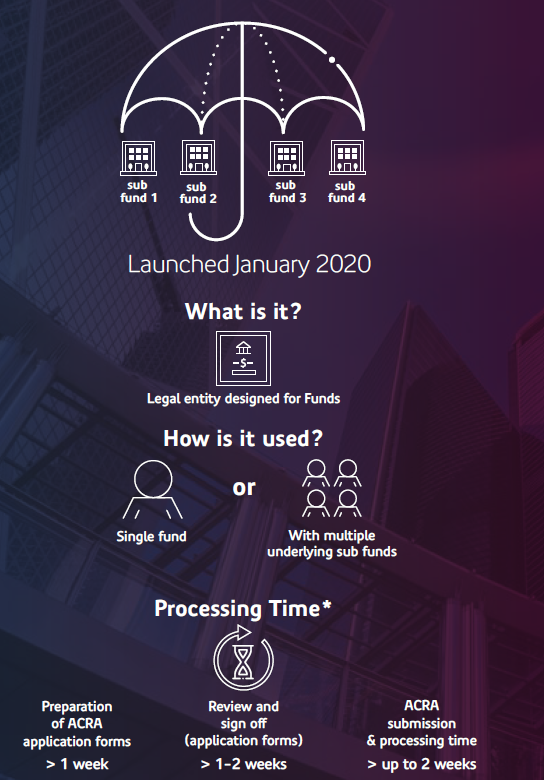

Catering to a wide range of investment strategies (traditional and alternative) and structures, the VCC can be used for either open- or close-ended funds. It also allows a variable capital shareholding structure. It can be set up as a standalone investment fund or structured as an umbrella fund with underlying sub-funds, thus holding segregated and protected portfolios.