Skip to content

Skip to content

Both Hong Kong and Singapore offer offshore or tax-free companies.

.

It’s hard to say which is better for setting up an offshore entity. It really depends on your business model.

.

For most people I say 2 things –

1. Hong Kong allows a local bank account for offshore companies but it takes years for offshore status to be conferred by the IRD

2. Singapore grants offshore status faster, does not require annual audits (below the threshold) but doesn’t normally allow domestic banking.

.

https://www.mooresrowland.tax/2017/12/privacy-in-dubai-compared-to-hong-kong.html

https://www.mooresrowland.tax/2017/12/where-should-you-set-up-asian-hq.html

Direct taxation of businesses

Hong Kong has a territorial system of taxation. Three conditions must be satisfied before a charge to profits tax can arise:

- the taxpayer must carry on a trade, profession or business in Hong Kong;

- profits to be charged must be from the trade, profession or business carried on by the taxpayer in Hong Kong; and

- the profits must be profits arising in or derived from Hong Kong.

Whether a person is carrying on a trade, profession or business in Hong Kong is a question of fact.

Six factors have emerged from case law in determining whether a taxpayer has engaged in trade, which collectively are referred to as the ‘badges of trade’, namely:

- the subject matter of the transactions;

- the length of ownership;

- whether there have been successive or frequent similar transactions;

- whether supplementary activities have been performed to make the assets marketable or to attract purchasers;

- the reason for the disposal or realisation of the subject matter; and

- the taxpayer’s motives.

In addition, the taxpayer’s intention to trade and the existence of a commercial purpose for the transaction are also relevant to such a determination. It is not necessary for all badges of trade to be present before a taxpayer will be found to be trading.

The definition of ‘business’ is much wider than ‘trade’. A company incorporated for the purpose of making profits for its shareholders that puts any of its assets to any gainful use is presumed to be carrying on a business. Business can be more passive than trade, with the receipt of share profits and fixed annuities having been held to be business. Similarly, the receipt of income by a holding company and the mere activity of depositing have been held to be carrying on a business as well.

One-off transactions may also fall under the definition of ‘business’ under the IRO. Having a registered office in Hong Kong of itself will not necessarily amount to carrying on a business in Hong Kong.

A ‘profession’ is not defined in the IRO. Case law indicates that it refers to work requiring either purely intellectual skill or manual labour dependent upon purely intellectual skill. If a person practices a profession but is an employee, he or she is not considered to be carrying on a profession for the purpose of profits tax.

On the source of profits, the IRO defines ‘profits arising in or derived from Hong Kong’ to include ‘all profits from business transacted in Hong Kong, whether directly or indirectly through an agent’. According to Commissioner of Inland Revenue v. Hang Seng Bank Limited, the process of determining the source of profit involves examining the gross profit of the transaction and what the taxpayer has done to earn the profit in question. However, the test outlined in this case is not consistently followed in subsequent case law, many of which revert back to an operations test (i.e., an examination of the operations of the taxpayer that contributed to the generation of net profits).

To provide some guidance and clarity in this area, the Hong Kong Inland Revenue Department (IRD) issued Departmental Interpretation and Practice Note (DIPN) No. 21. DIPNs are not legally binding, but are indicative of the IRD’s views on various legal issues. According to DIPN No. 21, transactions must be looked at separately and the profits of each transaction considered on their own. Where the gross profit from an individual transaction arises in different places, they can be apportioned as arising partly in and partly outside Hong Kong.

Further, the place where day-to-day investment decisions are undertaken does not generally determine the locality of profits. The absence of an overseas permanent establishment (PE) of a Hong Kong business does not of itself mean that all the profits of that business arise in or are derived from Hong Kong. However, practically, the IRD is less likely to accept an offshore profits claim in the absence of an offshore presence of the taxpayer.

