Skip to content

Skip to content

In March 2018, the Internal Revenue Service (IRS) has announced a number of tax-related provisions for 2018, including, the latest tax tables. These changes are due to the Tax Jobs and Cuts Act of 2017, signed into law by President Trump on December 22, 2017. The Internal Revenue Bulletin (IRB): 2018-10 dated March 5, 2018, confirms the new numbers. Changes of note include those to the EITC, adoption credit, and more.

These are the numbers for the tax year 2018 beginning January 1, 2018. You’ll use these numbers below to prepare your 2018 tax returns in 2019.

If you aren’t expecting any significant changes in 2018, you can use the updated tax tables and other tax numbers to estimate your liability. If you expect to make more money or have a change in your circumstances (i.e., get married, buy a house, start a business, have a baby), consider adjusting your withholding or tweaking your estimated tax payments.

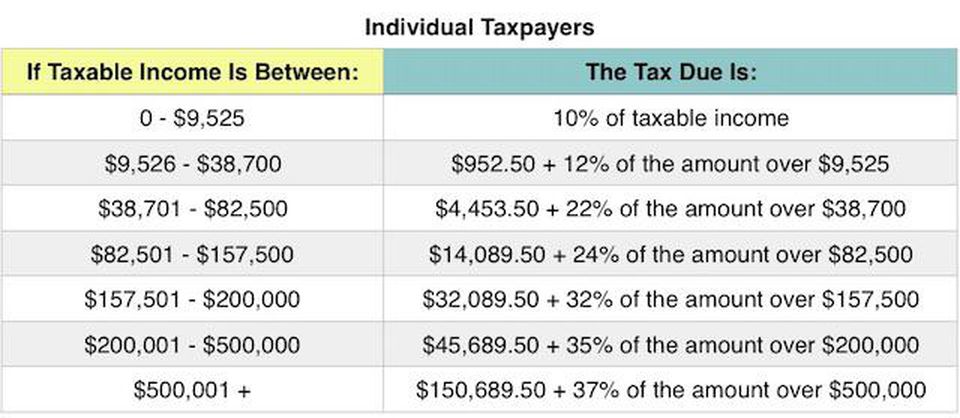

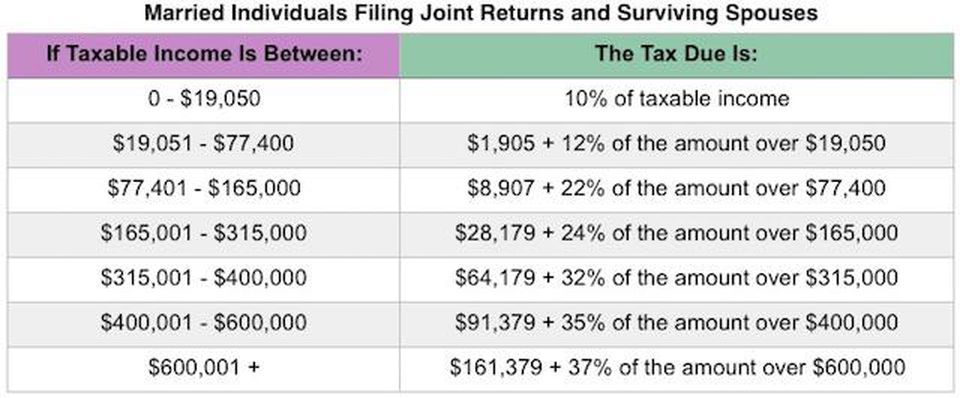

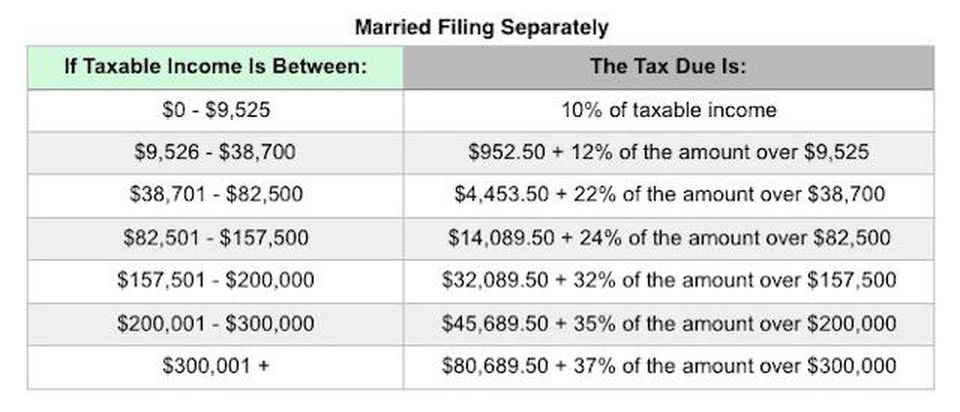

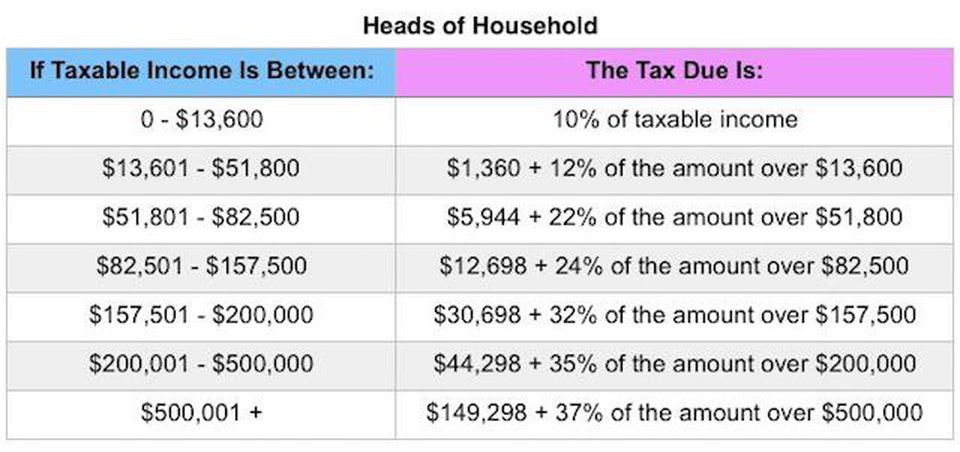

Tax Brackets and Tax Rates. The big news is, of course, the tax brackets and tax rates for 2018. There are still seven (7) tax rates. They are: 10%, 12%, 22%, 24%, 32%, 35% and 37% (there is also a zero rate). Here’s how those break out by filing status:

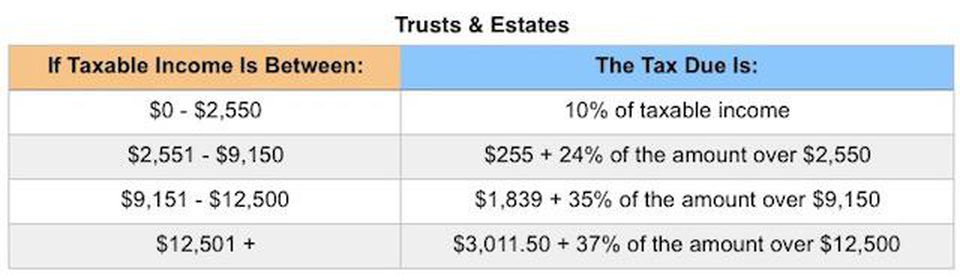

And it isn’t just the federal estate tax exemption that have been modified. Tax rates for trusts and estates have changed, too:

You can compare these numbers to the 2017 tax tables here and the original 2018 tax tables (those that IRS previously announced) here.

- Remember to pay attention to the progressive nature of the rates when you’re making comparisons – and don’t simply multiply your income by the top rate.

