Skip to content

Skip to content President Reagan signed H.R. 4170 into law on July 18, 1984. Thus, effective for tax years beginning after 1984, objective definitions of the terms residents aliens (“RAs”) and nonresidents aliens (“NRAs”) for Federal income tax purposes are incorporated into the Code.

It is very important to note however, that the new definitions do not affect the determination of residence for Federal estate and gift tax purposes (discussed later). In addition, the Joint Explanatory Statement of the Committee of Conference (the “Joint Statement”) also makes it clear that it is not intended that the definitions of RA and NRA affect the determination of whether an estate or trust is a U.S. or foreign estate or trust, “except insofar as that determination itself turns on the residence or non-residence of particular alien individuals.”

RESIDENCE TESTS

Code Section 7701(b) sets forth the following two (2) tests pursuant to which an alien individual will be considered a RA with respect to any calendar year if he:

- (i) is a lawful permanent resident of the United

States at any time during the calendar year (the “Green Card Test”);

or

- (ii) is present in the U.S. for thirty-one (31) days or more during the current calendar year and has been present in the United States for a substantial period of time–one hundred eighty-three (183)

days or more during a three (3) year period weighted toward the present year (the “Substantial Presence Test”).

Pursuant to Section 7701(b)(1)(A), an alien individual is to be considered a RA for any calendar year, if and only if, he satisfies the requirements of the Green Card Test, the Substantial Presence Test or the First Year Election.

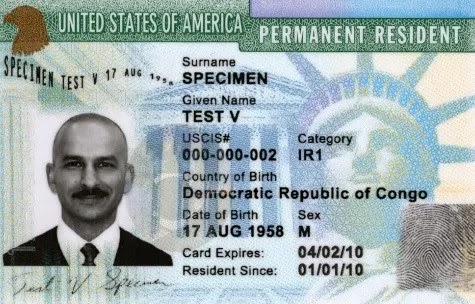

- The Green Card Test: A lawful permanent resident is defined as an individual who has the status of having been lawfully accorded the privilege of residing permanently in the United States in accordance with the immigration laws, and if such status has not been revoked (and has not been administratively or judicially determined to have been abandoned). Thus, a lawful permanent resident continues to be a

resident for income tax purposes until he officially loses or abandons the status of lawful permanent resident.

- The Substantial Presence Test: An alien individual is classified as a RA as to a calendar year (the “current year”) if he is present in the United States for thirty-one (31) or more days in the current year and has been present in the United States for one hundred eighty three (183) days or more during a three (3) year period, weighted toward the current year. This weighting takes place as follows: an alien is considered a RA during the current year if the sum of the days he is present in the United States during the current year, plus one-third (1/3) of the days present during the first preceding year, plus one-sixth (1/6) of the days present during the second preceding year, equals or exceeds one hundred eighty-three (183) days.

Source: https://www.mooresrowland.tax/2018/06/more-on-pre-immigration-us-tax-planning.html

But there are exceptions to the substantial presence test. These exceptions include

· An individual who is temporarily in the United States as a foreign government-related individual

This type of person will hold an “A” or “G” visa but not an “A-3” or “G-5” class visa.

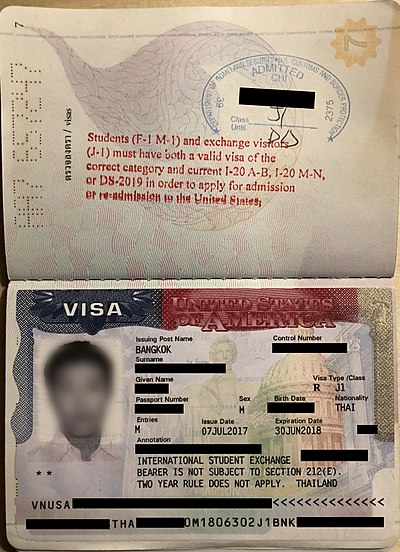

· A teacher or trainee who is temporarily in the United States under a “J” or “Q” visa

This person must substantially comply with the requirements of the visa.

· A student who is temporarily in the United States under an “F,” “J,” “M,” or “Q” visa

This person must substantially comply with the requirements of the visa.