All outgoings and business expenses incurred in the production of profits are deductible in the basis year in which they are incurred. Such expenses include:

- interest on borrowings for the purpose of producing profits, and other sums payable in connection with such borrowings, subject to the limitations outlined in Section VII.ii;

- rent paid by tenants for buildings or lands occupied for the purpose of producing profits;

- foreign tax paid by a Hong Kong taxpayer where they were incurred in the production of profits;

- bad debts;

- expenditure incurred in the repair of premises, plant, machinery, implements, utensils or articles in the production of profits;

- expenditure incurred on the replacement of any implement, utensil or article, provided that no depreciation allowances are made;

- expenditure for the registration of trademarks, designs or patents used in the trade, profession or business that produced the assessable profits; and

- contributions made by individual taxpayers to mandatory provident funds in Hong Kong.

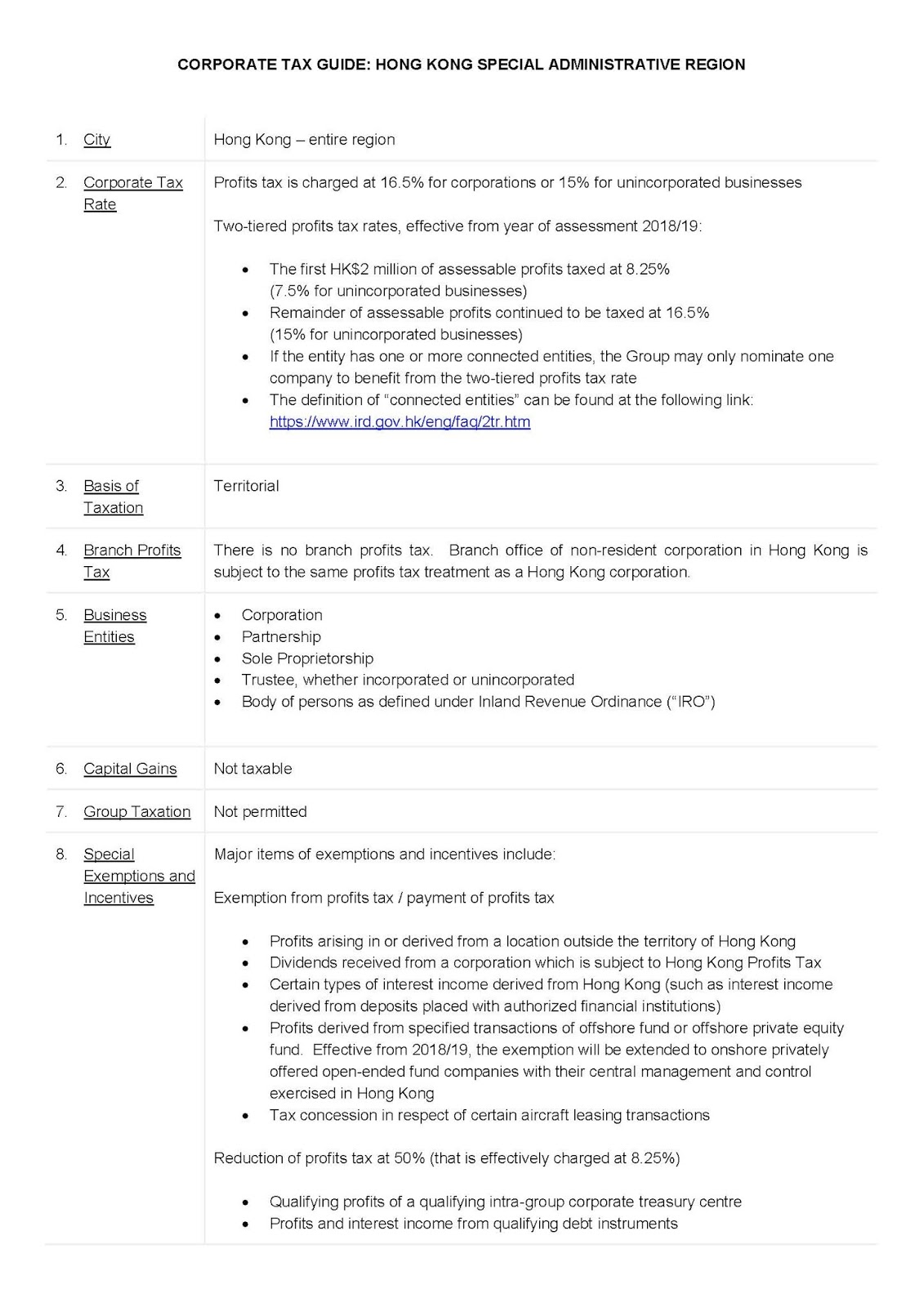

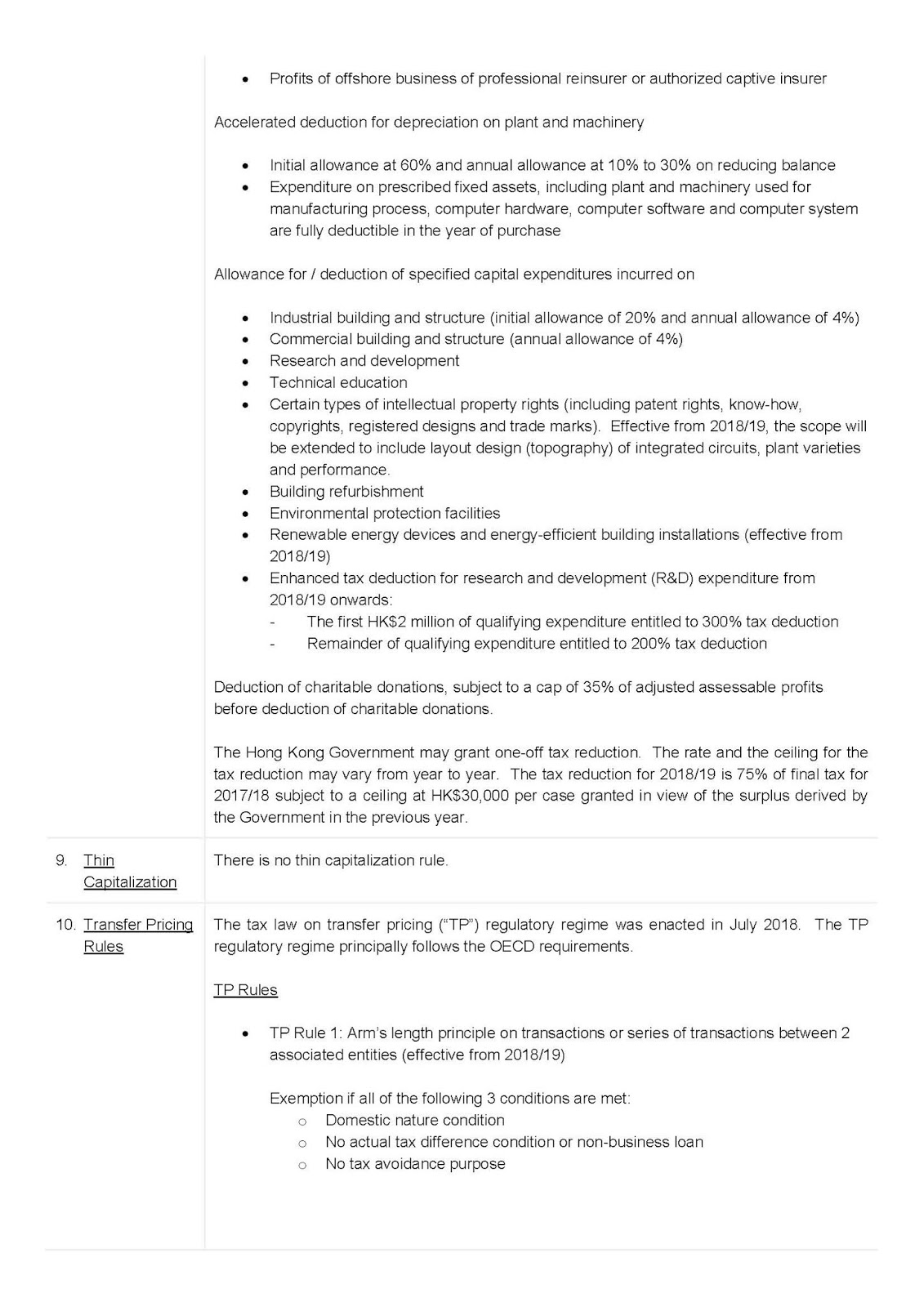

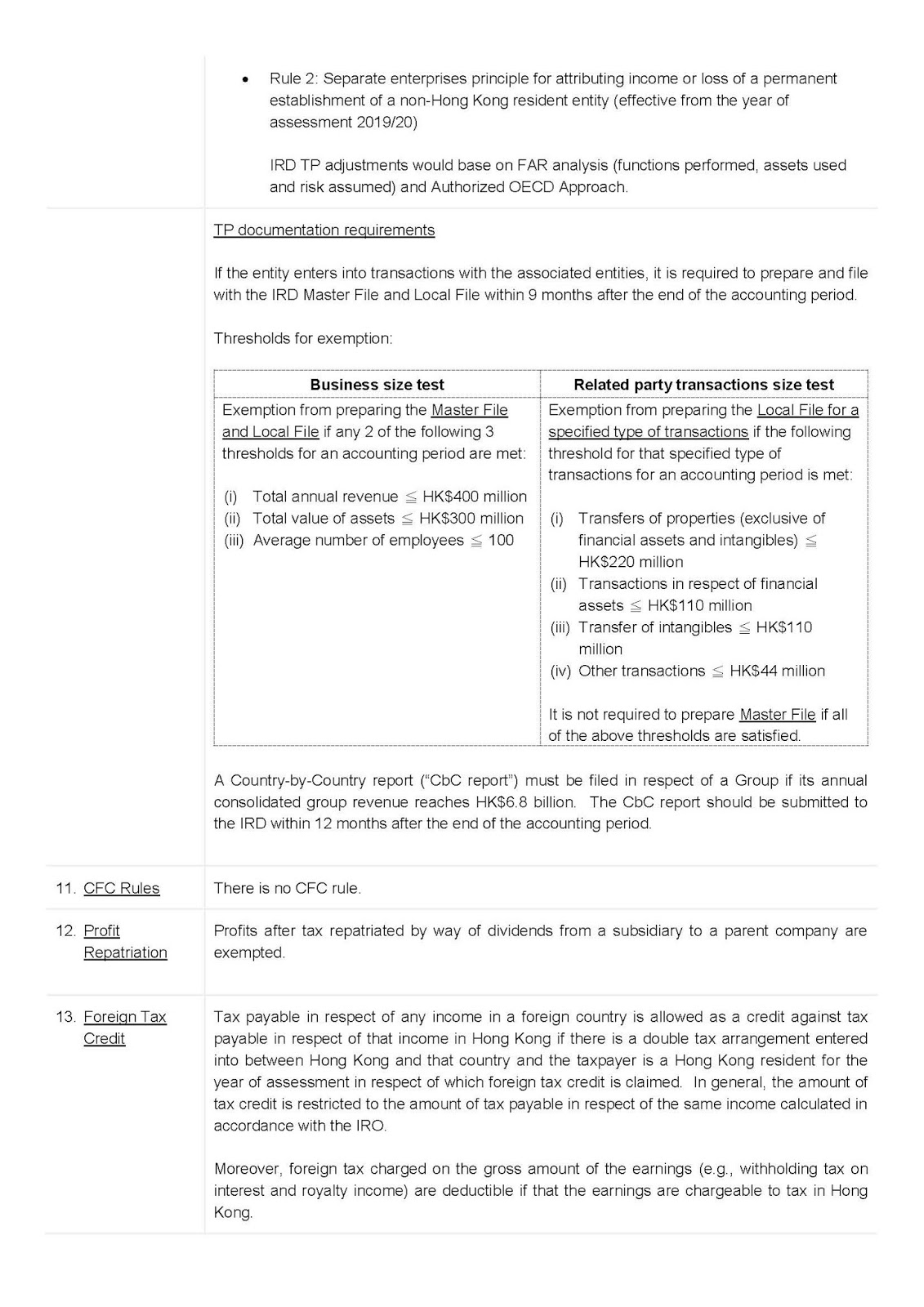

As a general rule, capital expenditures are not deductible. However, there are certain exceptions. For example, expenditure on research and development related to a taxpayer’s trade, profession or business is deductible provided that the expenditure is not on land or buildings, and that the payment is to an approved research institute for research and development related to that trade, profession or business or that the payment is to an approved research institute, the object of which is the undertaking of research and development relating to that particular class of trade, profession or business. To promote technological progress in local industries, the purchase of patent rights and rights to know-how are also deductible. In addition, payments for technical education and approved charitable donations may also be deducted from the assessable profits.

