Skip to content

Skip to content I. Introduction

Estate planning is a crucial aspect of financial planning that involves anticipating and arranging the management and disposal of an individual’s estate during their lifetime and after their death. It helps ensure that your assets are distributed according to your wishes and that your loved ones are cared for after you pass away.

A. Brief Overview of Trusts, Wills, and Foundations

Trusts, Wills, and Foundations are three common tools used in estate planning. To put it simply, a Will is a legal document that outlines how you want your assets to be distributed and your affairs handled after your death. A Trust is a fiduciary arrangement in which a grantor (also known as a trustor) gives a trustee the right to hold and manage assets for the benefit of a specific purpose or person. Foundations are legal arrangements that provide for the transfer of assets from their owner, called the grantor or trustor, to a council. They set the terms for the council’s management of the assets, distributions to one or more designated beneficiaries, and the ultimate disposition of the assets.

These tools offer different levels of control and flexibility in estate planning. Trusts can be revocable or irrevocable and offer advantages such as avoiding probate and ensuring privacy. Wills must go through the probate process but can cover a wide range of assets. Foundations can offer tax benefits, promote intergenerational philanthropy, and establish a structured approach to charitable giving.

B. Importance of estate planning

Estate planning holds a significant role in securing your financial future and the well-being of your loved ones. Without a clear plan in place, the fate of your assets and the ease with which they are transferred can be left to chance. This lack of direction may lead to unintended consequences, legal disputes, and unnecessary financial burdens on your family.

Trusts, Wills, and Foundations are not merely legal jargon; they are powerful tools that empower individuals to shape their legacy according to their desires. Each of these instruments serves as a pillar of support in estate planning, offering unique advantages tailored to specific circumstances.

Trusts go beyond just asset distribution. They provide an avenue for maintaining control over your assets while efficiently transferring them to your beneficiaries while avoiding probate complexities. The privacy that trusts afford also shields your estate’s details from public scrutiny.

Wills, on the other hand, represent a clear voice from beyond the grave. With a will, your instructions are etched in stone, ensuring your assets are distributed exactly as you intend. However, it’s essential to recognize that wills often come with the burden of probate, a process that can lengthen the distribution timeline and expose your affairs to the public eye.

Foundations provide a means of continuing your impact beyond your lifetime. By establishing a foundation, you create a lasting legacy through charitable and philanthropic endeavors that reflect your values. Beyond their altruistic nature, foundations can offer tax advantages and a structured approach to giving back.

In essence, estate planning through Trusts, Wills, and Foundations grants you the power to safeguard your family’s financial stability, respect your personal wishes, and contribute to meaningful causes. It is a thoughtful process that involves making informed decisions to ensure a seamless transition of your assets and the preservation of your values.

II. All about Trusts

A. What is a Trust

Trusts form the cornerstone of effective estate planning, offering a structured mechanism to manage and allocate assets as per the grantor’s intentions. A trust is a legally binding arrangement where one individual, known as the grantor or trustor, entrusts another person, referred to as the trustee, with the responsibility of holding and overseeing assets on behalf of designated beneficiaries. The essence of trusts lies in their ability to secure assets, streamline distribution, and even provide potential tax advantages.

The trust concept has existed since the 12th century. It is used for succession planning, allowing trusted professionals to administer wealth after the settlor’s lifetime (the person who transfers assets to the trust). Trusts can delay the time children become entitled to family wealth and provide protection from personal debts and other threats. There are various types of trusts, including those that pay income to one person during their lifetime or give trustees discretion to make decisions on paying out income and capital. Trusts can also provide tax savings depending on the laws of the settlor’s resident jurisdiction. Overall, trusts appeal for asset protection, succession, and estate planning.

Types of Trusts

The diversity of trust purposes is reflected in the various types available, each with its distinct advantages and considerations:

- Revocable Living Trust: Grantors maintain control over assets during their lifetime. Flexibility to modify or revoke the trust ensures adaptability to changing circumstances. These trusts bypass probate, enhancing the efficiency of asset distribution.

- Irrevocable Trust: Offering enhanced asset protection, these trusts cannot be altered or revoked without beneficiary consent. Estate tax reduction and creditor protection are common objectives.

- Special Needs Trust: Tailored for beneficiaries with special needs, these trusts ensure that financial support is provided without jeopardizing eligibility for government assistance programs.