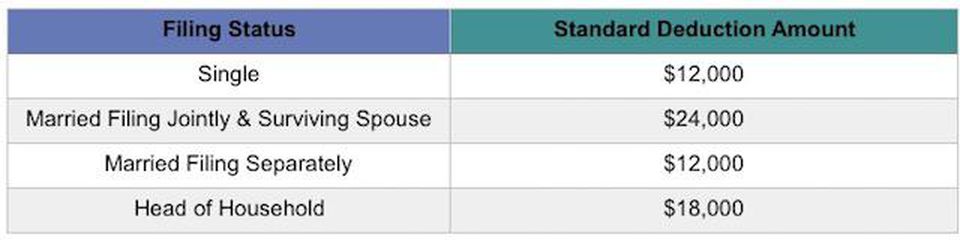

Standard Deduction Amounts. The standard deduction amounts will increase to $12,000 for individuals, $18,000 for heads of household, and $24,000 for married couples filing jointly and surviving spouses.

- For 2018, the additional standard deduction amount for the aged or the blind is $1,300. The additional standard deduction amount increases to $1,600 for unmarried taxpayers.

- For 2018, the standard deduction amount for an individual who may be claimed as a dependent by another taxpayer cannot exceed the greater of $1,050 or the sum of $350 and the individual’s earned income.

There will be no personal exemption amounts for 2018.

Since there will be no personal exemption amounts, here’s your cheat sheet for figuring whether you need to file a return in 2019 for the 2018 tax year (compare to the 2017 tax year rules here).

- For individual taxpayers, you will be required to file a tax return if your gross income for the taxable year is more than the standard deduction.

- For married taxpayers, you will be required to file a tax return if your gross income, when combined with your spouse’s gross income, is more than the standard deduction for a joint return, provided that you and your spouse lived in the same home; your spouse does not file a separate tax return; and neither you nor your spouse is a dependent of another taxpayer who has income other than earned income in excess of $500 (indexed for inflation).

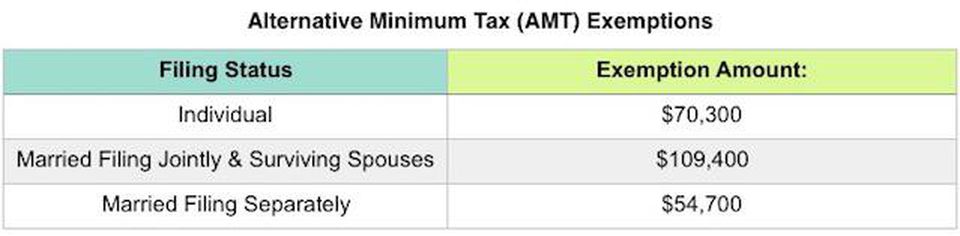

The alternative minimum tax (AMT) exemption amounts are permanently adjusted for inflation. The AMT exemption amounts will be as follows:

AMTERB

Kiddie Tax. The kiddie tax applies to unearned income for children under the age of 19 and college students under the age of 24. Unearned income is income from sources other than wages and salary, like dividends and interest. Taxable income attributable to net unearned income will be taxed according to the brackets applicable to trusts and estates (see above, earlier). With respect to earned income, the rules are the same as before.

For high-income taxpayers who itemize their deductions, the Pease limitations, named after former Rep. Don Pease (D-OH), previously capped or phased out certain deductions. For 2018, the Pease limitations do not apply.

Some additional tax credits and deductions were adjusted for 2018 or altered under the conference bill. Here’s a look at a few of the most popular:

- Child Tax Credit. The child tax credit has been expanded to $2,000 per qualifying child and is refundable up to $1,400, subject to phaseouts. The bill also includes a temporary $500 nonrefundable credit for other qualifying dependents. Phaseouts, which are not indexed for inflation, will begin with adjusted gross income (AGI) of more than $400,000 for married taxpayers filing jointly and more than $200,000 for all other taxpayers. For specific dollar amounts and more about the expanded CTC, click here.

