Skip to content

Skip to content

·

Dividends –

o

From April 2016 the Dividend Tax Credit will be

replaced by a new tax-free Dividend Allowance.

o

The Dividend Allowance means that you won’t have

to pay tax on the first £5,000 of your dividend income, no matter what

non-dividend income you have.

o

You’ll pay tax on any dividends you receive over

£5,000 at the following rates:

§

7.5% on dividend income within the basic rate

band

§

32.5% on dividend income within the higher rate

band

§

38.1% on dividend income within the additional

rate band

§

Personal Allowance: £11,000

§

Basic Rate Limit: £32,000

§

Higher Rate Threshold: £43,000

§

Additional rate band:Over £150,000

o

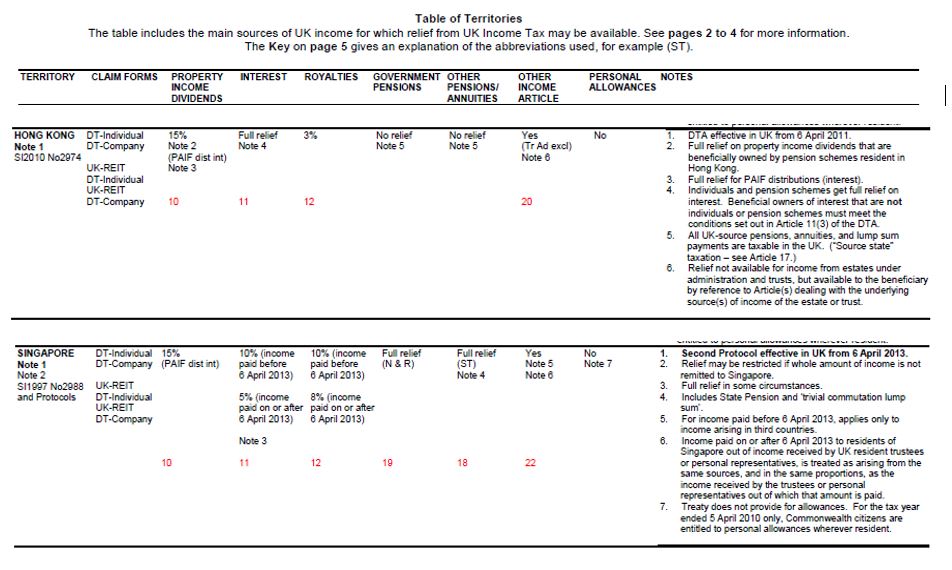

Note wording of the

treaty -2. However, such dividends may also be taxed in the Contracting

State of which the company paying the dividends is a resident and according to

the laws of that State, but if the recipient is the beneficial owner of the

dividends the tax so charged shall not exceed:

§

(a) 5 per cent of the gross amount of the

dividends if the beneficial owner is a company which controls, directly or

indirectly, at least 10 per cent of the voting power in the company paying the

dividends;

§

(b) 15 per cent of the gross amount of the

dividends in all other cases.