- Asset Protection Trust: Designed to safeguard assets from potential creditors or legal claims, these trusts prioritize the preservation of the grantor’s wealth.

- Charitable Trust: Aligned with philanthropy, these trusts facilitate contributions to charitable causes while potentially providing tax incentives.

B. Advantages and Disadvantages of Trusts

- Advantages:

- Avoiding Probate: Assets held in a trust typically bypass the probate process, which can save time, money and maintain privacy.

- Asset Protection: Irrevocable trusts can shield assets from creditors and legal claims.

- Control: The grantor can specify how and when assets are distributed to beneficiaries.

- Privacy: Trusts are private documents, whereas wills are public records.

- Flexibility: Trusts can be tailored to fit specific needs and circumstances.

- Disadvantages:

- Complexity: Creating and managing a trust can be more complex than a will.

- Costs: Establishing a trust might involve higher upfront costs compared to a will.

- Irrevocability: Some trusts, once established, cannot be easily altered or revoked.

- Tax Reporting: Trusts have specific tax reporting requirements that must be adhered to.

C. Setting Up a Trust

The process of establishing a trust is methodical, involving several steps:

- Identify Objectives: Determine the goals of the trust, whether it’s asset protection, efficient distribution, or charitable endeavors.

- Select Trust Type: Choose the appropriate type of trust that aligns with your goals and circumstances.

- Choose a Trustee: Designate a trustee responsible for managing trust assets and adhering to your instructions.

- Draft the Trust Document: Collaborate with legal professionals to craft a detailed trust agreement outlining terms, beneficiaries, and conditions.

- Fund the Trust: Transfer assets into the trust’s ownership, ensuring the proper legal process is followed.

- Legal Formalities: Adhere to notarization and other legal requirements in accordance with jurisdictional laws.

It’s important to carefully consider each step and work with legal and financial professionals to ensure that the trust is set up properly and meets your needs and goals.

D. Tax Implications of Trusts

Trusts can have varying tax implications for both the grantor and the beneficiaries, and the specifics of taxation can differ depending on the type of trust. For example, beneficiaries typically pay taxes on the income they receive from a trust, while the principal amount is usually exempt from taxation.

Additionally, irrevocable trusts can also help minimize estate tax liability by removing assets from the grantor’s estate. It’s important to carefully consider the tax implications when setting up a trust and to consult with a tax professional to ensure that the trust is structured in a way that meets your needs and goals.

According to a new revenue ruling issued by the Internal Revenue Service, assets held in an irrevocable trust, when there has been a completed gift, do not receive a step-up in basis upon the death of the original owner. This ruling is likely to impact only highly wealthy clients, such as those who own a successful business, but the IRS’ ruling is still instructive for those engaging in more advanced estate planning. Trusts constructed in this way are often referred to as being “defective” for income tax purposes.

E. Structure of Trusts

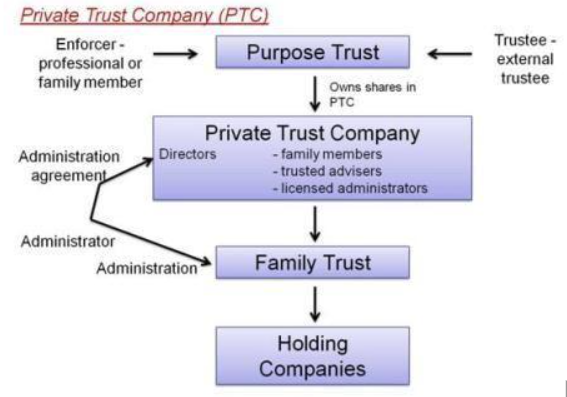

The diagram below illustrates the structure of a Private Trust Company (PTC). A PTC is a company that acts as a trustee for one or more family trusts. In this diagram, the PTC is owned by a Purpose Trust, which holds the shares in the PTC. The Purpose Trust is established to ensure that the PTC fulfills its intended purpose.

The PTC has a board of directors, which can include family members and trusted advisers. The PTC also has an administration agreement with an external administrator, who provides administrative services to the PTC.

The PTC acts as a trustee for one or more Family Trusts, which hold assets for the benefit of the family members. The Family Trusts can hold assets directly or through Holding Companies.

