Skip to content

Skip to content Closing a sole proprietorship when there are no employees involved is pretty easy. Simply file your final Schedule C the same way you always have in the past to report any income and expenses in the final year of business. That’s it!

The IRS doesn’t require that you inform them that you’re filing a final Schedule C or that you closed your sole proprietorship. In fact, there isn’t even a place on Schedule C to indicate that it’s a final return.

In addition, you don’t have to add any comments on Schedule C about the closing either. Just complete Schedule C as usual and file it.

Keep in mind, the only time you must file Schedule C is when your business has either income or expenses, or both, during any tax year. So, if you have neither, then you simply don’t file Schedule C for that year.

If your business is unincorporated (i.e. a sole proprietorship), you generally don’t incur the types of winding up expenses incurred by corporations and partnerships.

Corporations or Partnerships

Corporations and partnerships generally incur legal and accounting fees to dissolve the corporation and close the partnership. For example, the books have to be closed, financial statements prepared, gains and losses determined, tax returns prepared and filed, final payments made to employees, and final distributions made to owners.

If a corporation is closed:

Form 1120 – Line E(2) is used to indicate it’s a final return.

Form 1120S – Line F(2) is used to indicate it’s a final return.

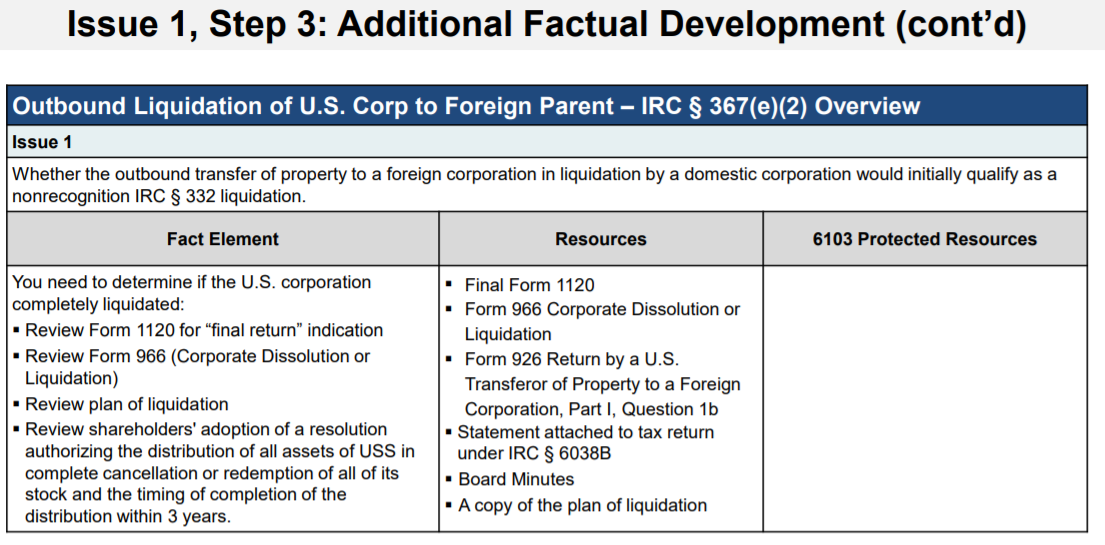

The IRS must be notified of the corporation’s termination by filing Form 966, Corporate Dissolution or Liquidation. Form 966 must be filed within 30 days after the plan or resolution of liquidation is adopted.

State Requirements for Dissolving a Corporation must also comply with your state’s requirement for dissolving the corporation. A corporation must be formally terminated and state tax obligations must be up to date. It’s not like a sole proprietorship, where you simply stop filing Schedule C and go on your merry way.

Contact your state’s Corporation Commission (or whatever the appropriate agency is called in your state) to find out the appropriate procedures to follow.