Depreciation is allowed for qualifying industrial and commercial buildings, and plant and machinery. For industrial buildings, a taxpayer who has incurred capital expenditure on the construction of an industrial building or structure is allowed a 20 per cent initial deduction of the capital expenditure. Thereafter, a 4 per cent deduction of the original capital expenditure is allowed annually.

A taxpayer with an interest in a commercial building or structure who has incurred construction costs can claim a deduction of 4 per cent annually. No depreciation deduction is available for commercial buildings that are more than 25 years old.

Capital expenditure on plant and machinery is allowed an initial deduction of 60 per cent in the year in which the expenditure is incurred. Thereafter, depending on the type of asset, depreciation is allowed on a reducing-value basis at 10, 20 or 30 per cent.

A super tax deduction scheme for research and development (R&D) expenditure was introduced on 2 November 2018. Under this new scheme, a 300 per cent tax deduction will be offered for the first HK$2 million of qualifying R&D expenditure and for expenditure in excess of HK$2 million, HK$6 million plus a 200 per cent tax deduction.

Capital and income

Hong Kong does not impose tax on capital gains. However, the issue as to whether income constitutes trading profits or non-taxable capital gains arises frequently in relation to the disposal of real property. Relevant factors include the frequency of the transactions, the accounting treatment adopted by the taxpayer, how long the property was held, how the property was financed and developed, and the reason for its sale. Profits obtained from properties acquired, developed and then sold are generally regarded as trading profits.