In summary, this diagram shows how a PTC can be structured to provide trustee services for one or more Family Trusts, with ownership and control of the PTC being held by a Purpose Trust and the Board of directors.

In summary, trusts epitomize structured legal arrangements designed to secure assets and ensure their distribution aligns with the grantor’s desires. The diverse array of trust types caters to a range of needs, spanning from wealth preservation to contributions to charitable endeavors. While establishing a trust may entail an investment of time and resources, the benefits extend to efficient asset management, potential tax advantages, and the realization of your legacy aspirations.

Subsequent chapters will delve into the worlds of wills and foundations, completing the trio of essential estate planning tools.

III. All About Wills

A will, also known as a last will and testament, is a crucial legal document that outlines an individual’s wishes for the distribution of their assets and other important matters after their death. This comprehensive guide covers the definition and purpose of wills, their advantages and disadvantages, the process of creating a will, and the tax implications that come with it.

A. What is a Will?

A will, often referred to as a last will and testament, is a legal document that outlines a person’s wishes for the distribution of their assets, property, and personal belongings after their death. The primary purpose of a will is to ensure that a person’s wishes are carried out effectively, providing clarity and legal direction to loved ones and beneficiaries. Wills also allow individuals to appoint guardians for minor children and name an executor who will be responsible for administering the estate.

B. Advantages and Disadvantages of Wills

- Advantages:

- Asset Allocation: Wills allow individuals to specify how their assets should be distributed and to whom.

- Exclusionary Control: Wills enable individuals to exclude certain parties from inheriting their assets.

- Guardianship Designation: Wills allow parents to appoint guardians for their minor children.

- Swift Access: Assets designated in a will are more easily accessible to beneficiaries.

- Tax Planning and Philanthropy: Wills enable strategic estate tax planning and facilitate charitable donations.

- Disadvantages:

- Postmortem Activation: Wills only take effect after death, so they cannot address scenarios that may arise during an individual’s lifetime or potential disabilities.

- Limited Lifetime Management: Wills do not provide mechanisms for managing assets during an individual’s lifetime.

- Probate and Privacy Concerns: The probate process can be time-consuming and expensive, and wills become public documents after death.

- Ineffectiveness in Specific Scenarios: Wills may not be effective in addressing inter-state planning or situations involving minors.

C. How to Create a Will:

To create a will, follow these steps:

- Gather Information: Collect information about your assets, debts, and beneficiaries. Choose an executor to manage your estate.

- Draft the Will: While templates and software are available, it is advisable to consult an attorney to ensure legal validity and clarity.

- Include Key Elements: A typical will includes identification of the testator (the person creating the will), a statement revoking any previous wills, specific bequests, the appointment of an executor, provisions for minor children, and distribution of the estate.

- Witnesses and Notarization: Most jurisdictions require two or three witnesses to sign the will for authenticity. Notarization may also be required.

- Review and Update: Regularly review and update your will to reflect changes such as births, deaths, marriages, or divorces.

D. Tax Implications of Wills:

- Estate Taxes: Depending on the jurisdiction, an estate tax (also known as an inheritance tax or death tax) may be imposed on the value of assets transferred from a deceased person to their beneficiaries. The tax rate and exemption threshold vary by location.

- Gift Taxes: In some regions, gifts made during an individual’s lifetime may be subject to gift taxes if they exceed a certain threshold. Lifetime gifts can also affect the estate’s value for estate tax purposes.

- Capital Gains Tax: Beneficiaries who inherit assets such as property or investments may be subject to capital gains tax when they sell or transfer these assets. The tax is based on the increase in value from the time the deceased acquired the asset.

- Generation-Skipping Transfer Tax: This tax applies when a person leaves assets to beneficiaries who are more than one generation younger than them. It aims to prevent wealthy individuals from avoiding estate taxes by directly transferring assets to grandchildren or great-grandchildren.

IV. All About Foundations

Foundations, a cornerstone of philanthropy and estate planning, are powerful legal entities established to promote charitable, educational, religious, scientific, or public benefit causes.

A. What is a Foundation?

Foundations are distinct legal entities that support a wide range of causes, such as charitable, educational, religious, and scientific endeavors. These entities are commonly initiated by individuals, families, or corporations and are typically overseen by a board of directors or trustees. The core objective of foundations is to offer financial backing to organizations or individuals that resonate with the foundation’s mission and objectives.

