Skip to content

Skip to content A permanent establishment (PE) is a fixed place of business which generally gives rise to income or value-added tax liability in a particular jurisdiction. The term is defined in many income tax treaties and in most European Union Value Added Tax systems. The tax systems in some civil-law countries impose income taxes and value-added taxes only where an enterprise maintains a PE in the country concerned. Definitions of PEs under tax law or tax treaties may contain specific inclusions or exclusions.

I first wrote about Permanent Establishment here – https://www.mooresrowland.tax/2015/06/e-commerce-and-taxation.html

Recent conversations mean that I need to return to the topic.

The contrasting of Permanent Establishment versus Nexus Standard is a very important subject of US International Tax to understand because, it will not only determine if a corporation is subject US Federal and/or State tax, but also how to manage expansion of a foreign corporation to the United States.

The United States uses a bilateral structure to tax the income of a ‘Foreign Corporation’ that is, in this case, a corporation which is formed in accordance with the laws of a country foreign to the US. (Internal Revenue Code Sec. 7701(a))

If the foreign corporation has Permanent Establishment in the United States, the resulting net income effectively connected with that U.S.trade or business is taxed at the customary graduated rates. (Internal Revenue Code Sec. 882). Also, the gross amount of a foreign corporation’s U.S.-Source income such as dividend, interest, royalty and other investment-type income commonly referred to as Fixed Determinable Annual and Periodic Income is subject to a flat-rate of 30% (IRS Pub. 515 Table 1).

The words PERMANENT ESTABLISHMENT are supremely important in the world of inbound US international taxation and that is because, in effect, a foreign corporation’s business profits are subject to U.S.taxation if the foreign corporation is ‘engaged in trade or business within the United States’.

But here is the problem; neither the Code nor the Regulations provide a comprehensive definition of the term trade or business. Sec. 864(b) of the Internal Revenue Code of the United States, the most authoritative Tax document in US Tax Law, presents that a U.S. trade or business includes ‘the performance of personal services within the United States’ but does not include the trading of stocks, securities, or commodities, if such trades are either made through an independent agent, or made for the taxpayer’s own account (unless the taxpayer is a broker dealer for example). In fact, these exceptions do not apply if the foreign corporation has an office in the United States through which the trades are made.

Case law proposes that a foreign corporation is engaged in a U.S. trade or business if its employees are engaged in considerable, continuous, and regular business activity within the United States. Also, if a partnership, estate, or trust is engaged in a U.S.trade or business, then each partner or beneficiary is measured to be engaged in a U.S.trade or business. (Code Sec 875)

