Skip to content

Skip to content

Overview

Principal legislation

The principal transfer pricing legislation is:

- the Indonesian Income Tax Law No. 7 of 1983, as last amended by Income Tax Law No. 36 of 2008 (ITL);

- Government Regulation No. 74 of 2011 concerning Procedures for Implementing Rights and Obligations of Taxation Liability;

- the Director General of Taxes Regulation No. PER-43/PJ/2010 (PER-43) as last amended by PER-32/PJ/2011 concerning the Application of the Arm’s-length Principle in Transactions Between Taxpayers and Related Parties (PER-32);

- the Director General of Taxes Regulation No. PER-22/PJ/2013 concerning the Guidelines for Examination of Taxpayers with Related Parties (PER-22);

- the Minister of Finance Regulation No. 240/PMK.03/2014 concerning Procedures for Implementation of the Mutual Agreement Procedures (PMK-240);

- the Minister of Finance Regulation No. 07/PMK.03/2015 regarding Procedure for Establishment and Implementation of an Advance Pricing Agreement (PMK-07); and

- the Minister of Finance Regulation No. 213/o3/2016 concerning Types of Documents and/or Additional Information that Must be retained by a Taxpayer who is conducting Transactions with Parties that Having a Special Relationship, and Procedure to Manage it (PMK-213); and

- the Director General of Taxes Regulation No. PER-29/PJ/2017 concerning the Management Procedure of Country by Country Reporting (PER-29).

Enforcement agency

Transfer pricing rules are enforced by the Directorate General of Taxes (DGT) that under the Ministry of Finance of the Republic of Indonesia.

OECD guidelines

As reference for formulating Indonesian transfer pricing policy and regulation and for dispute settlement.

Covered transactions

Transfer pricing rules apply for any type transactions if the following conditions are met:

- a ‘provision’ has been entered in to by two persons through a transaction or series of transactions;

- the ‘special relationship condition’ is satisfied; and

- the commercial or financial relations differs from the arm’s-length provision that would have been made between independent enterprises.

A special relationship between taxpayers may result from the dependency or the relationship of the following condition between those parties:

- an ownership or share of equity; and

- participation in management or technology.

In addition, related parties between individual taxpayers may also result from their relationship by blood or by marriage.

As defined in article 18 (4) Indonesian Income Tax Law and its elucidation, the special relationship is deemed to exist if:

- the taxpayer owns capital participation directly or indirectly of at least 25 per cent of another taxpayer, the relationship between taxpayers through ownership is at least 25 per cent of two or more taxpayers, or a relationship between two or more taxpayers mentioned later;

- a taxpayer who controls other taxpayer; or two or more taxpayers are directly or indirectly under the same control; or

- a family relationship either through blood or through marriage within one degree of direct or indirect lineage.

Furthermore, the elucidation of article 18(4)(b) provides the more guidance, as follows.

A special relationship between taxpayers may also result from a participation in management or technology even though there is no ownership. A special relationship is deemed to exist if one or more enterprises are controlled by the same persons, or the relationship between enterprises is controlled by the same person.

The term ‘relationship by blood in one degree of direct lineage vertically’ means parents, and son or daughter. The term ‘relationship by blood in one degree of direct lineage horizontally’ means relatives. The term ‘relationship by marriage in one degree of direct lineage vertically’ means parents-in-law, and a stepson or stepdaughter. The term ‘relationship by marriage in one degree of direct lineage horizontally’ means relatives-in-law.

Transfer pricing rules should be applied for domestic and cross-border transactions between related parties.

Arm’s-length principle

Yes. The DGT adheres to the arm’s-length principle as enshrined in article 9 of the OECD Model Treaty in applying the transfer pricing legislation.

Base erosion and profit shifting

Indonesia follows the guidance provided in the OECD Transfer Pricing Guidelines 2010 version. Indonesia is now in the process of finalising the finance ministry regulation to adopt the OECD’s recommendation in BEPS 8-10. The BEPS Action 13 recommendation has been fully adopted in the local transfer pricing rules with PMK 213/PMK.03/2016.