· A professional athlete who is temporarily in the United States to compete in a charitable sports event

Let’s talk about J visas.

A teacher or trainee is an individual, other than a student, who is temporarily in the United States under a “J ” or “Q ” visa and substantially complies with the requirements of that nonimmigrant status. You are considered to have substantially complied with the requirements of that nonimmigrant status if you have not engaged in activities that are prohibited by U.S. immigration laws and could result in the loss of your nonimmigrant status. Any nonimmigrant temporarily present in the U.S. in “J” or “Q” status who is not a student is included within the definition of “Teacher or Trainee.” For example, alien physicians, au pairs, short-term scholars, and summer camp workers temporarily present in the U.S. in “J” nonimmigrant status are included within the IRS definition of “Teacher or Trainee.” In addition, cultural exchange visitors in “Q” nonimmigrant status are also included within the IRS definition of “Teacher or Trainee”.

Also Included Are Immediate Family Members of Exempt Teachers and Trainees

Members of the immediate family include the individual’s spouse and unmarried children (whether by blood or adoption), but only if the spouse’s or unmarried children’s nonimmigrant statuses are derived from, and dependent on, the exempt individual’s nonimmigrant status. Unmarried children are included only if they meet all the following:

- Are under 21 years of age.

- Reside regularly in the exempt individual’s household.

- Are not members of another household.

The immediate family of an exempt individual does not include attendants, servants, or personal employees.

When a Teacher or Trainee is Not Exempt

You will not be an exempt individual as a teacher or trainee if you were exempt as a teacher, trainee, or student for any part of 2 of the 6 calendar years preceding the current year. However, you will be an exempt individual if you were exempt as a teacher, trainee, or student for any part of 4 (or fewer) of the 6 preceding calendar years and:

- A foreign employer paid all of your compensation during the current year.

- A foreign employer paid all of your compensation during each of the preceding 6 years

- you were present in the United States as a teacher or trainee.

A foreign employer includes an office or place of business of an American entity in a foreign country or a U.S. possession.

If you qualify to exclude days of presence as a teacher or trainee, you must file a fully-completed Form 8843, Statement for Exempt Individuals and Individuals with a Medical Condition with the IRS. Form 8843 may be attached to your U.S. federal income tax return for the tax year, or it may be mailed separately to the address indicated in the General Instructions attached to the Form 8843.

Example:

Carla is temporarily present in the United States as a teacher in J-1 nonimmigrant status. She entered the United States on August 15, 2012, and is employed by a university in California. She has never been in the United States prior to this visit. Carla is an Exempt Individual for calendar years 2012 and 2013 because during those two years she meets the test that prior to the current year she was not present during two years in the United States in F, J, M, or Q nonimmigrant status during the 6 calendar years prior to the current year. However, for calendar year 2014 she is no longer an Exempt Individual because she was present during two years in the United States in F, J, M, or Q nonimmigrant status during the 6 calendar years preceding the current year. For calendar year 2014, Carla must count her days of presence in the United States for the purpose of passing the Substantial Presence Test.

Source: https://www.irs.gov/individuals/international-taxpayers/exempt-individuals-teachers-and-trainees

What about a Student?

A student is an individual who is temporarily present in the United States under an “F,” “J,” “M,” or “Q” visa and who substantially complies with the requirements of the visa. If you

were a student under an “F,” “J,” “M,” or “Q” visa, you are considered to have substantially complied with the visa requirements if you haven’t engaged in activities that are prohibited by U.S. immigration laws and could result in the loss of your visa status.

Even if you meet these requirements, you can’t exclude days of presence in 2018 as a student if you were exempt as a teacher, trainee, or student for any part of more than 5 calendar years unless you establish that you don’t intend to reside permanently in the United States. The facts and circumstances to be considered in determining if you have established that you don’t intend to reside permanently in the United States include, but aren’t limited to:

1. Whether you have maintained a closer connection to a foreign country than to the United States (for details, see Pub. 519), and

2. Whether you have taken affirmative steps to change your status from nonimmigrant to lawful permanent resident.