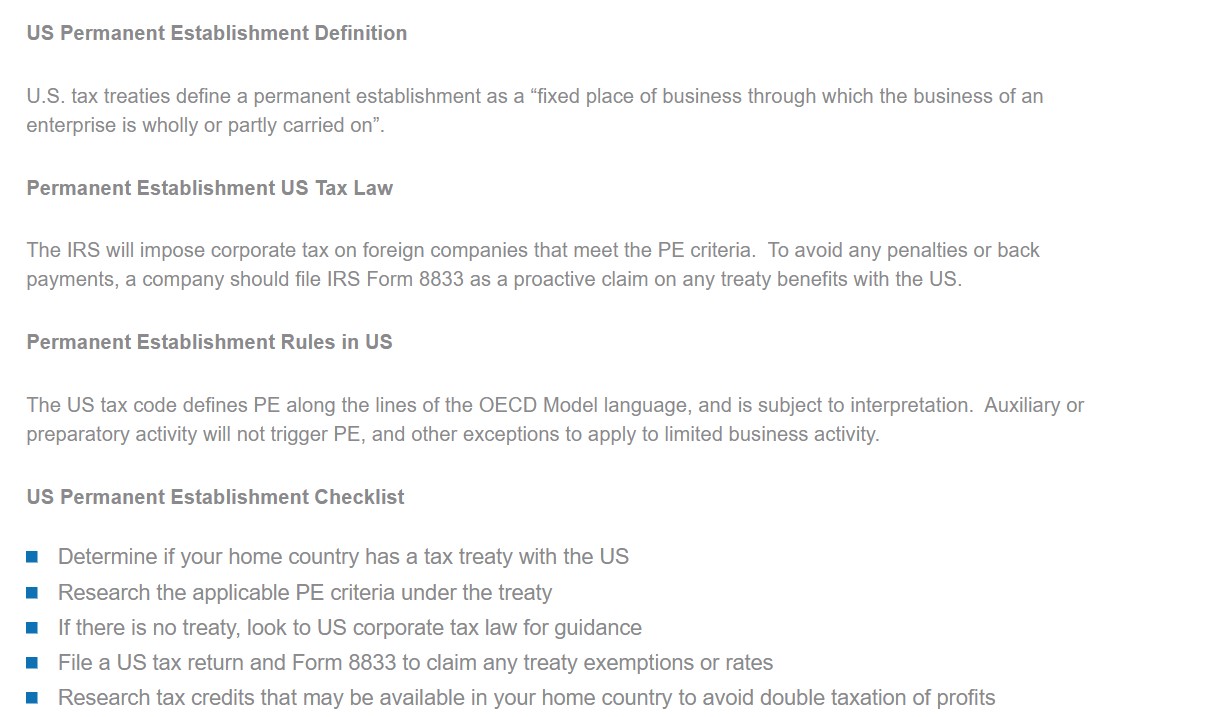

The IRS code could deem that a foreign company is conducting a taxable trade or business based on its level of business and contracts in the US. This can be avoided by foreign companies that are only planning on having limited activity in the US, and whose country of residency has an income tax treaty with the US. To do so, care must be taken to avoid creating a permanent establishment through a fixed place of business in the US.

To take advantage of this benefit, the foreign company must file a tax return position on a timely filed IRS Form 8833 claiming the treaty benefit. If a permanent establishment has not been created, then none of the income will be taxable, but a protective return will still have to be filed.