Pricing methods

Accepted methods

The DGT adopts the most appropriate method. The DGT accepts all OECD transfer pricing methods. However, if a traditional transaction method and a transactional profit method can be applied in an equally reliable manner, the traditional transaction method is preferable to the transactional profit method. Moreover, where the comparable uncontrolled price method (CUP) and another transfer pricing method can be applied in an equally reliable manner, the CUP method is preferred.

If a reliable CUP cannot be found, then, in line with the Guidelines, the DGT places emphasis on choosing the most appropriate method for the particular type of transaction, rather than establishing a rigid hierarchy of methods. For tangible or intangible property transactions, the DGT accepts the following five methods:

- the CUP method;

- the resale price method;

- the cost-plus (CP) method;

- the profit split method; and

- the transactional net margin method.

Other methods, such as valuation techniques using income-based approach, cost-based or market-based approach also accepted by the DGT as transfer pricing method for intangible property transactions.

For intragroup services transactions, the DGT has accepted the following three methods: the CUP, CP and transactional profit methods.

The Indonesian TP regulation also provides detailed guidelines on assessing the arm’s-length nature of intragroup services (IGS) and intangible property (IP) transactions. Rigorous tests must be applied in a hierarchical manner to prove the arm’s-length nature of IGS and IP transactions.

For loan transactions the DGT only accepts the CUP method. Current transfer pricing regulation does not contain specific mention of a method to be used for commodity. However, in current regulation regarding transfer pricing documentation the DGT encourages the use of CUP for commodities.

Following BEPS, the DGT has noticed an increasing acceptance of and reliance on profit split methods.

Cost-sharing

Cost-sharing arrangements are permitted in Indonesia. A cost-sharing arrangement is a framework agreed among business entities to share the costs, risks of developing, providing or obtaining assets, services, or rights and determine the nature and extent of the interests of each participant in those assets, services or rights. However, any detailed explanations on how it can be applied are not clearly stated and ruled out in Indonesian transfer pricing regulation. Indonesia follows the guidance provided in the OECD Transfer Pricing Guidelines 2017.

Best method

There is no strict hierarchy of methods; rather, the DGT follows the Guidelines’ ‘natural hierarchy’. Generally, the CUP method is preferred and in practice the DGT expects sufficient effort to be made to identify a suitable CUP. If both traditional transaction methods and transactional profit methods can be applied with equal reliability, the preference is for traditional transaction methods.

If a reliable CUP cannot be found, then, in line with the Guidelines, the DGT places emphasis on choosing the most appropriate method for the particular type of transaction.

The selection of the most appropriate method requires the following considerations:

- the strength and weakness of each transfer pricing method;

- the appropriateness of the method based on the nature of the related-party transaction, determined by a functional analysis;

- availability of valid information (on independent transactions) to apply the selected method; and

- the comparability level between related-party transactions with independent transactions, including whether any appropriate adjustments would need to be made to eliminate any material differences between the compared transactions or enterprises.

For more complex transactions, the DGT is open to exploring other methods if they are considered to provide a stronger case for application of the arm’s-length principle.

Taxpayer-initiated adjustments

Taxpayers are allowed to make year-end adjustments based on a self-assessment system (eg, as a year-end true-up or true-down) as long as they comply with the arm’s-length standard and are made before the tax audit notification letter is issued and received by the taxpayer.

Safe harbours

There are no safe harbour methods available in the current Indonesian Transfer Pricing regulation.