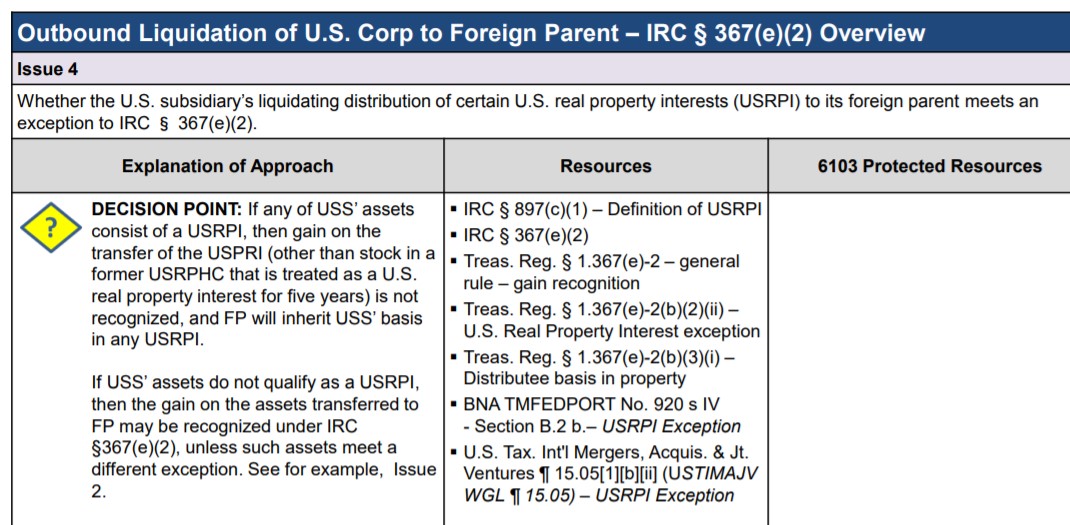

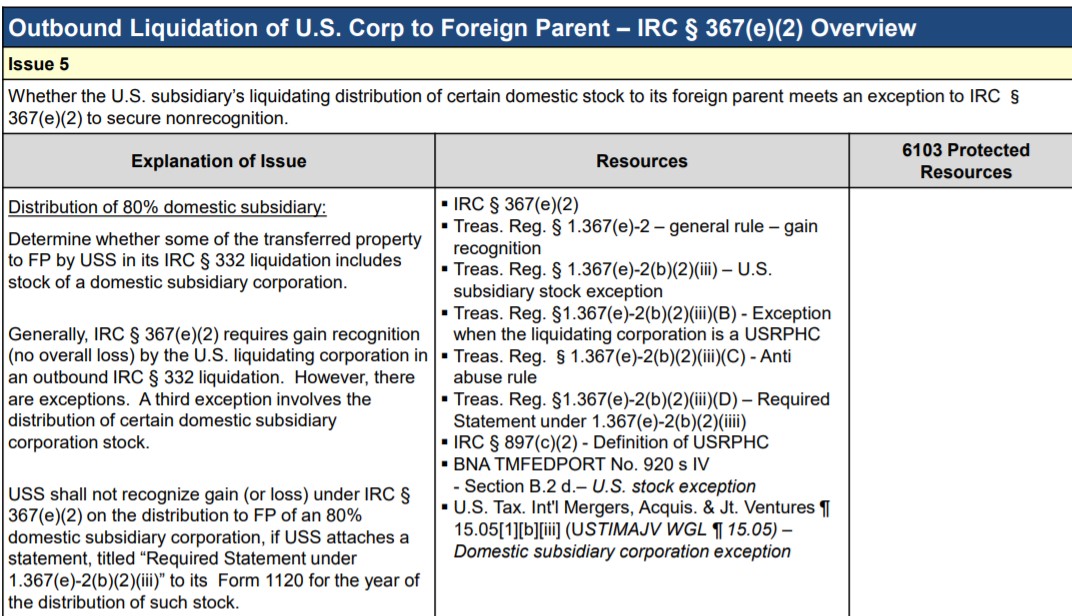

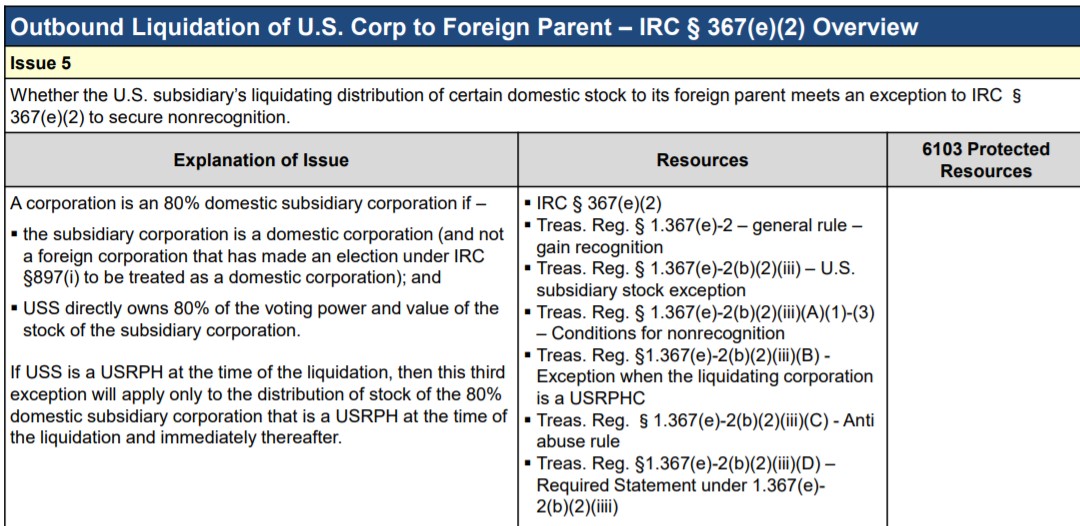

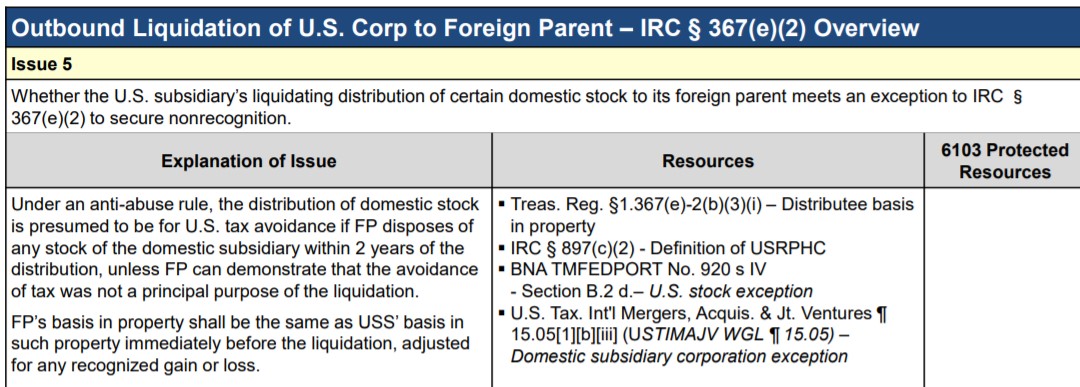

But that’s not why you’re reading this. Chances are, you’re reading this because you’re interested in finding out about “tax free” liquidations for subsidiaries of foreign companies. This is a valuable tool for non Americans wanting to invest into the US.