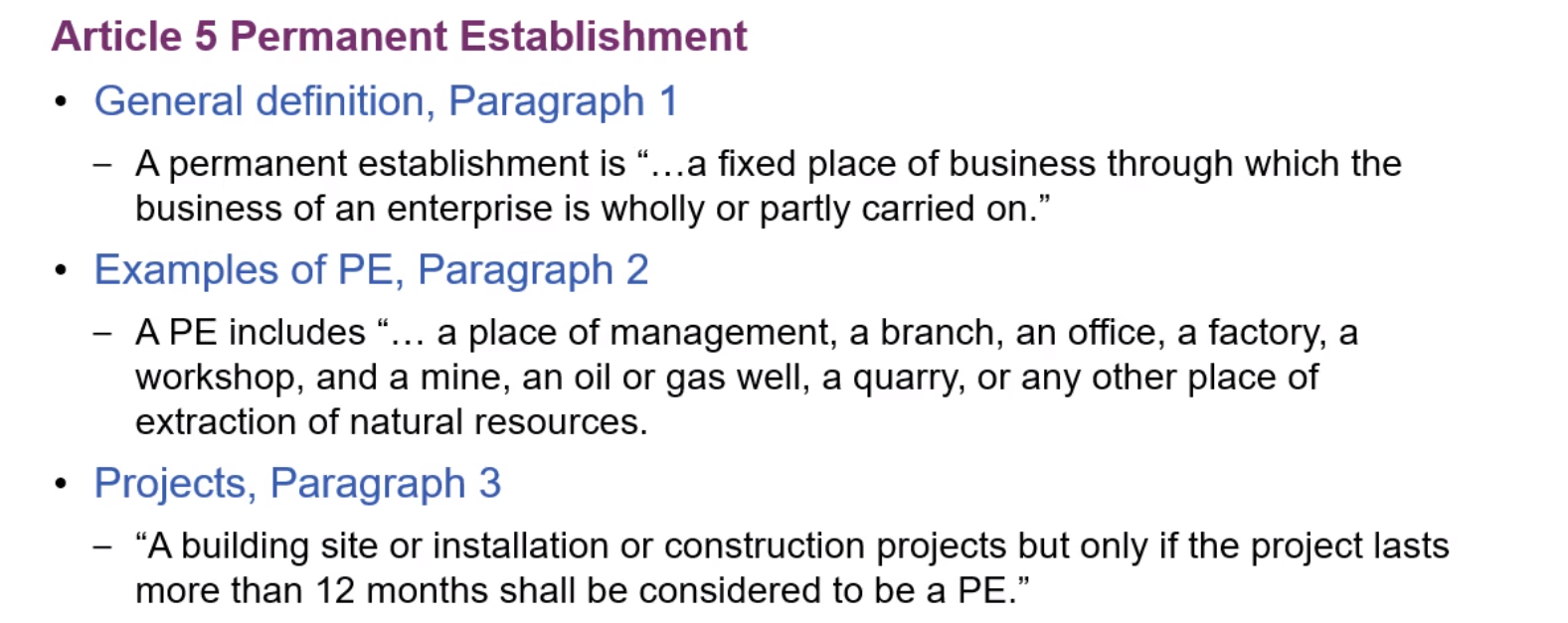

U.S. tax treaties define a permanent establishment as a “fixed place of business through which the business of an enterprise is wholly or partly carried on”. The existence of a permanent establishment is determined based on the facts and circumstances of each case, but even if the business of the foreign company is being conducted through a fixed place of business, the company will not be considered to have a permanent establishment if these activities are limited to certain auxiliary and preparatory activities.

Some examples of places of business, which create a permanent establishment, listed on the OECD Model Treaties include the following:

- Place of management

- Branch or office

- Factory

- Workshop

- Mine, oil or gas well, or any other place of extraction of natural resources

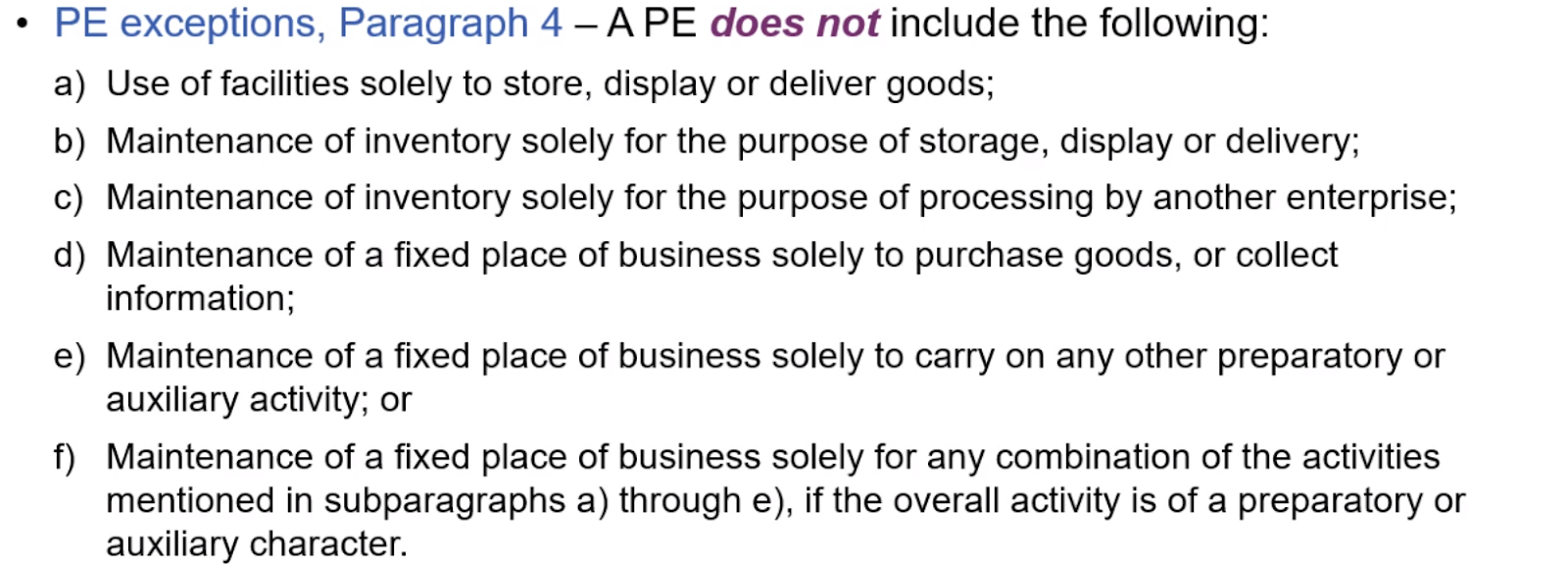

Examples of activities that do not create a permanent establishment include the following:

- Use of a facility to store, display or deliver goods or merchandise (E.g. Showroom)

- Maintaining a fixed place of business solely for the purpose of purchasing goods or merchandise, or of collecting information, for the enterprise

- Maintaining a fixed place of business solely for the purpose of advertising, supplying information, scientific research, or for the preparations relating to the placement of loans, or for similar activities which have a preparatory or auxiliary character, for the enterprise.