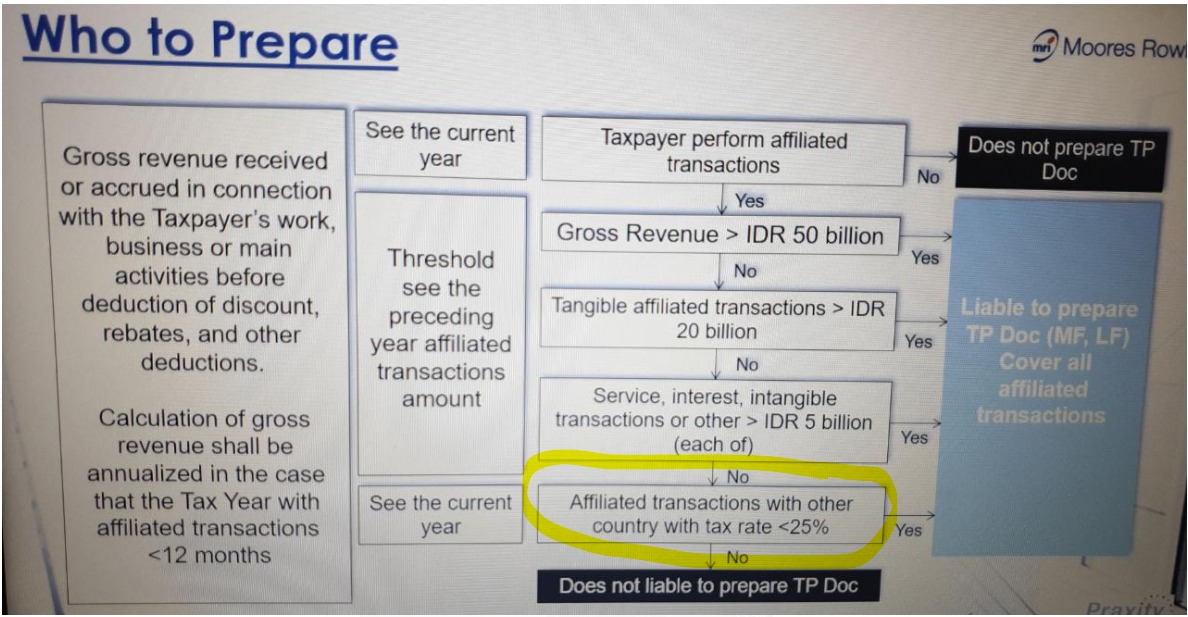

Disclosures and documentation

The DGT requires a separate master file and local file. As regulated in PMK 213, the minimum contents of the master file and local file are as follows.

Master file

- Structure and chart of ownership and countries or jurisdictions of each member of the group;

- business activities performed by the group;

- intangible assets owned by the group;

- financial and financing activities performed by the group; and

- parent entity’s consolidated financial statements and tax information of related-party transactions.

Local file

- Business identity and activities of the taxpayer;

- related-party and independent transaction information;

- determination of the arm’s-length principle;

- the taxpayer’s financial information; and

- non-financial events or facts affecting the formation of price or profit level.

The master file and local file must be prepared in Bahasa Indonesia.

Other than complying with mandatory documentation requirements, the main benefit of preparing and keeping proper transfer pricing documentation is that it would assist in resolving any future transfer pricing enquiries by the DGT and in general helps the taxpayer to achieve and maintain a lower transfer pricing risk rating with the DGT.

Indonesia operates on a self-assessment system, with companies setting their own transfer prices. The taxpayer should have documentation to prove that the transfer price of related parties’ transaction has been set at arm’s length on an ex-ante basis. In a tax audit context, having this documentation will shift the burden of proof to the DGT. If a taxpayer does not have documentation to support its transfer pricing policy, there is a high risk that the Indonesian Tax Office will make substantial adjustments during the tax audit, such as the denial of all deductions for management services fees or royalties paid to related parties.

Maintaining good transfer pricing documentation helps to demonstrate that the taxpayer has taken reasonable care in making any transfer pricing adjustments to its tax return, were this to be inquired into in future.

Country-by-country reporting

The DGT adopts country-by-country reporting as guided by OECD BEPS Action 13 Deliverables in the local rules. There is no difference between the local country-by-country reporting rules and the consensus framework of BEPS Action 13.

Timing of documentation

The master file and local file should be available four months after each fiscal year-end, in either Bahasa Indonesia or English (for taxpayers with approval to maintain bookkeeping in English, but it must be accompanied by a Bahasa Indonesia translation). The CBCR should be available 12 months after fiscal year end. The taxpayer should submit the transfer pricing documentation upon DGT’s request. The CBCR submission is due within one year after each fiscal year-end and together with the submission of subsequent year’s tax return and the notification of CBCR electronically, at the latest, 12 months after the fiscal year ends. The DGT can request the documents for compliance checking, a tax audit, an objection, a reduction of an administrative sanction and in other cases. In the next regulation, taxpayer should submit the transfer pricing documentation contemporaneously with the filing of the corporation tax return.

