Skip to content

Skip to content

Value Added Tax (VAT) is levied on the sale of goods or

services by UK businesses.

VAT is collected on behalf of HM Revenue & Customs by companies. A company

pays VAT to HMRC by calculation the amount of VAT charged to customers minus

any VAT they have paid on their own purchases.

All goods and services are either VAT-rated or VAT-exempt. VAT-exempt items

include rent, private education, health services, postal services, finance and

insurance, and gambling.

A business must register for VAT once the sales exceed £82k (as of 1st April

2015) in a year, or else you can make a voluntary registration even before

hitting this threshold.

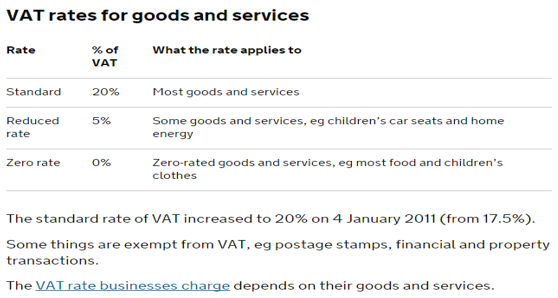

VAT is charged on goods at different levels. The current standard rate of 20%

applies to most items.

A Reduced Rate of 5% applies to many items including mobility aids for the

elderly, smoking cessation products (nicotine patches and gum), electricity and

gas for domestic and residential use, children’s car seats, booster seats and

booster cushions and many more.

Finally, there is a Zero Rate on many items, including but not limited to –

Cycle helmets (CE marked), Protective boots and helmets for industrial use,

children’s clothes and footwear, baby wear, printing of brochures, leaflets and

pamphlets, aircraft repair and maintenance, building services for disabled

people.

- From outside EU – vat is charged on goods imported from outside the eu as if it were customs duty. It does not matter whether the importer is a taxable person. Taxable persons need to keep evidence of the vat paid on imports as they will be able to recover the inpit tax in the normal way if they use the goods to make taxable supplies. Non taxable persons such as consumers or unregistered business will not be able to recover the tax

- If vat registered then

- If domestic, then add vat to selling price and on vat returns, he nets the paid from received

- If another eu country then zero rate

- If purchased from inside eu,

- If unregistered then pay exporters vat

- If registered then local vat rate

- On sales

- If vat registered then normal unless exporters which is zero domestic

- Sell outside eu then zero but keep documents to prove that outside eu