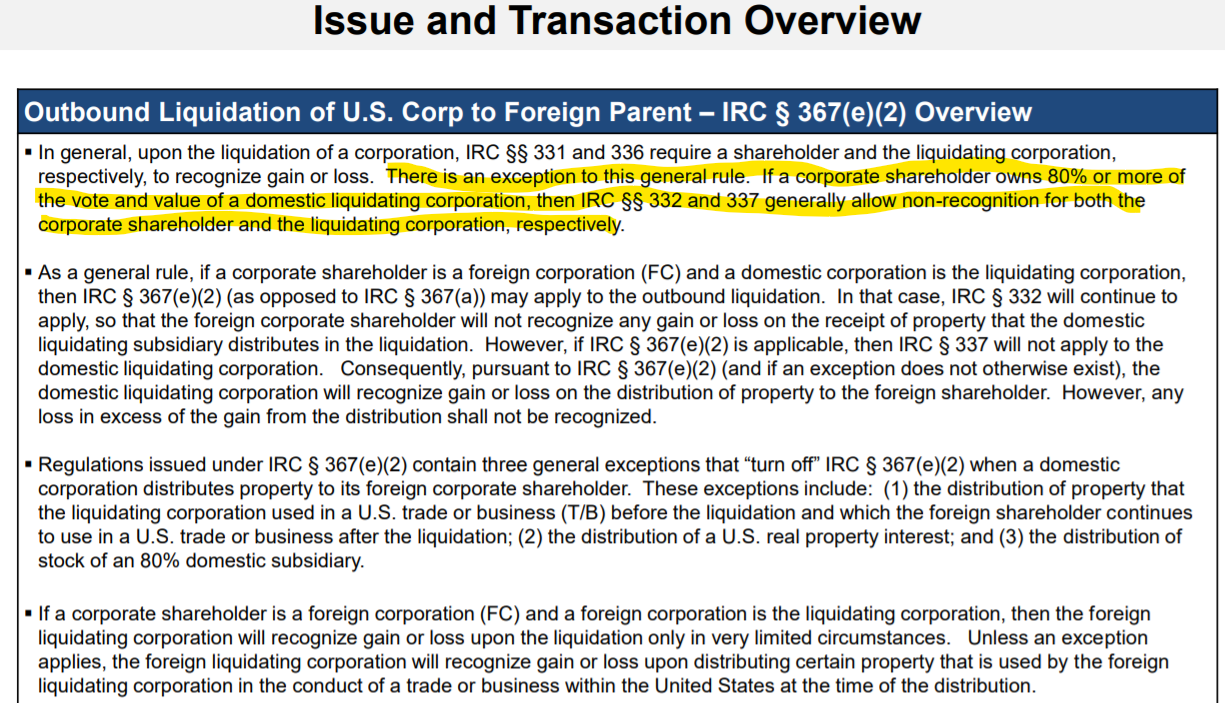

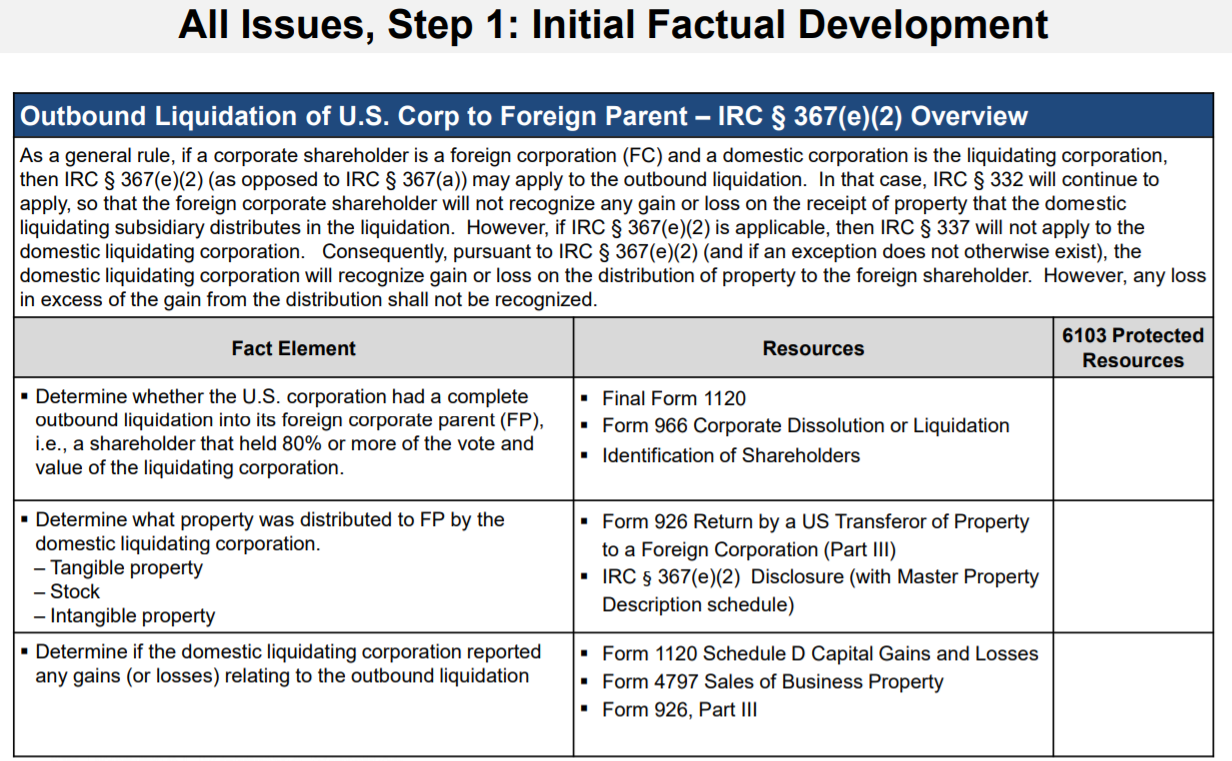

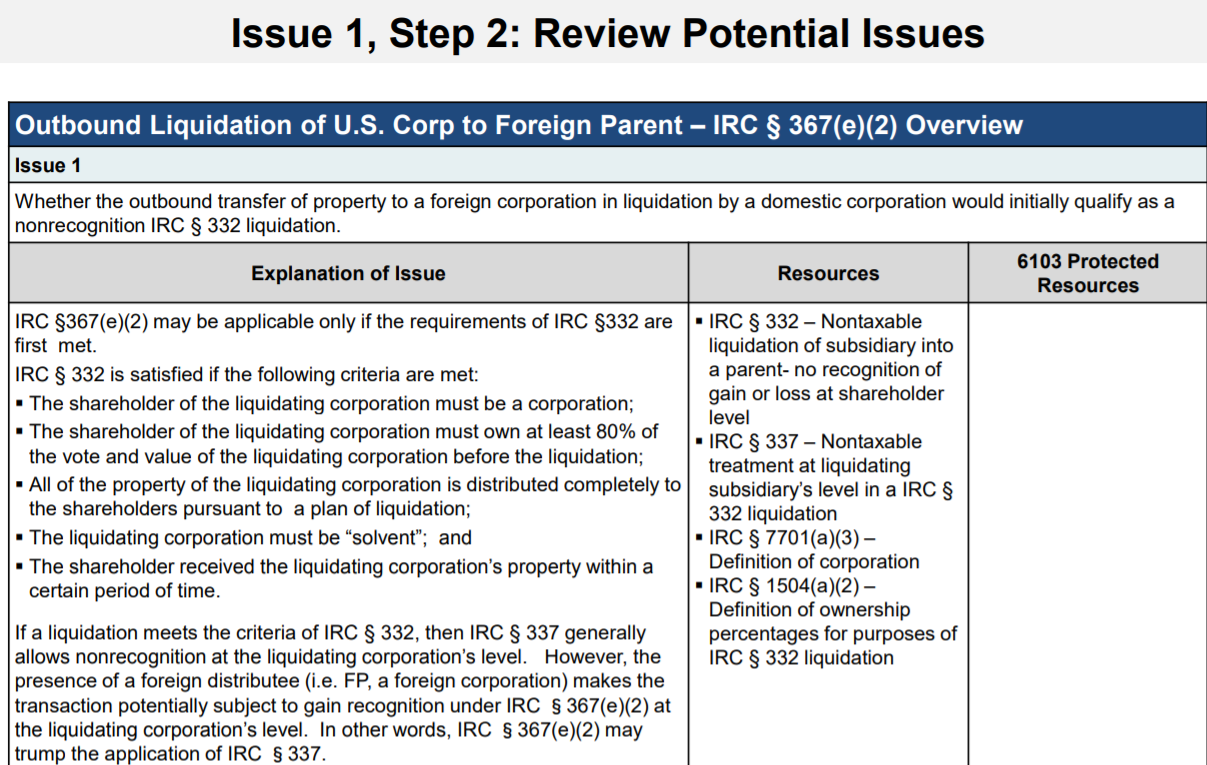

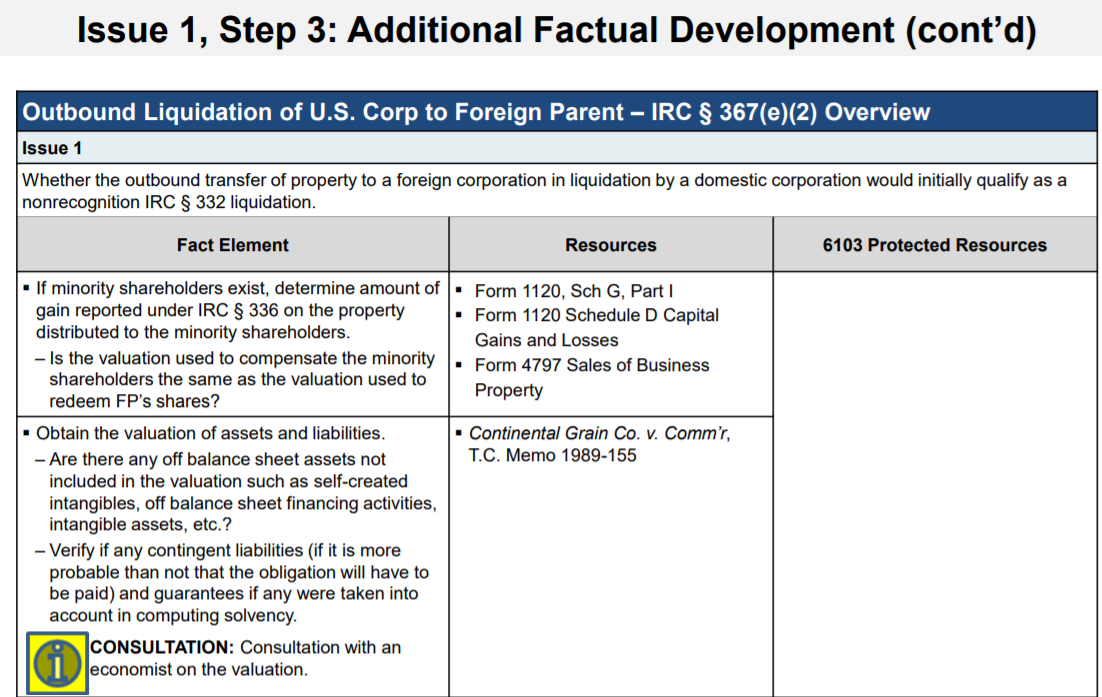

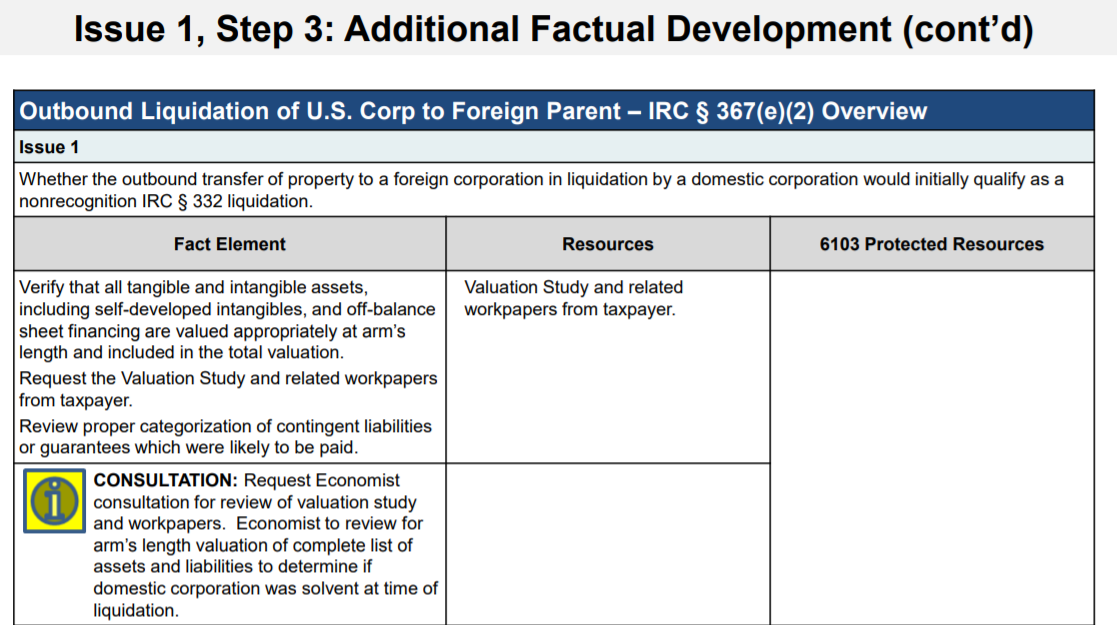

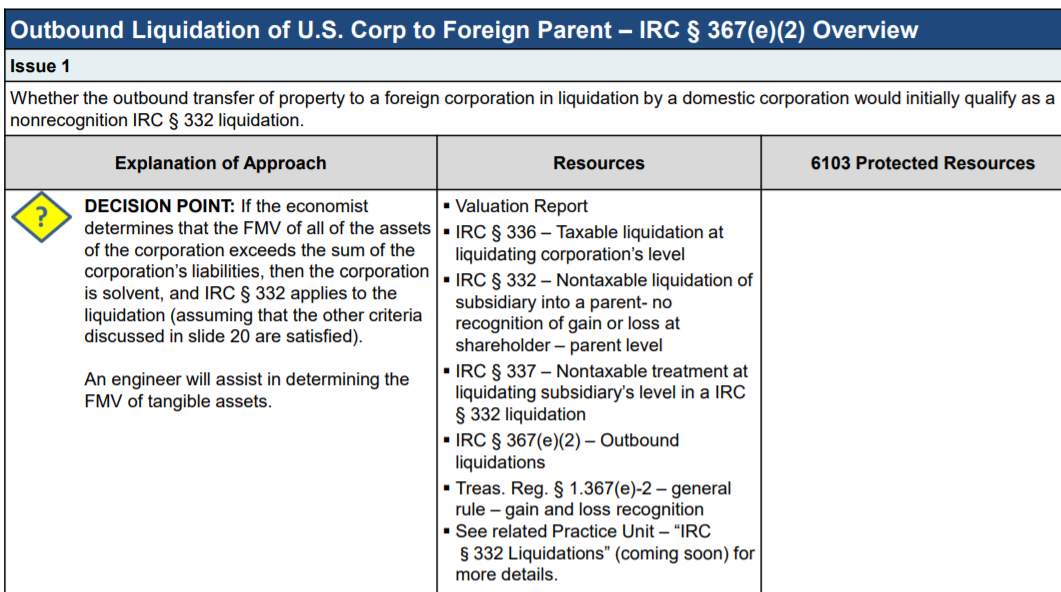

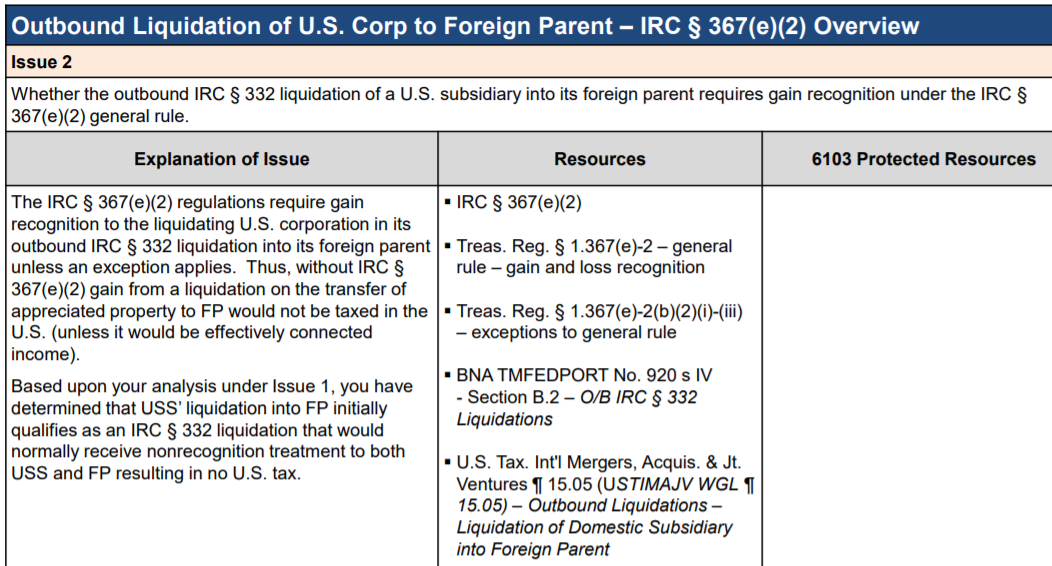

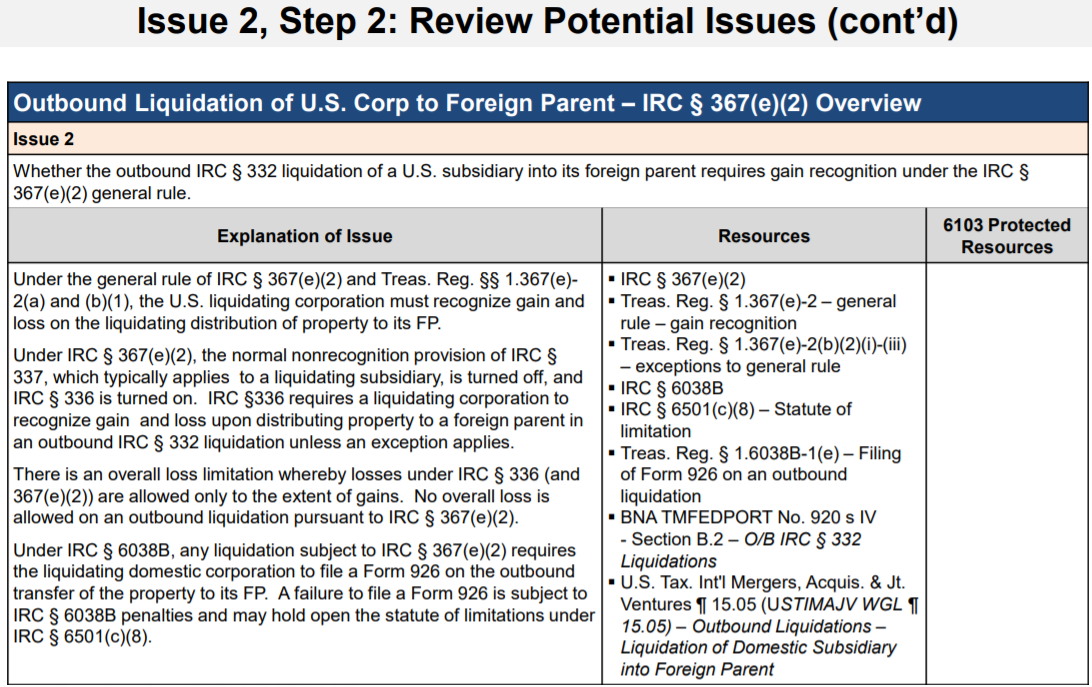

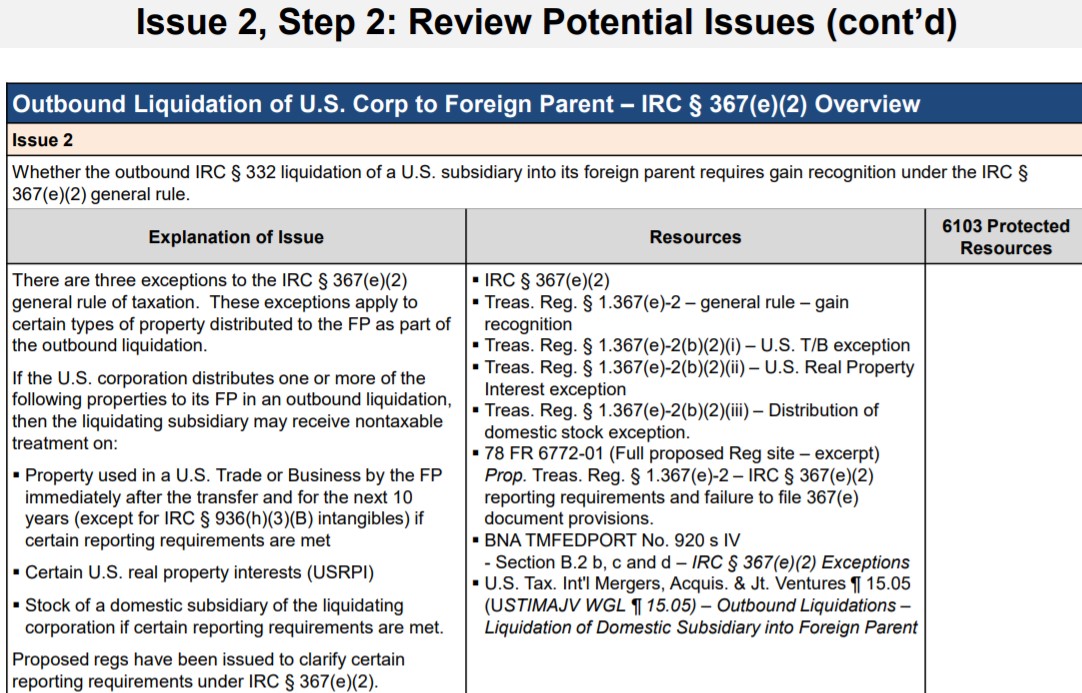

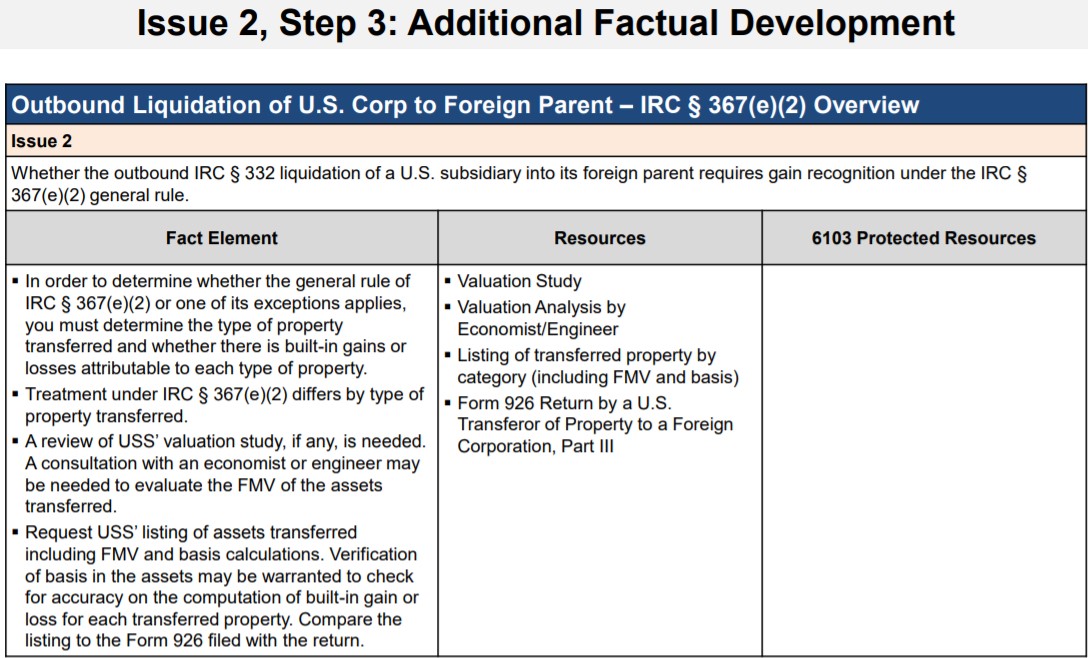

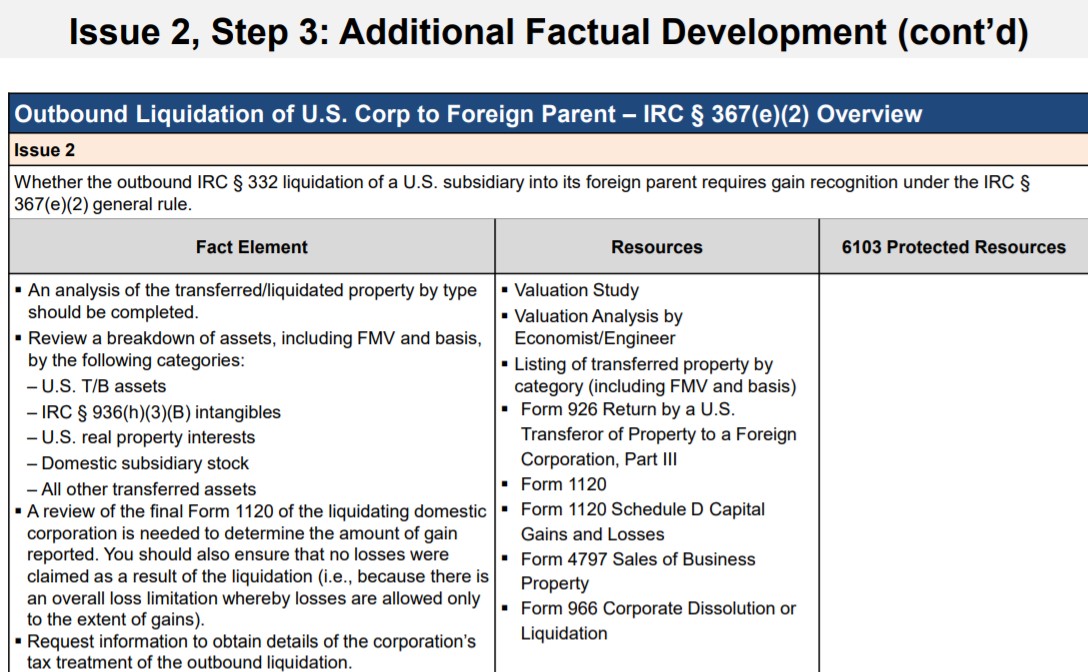

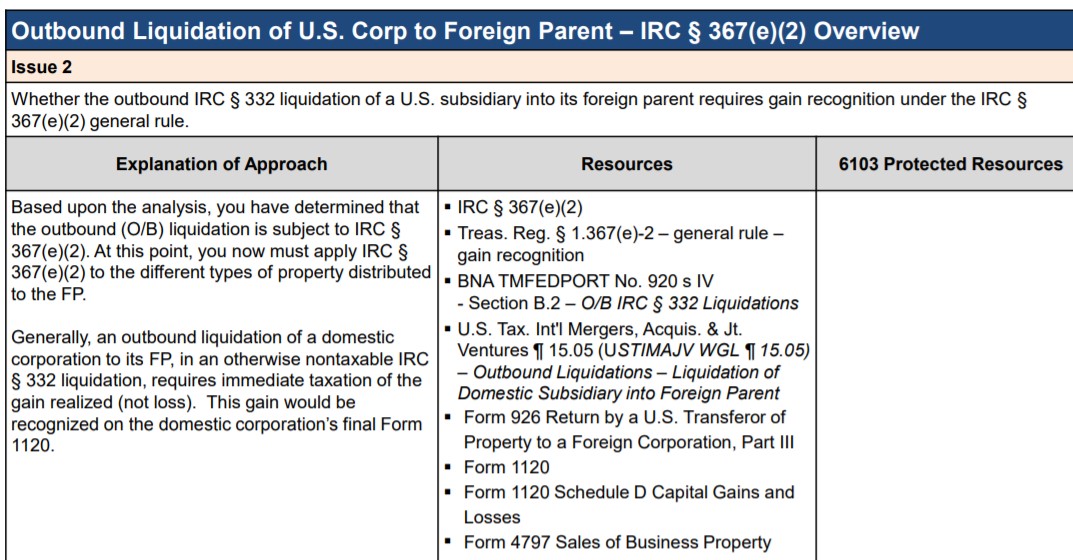

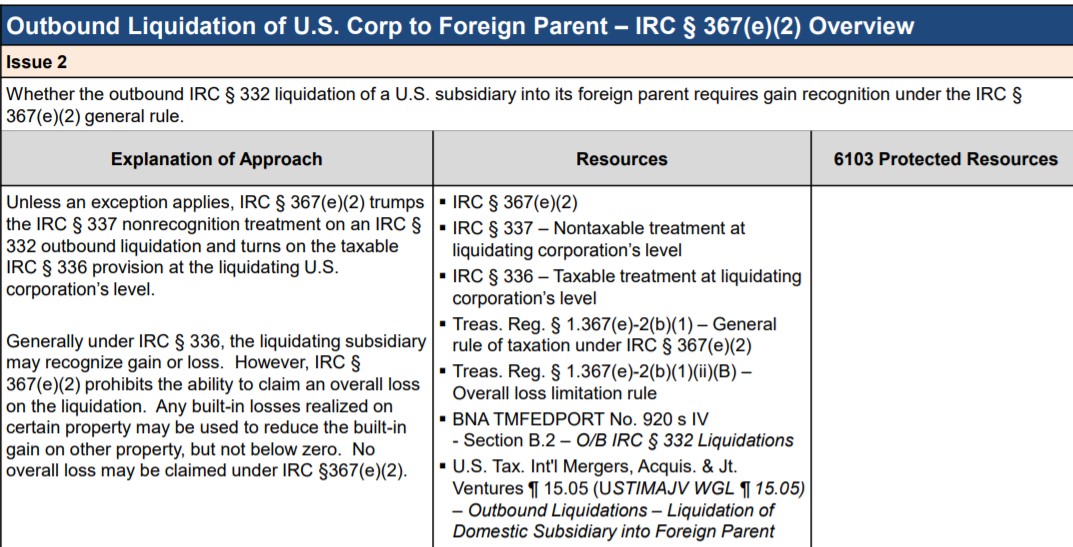

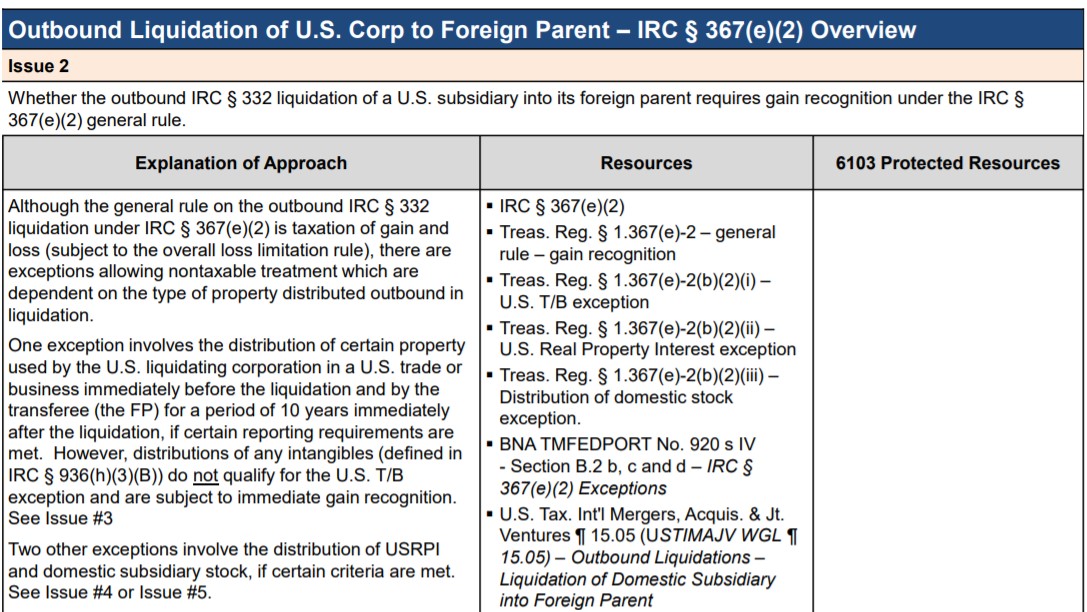