Failure to document

A taxpayer has four months (12 months for CBCR) after each financial year-end to prepare and declare, starting in its 2016 corporate tax return, that it is ready to submit the MF/LF. The MF/LF must be summarised in an attachment to the annual corporate income tax return (CITR) and the CBCR attached to the tax return of the following year.

Penalties exist for failing to prepare and submit the MF/LF upon request. Failure to prepare MF/LF is treated as not applying the arm’s-length principle. Failure to deliver an MF/LF when requested would result in the taxpayer being deemed as not having transfer pricing documentation.

Adjustments and settlement

Limitation period for authority review

Articles 15 and 16 Minister of Finance Regulation No.17/PMK.03/2013 last amended by PMK-184/PMK.03/2015 concerning ‘Tax Audit Procedures’, regulate the time line of a tax audit. In the field tax audit process, the examination phase should be done within six months and can be extended for two more months and the discussion phase should be completed within two months. Furthermore, for taxpayers with transfer pricing issues or financial engineering issues, an extension can be granted of three times for six months each.

Rules and standards

There are two transfer pricing audit guidance documents that govern the Indonesian Tax Authority in reviewing company compliance with transfer pricing rules:

- Directorate General of Taxation Regulation No. PER-22/PJ/2013, which provides tax audit procedures and guidelines for taxpayers with related party transactions; and

- Directorate General of Taxation Circular Letter No.SE-50/PJ/2013, which provides technical guidelines on transfer pricing audits. This circular letter aims to standardise the approach and nature of documents to be reviewed by tax auditors during the transfer pricing audit process.

The Indonesian tax system adopts a self-assessment system in which the burden of proof is on the taxpayer. In this regard, the taxpayer needs to prove that the argument to determine the price and its method is consistent with the arm’s-length principle. If the taxpayer cannot provide the required documentation, a substantial adjustment will be imposed, based on market prices, by the DGT.

Disputing adjustments

If the taxpayer does not agree with the transfer pricing adjustment applied by DGT, the dispute should be solved through objection and appeal process. The taxpayer may seek judicial review of a transfer pricing adjustment in the Supreme Court if the taxpayer disagrees with the tax court’s decision. The taxpayer may also resort to an alternative dispute resolution (ADR) mechanism using MAP (mutual agreement procedure). A MAP application can be made simultaneously with the objection application to the DGT. Advance pricing agreement (APA) also available to a taxpayer that needs to prevent transfer pricing disputes through a unilateral APA or bilateral APA.

Relief from double taxation

Indonesia has concluded tax treaties with more than 60 countries and jurisdictions covering its major trading partners in the Association of Southeast Asian Nations (ASEAN), America, Europe and much of the Asia-Pacific region. All of those tax treaties have MAP provisions.

Requesting relief

PMK-240 is the published MAP guidelines. A MAP application may be submitted by a taxpayer through the DGT or the tax competent authority of a tax treaty partner country or jurisdiction. As stated in PMK-240, an Indonesian taxpayer shall submit a request for a MAP to the Directorate of Regulation II of the DGT within the time limit stipulated in the relevant tax treaty. The request for a MAP shall provide certain information or explanations regarding, among others, the following matters:

- the taxpayer’s identity;

- the identity of the related foreign taxpayers involved including certificate of domicile or certificate of resident;

- the fiscal year concerned;

- actions taken by a resident taxpayer or the tax authority of a tax treaty partner country, which are considered not in accordance with the tax treaty provisions;

- a description of transactions to which the tax authority of the tax treaty partner country has made an adjustment, including the substance of the transaction, the amount and basis of the adjustment; and

- the taxpayer’s opinion on the adjustment made by the tax authority of the tax treaty partner country.

The taxpayer must submit the certificate of domicile of the relevant foreign taxpayer from the tax treaty partner country or jurisdiction in the MAP request.