B. Types of Foundations

Foundations manifest in various forms, tailored to specific aims:

- Private Foundations: Established by individuals or families, these foundations often have a narrowly defined charitable focus. In the United States, private foundations are subject to a 1% or 2% excise or endowment tax on net investment income unless classified as a public charity.

- Community Foundations: These entities aggregate resources from multiple donors to support local charitable initiatives.

- Corporate Foundations: Created by companies, corporate foundations uphold charitable causes that align with their corporate values.

C. Advantages and Disadvantages of Foundations

Advantages

- Long-Term Impact: Foundations enable sustained financial support for charitable causes over time.

- Focused Giving: Foundations can concentrate on specific issues or areas requiring attention.

Disadvantages

- Financial Commitment: Foundations involve setup and maintenance costs, potentially impacting resources available for charitable purposes.

- Regulatory Complexity: Strict regulations and reporting requirements can be associated with foundation operation.

D. Setting Up a Foundation: A Step-by-Step Guide

- Incorporation: Establish the foundation as a legal entity, defining its structure.

- Governing Documents: Draft bylaws and articles of incorporation to guide foundation operation.

- Tax-Exempt Status: Attain government approval for tax-exempt status.

- Legal and Financial Consultation: Engage legal and financial professionals to ensure compliance with all legal requisites.

E. Tax Implications of Foundations

Private foundations have numerous interactions with the IRS during their existence. They are required to file an application for recognition of tax-exempt status, file required annual information returns, and make changes in their mission and purpose.

Private foundations are subject to several restrictions and requirements, including restrictions on self-dealing between private foundations and their substantial contributors and other disqualified persons.

Moreover, they are also required to annually distribute income for charitable purposes, have limits on their holdings in private businesses, and must ensure that investments do not jeopardize the carrying out of exempt purposes.

Additionally, they must assure that expenditures further exempt purposes. Violations of these provisions can result in taxes and penalties against the private foundation and, in some cases, its managers, its substantial contributors, and certain related persons.

There are several tax implications for private foundations:

- Donor Tax Deductions: Donations to foundations may yield tax deductions for donors.

- Tax-Exempt Status: Foundations may enjoy exemptions from certain taxes.

Investment Income Tax: Foundations might be subject to taxes on investment earnings and other revenue sources.

F. Notable Information

Until 1969, the term private foundation was not defined in the United States Internal Revenue Code. Since then, every U.S. charity that qualifies under Section 501(c)(3) of the Internal Revenue Service Code as tax-exempt is a “private foundation” unless it demonstrates to the IRS that it falls into another category, such as public charity. Unlike nonprofit corporations classified as public charities, private foundations in the United States are generally subject to a 1% or 2% excise tax or endowment tax on any net investment income.

G. Foundation Structure

A private foundation is typically set up as a nonprofit corporation that bears the name of its donors but may alternatively be established as a trust. Donors specify the charitable purpose of the foundation (for example, grants for cancer research, scholarships for the needy, and support of religious goals). During their lifetime, they may continue their charitable giving by making tax-deductible contributions to the foundation.

The foundation may also be funded with a bequest from the donors’ will or trust or receive funds as the primary or secondary beneficiary of a qualified plan or IRA. The IRS reports that there were 115,340 private foundations in the U.S.

in 2008, of which 110,099 were grantmaking (non-operating) and 5,241 were operating foundations—approximately 75% of the private foundations file annually with the IRS.

A private foundation is a charitable organization classified by the Internal Revenue Service (IRS) based on its funding and governance. There are three main types of private foundations: Family foundations, Private Operating foundations, and Corporate Foundations.

Family foundations are typically established by a family and funded through an endowment. The donor’s family members often serve on the foundation’s board and actively participate in its charitable grantmaking.

Private Operating foundations are a unique type of private foundation that uses the majority of its income to operate its own charitable programs or services. These foundations must meet certain requirements, such as passing an Assets test, Endowment test, or Support test.

Corporate foundations, also known as company-sponsored foundations, are established by companies to support charitable causes that align with their corporate values. These foundations are usually funded by contributions from the company and may also receive donations from employees and customers.