In the case that a foreign company owns a partnership that has a permanent establishment in the United States, the company, as a partner in such company, is also deemed to have a permanent establishment. Even limited partners, as in the case of Donroy, Ltd v. United States, are considered to have a permanent establishment in these cases.

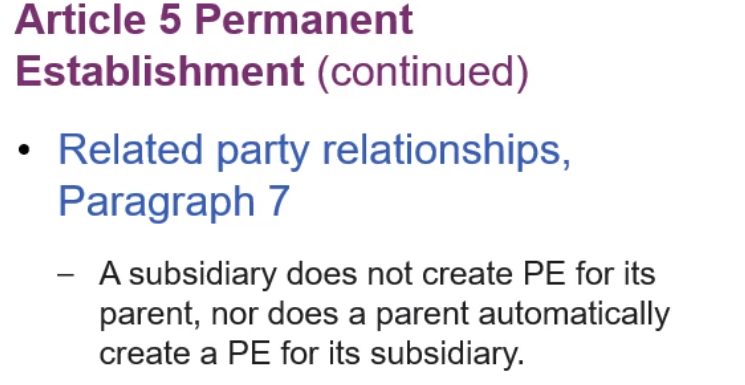

Having a subsidiary in the US, however, does not automatically create a permanent establishment for its parent as it is considered to be an independent legal entity, but there are ways that it could create a permanent establishment, for example, if both the parent and the subsidiary have the same officers, a permanent establishment could be created by the parent, if the activies of such officers in the US are considered to be on behalf of the parent rather than the subsidiary.

Note that under Reg. Section 1.882-4(a)(3)(vi), foreign corporations with limited activities in the US that determine that these activities do not give rise to effectively connected income may file a return for the tax year to protect their rights to receive the benefit of deductions and credits in the event that it is later determined, after the return is filed, that the determination was incorrect. The protective return does not need to report any income as effectively connected income or report deductions or credits but should include a statement that the return is being filed to preserve the foreign corporation’s right to deductions and credits