When relief is available

A request for a MAP should be completed with the supporting documents and submitted to the DGT within a time limit as stipulated in the relevant tax treaty by:

- a taxpayer through the DGT;

- the DGT; or

- the tax authority of the treaty country or jurisdictions.

For a MAP application initiated by the Indonesian taxpayer, the time limit to lodge an MAP application is the first notification of any action that triggers a tax assessment not in accordance with the relevant tax treaty.

As for the MAP application made by DGT or a tax authority of the tax authority of the country or jurisdiction, PMK 240 states that the starting points for counting the time limit for a MAP application that is stipulated under a tax treaty can be:

- the date of the tax assessment letters;

- the date of the withholding tax slips; or

- the times stipulated by the DGT.

The MAP application cannot be lodged when the tax court has declared an end of the court hearing process, regardless of the outcome of the Tax Appeal. MAP will cease when the Tax Court announces its decision. Furthermore, consultation with the treaty partner’s tax authority should ideally be concluded within three years of initiating MAP. However, the timeline may be extended after an agreement between two competent tax authorities.

Limits on relief

Yes, there are. The DGT only gives a response to the corresponding adjustment conducted by the tax treaty partner country.

Success rate

Currently, there are no statistics published on MAP case resolution by the DGT. The DGT do not published MAP agreement publicly, only the corresponding taxpayers could gather the information regarding the mutual agreement reached. However, based on information on Indonesian dispute statistics on the OECD website (www.oecd.org/tax/dispute/mutual-agreement-procedure-statistics-2016-per-country-all.htm), the average times needed to close MAP by the DGT are 39.98 months for transfer pricing cases and 27.9 months for non-transfer pricing cases. Details on MAP outcomes can be accessed via that link.

Advance pricing agreements

Availability

Indonesia has an APA programme consisting of unilateral and bilateral APAs (BAPAs). Indonesia basically does not have a multilateral APA programme. However, if the covered transactions and covered entities are from more than two countries, the APA can be conducted by applying multiple BAPAs with the countries concerned. The DGT is open and is willing to optimise APAs as a means to prevent double taxation and BEPS. This can be seen from the significant increase in the number of APAs completed in 2018. The statistics for APAs requested and closed can be found at www.pajak.go.id/id/apa-map.

Process

PMK 7 sets out the process or procedures to obtain an APA into the following two broad stages.

Establishment of the APA:

- submission of the preliminary discussion requests by taxpayer;

- preliminary discussions between the taxpayer and the DGT;

- invitation for an APA application request based on preliminary discussions;

- submission of the APA application by the taxpayer;

- formation of the APA team by the DGT;

- analysis, evaluation and discussions of the APA application by the APA team and taxpayer;

- drafting and finalisation of the APA document; and

- formal completion of the APA document and issuance of a decree by the DGT.

The second is the implementation stage including the evaluation of the APA through an annual compliance report and the potential to submit a new APA application for the subsequent year. This stage is relevant both for unilateral APAs (UAPAs) and BAPAs. There is no filing fee for APAs.

Time frame

Generally, the entire process of applying for a unilateral APA until it is completed may require six to 18 months, whereas an application for a bilateral APA may require three years, as stipulated in the tax treaties between Indonesia and the tax treaty partner country.

Duration

According to PMK-7, a unilateral APA will be valid for a maximum of three years. However, in relation to bilateral APAs, the validity period can be extended to a maximum of four years. Rollback facilities are available for bilateral APAs, and the DGT is currently in the process of revising the APA regulation to allow rollbacks for unilateral APAs.

Scope

All types of related-party transactions can be covered by APAs, inclu-ding tangible and intangible property transfers, related-party services, cost-sharing arrangements and financial transactions covering guarantees and the allocation of income of a financial institution engaged in the global trading of financial instruments.

Independence

Yes, the APA programme is independent from the tax authority’s examination function and from the competent authority staff handling other double taxation cases. All of the taxpayer’s documents will be returned to the taxpayer if the taxpayer’s APA application is not approved by the DGT or cancelled. No documentation during the APA process can be used by the DGT for tax audit and tax investigation purposes. Prior to 2016, MAP cases were handled by the Directorate of Tax Regulation II in the DGT. In 2016, a new International Tax Directorate was established and took over this role and responsibility.