Losses

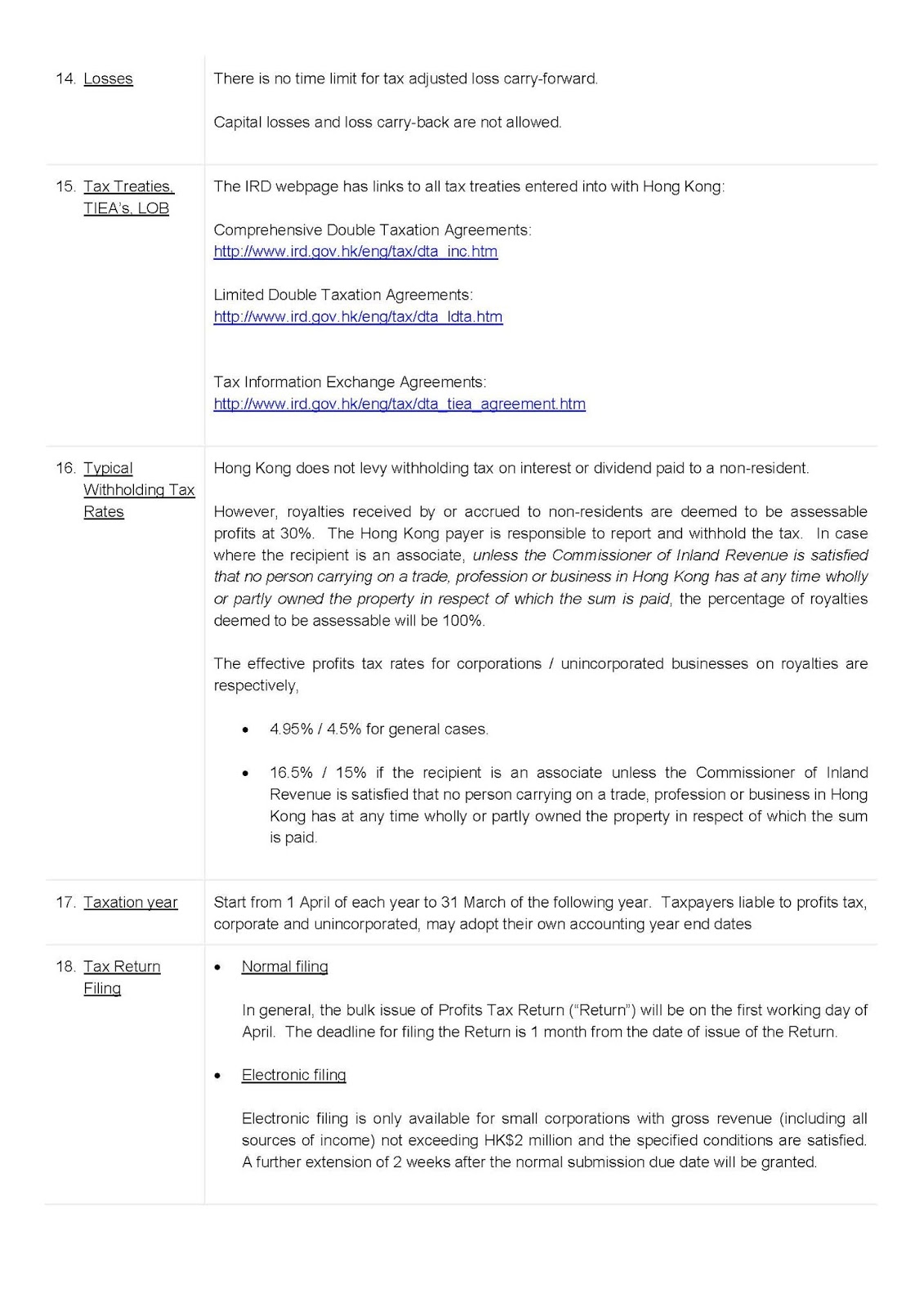

Hong Kong allows losses to be carried forward indefinitely.

Rates

The profits tax rate for companies is 8.25 per cent for the first HK$2 million of profits and 16.5 per cent for profits in excess of HK$2 million, subject to restrictions on connected entities discussed in Section II.i. If a company is a partner in a partnership, profits tax for its share of assessable profits is also charged according to the same two-tiered system of 8.25 per cent and 16.5 per cent. The rate for unincorporated businesses is 7.5 per cent for the first HK$2 million of profits and 15 per cent for profits in excess of that amount, subject to restrictions on connected entities as well.

Administration

A single tax authority – the IRD – exists in Hong Kong, and is responsible for administering the IRO.