The US-based Foundation Center uses a more specific definition of private foundation which hinges in part on the existence of an endowment: a private foundation is a nongovernmental, nonprofit organization that has a principal fund managed by its own trustees or directors. Hopkins (2013) listed four characteristics that make up a private foundation, also including endowment as a condition for private foundations:

- It is a charitable organization and thus falls under the rules applicable to charities in general.

- Its financial support originates from one source, often an individual, family, or company.

- Its annual expenditures are financed from earnings from an endowment or investment assets rather than from a continuous flow of contributions.

- It awards grants to other organizations for charitable purposes, as opposed to its own programs.

In summary, foundations stand as formidable tools in fostering positive societal change. These legal entities cater to a diverse array of causes, with private, community, and corporate foundations, each offering unique value. While foundations present financial commitments and regulatory complexities, they hold the potential to make a lasting difference in the world.

Now that we have gained a comprehensive insight into estate planning let’s explore the dynamic interplay between trusts, wills, and foundations. Let us compare Trusts, Wills, and Foundations, noting key differences and similarities, including tax considerations.

V. Trusts vs. Wills vs Foundations

Trusts, Wills, and Foundations are three common ways of transferring assets to beneficiaries after death. However, they have different features, advantages, and disadvantages that should be carefully considered before making a decision.

Trusts are legal arrangements that allow a person (the settlor) to transfer property to another person (the trustee) who holds and manages it for the benefit of a third person (the beneficiary). Trusts can be revocable or irrevocable, meaning that the settlor can change or cancel the trust during their lifetime or not. Trusts can also be created during the settlor’s lifetime (inter vivos) or upon their death (testamentary).

Wills are legal documents that express a person’s wishes (the testator) regarding the distribution of their property after their death. Wills can be changed or revoked by the testator at any time before their death. Wills must comply with certain formalities, such as being signed and witnessed, to be valid. Wills can also appoint an executor who is responsible for carrying out the testator’s instructions and administering their estate.

Foundations are legal entities established by a person (the founder) to pursue a specific charitable, social, or educational purpose. Foundations are usually funded by an endowment from the founder or other donors. Foundations have a board of directors who oversee the foundation’s activities and assets. Foundations can also have beneficiaries who receive grants or services from the foundation.

A. Wills vs. Trusts

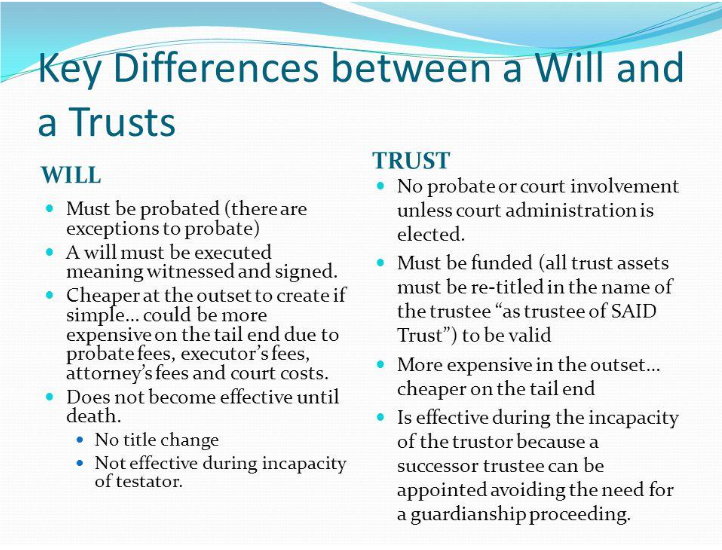

The two most common options are creating a Will or setting up a Trust. These are both legal documents that allow you to specify how your assets will be distributed after your death, The tables below provide an overview of their key differences, Table 1 explores their requirements, costs, effectiveness, and more, while Table 2 compares various aspects of these two legal documents, including when they become effective, who can create them, their effects on marriage, and more. By understanding these differences, you can make an informed decision about which option is best for your estate planning needs.