Advantages and disadvantages

The key advantages of APAs are minimising transfer pricing disputes, providing legal certainty and ease of tax calculation.

The advantages of an APA can include:

- reducing the uncertainty and enhanced predictability arising from related-party transactions conducted in the future;

- providing certainty concerning the transfer pricing method to be applied to particular transactions;

- lowering the ongoing compliance costs and reporting requirements once the APA has been agreed;

- reducing the risk of double taxation, especially in the case of BAPAs;

- avoiding costly and time-consuming litigation or examinations;

- a better understanding of the business on the part of the DGT; and

- the opportunity to establish or improve relationship with the DGT in a non-adversarial environment.

The disadvantages of an APA can include:

- external professional fees;

- close scrutiny of a transaction by the DGT;

- significant time of key executives;

- no guarantee that the tax authorities will agree terms that are acceptable to the taxpayer; and

- a large amount of information must be volunteered to the DGT.

It should be noted that there is no guarantee that an APA application will be approved by the DGT.

There are some factors that cause difficulties in reaching agreement about APAs with the DGT:

- lack of transparency from taxpayers;

- a subsidiary company in Indonesia does not have the authority to make decisions independently;

- lack of flexibility in negotiation in some issues in APA applications, such as the most appropriate transfer pricing method that is in line with the facts and circumstances surrounding the transactions proposed in the APA; and

- the taxpayer proposes an APA result that is lower than the actual or current performance.

Special topics

Recharacterisation

Under article 18(3) of the ITL, the DGT may challenge the form of related-party transactions as structured by the taxpayer. The DGT is authorised to determine the amount of income and expenses, and determine or recharacterise the debt as capital to calculate the amount of taxable income for taxpayers having a special relationship with the other taxpayer in accordance with the arm’s-length principle. Generally, the DGT may execute its authority to adjust and recharacterise the related-party transactions if those transactions are considered as not complying with the arm’s-length principle.

Selecting comparables

Indonesian transfer pricing guidelines do not specifically mention that local comparable companies are preferable, but in practice the local comparable is preferred. However, owing to lack of local comparable company database from Indonesia, the DGT has no objection to using a set of comparable companies from the Asia-Pacific region. The DGT uses some parameter screening criteria, statistical screening, manual review and website review for selecting and evaluating comparable companies. The purpose of this search process is to find companies that have the highest degree of comparability in business function, assets, risks and products with the taxpayer. The detail of the comparable company’s search process should be attached to the transfer pricing documentation.

Secret comparables

In existing regulation, there is no restriction on using secret comparables. However, so far the DGT have not yet made use of any secret comparables in auditing or litigation.

Secondary adjustments

The primary adjustment performed by the tax auditor may result in a secondary adjustment. The secondary adjustment is a further correction that may occur owing to the primary adjustment on related-party transactions. If a tax auditor makes a positive correction on related-party transactions and the result of the correction is an overpayment to the related party, the tax auditor may make a secondary adjustment for such overpayment applied under applicable taxation provisions (eg, withholding tax on deemed dividends).

There is also a possibility that equity is stated as debt, namely disguised equity. In such case, the DGT is authorised to characterise debt as equity. This recharacterisation may be made by comparing the ratio of the company’s liabilities to the company’s equity of independent parties or based on other data. As a result, interest paid with respect to that debt is not deductible, and in the hands of shareholders such payment is considered as a dividend that is subject to tax.

To obtain relief from the adverse tax consequences of certain secondary adjustments, the taxpayer should be able to prove that all of its related-party transactions have been conducted in accordance with arm’s-length principles. Having an APA with the DGT may exempt the taxpayer from this transfer pricing adjustment.

Non-deductible intercompany payments

There are no specific categories of intercompany payment that are non-deductible. Intercompany payments shall comply with transfer pricing regulation and subject to the same tax rules on their deductibility as third-party payments.

