Skip to content

Skip to content

Gifting in General

An annual

exclusion giving program is a simple and powerful method to reduce one’s

taxable estate upon death. In general,

an individual with a net worth over $5,250,000 in

2013 (or a married couple whose combined net worth exceeds $10,500,000) can

anticipate that federalestate taxes will be due upon death.

An individual

can give $14,000 each year to as many persons as he or she may choose ($28,000

for a couple). A done may be a child, a

child’s spouse, other family member, or a non-relative. Annual gifts that do not exceed the $14,000

limit are not subject to federalgift tax, and no gift tax return needs to be

filed for such transfers. For most states, annual exclusion gifts often do not

incur state gift taxation because most states do not impose a gift tax.

Annual

exclusion gifts that are made outright to a grandchild or more remote

descendant also do not incur generation-skipping transfer (GST) tax. GST tax may otherwise apply when lifetime

transfers or transfers upon death are made which skip a generation.

The federal

estate tax benefit of a single $14,000 annual exclusion gift can be about

$5,600 (40% tax). Any future

appreciation in value or the accumulation of future income generated by the

property given away is also excluded from the donor’s taxable estate. For residents of the District of Columbia and

Maryland, additional savings of about $1,100 apply because these jurisdictions

impose their own estate tax in addition to the federal estate tax.

A married

couple can effectively double the savings. This can be accomplished with

each spouse, separately each

from their own separate bank account, giving $14,000 each per recipient

(for a total of $28,000). Further, a married couple can use each

individual spouse’s $14,000 annual limit regardless of which spouse actually

owns the transferred money (or property), such as when a jointly held checking

account is used to pay out the gifts from. This is accomplished by the timely filing of a

federal gift tax return signed by both spouses, making the so-called

“split-gift election.” The need for the separate gift tax

return can sometimes be avoided simply by avoiding the use of a jointly held

checking account for gift giving, and using a separately held bank account from

which the gift is made from.

In addition

to the $14,000 annual gift tax exclusion, an individual may directly pay medical

or educational expenses in an

unlimited amount. Such payments are

excluded from the federal gift tax (also avoiding gift and estate taxes in most

states) and do not reduce the $14,000 annual exclusion. If the person

qualifies as your dependent for medical itemized deductions, you may be

entitled to a deduction for the payments as well.

Annual

exclusion gifts may be (and frequently are) made in trust. The trust must be specifically designed to

ensure that annual gifts made in trust continue to qualify for the $14,000

annual exclusion, otherwise an annual gift tax return is required and your

life-time exclusion is depleted. Annual exclusion gifts also may be made

to Educational Section 529 plans to cover college costs for a beneficiary, such

as a grandchild. Special

feature: optionally, via an election made on a gift tax return, five years

of annual exclusion gifts may be made all at one time (i.e., up to $70,000 for

an individual donor in 2013, or up to $140,000 for a married donor electing a

split-gift election) to a Section 529 plan.

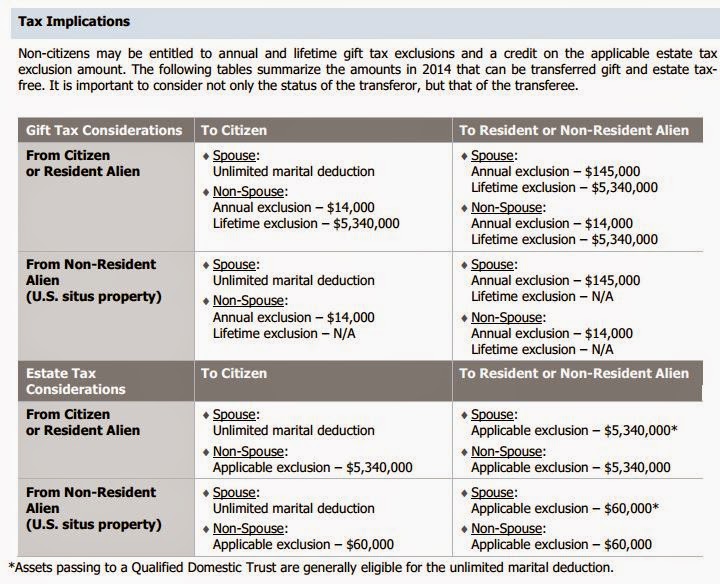

Spousal Gifts

If your

spouse is a U.S. citizen, then due to the unlimited marital deduction you can

gift any amount to your spouse without incurring any federal gift tax or state

gift tax consequences as long as the gift is of a present interest.