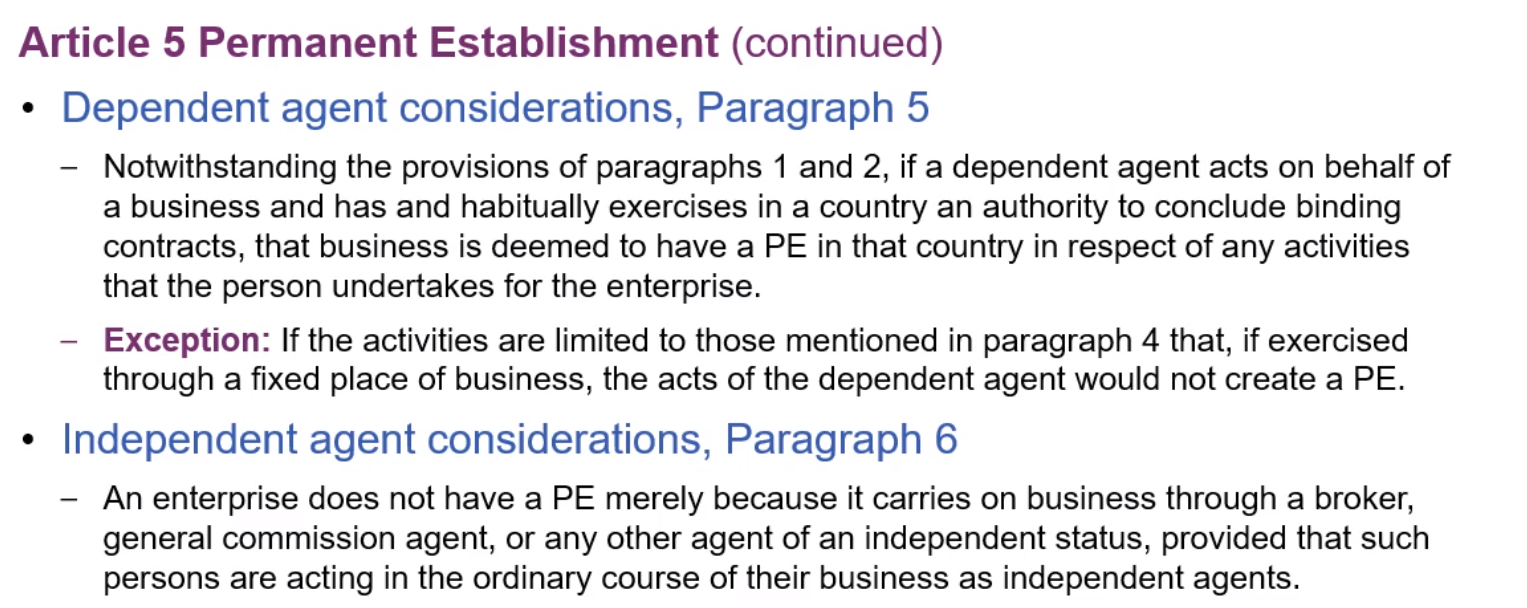

If a foreign company has agents in the United States, they could also create a permanent establishment for the foreign company. For this to happen, two requirements would have to be met:

- The person is not a broker, commission agent, or other agent of independent status, and is conducting acts in the ordinary course of its business on behalf of the foreign company in the United States.

- That person has and habitually exercises in the United States an authority to conclude contracts that are binding on the corporation.