- Earned Income Tax Credit (EITC). For 2018, the maximum EITC amount available is $6,431 for taxpayers filing jointly who have three or more qualifying children. Income phaseouts apply. For more info, IRB 2018-10 has a table providing maximum credit amounts for other categories, income thresholds, and phaseouts.

- Adoption Credit. For 2018, the credit allowed for an adoption of a child with special needs is $13,810, and the maximum credit allowed for other adoptions is the amount of qualified adoption expenses up to $13,810. Phaseouts apply beginning with modified adjusted gross income (MAGI) in excess of $207,140 and completely phased out for taxpayers with MAGI of $247,140 or more.

- Student Loan Interest Deduction. For 2018, the maximum amount that you can deduct for interest paid on student loans remains $2,500. Phaseouts apply for taxpayers with MAGI in excess of $65,000 ($135,000 for joint returns) and is completely phased out for taxpayers with MAGI of $80,000 or more ($165,000 or more for joint returns). The conference bill did not repeal the deduction.

- Foreign Earned Income Exclusion. For tax year 2018, the foreign earned income exclusion is $103,900, up from $102,100 for tax year 2017.

- Medical Savings Accounts (MSA). For 2018, a high-deductible health plan (HDHP) is one that, for participants who have self-only coverage in an MSA, has an annual deductible that is not less than $2,300 but not more than $3,450; for self-only coverage, the maximum out-of-pocket expense amount is $4,550. For 2018, HDHP means, for participants with family coverage, an annual deductible that is not less than $4,550 but not more than $6,850; for family coverage, the maximum out-of-pocket expense is $8,400.

There are significant changes to itemized deductions found on Schedule A, including:

- Medical and Dental Expenses. The “floor” for medical and dental expenses is 7.5%. That means that you can only deduct expenses which exceed 7.5% of your AGI.

- State and Local Taxes. Deductions for state and local sales, income, and property taxes normally deducted on a Schedule A remain in place but are limited. The amount that you are claiming for all state and local sales, income, and property taxes together may not exceed $10,000 ($5,000 for married taxpayers filing separately). Foreign real property taxes may not be deducted under this exception.

- Home Mortgage Interest. The home mortgage interest deduction has been modified. You may only deduct interest on acquisition indebtedness – your mortgage used to buy, build or improve your home – up to $750,000 ($375,000 for married taxpayers filing separately). For mortgages taken out before December 15, 2017, the limit is $1,000,000 ($500,000 for married taxpayers filing separately). For more on mortgage interest under the new law, click here.

- Charitable donations. The percentage limit for charitable cash donations by an individual taxpayer to public charities and certain other organizations has increased from 50% to 60%.

- Casualty and Theft Losses. The deduction for personal casualty and theft losses is repealed except for those losses attributable to a federal disaster as declared by the President (generally, this is meant to allow some relief for victims of Hurricanes Harvey, Irma, and Maria). For more on casualty losses after a disaster, click here.

- Job Expenses and Miscellaneous Deductions subject to 2% floor. Miscellaneous deductions which exceed 2% of your AGI have been eliminated. This includes deductions for unreimbursed employee expenses and tax preparation expenses. To be clear, it includes expenses that you incur in your job that are not reimbursed, like tools and supplies; required uniforms not suitable for ordinary wear (like those ABBA costumes); dues and subscriptions; and job search expenses. These expenses also include unreimbursed travel and mileage, as well as the home office deduction.

The shared individual responsibility payment remains in place. Taxpayers that don’t maintain health insurance coverage must claim a waiver or exemption or be subject to the penalty. For 2018, the penalty is equal to 2.5% of your AGI, or $695 per adult and $347.50 per child, up to a maximum of $2,085, whichever is higher. That amount is unchanged from 2017.

And don’t forget about those changes affecting pass-throughs and business owners who file a Schedule C. You’ll find more on that here.

source: https://www.forbes.com/sites/kellyphillipserb/2018/03/07/new-irs-announces-2018-tax-rates-standard-deductions-exemption-amounts-and-more/#613e95e23133

More on deductions here – https://www.mooresrowland.tax/2019/01/deduction-highlights-2019.html