If your

spouse isn’t a U.S. citizen, then you are given an annual exclusion from gift taxes for

gifts of a present interest made to your noncitizen spouse. In 2013 the annual exclusion from gift taxes

for gifts made to a noncitizen spouse is $143,000.

In order for

a gift to your spouse to qualify for either the unlimited marital deduction if

your spouse is a U.S. citizen or for the annual exclusion from gift taxes if

your spouse isn’t a U.S. citizen, the gift must be of a “present

interest” in the gifted property. In other words, you need to give the

property entirely over to your spouse for his or her use, enjoyment and

benefit, free from any strings attached.

Contrast this

with a gift of a “future interest” – this is a type of gift with

strings attached, meaning that your spouse won’t have complete use and

enjoyment of the gift until some future point in time. A gift of a future interest doesn’t qualify

for the unlimited marital deduction, the $14,000 annual exclusion from gift

taxes for gifts made to nonspouses, or the $143,000 annual exclusion from gifts

taxes for gifts made to a noncitizen spouse.

A common

example of a gift of a future interest is reserving a life estate for yourself

in a piece of real estate and then when you die your spouse will become the

full and vested owner of the property. Another example is a gift made into a

trust for the benefit of your spouse instead of giving the gift directly to your

spouse – if your spouse doesn’t have the immediate right to use, enjoy and

benefit from the property gifted into the trust, then you’ve made a gift of a

future interest to your spouse.

If you’ve

made a gift of a future interest to your spouse, then regardless of whether or

not your spouse is a U.S. citizen, the entire gift is taxable for gift tax

purposes and must be reported to the IRS on Form 709, United States Gift (and Generation-Skipping

Transfer) Tax Return.

Non Residents

The

Internal Revenue Code (IRC) imposes a tax on the transfer of property by gift [1].

The gift tax applies to both direct and

indirect transfers of real, tangible and intangible property. However, the tax does not apply to a

nonresident taxpayer that is not a citizen of the U.S. unless the property being

transferred is situated within the U.S. at the time of the transfer.

[2]

The tax does not apply to the transfer of intangible property by a person who

is neither a citizen nor a resident of the United States unless such person is

an expatriate who lost his or her citizenship within 10 years of the date of

the transfer. [3] Real and tangible

personal property are generally situated within the U.S. only if they are

physically within the U.S. in a geographic sense. [4] Intangible personal property is located

within the U.S. if it consists of a property right legally enforceable against

a resident of the U.S. or a domestic corporation. [5] Cash, or bank deposits,

are considered tangible personal property.

[6]

Deposits owned by nonresident aliens in United States banks are treated as

property situated outside of the United States if interest from the accounts is

not effectively connected with the conduct of a trade or business within the

United States. [7] Transfers, or gifts,

that a U.S. resident receives from a nonresident alien that exceed $14,139 (for

corporations) or $100,000 (for individuals) annually must be reported on Form

3520.

[ 1] IRC

§2501(a)(1)

[ 2] I RC

§2511(a)

[ 3] Treas.

Reg. §25.2511-1(b)(1)

[ 4] Treas

Reg §25.2511-3(b)(1)

[ 5] Treas

Reg §25.2511-3(b)(2)

[ 6] BLODGETT

V. SI LBERMAN, 227 U.S. 1 (1928);

THOM

AS V. VI RGI NI A, 364 U.S. 443 (1960); Rev. Rul. 55-

143,

1955-1 C.B. 465

[ 7]I RC

§2105(b)(1)