Table 1 Key Differences between a Will and a Trust

Table 2 Comparing Wills and Trusts: Key Aspects to Consider

| Feature | Wills | Trusts |

| When is the actual transfer of property? | After the testator dies and the will goes through probate | When the assets are transferred into the trust and managed by the trustee according to the terms of the trust |

| When does it become effective? | Only after the death of the testator | As soon as it is created, funded, and validly executed |

| Is there any Age requirement? | No, but some jurisdictions may have age requirements for serving as an executor or trustee | No, but some jurisdictions may have age requirements for serving as an executor or trustee |

| What is the effect of death of the testator/ settlor? | The will becomes effective and its instructions are carried out | Depends on the terms of the trust; some trusts may terminate upon the death of the settlor, while others may continue |

| Type of assets | all assets in the Estate | only those assets specified in the Trust Deed |

| Is any application to court necessary? | Yes, an application to court is necessary to probate a will | No, trusts generally do not require court involvement unless there is a dispute among the parties involved |

| Is there any effect on marriage? | Yes, in some jurisdictions marriage can revoke a pre-existing will | Yes, marriage can affect the terms of a trust if the trust includes provisions for the settlor’s spouse |

| What is required to be effective? | Must meet certain requirements such as being in writing, signed by the testator, and witnessed by two people (requirements vary by jurisdiction) | Must be created and funded (assuming it was validly executed). Witness not necessarily required |

| Can there be more than one? | Yes, a person can have multiple wills (but only one will be valid at a time, usually the latest one) | Yes, a person can create multiple trusts |

| Can it be revoked by the person who made it? | Yes, a will can be revoked by the testator at any time before their death | Yes, a revocable trust can be revoked by the settlor at any time. However, an irrevocable trust generally cannot be revoked once it has been created |

| Creditor Proof | No, assets distributed through a will are subject to creditor claims | Yes, assets placed in an irrevocable trust are generally protected from creditors because they are no longer owned by the settlor |

| Type of document | Will | Trust Deed |

B. Foundations vs Trusts

When it comes to charitable giving, there are several options available, including gift trust accounts and private foundations. Gift trust accounts were originally created to provide flexibility for charitable contributors who were not ultra-wealthy. Nowadays, large firms offer gift trust accounts as a supplement to a private foundation strategy. While gift trust accounts do provide the same benefits in terms of gifting and tax deductions, there are certain advantages that private foundations offer that gift trust accounts do not.

One advantage of private foundations is the ability to name the entity after the founder or their family. This allows wealthy clients to connect their family name and values to a charitable entity that will last in perpetuity. In contrast, the gift trust of a large mutual fund family is unlikely to change its name to accommodate individual clients.

Another advantage of private foundations is the ability to appoint the board of directors and leadership for the entity. This allows clients to ensure that their values are instilled in future generations by involving them in the management of the foundation. For example, some may be concerned that their wealth will cause their descendants to become unmotivated trust-fund babies. Involving them in the management of the foundation can help instill their values and work ethic in their offspring and grandchildren.

It’s important to note that private foundations are subject to increased government scrutiny. IRS audits are on the rise, and those who use their private foundations to provide personal benefits to friends and family members are under closer scrutiny than ever before. While legitimate reasons may exist for a private foundation to have salaries and other operating expenses, these expenses must be reasonable if audited at the private foundation level.

C. Key differences and similarities between Trusts, Wills, and Foundations

Further, the table below illustrates the key differences and similarities between Trusts, Wills, and Foundations pertaining to Probate Avoidance, Privacy, and Security, Flexibility and Control, as well as Tax Implications.

Table 3. Summary of Key Differences and Commonalities of Trusts, Wills, and Foundations

| Feature | Trusts | Wills | Foundations |

| Probate | Can avoid probate | Must go through probate unless the estate is very small or passes by other means | Can avoid probate |

| Flexibility and Control | Can provide more flexibility and control over the distribution of assets | Can provide more flexibility and control over the distribution of assets | Must adhere to their stated purpose and follow certain rules and regulations regarding their operations and distributions |

| Privacy and Protection | Can provide more privacy and protection than Wills | Public record, can be accessed by anyone after probate | Can provide more privacy and protection than Wills |

| Tax Implications | Subject to estate tax, may be subject to generation-skipping transfer tax | Subject to estate tax, may be subject to inheritance tax | Exempt from estate tax but subject to income tax on their earnings and excise tax on their net investment income, may be eligible for charitable deductions or credits for their donations or grants. |

D. Choosing Between Trusts, Foundations, and Wills:

(Factors to Consider)

Trusts, Wills, and Foundations each have their own unique advantages and disadvantages, and it’s important to carefully consider these before making a decision. When choosing between these options, some key factors to consider include:

- Estate Size and Complexity: The size and complexity of your estate can influence which option is best for you. For example, larger and more complex estates may benefit from the flexibility and control offered by Trusts or Foundations.