Anti-avoidance

The regulations governing tax avoidance are:

- Minister of Finance Regulation No. 35/PMK.03/2019 regarding Determination of Permanent Establishment. PMK-35 is in line with existing PE concepts in the ITL and the relevant OECD and UN Commentaries. However, particularly with respect to the ITL provisions, it does provide more detail on some interpretive issues that were not included in previously existing regulations, such as:

- some principles to be applied in making determinations of ‘a fixed place of business that is permanent in nature, through which the foreign subjects carry out business or conduct activities in Indonesia’;

- the definition of business or activity that covers anything that is conducted to obtain, collect or maintain income;

- some guidance of what constitutes ‘preparatory’ or ‘auxiliary’ activities that are excluded as a PE;

- the inclusion of construction, installation or assembly projects where the projects are in Indonesia but work is performed outside Indonesia, or where work is subcontracted to domestic or foreign subcontractors as (part of) a PE;

- expanding on the tax law definition of a Services PE. A Service PE can apply if the employee or other personnel is employed by a foreign subject or is a subcontractor of a foreign subject, the provision of the service is performed in Indonesia, and the service is delivered to parties in or outside of Indonesia; and

- expanding on the determination of dependent versus independent agents as relating to the establishment of a PE for a foreign subject. A person or entity is considered to be acting for and on behalf of foreign subjects, and determined as a dependent agent, if their business or activity is acting under instructions from the foreign subjects or does not bear their own risk from the business or activity;

- Minister of Finance Regulation No. 107/PMK.03/2017 as updated by Minister of Finance Regulation No. 93/PMK.03/2019 Regarding CFC Rules. This regulation is in line with OECD BEPS Recommendation No. 3; and

- Minister of Finance Regulation No. 169/PMK.010.2015 regarding the Debt to Equity Ratio for Income Tax Calculation. This regulation is in line with OECD BEPS Recommendation No. 4.

Location savings

There is no specific ruling regarding location savings and other location-specific attributes under the applicable existing transfer pricing rules. However, Indonesia follows the guidance provided in the OECD Transfer Pricing Guidelines 2017 version. Indonesia is now in the process of finalising the finance ministry regulation to adopt the OECD’s recommendation in BEPS 8-10.

Branches and permanent establishments

The profits attributed to the PE are those that it might be expected to make if it were a separate enterprise, dealing independently with the enterprise. Profits are therefore calculated on an arm’s-length basis.

Exit charges

No specific exit charges are imposed on restructurings, although a transfer pricing adjustment may be applied within the normal course of transfer pricing if certain aspects of the restructuring are considered not to be arm’s-length.

Temporary exemptions and reductions

Yes. As stated in Minister of Finance Regulation No. 150/PMK.010/2018 dated 26 November 2018, the tax holiday is available for new investments that meet the requirements as listed.

- These include pioneer industries in the following business sectors:

- integrated upstream basic metal;

- integrated oil and gas refinery;

- integrated petrochemicals from oil, gas or coal;

- integrated inorganic basic chemicals;

- integrated organic basic chemicals from agriculture, plantation or forestry products;

- integrated pharmaceutical raw materials;

- semi-conductors and other main components of computers thatare integrated with computer manufacturing;

- the main components of communication equipment that are integrated with smartphone manufacturing;

- the main components of health equipment, which are integrated with irradiation, electro medical or electrotherapy manufacturing;

- main components of industrial machinery that are integrated with machinery manufacturing;

- main components of machinery that are integrated with motor vehicle manufacture;

- robotics components that are integrated with the manufacturing industry;

- main components of vessels that are integrated with vessel manufacturing;

- main components of aircraft that are integrated with aircraft manufacturing;

- main components of train that are integrated with train manufacturing;

- power plant machinery;

- economic infrastructure; or

- digital economy, which includes data processing, hosting and activities related to it.

- The minimum legalised capital investment plan is 500 billion rupiah. PMK 35 does not require this new investment in the form of a new taxpayer (ie, company) nor the placing of an investment commitment in the form of a bank deposit.