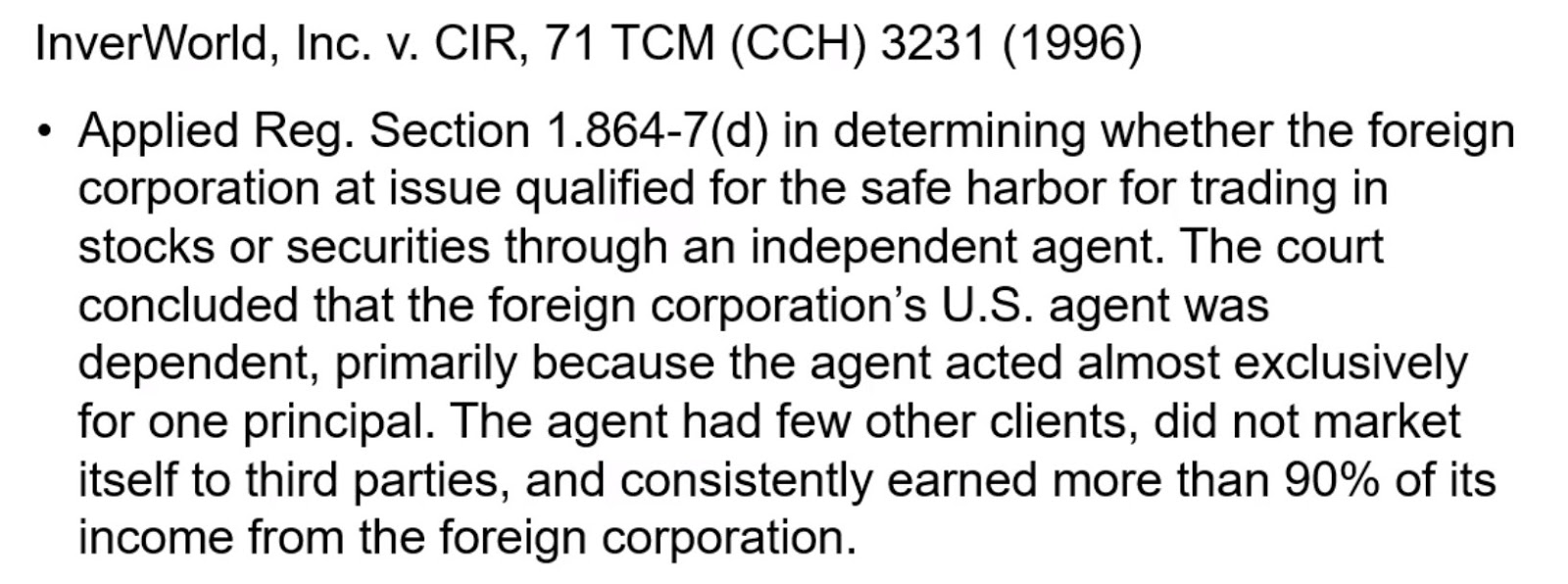

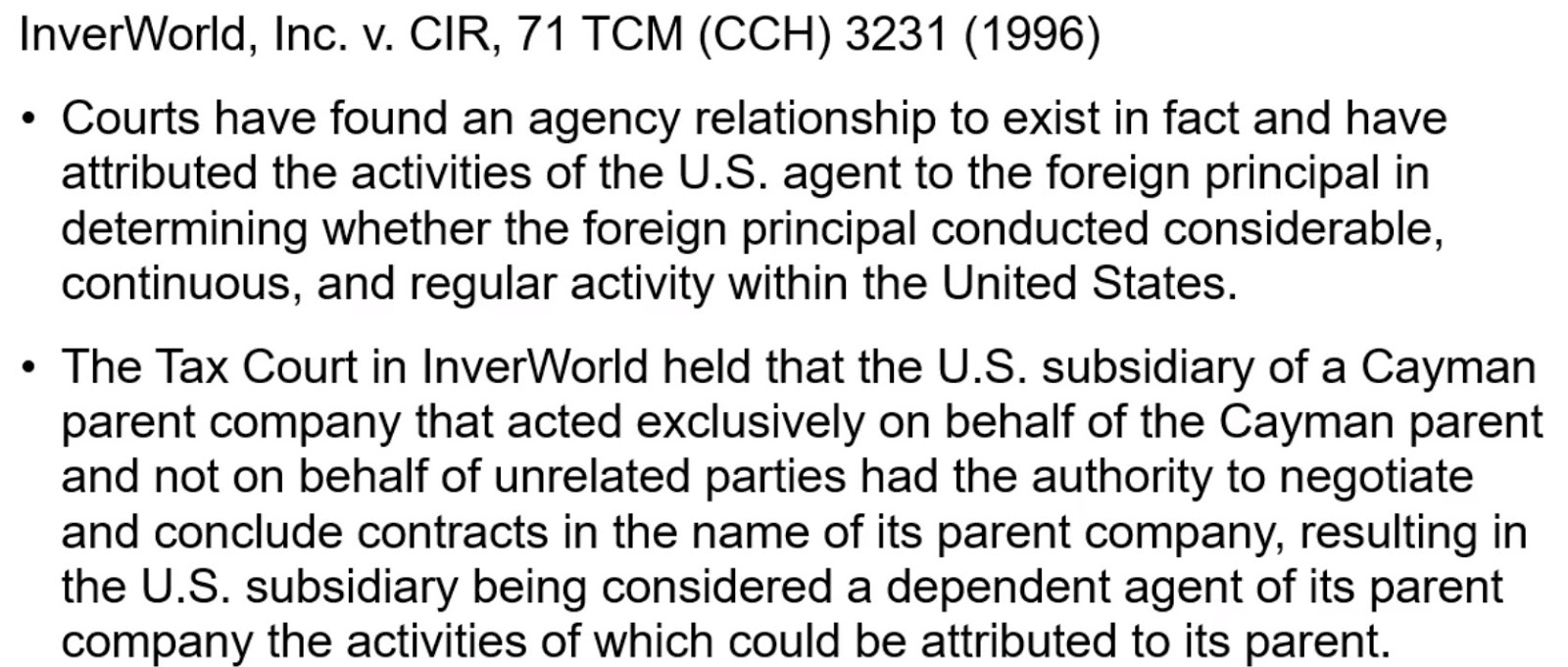

To understand PE issues requires more than reviewing the IRC code sections but we need to grasp the principles derived from case law too. Here’s a 1996 case where PE was determined because of a dependent agent

In summary –

The above discussion refers to Federal Taxation only. For a discussion on state tax? Have a look here – https://www.mooresrowland.tax/2019/11/responsible-person-rules-in-wake-of.html

Questions? Talk to your tax consultant today