- Beneficiaries or Recipients: The number and identity of your beneficiaries or recipients can also play a role in your decision. For example, if you have multiple beneficiaries with different needs, a Trust may provide more flexibility in distributing assets.

- Purpose and Duration: The purpose and duration of your transfers can also influence your decision. For example, if you want to provide for your beneficiaries over a long period of time, a Trust may be a better option than a Will.

- Privacy and Protection: The level of privacy and protection you desire can also be a factor to consider. Trusts and Foundations can provide more privacy and protection than Wills, as they are not public records.

- Cost and Ease: The cost and ease of creation and administration can also be important considerations. While Wills may be cheaper to create initially, they can be more expensive to execute due to probate fees, executor’s fees, attorney’s fees, and court costs.

- Tax Consequences: The tax consequences for you and your beneficiaries or recipients should also be taken into account. Trusts, Wills, and Foundations have different tax implications that depend on various factors.

VI. CONCLUSION

Trusts, Wills, and Foundations are all important tools for estate planning, each with its own unique advantages and disadvantages. Trusts offer flexibility and control over the distribution of assets, while Wills provide a straightforward way to express your wishes regarding the distribution of your property after your death. On the other hand, foundations allow you to establish a charitable entity to pursue a specific purpose.

When choosing between these options, it’s important to carefully consider factors such as your purpose, the size and complexity of your estate, the number and identity of your beneficiaries or recipients, the purpose and duration of your transfers, the level of privacy and protection you desire, the cost and ease of creation and administration, and the tax consequences for you and your beneficiaries or recipients.

Given the complexity of estate planning, it’s always a good idea to seek professional advice when making decisions about Trusts, Wills, Foundations, and other estate planning tools. A qualified attorney, tax expert, or financial advisor can help you understand the pros and cons of each option and guide you in making the best decisions depending on your unique situation. This is especially important when it comes to tax planning, as the tax implications of Trusts, Wills, and Foundations can be complex.

In summary, Trusts, Wills, and Foundations are all valuable tools for estate planning. By understanding the key differences between these options and carefully considering your own needs and goals, you can make informed decisions about how to best protect your assets and provide for your loved ones after your death. And remember: seeking professional advice is always a good idea when it comes to estate planning.

A. Key Takeaways:

Tailored Solutions: Professional advisors possess the knowledge to customize trusts, wills, or foundations to suit unique family dynamics, assets, and philanthropic aspirations. This personalization ensures that your wishes are accurately represented and executed.

Mitigating Risks: With their comprehensive understanding of legal and financial intricacies, professionals can identify potential pitfalls and risks associated with each option. This awareness helps in safeguarding your assets and avoiding complications down the line.

Tax Efficiency: Tax implications play a significant role in estate planning. Professionals have the expertise to structure trusts, wills, or foundations in ways that maximize tax benefits, potentially saving heirs a significant amount of money.

Compliance and Regulation: Estate planning involves navigating a complex web of legal regulations and compliance requirements. Professionals ensure that your arrangements adhere to the latest laws and regulations, avoiding legal disputes in the future.

B. The Importance of Seeking Professional Advice:

Estate planning decisions are not merely about transferring assets; they are about securing the legacy you wish to leave behind. Mistakes made in haste or without expert guidance can lead to unintended consequences and potential family disputes. Professionals offer the expertise needed to interpret nuanced legal language, assess financial implications, and navigate intricate tax codes.

While the allure of DIY solutions or generic templates might seem appealing, the risks far outweigh the benefits. A single misstep could have lasting repercussions for your loved ones and beneficiaries. By engaging a team of professionals, including estate attorneys, financial advisors, and tax experts, you equip yourself with the tools necessary to make informed decisions that align with your goals.

The peace of mind that comes from knowing your estate affairs are in capable hands is immeasurable. Your legacy deserves the attention to detail and comprehensive planning that only professionals can provide. Embrace the expertise at your disposal to craft a legacy that endures through generations while minimizing the burdens your heirs might face.