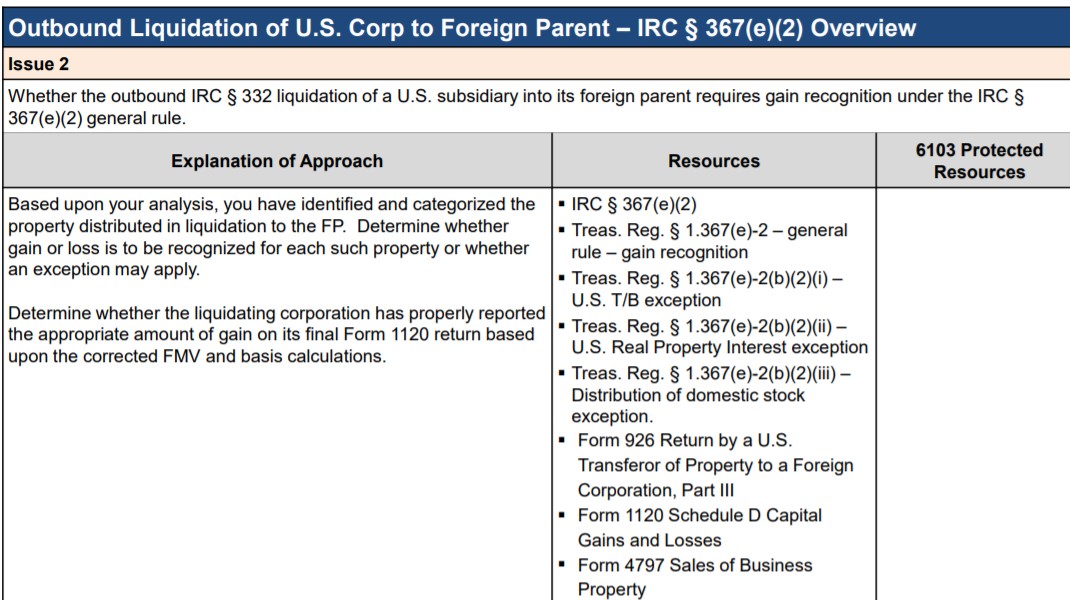

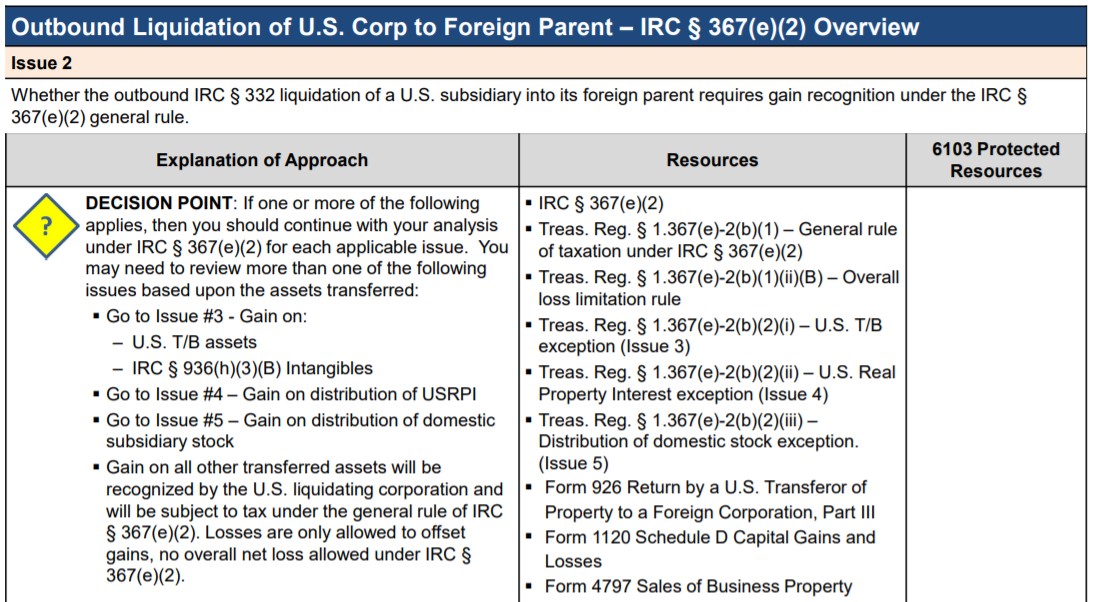

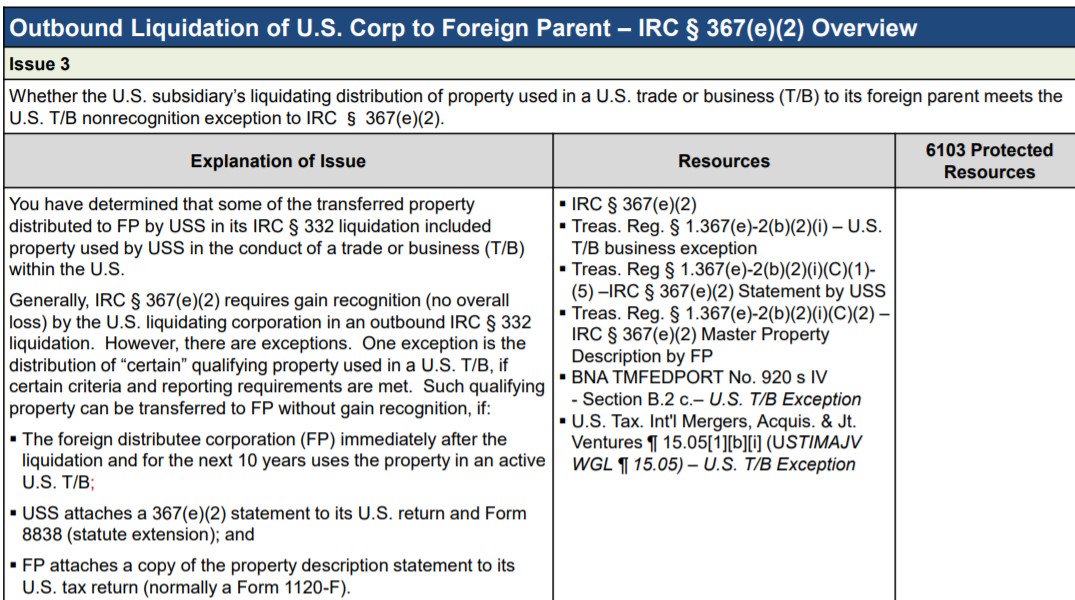

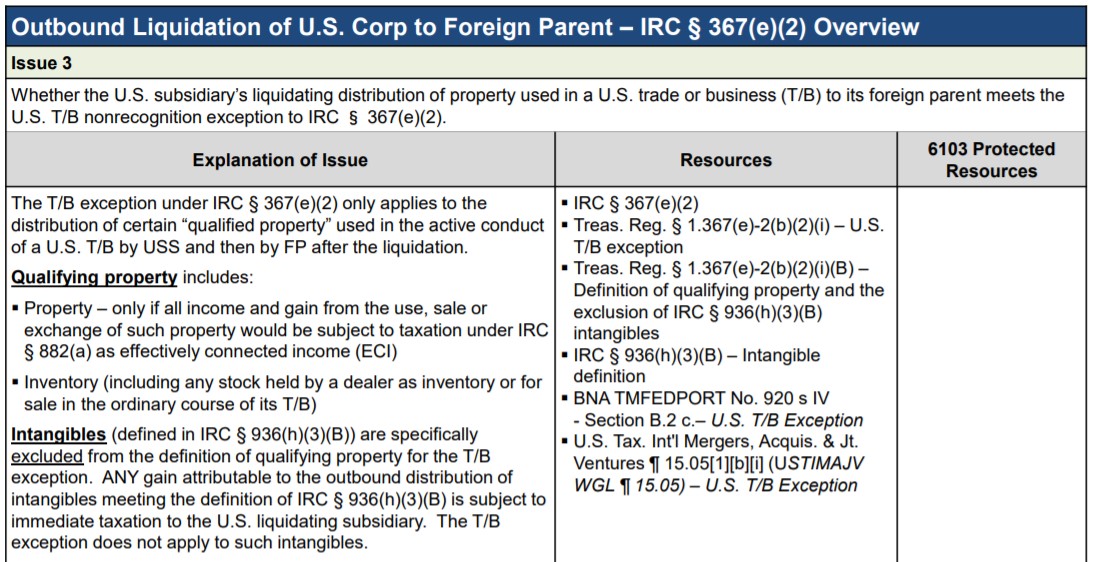

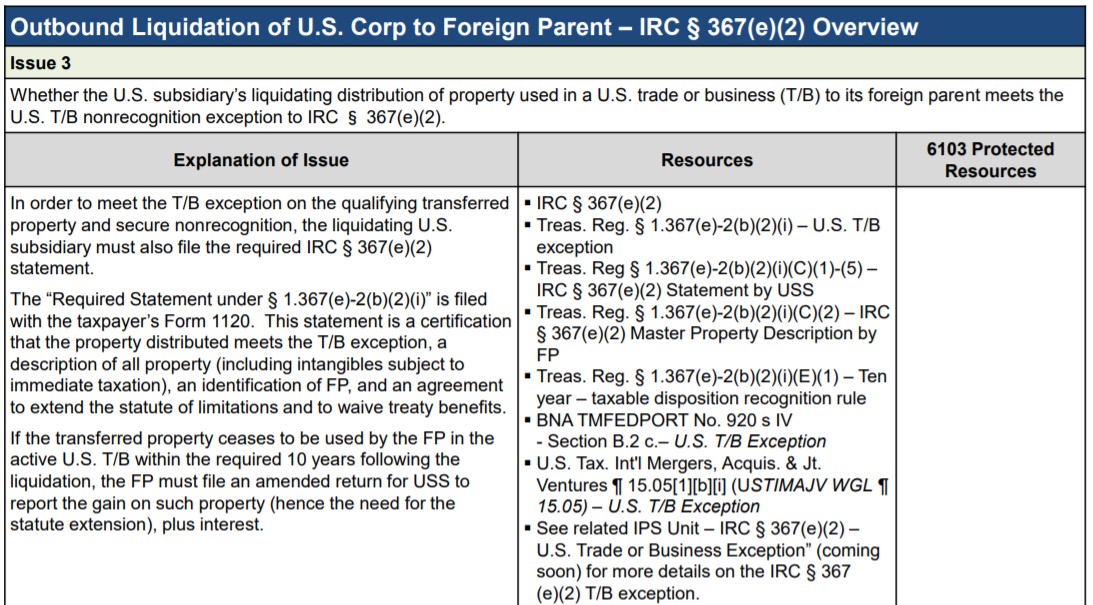

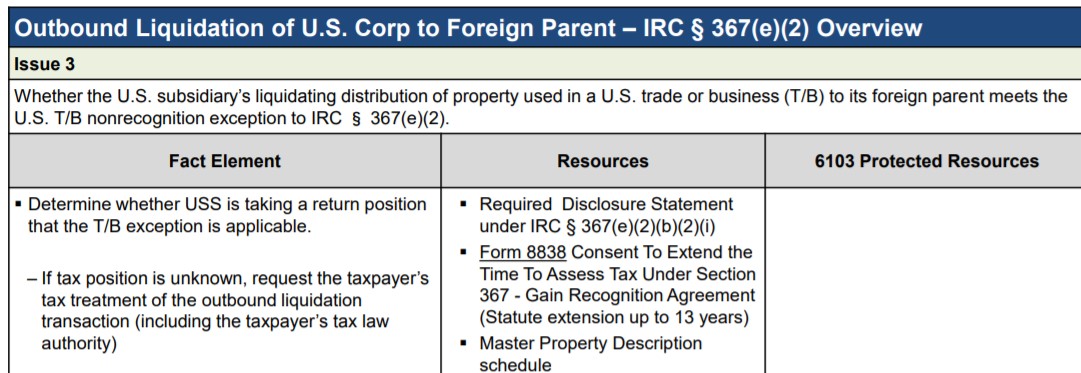

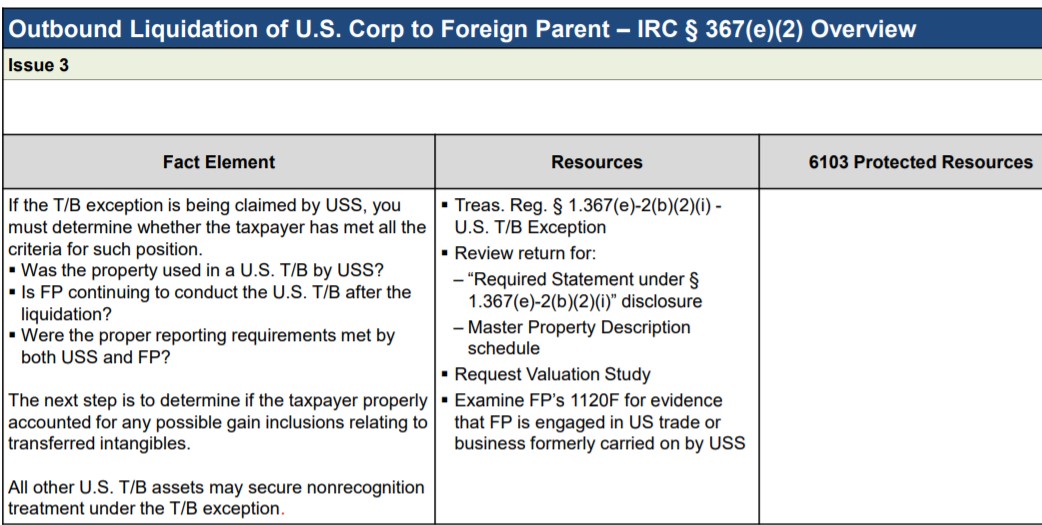

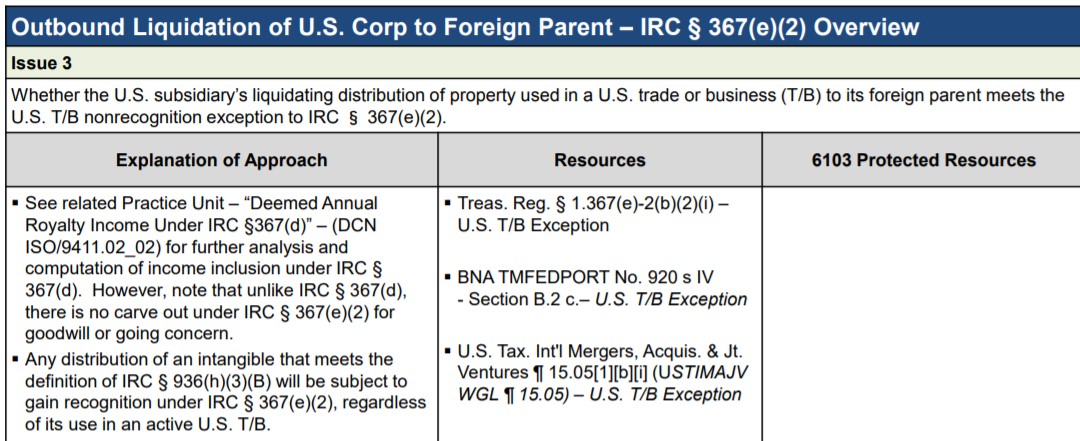

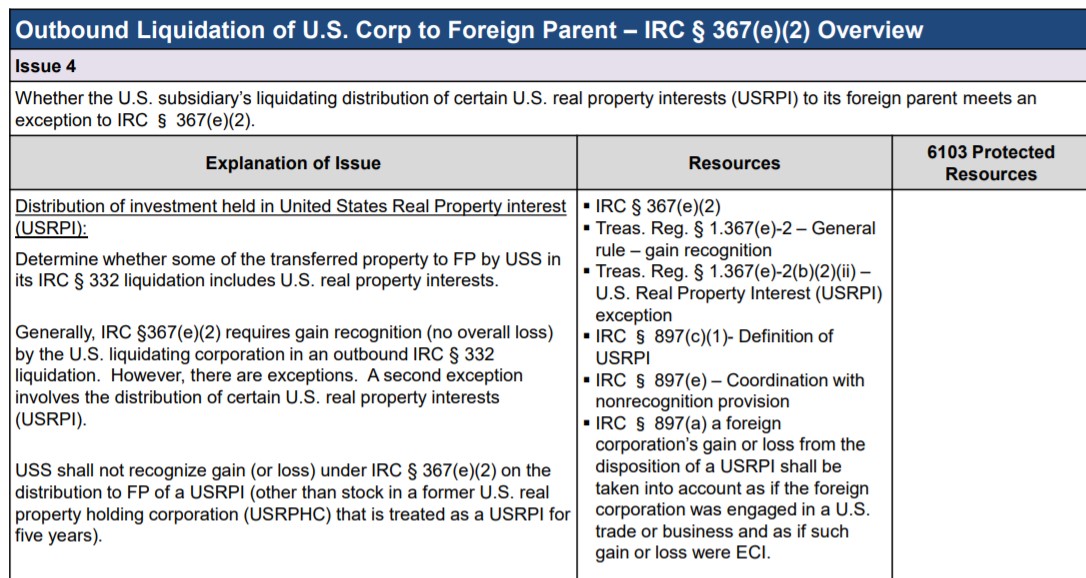

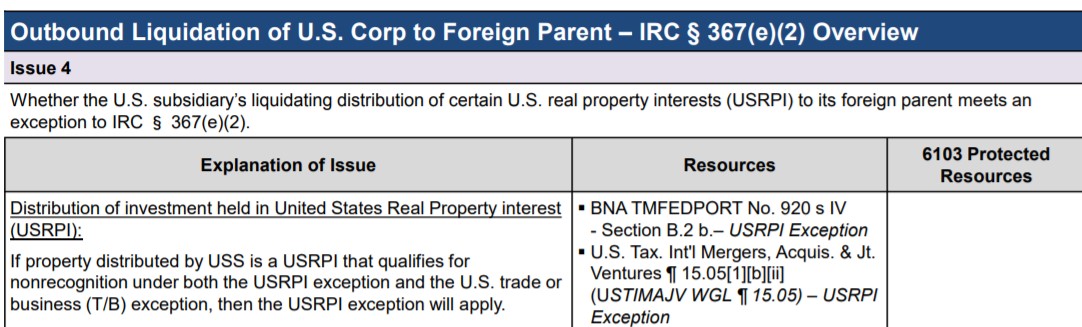

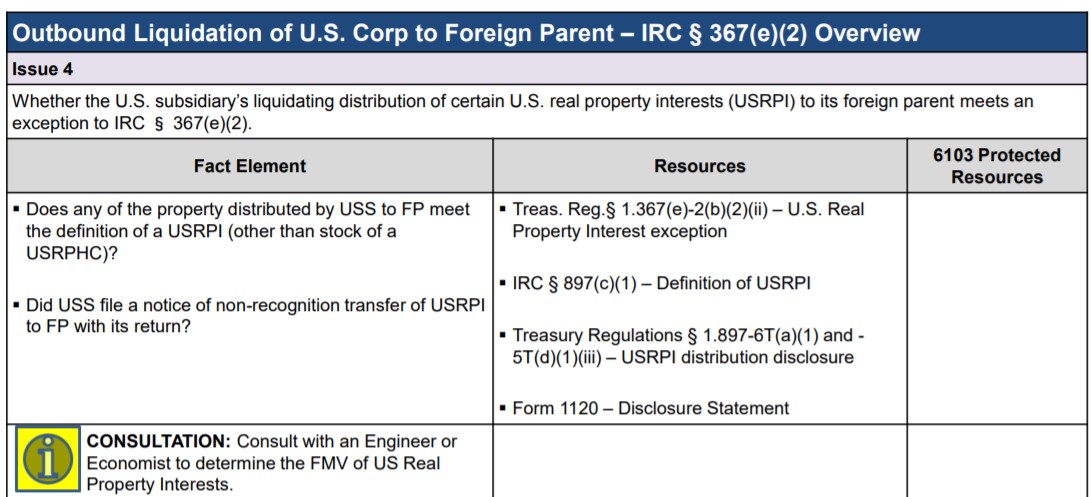

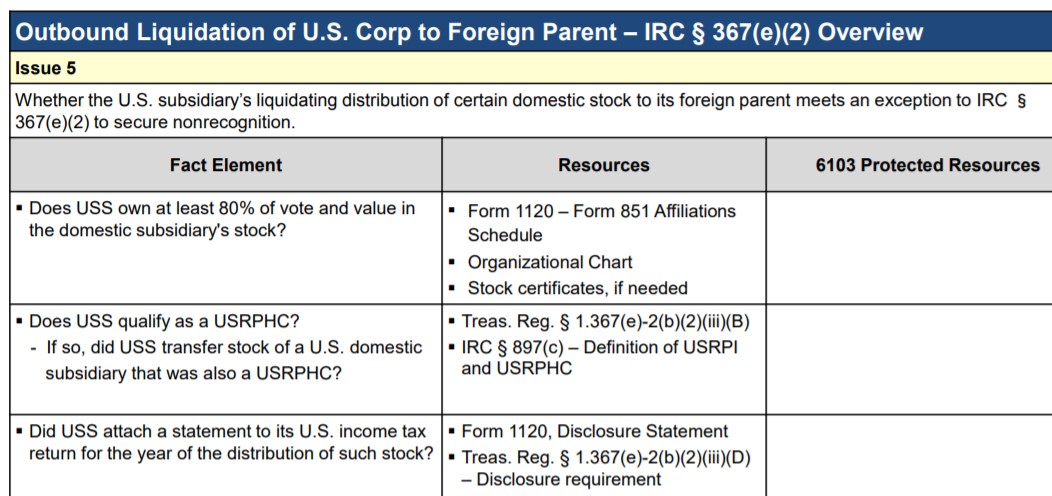

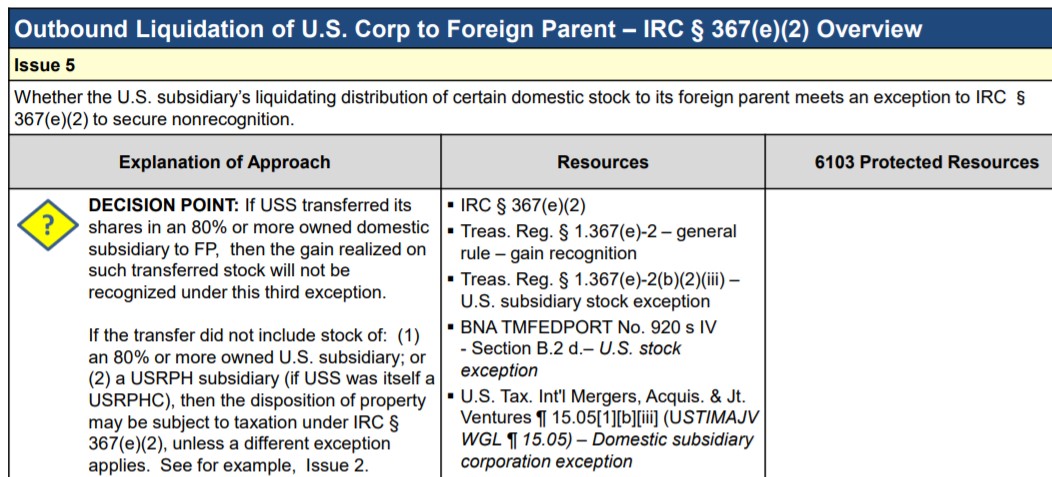