- The taxpayer is required to satisfy the debt-to-equity ratio for income tax purposes as stipulated in MoF Regulation No. 169/PMK.010/2015.

- The taxpayer has never had its tax holiday application granted or rejected by MoF.

- The taxpayer is in incorporated in Indonesia.

- Domestic shareholders of the applicant must obtain a tax clearance letter issued by the DGT.

The facilities under MoF 150 are:

- a 100 per cent corporate income tax reduction for new investments of a minimum 500 billion rupiah, and a 50 per cent corporate income tax reduction for new investments between 100 billion rupiah and 500 billion rupiah;

- the concession period for 100 per cent corporate tax reduction facilities is five to 20 years, depending on the investment value, and five years for the 50 per cent corporate income tax reduction facility; and

- a transition period – 50 per cent corporate income tax reduction for the next two years after the end of the concession period for minimum new investments of 500 billion rupiah and 25 per cent corporate income tax reduction for the next two years after the end of the concession period for new investments of 100 million rupiah to 500 billion rupiah.

Update and trends

Tax authority focus and BEPS

Tax authority focus and BEPS41 What are the current issues of note and trends relating to transfer pricing in your country? How is the OECD’s project on base erosion and profit shifting affecting both policymakers and tax administrators?

The focus and targets of transfer pricing audits based on Circular Letter of DGT No 15/PJ/2018 are:

- analysis of corporate tax to turn over ratio, gross profit margin and net profit margin compared to benchmarking of similar industries, based on industry reports or benchmarking results in accordance with the provisions governing benchmarking. The risk of non-compliance is high if the difference between the analysis and the industry average is greater than 10 per cent;

- having transactions with parties that have a special relationship, especially with affiliates domiciled in countries that have an effective tax rate that is lower than the effective tax rate in Indonesia;

- having a domestic affiliate transaction (intragroup transaction) with a transaction value of more than 50 per cent of the total transaction value; and

- having a domestic affiliated transaction with members of a business group that has compensation for losses.

—————–

Deemed Dividends for CFCs

Indonesia’s Ministry of Finance (MOF) issued a regulation (PMK-93) on 26 June 2019 that updates the controlled foreign corporation (CFC) rules as from fiscal year 2019. PMK-93 amends certain provisions of a regulation dating from 2017 (PMK-107) relating to the determination of deemed dividends from CFCs.

Under Indonesian tax law, a CFC is a foreign company in which an Indonesian resident company or individual (either alone or together with other shareholders) holds at least 50% of the company’s total share capital. An Indonesian shareholder in a CFC must pay Indonesian tax on its share of deemed dividends from the CFC each year, to the extent the related profits are not distributed to the shareholder in the form of actual dividends. Where an actual dividend distribution exceeds prior year deemed dividends, the excess is taxable in the year the actual dividend is paid. The CFC rules do not apply to shareholdings in listed foreign companies.

Determination of deemed dividend income

PMK-93 updates the rules for determining deemed dividends from CFCs. As opposed to the rules prescribed under PMK-107, which stipulated that deemed dividends include all income from both direct and indirect CFCs irrespective of the nature of the income (i.e. whether active or passive), PMK-93 limits deemed dividends to the following types of passive income:

- Dividends (excluding dividends from other CFCs);

- Interest (excluding interest received by a CFC that is owned by an Indonesian tax resident bank; however, this exception does not apply to interest income received by a CFC from Indonesian tax resident related parties);

- Rent from land, buildings and other assets (if received from a related party);

- Royalties; and

- Gains from the sale or transfer of assets.

Deemed dividend calculation

Under PMK 93, deemed dividends are calculated as the gross income of the CFC from the types of passive income described above, reduced by the following deductions and taxes:

- Expenses incurred by the CFC to obtain, maintain and collect the income; and

- Income taxes due or paid by the CFC with respect to the income, including taxes withheld from the income when it was paid to the CFC.

Comments

The new CFC rules are expected to accommodate the needs of Indonesian businesses to expand overseas. The exclusion of active business income from deemed dividends means that offshore subsidiaries of Indonesian holding companies will be able to reinvest their net active business income without incurring additional Indonesian tax.