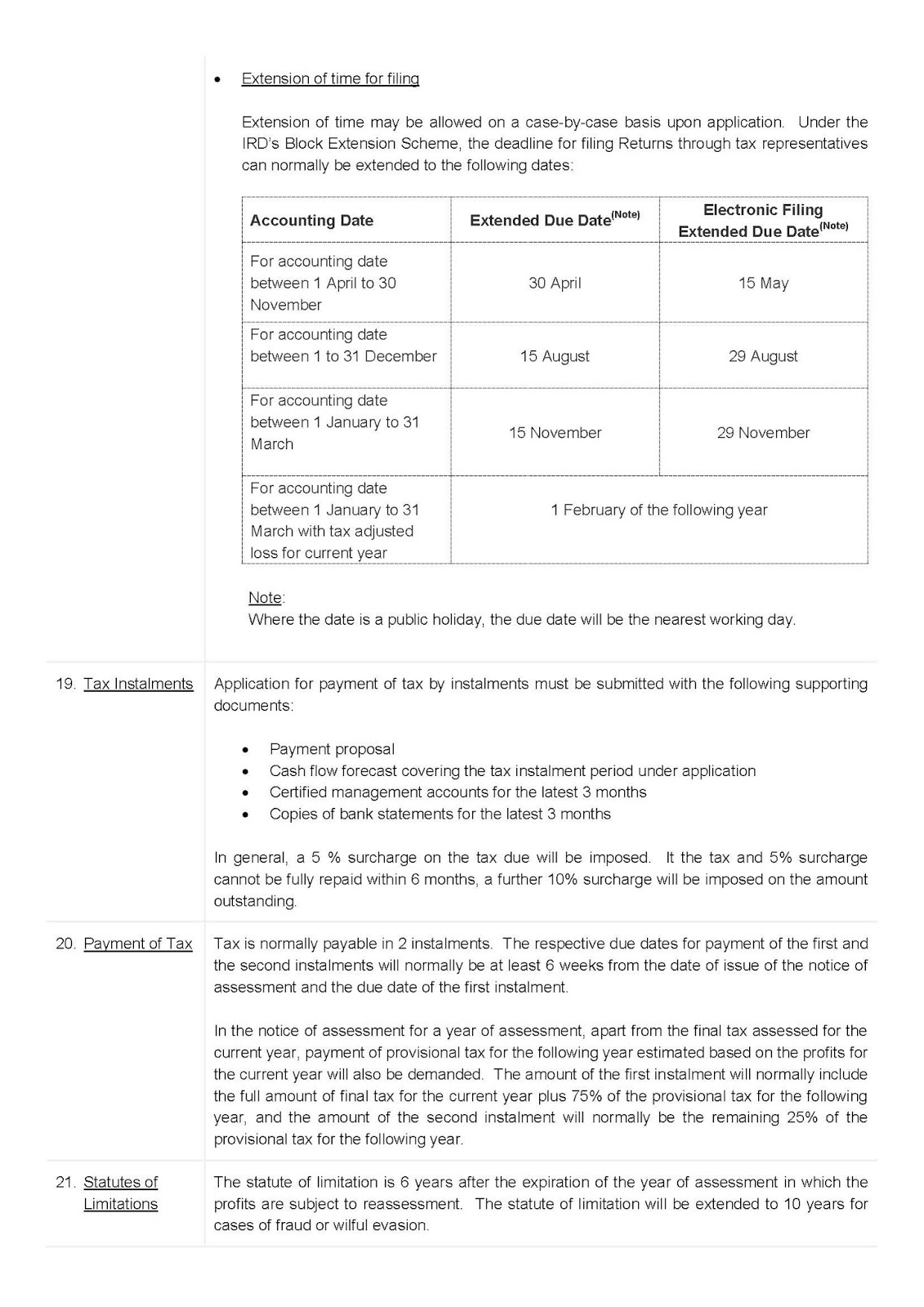

Tax is charged on the assessable profits for the year of assessment. The assessable profits for a business that makes up annual accounts are calculated on the profits of the year of account ending in the year of assessment. Generally, profits tax returns should be filed within one month of the date of issue. However, under the IRD’s Block Extension Scheme, this may be extended depending on the accounting date of the company. If a business objects to a tax assessment issued by the IRD, it has the right to file an objection within one month of the issuance of the assessment with the IRD, which will then render a determination that is subject to appeal to the IRD Board of Review as well as the Hong Kong courts.

Tax grouping

No group loss relief is available to companies that are members of a group in Hong Kong.

ii Other relevant taxes

Stamp duty

Hong Kong imposes stamp duty on instruments of transfer rather than the transaction itself. Instruments relating to the sale and lease of real property are subject to stamp duty, as are instruments relating to the sale of Hong Kong stock. Hong Kong stock is defined to include equity and debt instruments registered on a Hong Kong register. Therefore, if an offshore company maintains its share register in Hong Kong, any transfer of shares will be subject to stamp duty. Stock also includes units in unit trusts that maintain their registers in Hong Kong.

Hong Kong bearer instruments such as promissory notes and bills of exchange are also subject to stamp duty. However, owing to the range of exemptions applicable to these instruments, they are rarely subject to stamp duty in practice.

Should you require any assistance with your US Taxes, either in Hong Kong or Singapore, please don’t hesitate to get in touch.