Outbound Liquidation of U.S. Corp to Foreign Parent – IRC § 367(e)(2) Overview

ETR of Company

- With an outbound transfer of appreciated property, corporations are often attempting to minimize their overall tax exposure by

moving such gain to a foreign country that has a foreign tax rate that is lower than the U.S. corporate tax rate. - If the outbound

transfer is accomplished with little to no residual U.S. tax exposure, the corporation has permanently reduced its ETR attributable to

any future disposition of such property. - You should determine the potential gain on the appreciated property that was transferred

outbound in the liquidation. - If Foreign Parent (FP) is not a CFC, an outbound liquidation of the US Subsidiary (USS) into FP does not simply result in the deferral of foreign earnings in the foreign

corporation until they are repatriated (such as would be the case in a 367(a) transfer to a CFC). Rather, it would permanently

remove non-effectively connected income (ECI) assets from US taxing jurisdiction. - If the FP in an outbound liquidation is a CFC, the liquidation of FP’s US subsidiary may reduce the ETR of its US parent by reducing

its exposure to an inclusion under section 956.

ETR Impact of Adjustment

- A liquidating US subsidiary’s outbound transfer of appreciated property to its FP that is located in a low tax foreign country that is

subject to the general rule of IRC § 367(e)(2) will generally reduce a corporation’s ETR over time; however, there may be a one-time

increase due to the up-front U.S. tax cost. An outbound liquidation of appreciated property that is subject to the general rule of IRC §

367(e)(2) will cause an increase in the corporation’s ETR.

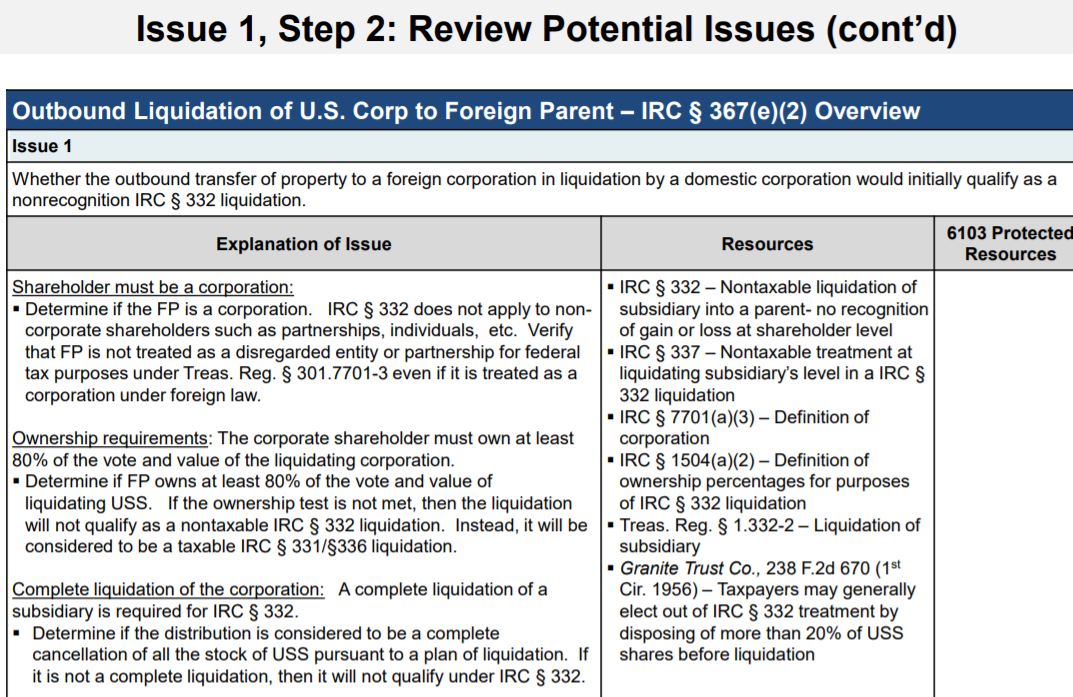

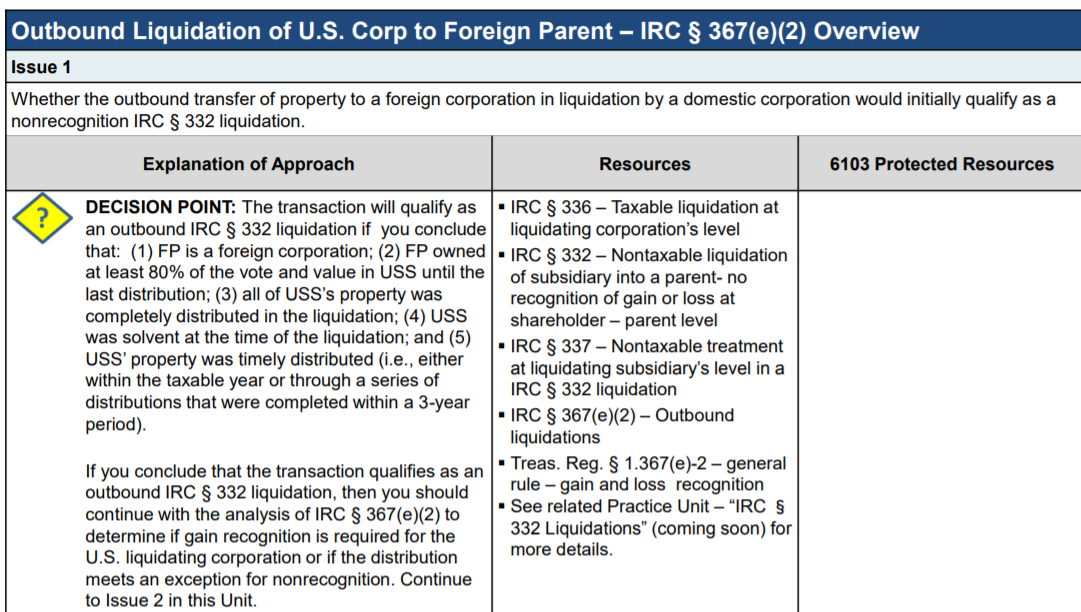

The shareholder must receive the liquidating corporation’s property within

a certain period of time.

- Generally, the liquidating corporation distributes its property to its

shareholder within the taxable year. - Alternatively, the liquidating distribution may be one of a series of

distributions when the transfer of all of the property is to be completed

within 3 years from the close of the taxable year during which is made

the first of a series of distributions under the plan of liquidation.

source:

https://www.irs.gov/pub/int_practice_units/ISI9422_10_01.pdf